- Retail

- India Packaged Drinking Water Market

India Packaged Drinking Water Market Size, Share, and Growth Forecast 2025 - 2032

India Packaged Drinking Water Market Pack Size (250 mL, 500 mL, 1 L, 1.5 L, 2 L, 5 L, 20 L), Packaging Type (Cups, Pouches, Bottles, Can & Jars), Product Type (Spring Water, Mineral Water), Price Category (Mass, Premium, Luxury), Sales Channel (Off-Trade, On-Trade), City Tier (Tier-1, Tier-2, Tier-3), End-user (Retail Consumers, Corporates, Institutions, Commercial) by Regional Analysis, 2025 - 2032

India Packaged Drinking Water Market Size and Trend Analysis

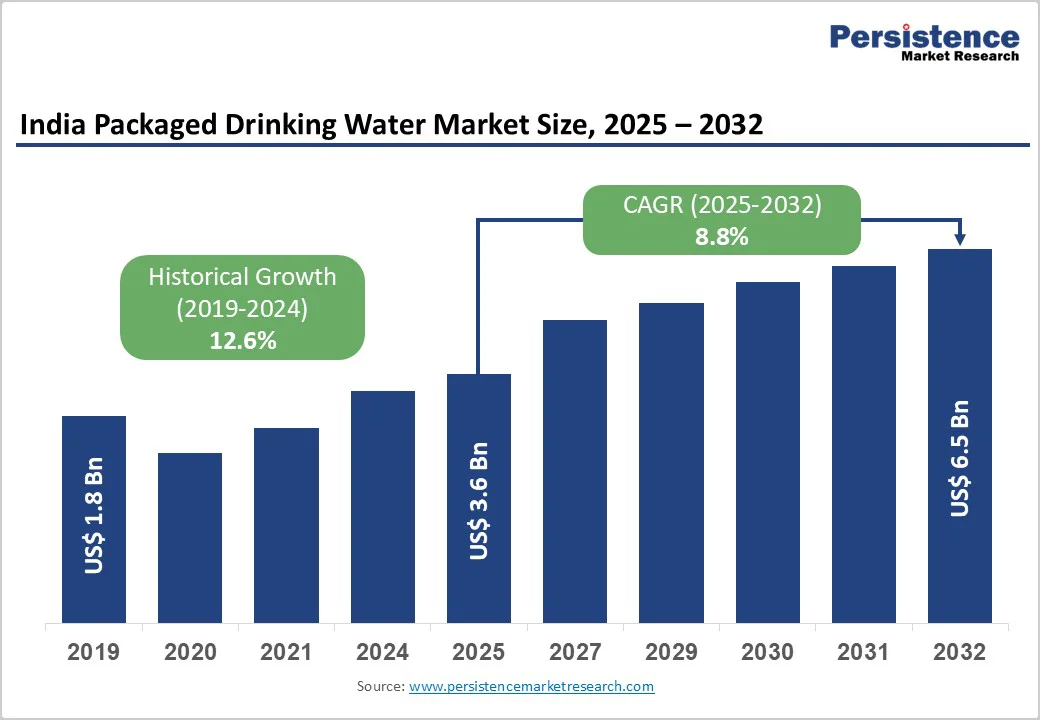

India packaged drinking water market size is likely to value at US$ 3.6 billion in 2025 and is projected to reach US$ 6.5 billion, growing at a CAGR of 8.8% between 2025 and 2032.

Evolving consumer preferences toward safe hydration solutions are driven by health consciousness, rapid urbanization, and persistent concerns about municipal water quality. The demand for packaged drinking water demonstrates India's significant potential as consumers across economic segments prioritize packaged water encouraged by awareness about waterborne diseases affecting approximately 37.5 million Indians annually.

Key Industry Highlights:

- Leading Region: North India leads regional consumption with 35% market share driven by large urban centers, corporate demand, and persistent water quality challenges across Delhi-NCR, UP, and Punjab

- Emerging Region: South India emerges as fastest-growing region with 12.5% CAGR fueled by severe water scarcity, educated consumer base, and thriving IT/tourism sectors demanding premium hydration solutions

- Dominant Pack Size: 1-liter bottles dominate pack size category with 32% market share, offering optimal convenience-value balance for households and individual consumers across urban-rural markets.

- Fastest Growing Price Category: Premium segment demonstrates accelerated growth as health-conscious consumers embrace natural mineral water, alkaline variants, and functional waters commanding 150-300% price premiums over mass alternatives.

