- Processed Food

- Hot Sauce Market

Hot Sauce Market Size, Share, and Growth Forecast, 2026 - 2033

Hot Sauce Market by Packaging Format (Glass Bottles, Plastic Squeeze Bottles, Pouches, Single-Serve Sachets, Bulk Drums), Product Type (Condiment Sauces, Cooking Sauces & Marinades, Specialty/Artisan/Craft Sauces, Functional Sauces, Others), Distribution Channel (Supermarkets & Hypermarkets, Online Retail, Foodservice Outlets, Specialty & Gourmet Stores), and Regional Analysis for 2026 - 2033

Hot Sauce Market Share and Trends Analysis

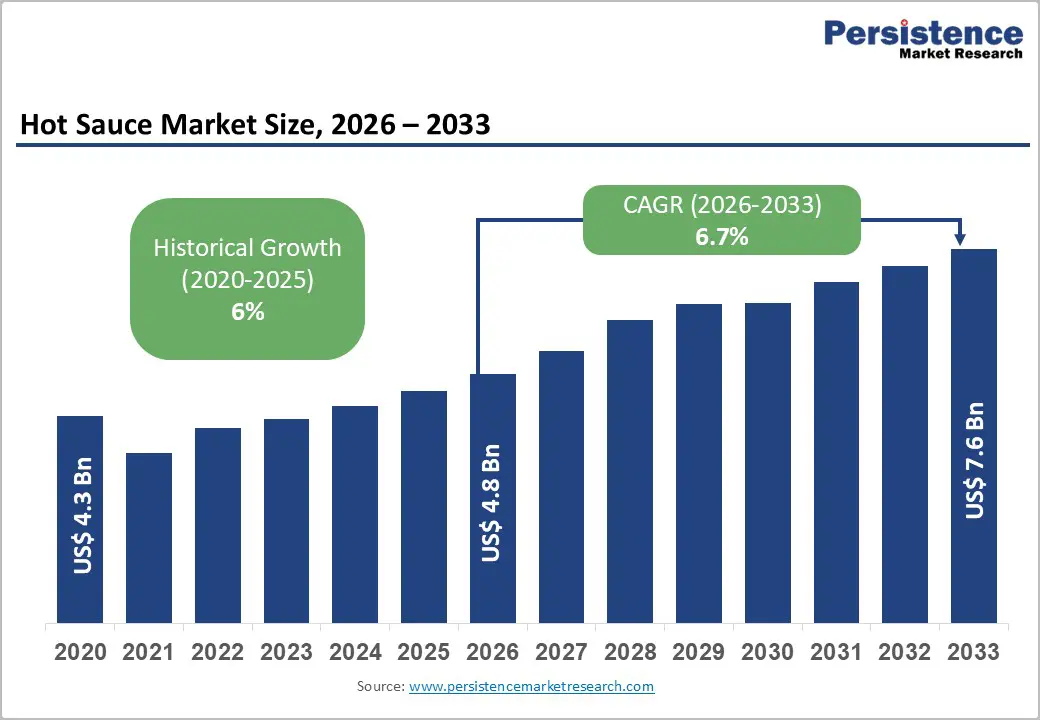

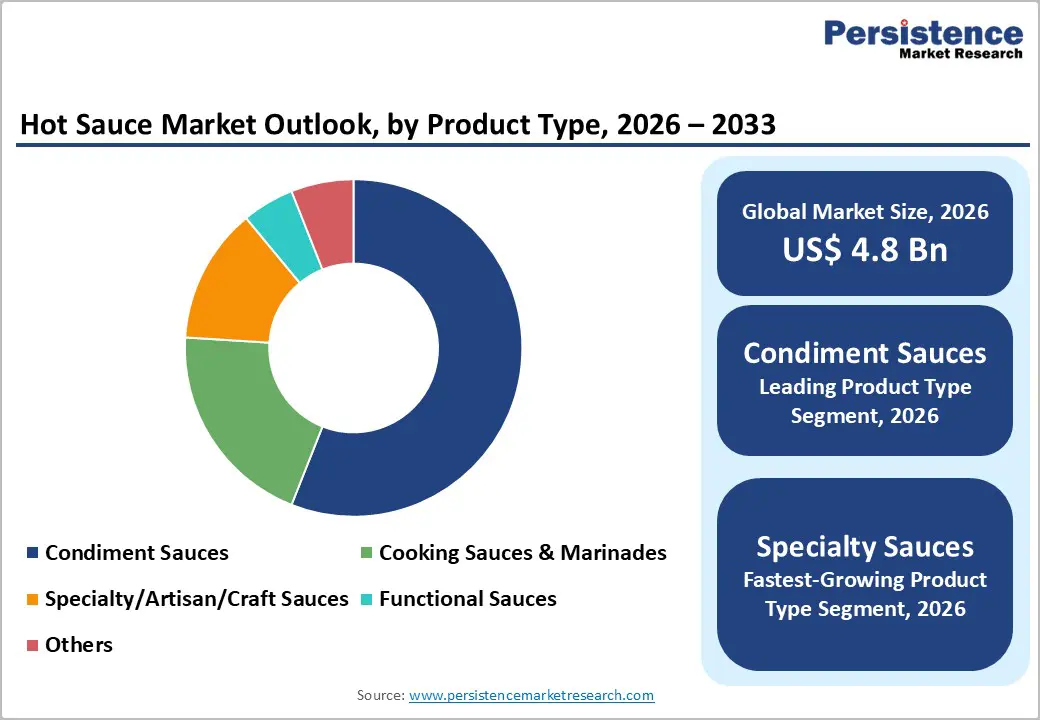

The global hot sauce market size is likely to be valued at US$ 4.8 billion in 2026, and is projected to reach US$ 7.6 billion by 2033, growing at a CAGR of 6.8% during the forecast period 2026 - 2033.

The market is entering a healthy growth phase, transitioning from post-pandemic volume acceleration toward value-led expansion driven by premiumization, packaging innovation, and channel rebalancing. Market growth is increasingly supported by higher average selling prices (ASPs), diversified consumption occasions, and stronger brand-led differentiation across mature and emerging markets. Between 2020 and 2025, the market expanded rapidly due to the adoption of at-home cooking, foodservice recovery, and broader acceptance of heat-forward cuisines.

