- Industrial Goods & Service

- India Industrial Racking System Market

India Industrial Racking System Market Size, Share, and Growth Forecast, 2026 - 2033

India Industrial Racking System Market by Design (Selective Racking, Cantilever Racking, Push Back Racking, Narrow & Wide Aisle Racking, Drive-In Racking, Pallet Flow Racking, Carton Flow Racking, Mobile Racking, Rack Supported Warehouse, Misc.), Carrying Capacity (Light Duty (40 to 200 kg), Medium Duty (0.25 to 1 Ton), Heavy Duty (2-4 Tons).), Ownership (Direct Ownership, Rentals), Industry, and Regional Analysis for 2026 - 2033

India Industrial Racking System Market Size and Trends Analysis

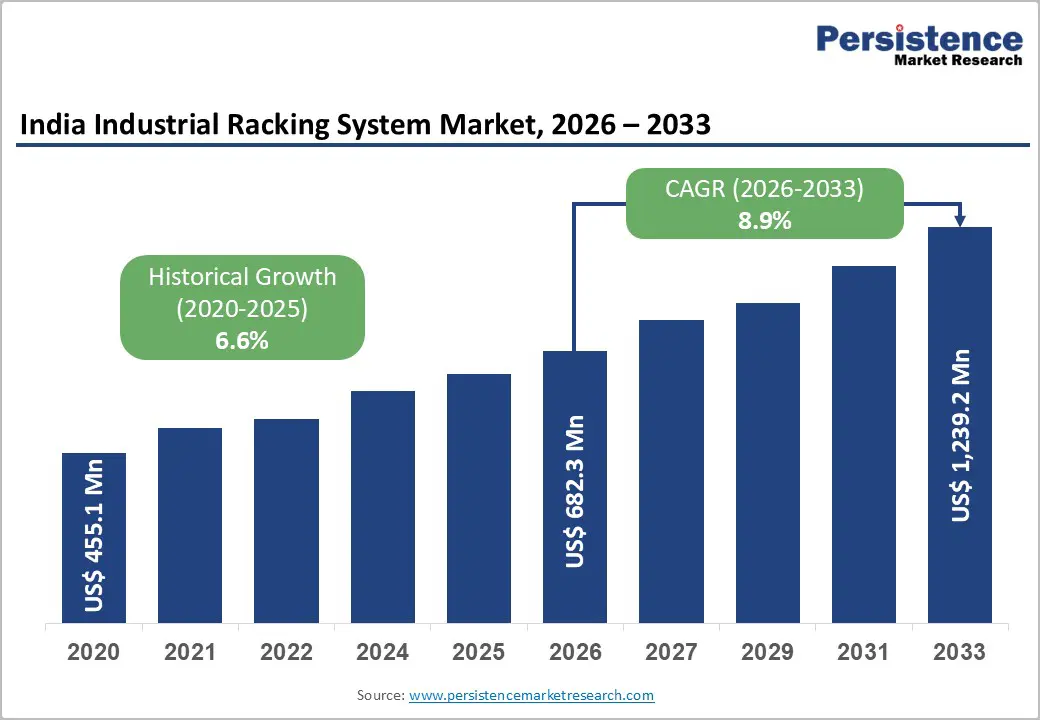

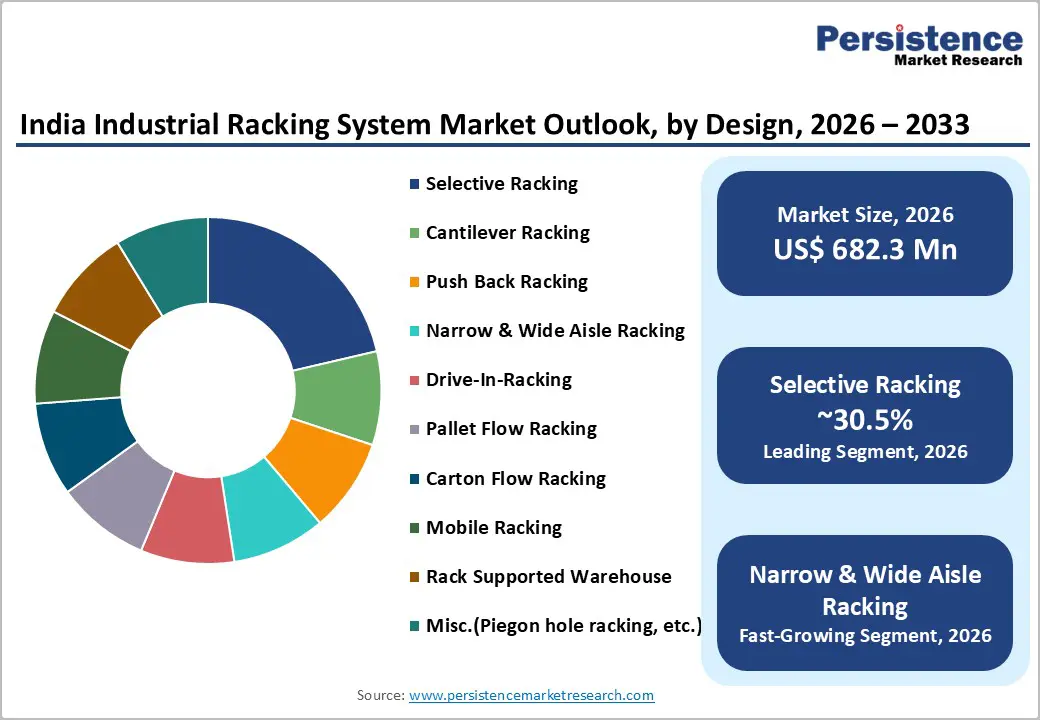

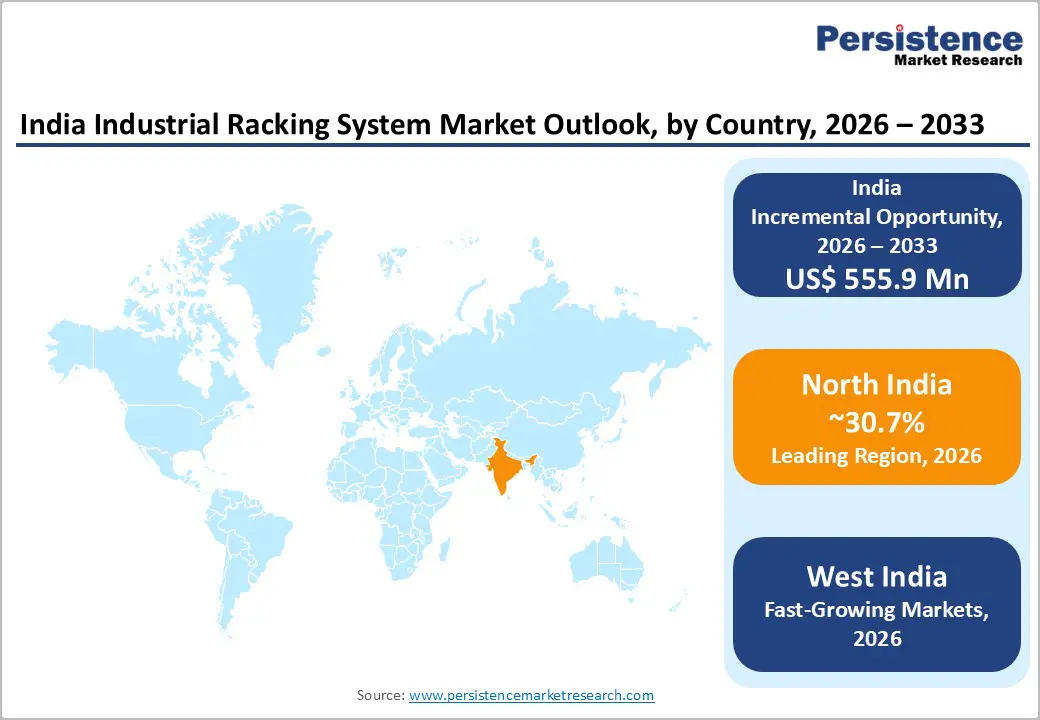

India industrial racking system market size is likely to be valued at US$ 682.3 million in 2026 and is projected to reach US$ 1,239.2 million by 2033, growing at a CAGR of 8.9% between 2026 and 2033. The warehousing and logistics sector's share of India's economy surged from 2 percent in 2020 to nearly 20 percent in 2021, establishing the foundation for sustained demand across industrial storage infrastructure.

Industrial and warehousing segment leasing reached a record 39.5 million square feet in 2024, with 3PL operators commanding 41 percent of total demand, while e-commerce platforms captured an expanding 25 percent market share. Strategic government policy interventions, including the Production Linked Incentive (PLI) schemes, the National Logistics Policy, and the PM Gati Shakti multimodal infrastructure programme, create systemic demand for modernised, technology-enabled storage solutions across manufacturing, distribution, and fulfilment applications.