- Key Opportunity: Digital commerce and rural penetration represent key growth opportunities with online platforms enabling regional brands to access urban markets while untapped rural areas offer expansion potential.

| Key Insights | Details |

|---|---|

| India Packaged Drinking Water Market Size (2025E) | US$ 3.6 Billion |

| Market Value Forecast (2032F) | US$ 6.5 Billion |

| Projected Growth CAGR (2025 - 2032) | 8.8% |

| Historical Market Growth (2019 - 2024) | 12.6% |

Market Dynamics

Driver - Rising Health Consciousness and Water Quality Concerns

India's packaged drinking water market is experiencing unprecedented growth driven by escalating health awareness and persistent water quality challenges. According to the World Bank, approximately 200,000 people die annually due to inadequate access to safe water, while waterborne diseases impose an economic burden of US$ 600 million annually with 73 million days of lost labor.

The Central Pollution Control Board monitors water quality at 4,294 locations nationwide, revealing that only 33.5% of households in Kerala have access to safe drinking water, representing one of the worst statistics nationally.

Government initiatives like the Jal Jeevan Mission, despite connecting 146 million households, have not fully addressed contamination concerns, particularly in urban areas where 77% of waste is dumped into open landfills without treatment. Consumer confidence in municipal water supplies remains low, with 83% of tap water samples containing microplastics, further driving preference for packaged alternatives.

Rapid Urbanization and Expanding Tourism Industry

India's accelerating urbanization, with over 500 million people expected to live in cities by 2030, represents a fundamental driver of packaged water consumption patterns. Urban centers face acute infrastructure deficits despite government investments exceeding USD 50 billion under various water supply schemes, creating persistent demand for reliable packaged alternatives.

The expanding modern retail infrastructure, including 70,000+ organized retail outlets and growing e-commerce penetration reaching 350 million users, significantly enhances product accessibility across Tier-1, Tier-2, and Tier-3 cities.

The Production Linked Incentive Scheme and Pradhan Mantri Kisan Sampada Yojana are strengthening distribution networks in emerging markets, while rising tourism industry contributions create seasonal demand spikes in popular destinations.

Corporate establishments, including the expanding HoReCa sector and IT industry employing 5.4 million professionals, increasingly rely on packaged water to ensure employee welfare and guest satisfaction, creating stable B2B demand streams.

Restraint - Environmental Sustainability and Plastic Waste Concerns

The packaged water industry faces mounting pressure from environmental concerns, with India generating 9.3 million tonnes of plastic waste annually, of which 3.5 million tonnes are mismanaged and leak into the environment. Single-use plastics, including water bottles, account for 43% of India's total plastic waste despite regulatory bans introduced in 2022.

The informal waste sector handles 60% of plastic waste in unregulated conditions, often exacerbating pollution rather than mitigating it. Consumer awareness about plastic pollution is rising, with 80% of marine litter along India's coastlines comprising plastic waste, creating negative sentiment toward bottled water consumption.

Environmental activists and NGOs increasingly campaign against single-use packaging, while microplastics found in 83% of tap water samples paradoxically highlight the broader water contamination crisis.

Regulatory Compliance and Quality Control Challenges

The packaged water industry operates under increasingly stringent regulatory frameworks that pose significant compliance challenges for manufacturers. The Food Safety and Standards Authority of India (FSSAI) recently classified packaged drinking water as high-risk food, mandating comprehensive testing in FSSAI-approved laboratories and regular quality audits.

New labeling requirements demand detailed product information, including manufacturer details, batch numbers, packaging dates, and FSSAI registration numbers with penalties for non-compliance.

The transition from voluntary BIS certification to mandatory FSSAI licensing creates operational complexities, particularly for smaller manufacturers who struggle with infrastructure investments and testing protocol implementation, potentially limiting market participation and innovation.

Market Opportunities

Premium and Functional Water Segment Expansion

The premium packaged water segment presents exceptional growth opportunities, with consumer preferences shifting toward natural spring water, alkaline water, and functional beverages with added electrolytes and vitamins. Premium brands emphasize glacier-sourced, mineral water, and high-mineral-content varieties command 200-400% price premiums over mass market alternatives, appealing to health-conscious consumers seeking enhanced hydration experiences.