Demand is expected to remain resilient, backed by rising urbanization, increased exposure to global cuisines, and sustained demand from quick-service restaurants (QSRs) and packaged food manufacturers. Evolution of packaging formats, particularly toward squeeze bottles and single-serve sachets, is improving unit economics and enabling deeper penetration in emerging markets.

At the same time, specialty and craft sauce makers are expanding margins in North America and Europe. Asia Pacific is increasingly influencing global flavor innovation, although North America remains the largest revenue contributor. Market forces are favoring players that can manage agricultural input volatility, optimize multi-channel distribution, and scale differentiated stock-keeping units (SKUs) across geographies.

Key Industry Highlights

- Product Type Dominance: Condiment sauces are anticipated to dominate with a projected 56% revenue share in 2026, reflecting routinized household and QSR usage

- Fastest-growing Product Type: Specialty and artisan sauces are likely to grow the fastest through 2033, as premiumization, fermentation, and flavor differentiation gain traction.

- Leading Packaging Formats: Glass bottles are projected to lead with an estimated 39% revenue share in 2026, owing to regulatory acceptance, while single-serve sachets are expected to grow the fastest through 2033, driven by foodservice expansion and affordability.

- Channel Dynamics: Supermarkets and hypermarkets are likely to account for roughly 46% of sales in 2026, driven by shelf visibility and private-label scale.

