- Smart Packaging

- Hot Fill Packaging Market

Hot Fill Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Hot Fill Packaging Market by Product Type (Bottles, Pouches, Others), Material Type (PET, Glass, Others), Application, and Regional Analysis for 2026 - 2033

Hot Fill Packaging Market Size and Trends Analysis

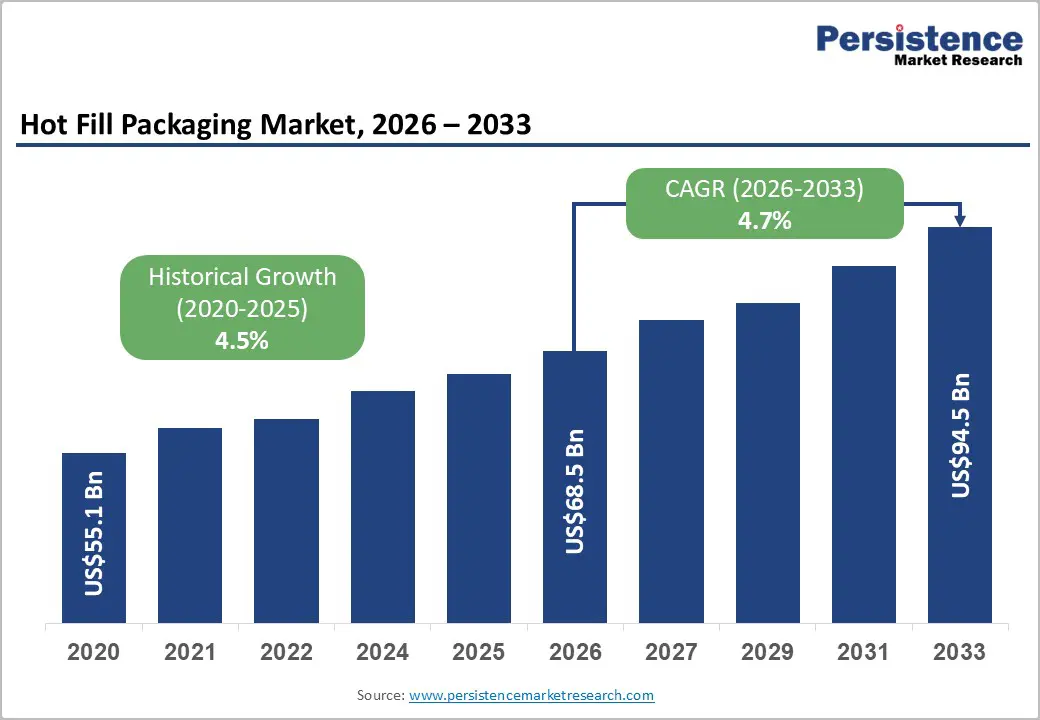

The global hot fill packaging market size is likely to be valued at US$68.5 billion in 2026 and is expected to reach US$94.5 billion by 2033, growing at a CAGR of 4.7% between 2026 and 2033, driven by the sustained growth of ready-to-drink beverages, rising consumption of shelf-stable fruit juices and sauces, and continued investments in lightweight, high-barrier packaging materials that preserve product quality while reducing logistics costs.

Manufacturers are increasingly prioritizing PET and advanced polymer structures for cost efficiency and performance, while glass packaging is gaining momentum in premium and specialty product segments. Industry consolidation and sustainability mandates are reshaping supplier strategies and capital allocation, with Asia-Pacific remaining the largest regional market.