The alkaline water market specifically demonstrates strong growth potential as consumers increasingly associate higher pH levels with health benefits, while functional water incorporating vitamins, electrolytes, and natural flavors addresses specific wellness needs. The segment benefits from celebrity branding initiatives where notable personalities endorse premium water brands, creating aspirational appeal and driving brand differentiation in competitive markets.

E-commerce and Digital Distribution Channel Development

The rapid digitization of India's retail landscape creates unprecedented opportunities for packaged water market expansion beyond traditional urban strongholds. Online sales channels through platforms like Amazon, BigBasket, Zepto, and Blinkit provide instant access to regional brands while enabling subscription models for recurring purchases.

Rural market penetration represents significant untapped potential, with 68% of India's population residing in rural areas where unorganized market players currently dominate through local manufacturing and distribution networks.

The BeverageCart mobile app and similar platforms address last-mile delivery challenges for the HoReCa sector, while direct-to-consumer (D2C) initiatives enable brands to gather valuable consumer insights and implement targeted marketing campaigns.

Chilled drinking water vending machines in high-traffic locations including railway stations, airports, and shopping centers create convenient access points while reducing packaging waste through refillable container systems.

Category-wise Insights

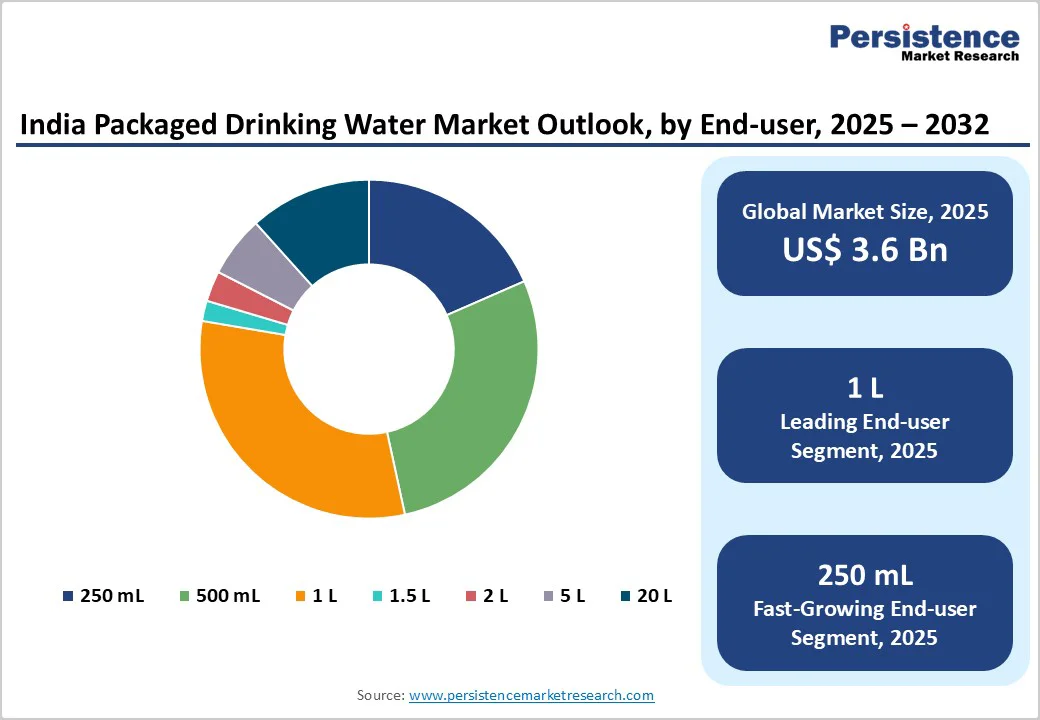

Pack Size Analysis

The 1-liter bottle segment dominates the India packaged drinking water market, commanding approximately 32% market share due to optimal balance between convenience and value proposition. This segment appeals to both individual consumers and households seeking cost-effective hydration solutions for daily consumption. The 500 mL bottles represent the second-largest segment, preferred by on-the-go consumers, office workers, and travelers prioritizing portability.

Small pack sizes (250 mL) capture 18% market share, primarily driven by impulse purchases at retail outlets, schools, and transportation hubs where affordability and convenience intersect. The 20-liter bulk segment holds significant market share, serving corporate offices, households, and institutions requiring large-volume water supply through home and office delivery services.

Premium segments including 1.5-liter and 2-liter bottles account for the remaining market share, appealing to families and health-conscious consumers seeking enhanced hydration experiences.