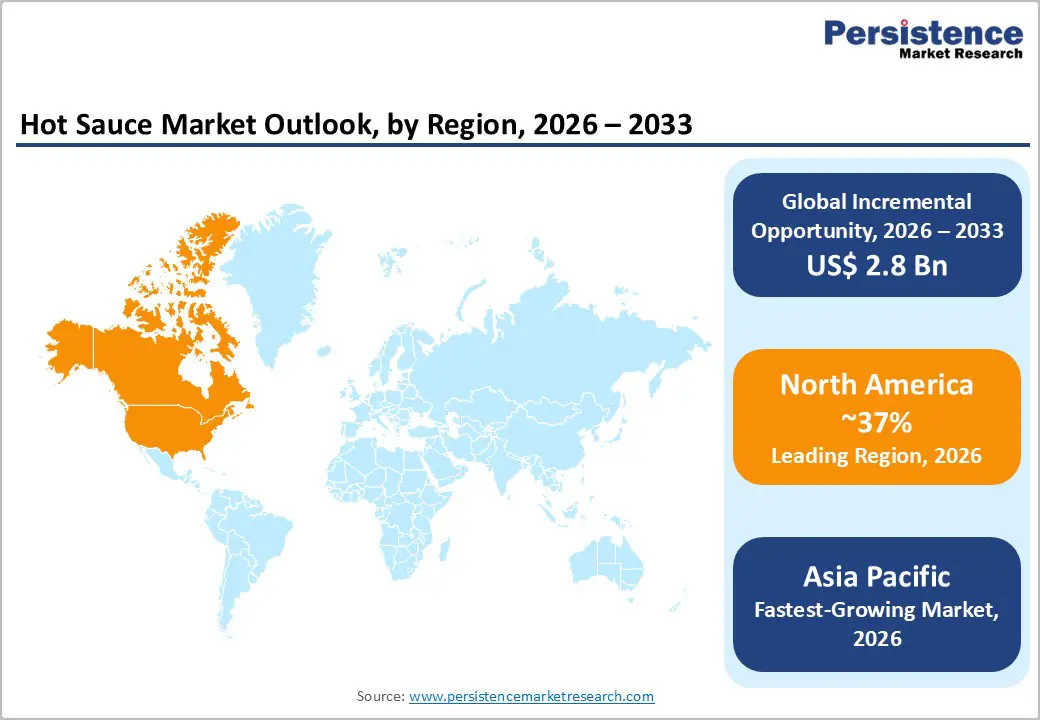

- Regional Momentum: Asia Pacific is projected to be the fastest-growing regional market through 2033, underpinned by modern retail expansion and unprecedented foodservice penetration.

- Prime Growth Driver: The institutionalization of hot sauce as a standardized flavor component on foodservice and QSR menus worldwide is the primary demand driver.

- July 2025: Ohly introduced two new ProDry culinary hot sauce powders to help food manufacturers deliver authentic and complex spicy flavours with efficient dispersion and controlled heat.

| Key Insights | Details |

|---|---|

| Hot Sauce Market Size (2026E) | US$ 4.8 Bn |

| Market Value Forecast (2033F) | US$ 7.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 1.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Foodservice-led Standardization of Heat as a Core Flavor Profile

The most relevant factor driving the hot sauce market growth is the increasing standardization of hot sauce as a default flavor enhancer within global foodservice menus, particularly across QSRs and fast-casual dining formats. Foodservice operators are increasingly integrating proprietary or co-branded hot sauces directly into menu architecture, rather than positioning them as optional table condiments.

This shift is reinforced by menu engineering strategies that increase average order value and repeat visitation. This consumption pattern is favoring condiments that deliver high perceived flavor intensity at a low incremental cost per serving. Hot sauce meets this requirement more effectively than most competing condiments due to its concentrated formulation, low dosage requirement, and strong sensory impact.

At the same time, regulatory clarity regarding food additives and preservatives in major markets of consumption is reducing formulation risk for large foodservice suppliers and multinational chains. In parallel, advances in shelf-stable processing technologies and bulk packaging systems are improving product consistency while reducing spoilage and operational waste across outlets.

These developments are enabling global QSR operators to standardize flavor profiles across regions without compromising food safety or cost efficiency. Foodservice demand is increasingly anchoring baseline volumes, which is dampening the cyclicality traditionally associated with retail consumption. For manufacturers, this dynamic is shifting portfolio priorities toward bulk packaging formats, co-development partnerships, and long-term supply agreements. As a result, the industry is moving toward a structurally higher demand floor that remains resilient even as consumer-discretionary spending tightens.

Growing Exposure to Chili Pepper Supply Volatility

A key restraint is the continued exposure of the hot sauce industry to volatility in agricultural inputs, particularly the geographic concentration and climate sensitivity of chili pepper supply. Global chili production remains heavily concentrated in a limited number of countries, including India, China, Mexico, and several African producers, thereby increasing systemic supply risk.