Key Industry Highlights:

- Leading Design Segment: Selective racking systems lead the design segment with a 29.4% market share, driven by versatility, forklift accessibility, and broad applicability across industries.

- High-Value Leading Carrying Capacity: Medium-duty racking accounts for 50.4% of carrying capacity, aligning with mainstream applications in e-commerce, retail, pharmaceuticals, and general manufacturing.

- Leading Industry: 3PL operators are the largest end-use segment with 34.1% share, fueling demand for modular, scalable, and technology-integrated racking solutions.

- Fastest-Growing Industry: E-commerce expansion and last-mile fulfilment are key growth drivers, driving demand for flexible, high-rotation storage systems across India’s logistics hubs.

- Growth Opportunity: Cold chain infrastructure and warehouse automation investments create premium opportunities, with temperature-controlled and technology-integrated racking solutions catering to pharmaceuticals, food processing, and high-value goods.

- Fast Growing Design Segment: Narrow and wide-aisle racking systems are the fastest-growing designs, supporting space optimisation and automation integration in high-density urban warehouses.

| Key Insights | Details |

|---|---|

| India Industrial Racking System Market Size (2026E) | US$ 682.3 Mn |

| Market Value Forecast (2033F) | US$ 1,239.2 Mn |

| Projected Growth (CAGR 2026 to 2033) | 8.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.6% |

Market Dynamics

Drivers - E-Commerce Penetration and Last-Mile Fulfilment Infrastructure Requirements

India's e-commerce sector has transitioned from an initial growth phase to rapid scale-up, with the market valued at approximately US$125 billion in 2024 and projected to reach US$345 billion by 2030 and US$550 billion by 2035. This expansion is accompanied by a fundamental transformation in consumption patterns: tier-2 and tier-3 cities now account for e-commerce order volumes of 55 percent or more, reflecting digital adoption among nearly one billion internet and smartphone users.

During H1 2025, e-commerce platforms leased 4.5 million square feet of warehousing space across India's eight primary logistics markets, representing sustained demand for flexible, space-efficient industrial racking systems. The rise of quick commerce platforms, direct-to-consumer brands, and subscription-based retail models creates recurring demand for reconfigurable storage infrastructure capable of supporting rapid inventory rotation and multi-SKU fulfilment operations.

These operational characteristics favour selective racking systems that offer direct forklift access, narrow-aisle configurations that maximise vertical space utilisation, and mobile racking solutions that enable rapid facility reconfiguration. India's industrial racking system market directly benefits from warehousing density optimisation, as e-commerce operators prioritise reducing cost-per-unit-storage while maintaining order fulfilment velocity. Storage system sophistication encompassing selective racking for standard pick operations, narrow-aisle systems for constrained urban facilities, and mobile configurations for multi-tenant logistics parks establishes sustained demand trajectories across end-use segments.

Third-Party Logistics Sector Expansion and Supply Chain Decentralization

The 3PL sector has emerged as the dominant driver of warehousing demand. A CBRE study indicates that 70 percent of Asia-Pacific occupiers expect to expand logistics operations in India within the next two years, positioning India as the most attractive 3PL expansion market in the Asia-Pacific region. Between 2021 and H1 2025, 3PL providers accounted for 40-50 percent of total warehouse leasing activity, particularly in strategic hubs such as Delhi-NCR, Mumbai, and Bengaluru. This sector leadership reflects multiple underlying drivers: supply chain diversification strategies implemented under "China+1" sourcing paradigms; the acceleration of nearshoring of manufacturing operations from developed markets; the expansion of consumer goods distribution networks; and specialised logistics requirements arising from the pharmaceutical, automotive, and electronics sectors. 3PL operators are increasingly adopting multi-tenanted warehouse formats, enabling rapid facility scaling while reducing capital intensity and diversifying customer risk profiles.

Complementing this infrastructure expansion is systematic adoption of warehouse management software, IoT sensors, robotic picking systems, automated storage and retrieval systems (AS/RS), and goods-to-person solutions. These technology investments establish sustained demand for advanced, modular, and automation-compatible racking system configurations that support space optimisation, real-time inventory visibility, and labour-efficiency objectives.

The India Industrial Racking System Market's 3PL-driven growth reflects this sector's capital intensity and infrastructure modernisation imperatives, as operators compete on service velocity, cost efficiency, and supply chain transparency.