Packaging Type Analysis

Bottles overwhelmingly dominate the packaging type category, with PET bottle representing approximately 78% market share due to lightweight properties, durability, cost-effectiveness, and extensive recycling infrastructure. The segment benefits from technological innovations in PET manufacturing, including the development of bio-paraxylene bottles from used cooking oil by companies like Suntory, reducing carbon emissions compared to petroleum-based materials.

Glass bottles constitute 12% market share, experiencing rapid growth at 11.5% CAGR driven by premium positioning and environmental consciousness among affluent consumers. This segment particularly resonates with hospitality establishments and health-conscious consumers who associate glass packaging with purity and sustainability.

Pouches account for small but significant market share, primarily popular in rural and semi-urban markets due to affordability and local manufacturing capabilities. Cans and jars are emerging as innovative packaging solutions for large volume requirements.

Price Category

The mass market segment commands approximately 87% market share, driven by price-sensitive consumers across urban and rural markets seeking affordable hydration solutions without compromising basic quality standards. This segment faces intense competition from regional players and private labels implementing aggressive pricing strategies, creating margin pressures for established national brands while expanding market accessibility.

The premium segment represents a small share but demonstrates exceptional growth potential as rising disposable incomes and health consciousness drive consumer willingness to pay higher prices for perceived quality benefits. Premium brands successfully justify 150-300% price premiums through superior sourcing narratives, innovative packaging, and celebrity branding initiatives that create aspirational appeal and brand differentiation.

The luxury segment accounts for a little market share, targeting affluent consumers and hospitality establishments where price sensitivity is minimal and status signaling drives purchasing decisions. Luxury water brands employ limited distribution tactics to maintain exclusivity while commanding impressive margins that fund extensive marketing and brand-building initiatives focused on premium positioning and lifestyle association.

Sales Channel Analysis

The off-trade segment dominates with 85% market share, encompassing supermarkets, hypermarkets, convenience stores, and traditional retail outlets that provide widespread accessibility across India's diverse retail landscape.

Supermarkets and hypermarkets lead within off-trade channels with 42% segment share, offering convenience for bulk purchases, brand comparison shopping, and promotional activities preferred by urban consumers. Convenience stores and mini markets capture 28% off-trade share in high-traffic locations including transportation hubs, office complexes, and residential areas where impulse purchases and immediate consumption drive sales patterns.

The on-trade segment represents remaining market share, comprising restaurants, cafes, hotels, and entertainment venues where premium positioning and experiential consumption justify higher margins and brand differentiation opportunities.

Online sales channels are experiencing accelerated growth, particularly post-COVID-19, with brands partnering with delivery platforms to expand digital reach and capture tech-savvy consumers seeking convenience and doorstep delivery services.

Product Type Analysis

Mineral water commands 82% market share in the product type category, embodying the core packaged drinking water segment processed via filtration, purification, and mineral enhancement to comply with Bureau of Indian Standards (BIS) norms.

It caters to mass consumers with affordable, reliable options from leaders like Bisleri, Kinley, and Aquafina, leveraging vast distribution, economies of scale, and robust FSSAI-aligned quality to fend off premium rivals through pricing and marketing.

Natural spring water holds the remaining share yet surges at 13% CAGR, attracting health-focused buyers with premium, minimally processed purity from protected sources. Brands such as Himalayan, Evian, and Volvic charge 300-500% premiums, thriving on urban affluence, sourcing transparency, and lifestyle endorsements.

City Tier Analysis

Tier-1 cities command 58% market share in packaged drinking water consumption, led by metros like Mumbai, Delhi, Bangalore, Chennai, Kolkata, and Hyderabad, where dense populations, corporate hubs, and affluent buyers fuel demand across segments.

Advanced retail, with modern trade, and premium preferences for glass-bottled or spring water, thrive on health and eco-awareness, alongside 18% e-commerce penetration versus the national average penetration of 8%.

Demand for packaged drinking water in Tier-2 cities such as Indore, Ahmedabad, and Jaipur boosted by rising incomes, retail expansion, and tourism, while in Tier-3 towns demand is propelled by urbanization and quality concerns. In these cities, a balanced mass-premium uptake favors 1 L and 500 mL packs, supported by local brands' pricing edge.

End-user Analysis

Retail consumers constitute the largest end-user segment with approximately 68% market share, driven by household consumption, individual hydration needs, and growing health consciousness across demographic segments. This segment benefits from expanding retail infrastructure, diverse pack size options, and increasing affordability of packaged water relative to income levels.