Key Industry Highlights

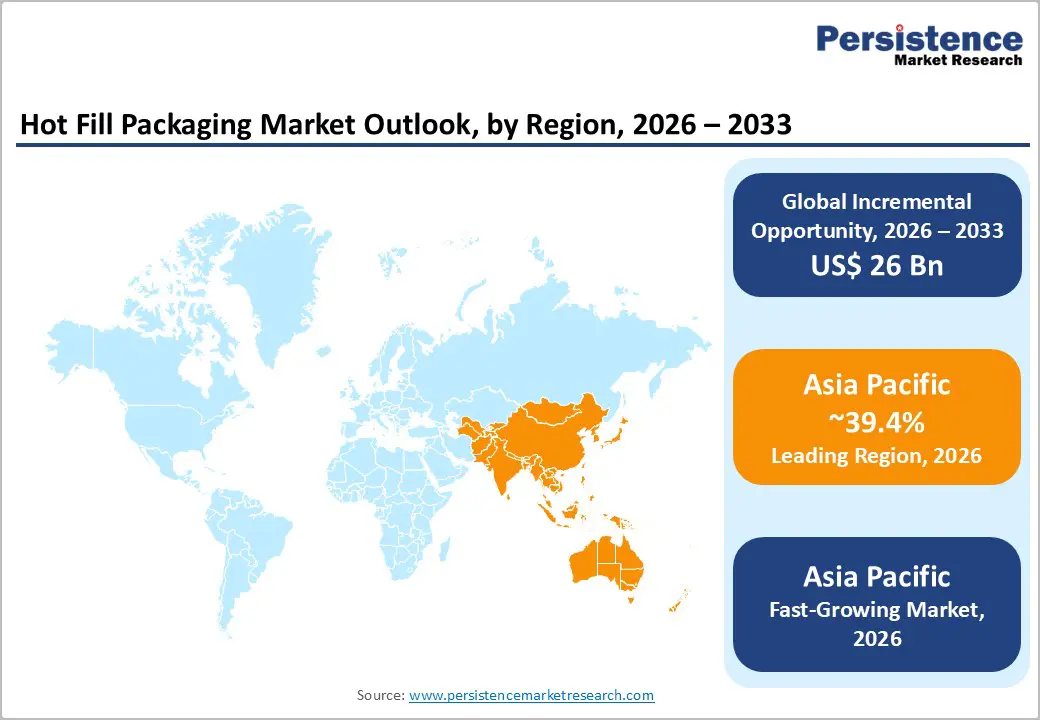

- Leading Region: Asia Pacific is projected to dominate the market, accounting for an estimated 39.4% share in 2026, supported by large-scale beverage manufacturing, strong demand for shelf-stable RTD products, and cost-efficient PET and glass production capacity across China, India, Japan, and ASEAN economies.

- Fastest-growing Region: North America is the fastest-growing regional market, driven by high per-capita consumption of RTD beverages, expanding functional drink portfolios, and increasing adoption of hot-fill-compatible recycled PET under state-level sustainability and food safety regulations.

- Investment Plans: Investment activity is concentrated in recycled PET (rPET) supply chains, heat-set PET barrier innovation, lightweight glass bottles, and recyclable pouch structures, with packaging manufacturers and brand owners expanding capacity to meet regulatory compliance and sustainability commitments across North America, Europe, and Asia Pacific.