Restraint - High Initial Capital Investment and Infrastructure Development Costs

The deployment of advanced industrial racking systems, particularly selective racking configurations for heavy-duty applications and automation-integrated solutions, requires substantial upfront capital investment, with comprehensive facility solutions frequently exceeding 10 million rupees for warehouse capacities exceeding 100,000 square feet.

Metropolitan warehousing costs have surged 15-18% annually across Mumbai, Bengaluru, and Delhi-NCR regions over the past two years, driven by limited land availability, rising property acquisition expenses, and heightened competition for premium logistics real estate.

Grade A warehousing standards increasingly mandated by multinational corporations and large-scale e-commerce operators demand investment in high-specification construction, advanced automation systems, environmental controls, and digital infrastructure, compounding capital requirements. Smaller and mid-sized enterprises, particularly regional 3PL operators and specialized logistics providers, face capital-constrained conditions that limit facility modernization timelines, creating bifurcated market dynamics between well-capitalized multinational operators and resource-constrained domestic competitors.

Opportunity - Tier-2 and Tier-3 City Geographic Expansion and Regional Supply Chain Resilience

Tier-2 and tier-3 cities have emerged as the fastest-growing segments of the logistics infrastructure sector in India, capturing 36 percent of new warehousing lease volumes in 2024, a dramatic acceleration from 22 percent in 2021. These cities offer compelling competitive advantages: warehousing land costs are 30 to 60 percent lower than in metropolitan locations, reducing per-unit-space capital requirements; truck turnaround times are substantially shorter due to lower congestion; and growing consumption in these regions, driven by digital adoption and rising discretionary spending, creates local fulfilment demand.

Strategic infrastructure investments, including dedicated freight corridor connections, multimodal logistics park development in cities including Varanasi, Kanpur, Nagpur, and Vijayawada, and highway upgrades under Bharat Mala create competitive logistics advantages.

Each large-format warehouse, such as 50,000 plus square feet, established in tier-2/3 cities generates 150 to 200 direct employment positions and 250+ indirect jobs, addressing regional labour market opportunities and attracting government policy support.

India's industrial racking system market benefits substantially from this geographic diversification through greenfield opportunities in emerging logistics hubs. Regional specialization opportunities are emerging across textiles, pharmaceuticals, automotive, and food processing clusters, where concentrated industrial activity creates demand for specialised racking configurations addressing sector-specific requirements.

Tier-2/3 city warehousing typically incorporates modular, scalable storage systems enabling rapid facility expansion and reconfiguration, driving demand for flexible racking designs, including selective systems, mobile solutions, and carton flow systems. Government initiatives supporting regional industrial development create policy tailwinds for infrastructure investors, enabling accelerated deployment of integrated storage solutions.

As businesses optimise supply chain footprints to balance cost efficiency with fulfilment velocity, tier-2/3 city expansion represents a distinct growth vector for industrial racking system manufacturers that can offer standardised, cost-optimised, rapidly deployable solutions.

Automation Integration and Cold Chain Infrastructure Development

India's warehouse automation market is undergoing a significant transformation with systematic adoption of automated storage and retrieval systems (AS/RS), robotic picking, autonomous guided vehicles, and software orchestration platforms addressing labour cost pressures, order accuracy requirements, and operational efficiency imperatives. Approximately 70% of Indian warehouse decision-makers planned to adopt automation by 2024, with semi-automated systems accounting for 48.6% of the automation market, indicating a pragmatic approach that combines cost-effectiveness with productivity gains.

Picking and sorting automation accounted for 34.1 percent of 2025 automation spending, while transportation and AGV/AMR solutions are expanding at a 26.9 percent CAGR, reflecting end-to-end supply chain orchestration initiatives.

India's food processing sector, valued at US$354.5 billion in 2024 and projected to reach US$535 billion by FY26, is driving substantial cold chain infrastructure investment, estimated at INR16,000-INR 21,000 crore through modernisation initiatives. Cold storage capacity currently stands at 37-39 million tonnes across 7,645 facilities, with significant capacity and technology gaps creating expansion opportunities.

Government initiatives, including Pradhan Mantri Kisan SAMPADA Yojana, the Agriculture Infrastructure Fund, and steel silo modernisation projects, are accelerating cold chain development in states including Telangana, reducing post-harvest spoilage, and supporting agricultural value addition.