Climate variability, rising water stress, and tightening agricultural labor availability are increasingly disrupting the stability of yields across these regions. Data from the Food and Agriculture Organization (FAO) and national agricultural ministries indicate that annual fluctuations in chili yield are becoming more frequent and intense in major producing areas. This volatility directly translates into raw material price instability, as chili peppers account for a disproportionately large share of the cost of goods sold relative to their volumetric contribution in hot sauce formulations.

Limited financial hedging mechanisms are amplifying manufacturer exposure, since chili peppers lack the deep and liquid futures markets available for staple crops. Regulatory tightening on pesticide residues, traceability requirements, and import compliance, particularly across the European Union, further constrains sourcing flexibility. Smaller producers are facing rising certification and compliance costs that are eroding competitiveness, while larger manufacturers are experiencing margin compression during periods of spot price inflation.

These risks are becoming more pronounced in premium and single-origin sauces, where ingredient substitution is not feasible without undermining brand positioning. From a business risk perspective, sustained input volatility is increasing working capital requirements and compressing gross margins across the value chain. For investors, this restraint is reinforcing the importance of supply chain governance, agricultural risk management, and sourcing transparency as core diligence criteria.

Scalable Premiumization in Emerging Urban Markets

A highly lucrative opportunity is emerging from scalable premiumization strategies that are targeting urban consumers across the Asia Pacific and Latin America. Unlike mature markets, where premium hot sauce consumption is already well established, these regions remain in the early phase of value migration despite strong cultural familiarity with spicy foods and high baseline heat tolerance.

Urban middle-income households are increasingly prioritizing convenience, food safety, and brand assurance, which is reshaping condiment purchasing behavior. Countries such as India, Indonesia, Vietnam, and Mexico are witnessing a steady shift from home-prepared sauces toward packaged alternatives as urban lifestyles are becoming more time-constrained.

Digital retail infrastructure is lowering entry barriers to premium products, thereby further stimulating the market. E-commerce platforms and quick-commerce channels enable manufacturers to launch, test, and refine premium SKUs without relying heavily on physical retail networks. This is accelerating product iteration cycles and improving capital efficiency. Importantly, premiumization in these markets is being driven less by extreme heat levels and more by flavor complexity, hygiene assurance, and brand credibility. Consumers are increasingly valuing consistent taste profiles, trusted sourcing, and modern packaging formats.

This dynamic is creating a sizable mid-premium opportunity positioned between unbranded local products and imported gourmet offerings for sauce manufacturers. Companies that are localizing flavor development, optimizing pack sizes, and aligning pricing with urban purchasing power will benefit enormously as these markets mature.

Category-wise Analysis

Packaging Format Insights

Glass bottles are poised to lead in 2026, accounting for an estimated 39% of the hot sauce market revenue share. This leadership position is being supported by strong premium positioning, high perceived product integrity, and broad regulatory acceptance across major consumption regions.

Glass packaging is remaining the preferred format in North America and Europe for retail SKUs, particularly within specialty and branded segments, where shelf visibility, product authenticity, and reusability are influencing purchasing decisions. From a profitability perspective, glass bottles support higher ASPs, helping manufacturers offset elevated transportation and handling costs associated with heavier packaging materials.

Single-serve sachets are projected to grow at the fastest CAGR of 8.7% between 2026 and 2033. This expansion is driven by rising foodservice usage, institutional catering demand, and increasing urban on-the-go consumption across the Asia-Pacific and Latin America.

Sachet formats improve affordability, minimize product waste, and enable deeper market penetration in price-sensitive consumer segments. For manufacturers, sachets enable rapid volume scalability and broader distribution reach, but they also require targeted investments in high-speed filling lines, packaging automation, and cost-efficient material sourcing to maintain margins.

Product Type Insights

Table and condiment sauces are slated to dominate with an estimated hot sauce market share of 56% in 2026. This segment is supported by habitual consumption patterns, broad cross-cuisine compatibility, and strong visibility in organized retail environments.