Corporate establishments represent the second largest market share, including office buildings, business centers, and commercial complexes requiring reliable water supply for employee welfare and guest services.

The institutional segment encompasses hospitals, educational institutions, government buildings, and healthcare facilities where water quality standards are non-negotiable.

Commercial end-users, including event organizers, wedding planners, and conference facilities, also hold a commendable market share but usually show seasonal demand, requiring bulk supply for specific occasions and events. This segmentation reflects India's diversifying economy and the universal necessity of safe drinking water across all sectors.

Regional Insights

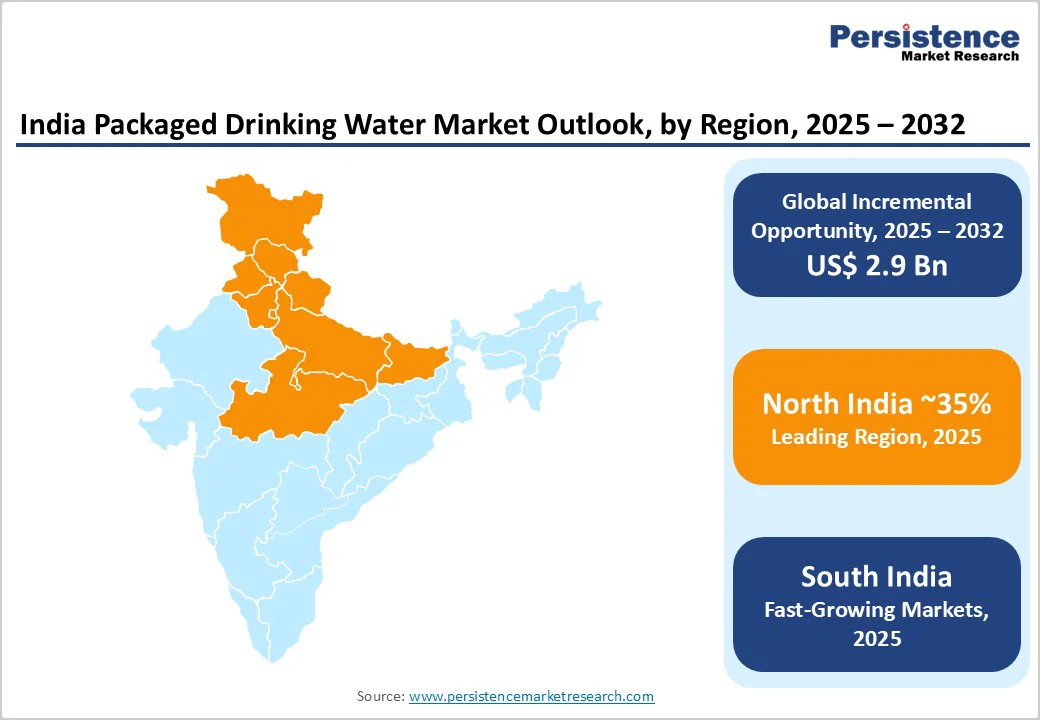

North India Packaged Drinking Water Market Trends

North India dominates the packaged drinking water market, accounting for approximately 35% national market share, driven by large population centers including Delhi-NCR, Uttar Pradesh, Punjab, Haryana, and Rajasthan. The region benefits from robust economic activity, extensive corporate presence, and significant tourism infrastructure that generates substantial demand from offices, hotels, restaurants, and households.

Delhi-NCR alone represents a billion-dollar opportunity due to persistent municipal water quality issues, high population density, and an affluent consumer base willing to pay premium prices for safe hydration. The region faces acute water quality challenges, with groundwater in one-third of districts containing fluoride, iron, salinity, and arsenic levels exceeding permissible limits, creating a strong preference for packaged alternatives.

South India Packaged Drinking Water Market Trends

South India represents the fastest-growing regional market with a 12.5% CAGR growth driven by rapidly deteriorating water levels and persistent drought conditions. Kerala demonstrates the most critical water situation, with only 33.5% of households having access to safe drinking water, creating urgent demand for packaged alternatives. Tamil Nadu faces severe groundwater depletion and major reservoir drought, forcing both urban and rural populations toward bottled water consumption.