The Indian industrial racking system market directly benefits from cold chain expansion, as specialised storage systems are required. Temperature-controlled environments require precise racking configurations that support modular expansion, are durable in high-moisture environments, and integrate with environmental monitoring systems. Pharmaceutical sector growth, driven by global outsourcing, stringent regulatory standards, and export-oriented manufacturing, creates additional specialized racking requirements for batch-tracked, compliant storage systems. These opportunities for automation and cold-chain convergence establish distinct premium market segments for advanced racking system providers capable of offering technology-integrated, sector-specific solutions aligned with regulatory requirements and operational efficiency objectives.

Category-wise Analysis

Design Insights

Selective racking systems account for the largest share of the design segment at 29.4%, reflecting their versatility, accessibility, and suitability for diverse industrial applications. These systems provide direct forklift access to each pallet from multiple directions, enabling straightforward inventory management, rapid stock rotation, and flexible product mix accommodation, critical requirements across automotive components, food & beverage products, pharmaceutical inventories, and retail merchandise distribution.

Selective racking systems maintain operational simplicity through the utilisation of standard material handling equipment, minimising training requirements and enabling rapid deployment across facilities with varying technical expertise levels.

The segment's dominance is reinforced by its universal applicability across end-use industries and facility types. From e-commerce fulfilment centres requiring rapid order processing to manufacturing-attached warehouses supporting just-in-time inventory models, selective racking systems deliver the optimal balance between storage density and accessibility. This broad applicability establishes selective racking as the default technology for general-purpose storage, supporting sustained market share leadership across the forecast period. Market adoption is further supported by the segment's cost-effectiveness relative to specialised storage systems, enabling widespread deployment across small and medium-sized operators, regional manufacturers, and organised retail networks.

Narrow and wide-aisle racking systems achieve the fastest growth momentum within the design segment, driven by intensifying space utilisation imperatives in high-value urban real estate and automation integration trends. These systems enable vertical storage-density optimisation through aisle width reduction to 1.5 to 1.8 meters compared to standard 3.5 plus meter aisles characteristic of selective racking, while maintaining accessibility through specialised handling equipment, including narrow-aisle trucks and vertical lift modules. Space utilisation efficiency reaches 50-55%, compared with approximately 40% for standard selective configurations, providing compelling financial justification for capital-constrained metropolitan operators seeking to maximise warehouse footprint productivity.

Carrying Capacity Insights

Medium-duty racking systems, accommodating payload capacities between 250 kilograms and 1 ton, command the 50.4% of the Indian Industrial Racking System Market. This dominance reflects the segment's alignment with mainstream industrial applications across organised retail, e-commerce fulfilment, food & beverage distribution, pharmaceutical warehousing, and general manufacturing. Medium-duty configurations optimise the cost-benefit trade-off between structural investment and payload capacity, enabling widespread deployment across diverse facility types without requiring specialised engineering or premium materials.

The segment benefits from India's expanding e-commerce sector, which predominantly handles consumer packaged goods, apparel, consumer electronics, and food products commodities typically within medium-duty capacity specifications. 3PL operators, rely heavily on medium-duty systems to support multi-customer operations within shared warehouse footprints, as this capacity range accommodates the majority of pallet and carton configurations across customer portfolios.

Industry Insights

3PL operators hold the largest share of the end-use segment in the India Industrial Racking System Market, reflecting this sector's emergence as the primary driver of demand for industrial warehousing infrastructure. 3PLs accounted for 34.1% of the industry segment, establishing themselves as dominant customers for tracking system manufacturers. The segment's prominence creates systematic influence over storage system design evolution, such as 3PLs prioritizing standardization, modular design architecture, technology integration, and scalable infrastructure enabling efficient multi-customer operations within shared warehouse facilities.

3PL sector growth is underpinned by multiple structural drivers: supply chain diversification strategies, manufacturing decentralization, e-commerce fulfilment requirements, and supply chain resilience investments. Multi-tenanted warehouse formats increasingly adopted by 3PLs require flexible, modular racking systems capable of supporting rapid facility reconfiguration as customer requirements evolve. Quick-commerce platforms, subscription-based e-commerce services, and tier-2/3 city fulfilment operations are driving geographic expansion and multiplying warehouse footprints, creating substantial capital requirements for racking system investment.

Government initiatives emphasising logistics modernisation and the National Logistics Policy establish policy tailwinds supporting 3PL sector expansion, directly translating into sustained demand within the Indian Industrial Racking System Market.