Demand remains resilient due to consistent household usage and widespread placement on foodservice tables, particularly in quick-service restaurants. From a commercial perspective, these products are providing stable base volumes and predictable demand cycles, which is allowing manufacturers to optimize production planning and distribution efficiency.

In contrast, specialty and artisan sauces are projected to expand at the fastest CAGR (2026-2033), at 9%. Growth is being driven by rising consumer interest in flavor experimentation, fermented formulations, and limited-release offerings.

Although absolute volumes are remaining relatively small, this segment is delivering disproportionately high margins and stronger brand engagement. Specialty sauces are increasingly serving as an innovation pipeline, shaping flavor trends and product narratives that are later scaled into mainstream portfolios. For manufacturers, disciplined portfolio segmentation is becoming critical to capture premium upside without diluting core volume performance.

Distribution Channel Insights

Supermarkets and hypermarkets are likely to remain the primary distribution channels for hot sauce in 2026, accounting for an estimated 46% of global sales. These modern-trade facilities maintain their dominance in mature markets due to established shelf allocation practices, the expansion of private-label offerings, and the continued use of promotional pricing to drive volume.

While this channel remains critical for scale and visibility, growth is gradually moderating as store networks reach saturation and incremental shelf gains become more difficult. Supermarkets and hypermarkets are increasingly emphasizing operational efficiency, portfolio rationalization, and strong retailer relationships, pushing companies and manufacturers to adopt new expansion strategies in the market.

Online retail is projected to achieve the highest CAGR of approximately 10.5% between 2026 and 2033. This growth is being supported by rising demand for premium stock-keeping units, subscription-based replenishment models, and influencer-driven product discovery.

Digital channels are enabling manufacturers to access richer consumer data, shorten innovation cycles, and exercise greater control over pricing and assortment strategies. However, these advantages are being partially offset by higher customer acquisition costs and increased spending on digital marketing, making disciplined channel strategy and performance tracking essential for sustainable profitability.

Regional Insights

North America Hot Sauce Market Trends

North America is expected to be the largest regional market for hot sauce in 2026, accounting for an estimated 37% of global revenue. Market growth here is being supported by sustained premiumization trends, high penetration of quick-service restaurants, and ongoing brand-led product innovation. Although the region exhibits characteristics of a mature market, demand remains stable and predictable. As a result, the market in North America is forecast to grow at a robust rate between 2026 and 2033.

From a structural standpoint, regulatory clarity regarding food safety and labeling, combined with well-developed cold-chain and logistics infrastructure, continues to favor established manufacturers with scale advantages. High levels of marketing and promotional spending reinforce brand loyalty and create entry barriers for smaller players.

Investment opportunities are increasingly concentrated in specialty and premium sauce segments, as well as in long-term foodservice partnerships that offer stable volumes and lower demand volatility. Achieving success in North America for hot sauce companies increasingly depends on disciplined portfolio management, differentiated branding, and the ability to translate innovation into scalable retail and foodservice distribution.

Europe Hot Sauce Market Trends

Europe is projected to account for approximately 23% of the hot sauce market in 2026, with growth remaining concentrated in Western European markets. Regional demand is being fueled by rising clean-label preferences and increasing adoption of multicultural cuisines, which are expanding the role of hot sauce beyond traditional ethnic food segments. Considering these factors, the European hot sauce market is expected to showcase a CAGR of approximately 5.5% during the 2026 - 2033 forecast period, reflecting steady but disciplined expansion.

Heightened scrutiny of food additives, preservatives, and labeling under the European Union (EU) regulatory framework is actively shaping product formulations and supplier selection across the region. Compliance requirements are increasing development and certification costs, particularly for smaller brands.

Private-label penetration remains high across the European retail ecosystem, enabling volume growth but placing sustained pressure on branded margins. For manufacturers, competitive advantage in Europe is increasingly tied to regulatory expertise, cost-efficient formulation strategies, and selective participation in private-label programs that protect scale without eroding long-term brand equity.

Asia Pacific Hot Sauce Market Trends

The Asia-Pacific hot sauce market is projected to be the fastest-growing, with a CAGR of approximately 7.7% through 2033. Market expansion here is being driven by rapid urbanization, sustained growth in middle-income households, and continued expansion of modern retail and organized foodservice infrastructure.