The region exhibits strong premium consumption trends, with South Indian consumers demonstrating higher willingness to pay for natural mineral water, alkaline water, and functional beverages. Corporate demand is particularly robust, driven by the region's thriving IT sector, manufacturing hubs, and medical tourism industry, requiring a reliable water supply for international clients and employees.

Tourism infrastructure in states like Kerala, Karnataka, and Tamil Nadu generates significant seasonal demand, with hospitality establishments increasingly offering premium bottled water as differentiated guest services.

West India Packaged Drinking Water Market Trends

West India demonstrates exceptional growth potential with the highest dollar opportunity, driven by higher disposable incomes, industrial expansion, and proactive hospitality sustainability programs.

The region, encompassing Maharashtra, Gujarat, Rajasthan, and Goa, benefits from robust economic infrastructure, established manufacturing sectors, and significant industrial water demand. Mumbai and Pune represent major consumption centers due to dense urban populations, extensive corporate presence, and well-developed retail infrastructure supporting premium brand penetration.

Gujarat showcases strong regional brand loyalty with local champions such as Aava thriving through community-driven distribution networks and trust-based marketing approaches.

The region's industrial sector creates substantial B2B demand, with manufacturing facilities, chemical plants, and textile industries requiring safe drinking water for employee welfare and operational needs. Goa's tourism industry generates significant seasonal demand fluctuations, with hospitality establishments requiring premium packaged water for domestic and international tourists.

Competitive Landscape

India packaged drinking water market exhibits a consolidated competitive structure with the top three brands controlling over 50% market share, led by Bisleri, Kinley, and Aquafina.

This concentration reflects strong brand equity, extensive distribution networks, and significant barriers to entry for new competitors. However, approximately 45% of the overall market belongs to regional and small players, demonstrating that local distribution capabilities can effectively compete with national brands.

The market structure favors companies with comprehensive distribution networks spanning thousands of outlets, from urban supermarkets to rural kiranas, highlighting the infrastructure-intensive nature of the business.

Key differentiators employed by market leaders include aggressive advertising campaigns, premium product portfolios, sustainable packaging initiatives, and strategic partnerships with regional manufacturers for expanded geographical coverage.

Emerging business model trends include direct-to-consumer channels, subscription services, online marketplace partnerships, and corporate bulk supply contracts that provide recurring revenue streams and enhanced customer relationships.

Key Market Developments

- October 2025: Reliance Consumer Products Ltd. (RCPL) launched Campa Sure bottled water, entering direct competition with market leaders through aggressive pricing strategy offering 250mL bottles at INR 5 and 1-liter packs at INR 15, representing 20-30% cost savings compared to established competitors, with initial rollout across northern India.

- March 2024: Energy Beverages (Clear Premium Water) expanded HoReCa client base to 1,600 establishments, representing significant growth from 90 clients in 2020, demonstrating strong premium segment expansion and successful B2B market penetration strategies.

Companies Covered in India Packaged Drinking Water Market

- Bisleri International Pvt. Ltd.

- Coca-Cola India (Kinley)

- PepsiCo India (Aquafina)

- Mulshi Agro Products

- Aava Water

- Qua (Narang Group)

- Himalayan & Tata Copper+ (Tata Consumer Products)

- Acquafina

- Oxyrich (Manikchand)

- Bailley (Parle Agro)

- Evian (Danone)

- Voss

- Evocus

- Kingfisher (UBL)

- Rail Neer (IRCTC)

- Nestle Pure Life

- Reliance (Campa Sure)

- Catch (DS Group)

Frequently Asked Questions

The India packaged drinking water market is projected to reach US$ 6.5 billion by 2032, growing from US$ 3.6 billion in 2025 at a CAGR of 8.8% during the forecast period.

Key demand drivers include escalating health consciousness, persistent water quality concerns affecting 37.5 million Indians annually, rapid urbanization with 500+ million urban population by 2030, and expanding modern retail infrastructure enhancing product accessibility.

The 1-liter bottle segment dominates with approximately 32% market share, offering optimal convenience-value balance for households and individual consumers across urban and rural markets.

South India emerges as the fastest-growing region with 12.5% CAGR driven by severe water scarcity, educated consumer base, and thriving IT/tourism sectors demanding premium hydration solutions.

Major opportunities include premium and functional water segment expansion, digital commerce and rural market penetration, and sustainable packaging solutions addressing environmental consciousness among urban consumers.

Key market players include Bisleri International, Coca-Cola's Kinley, PepsiCo's Aquafina, with the top three brands controlling over 50% of the organized market.