Competitive Landscape

India's industrial racking system market is moderately consolidated with a mix of global engineering majors and strong regional specialists competing across product design, customisation, and after-sales services. International players such as Kardex AG, Jungheinrich AG, SSI Schaefer, Daifuku Co., Ltd., and Gonvarri Material Handling offer advanced automation, engineered storage solutions, and established supply chains, serving large institutional and industrial clients. At the same time, domestic and regional firms like Godrej Group, Nilkamal Material Handling, Delta Storage Systems Pvt. Ltd., and SILVER LINING Storage Solutions leverage local market knowledge, cost-competitiveness, and quicker deployment for SMEs, 3PLs, and manufacturing segments.

The industry exhibits competitive fragmentation beyond the top tier, with smaller players such as Storewel Racking & Shelvings, Giraffe Storage Solutions, and Storage Technologies & Automation Pvt. Ltd. addressing niche requirements and specialized installations. While the leading players generally command a significant share in high-end and automated racking systems, the long tail remains competitive due to price sensitivity and customization needs in India’s diverse industrial base.

E-commerce platforms achieve rapid growth as an end-use segment within the India Industrial Racking System Market, driven by explosive sector expansion and evolving fulfilment infrastructure requirements. The e-commerce market's projected growth from US$125 billion in 2024 to US$345 billion by 2030 creates systematic demand for new warehouse facilities, fulfilment centre networks, and return management infrastructure. H1 2025 warehouse leasing data indicates e-commerce operators captured 25% of total leasing activity across eight major cities, establishing this sector as the second-largest demand driver after 3PLs.

The rise of quick-commerce platforms, requiring hyperlocal fulfilment network density, creates distinct racking requirements distinct from traditional e-commerce distribution centers. Dark stores and micro-fulfilment centres, typically 5,000 to15,000 square feet, require compact, densified storage systems supporting rapid inventory rotation and piece-pick operations

As India's e-commerce sector matures and supply chain sophistication advances, specialised racking requirements for automation integration, climate control, and real-time inventory visibility become increasingly critical, positioning e-commerce as the fastest-growing end-use segment within the India Industrial Racking System Market.

Key Industry Developments

- In October 2025, Godrej Enterprises Group: The Storage Solutions business of Godrej Enterprises Group received CE certification from TÜV NORD for its indigenously developed Mobile Pallet Racking (MPR) System, marking a major engineering milestone. This certification validates compliance with stringent European safety and machinery standards, showcasing India’s capability in advanced intralogistics and high-density storage technologies. The achievement enhances global market access for Indian-made racking systems, strengthening competitiveness and export potential in the industrial racking space.

- In October 2025, Palladium Dynamics strengthened its presence in the Indian Industrial Racking System market by launching advanced heavy-duty industrial racks. The company focuses on engineered, safety-compliant, and space-optimised storage solutions designed to enhance efficiency and scalability in Indian factories, warehouses, and logistics centers.

Companies Covered in India Industrial Racking System Market

- Kardex AG

- Jungheinrich AG

- Allied Technical Services L.L.C

- Storewel Racking & Shelvings

- Daifuku Co., Ltd.

- SSI Schaefer

- Gonvarri Material Handling

- Godrej Group

- Nilkamal Material Handling

- SILVER LINING Storage Solutions

- Delta Storage Systems Pvt. Ltd.

- Giraffe Storage Solutions

- Storage Technologies & Automation Pvt. Ltd. (Racks & Rollers)

- Sadr Logistics Co.

- SNR International Services LLC

- ACROW.LTD

Frequently Asked Questions

India Industrial Racking System Market is projected to be valued at US$ 682.3 Mn in 2026.

The selective racking segment is expected to account for approximately 29.4% of India industrial racking system market by design in 2026.

India industrial racking system market is expected to witness a CAGR of 8.9% from 2026 to 2033.

Growth of the India Industrial Racking System Market is driven by rapid e-commerce expansion, last-mile fulfilment requirements, and 3PL sector growth, creating strong demand for flexible, modular, and automation-compatible racking solutions.

Key market opportunities in the India Industrial Racking System Market lie in Tier-2 and Tier-3 city expansion, regional supply chain resilience, and growth in automated and cold chain-enabled warehousing supporting modular, flexible, and sector-specific racking solutions.

Key players in the Industrial Racking System Market include Kardex AG, Godrej Group, Nilkamal Material Handling, Delta Storage Systems Pvt. Ltd., Jungheinrich AG, SSI Schaefer, Daifuku Co., Ltd., and Gonvarri Material Handling.