Large metropolitan areas across China, India, Southeast Asia, and South Korea are experiencing a steady shift toward packaged condiments, as urban consumers prioritize convenience, food safety, and consistent flavor profiles. The proliferation of quick-service restaurants and casual dining formats is increasing baseline demand for standardized hot sauce offerings.

In terms of competition, local and regional brands are continuing to dominate volume sales due to deep cultural alignment, localized flavor profiles, and strong price competitiveness. Global manufacturers are increasingly focusing on premium and mid-premium niches rather than competing directly on mass-market volumes. These players are leveraging brand credibility, perceived quality assurance, and differentiated formulations to capture higher-margin segments.

Regulatory fragmentation across the Asia-Pacific region remains a structural challenge, as food safety standards, labeling requirements, and import regulations vary significantly across countries. However, this complexity is also acting as a barrier to rapid market entry, favoring incumbents with established regulatory expertise and local partnerships.

Asia-Pacific offers a compelling combination of scale, growth, and margin-expansion potential, provided that strategies are tailored to local regulatory environments and consumer preferences rather than relying on uniform regional approaches.

Competitive Landscape

The global hot sauce market is expected to remain moderately fragmented, with the top five manufacturers collectively accounting for roughly 40% of total global revenue. This structure reflects the coexistence of large multinational food companies and a wide base of regional and local producers.

Market leaders are benefiting from strong brand equity, broad product portfolios, and long-standing relationships with foodservice operators and organized retail chains. These advantages are enabling leading players to secure shelf visibility, negotiate favorable distribution terms, and maintain consistent product availability across multiple geographies.

Competitive dynamics are gradually shifting away from price-based competition toward differentiation built on brand positioning, supply reliability, and the pace of innovation. Manufacturers are increasingly competing on flavor authenticity, formulation consistency, and the ability to launch new variants in response to evolving consumer preferences.

Supply chain resilience, particularly access to stable chili pepper sourcing and scalable packaging infrastructure, is becoming a key competitive factor. For investors and strategic buyers, this competitive landscape favors companies with defensible brands, diversified sourcing strategies, and repeatable innovation capabilities, rather than those relying solely on cost leadership.

Key Industry Developments

- In January 2026, Highlander Partners acquired Tapatío, the number five hot sauce brand in the United States. The acquisition reflects Highlander’s strategy to expand Tapatío’s geographic reach, broaden distribution channels, and accelerate new product development in a hot sauce category that continues to benefit from secular demand trends in spicy and flavorful foods.

- In July 2025, Popeyes introduced its first-ever Signature Sauce, developed over five years and inspired by Louisiana’s classic “holy trinity” of bell pepper, celery, and onion with a touch of hot sauce, now a permanent menu item across the United States and Canada. The chain is also offering limited-time Chicken Dippers, enhancing summer menu variety and deepening customer engagement with its core flavors.

- In June 2025, First We Feast and HEATONIST showcased the new Hot Ones Tropical Amarillo hot sauce at the 2025 Summer Fancy Food Show, featuring vibrant notes of mango, pineapple, and warm spices. The release, part of the Hot Ones Season 27 lineup, capitalizes on consistent consumer interest in novel and approachable heat profiles.

Companies Covered in Hot Sauce Market

- McCormick & Company

- Huy Fong Foods

- The Kraft Heinz Company

- Unilever PLC

- Hormel Foods Corporation

- Conagra Brands

- Nestlé S.A.

- Grupo Herdez

- Campbell Soup Company

- Southeastern Mills

- Kikkoman Corporation

- Lee Kum Kee

Frequently Asked Questions

The global hot sauce market is projected to reach US$ 4.8 billion in 2026.

Diversification of consumption occasions, stronger brand-led differentiation across mature and emerging markets, and broadening acceptance of heat-forward cuisines are driving the market.

The market is poised to witness a CAGR of 6.8% from 2026 to 2033.

Rapidly evolving flavor preferences among urban consumers, increased exposure to global cuisines, and sustained demand from QSRs and packaged food manufacturers are key market opportunities.

McCormick & Company, Huy Fong Foods, The Kraft Heinz Company, and Unilever PLC are some of the key players in the market.