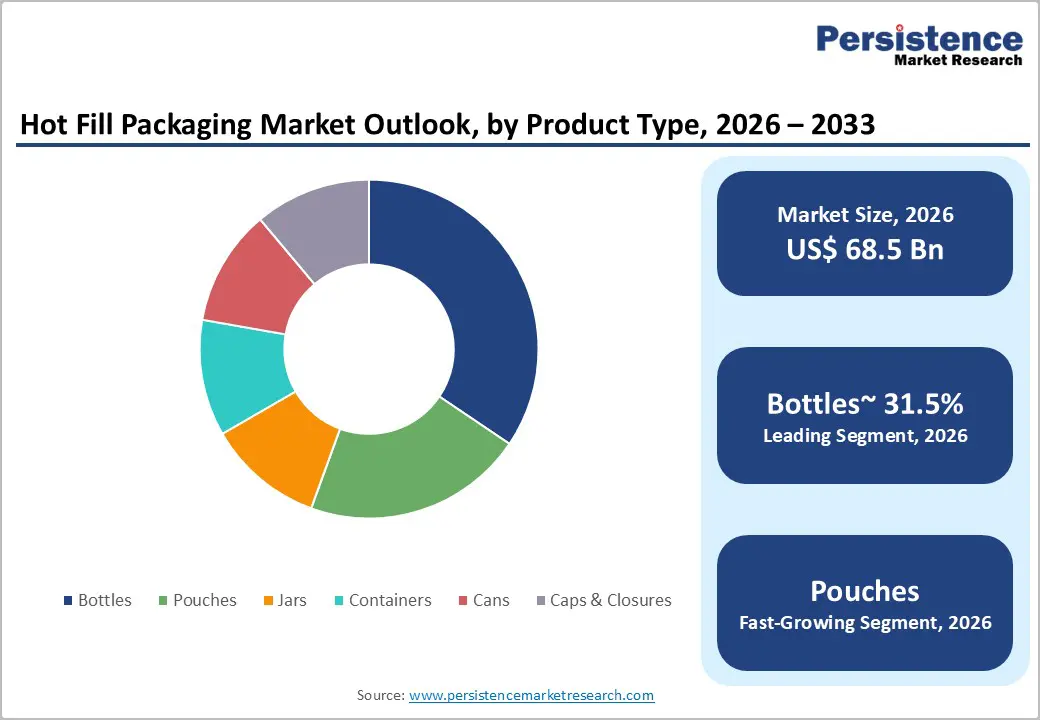

- Dominant Product Type: Bottles are expected to remain the leading product type, accounting for 31.5% of the market in 2026, owing to their durability, thermal stability, compatibility with automated filling lines, and continued preference for juices, sauces, and ambient RTD beverages.

- Leading Application: Fruit juices are projected to account for the largest share, at 36.8%, driven by acidic formulations, preservation requirements, and widespread reliance on hot-fill processing for shelf-stable, multi-serve packaging formats.

| Key Insights | Details |

|---|---|

| Hot Fill Packaging Market Size (2026E) | US$68.5 Bn |

| Market Value Forecast (2033F) | US$94.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Growth in Ready-To-Drink Beverages and Fruit Juice Consumption

Global consumption of ready-to-drink beverages and shelf-stable fruit juices continues to rise due to urbanization, busier lifestyles, and increased demand for convenience-oriented food and beverage solutions. Hot-fill packaging remains a preferred preservation method because it enables effective microbial control without requiring aseptic processing or chemical preservatives. Filling temperatures typically range from 85°C to 95°C to denature enzymes and inactivate microorganisms, extending shelf life for juices, nectars, sauces, and several RTD beverage categories. This preservation efficiency reduces cold-chain dependency and preservative formulation costs, directly improving gross margins for beverage manufacturers and reinforcing hot-fill adoption across high-volume product lines.

Material Innovation in PET and Recyclable Packaging Formats

Technological advances in PET coextrusion, enhanced oxygen-barrier layers, and improved sourcing of recycled PET have strengthened PET’s position as the dominant material in hot-fill packaging. PET’s lightweight nature lowers transportation costs and emissions, while improved thermal resistance and barrier performance enable reliable hot-fill applications. Multi-layer PET and PET-based hybrid structures offer resilience against deformation at high temperatures, enabling manufacturers to replace heavier glass formats in mass-market segments. Ongoing investment in recycled feedstocks and advanced recycling processes supports compliance with recycled-content targets, reduces supply-chain emissions exposure, and reinforces PET’s long-term material leadership.

Regulatory and Sustainability Pressures

Governments, retailers, and brand owners are tightening packaging sustainability requirements, accelerating the transition toward recyclable and circular hot-fill solutions. Mandates related to recycled content, packaging recovery, and extended producer responsibility increase the commercial attractiveness of mono-material packaging and recyclable rigid containers. These regulations are driving capital investment in sustainable material design, packaging lightweighting, and traceable supply chains. Over time, compliance reduces exposure to waste management surcharges and regulatory penalties, supporting more predictable operating costs and reinforcing sustainability as a core strategic priority across the hot-fill packaging ecosystem.

Barrier Analysis - High Capital Intensity and Retrofit Complexity

Hot-fill packaging requires specialized filling lines, thermal control systems, and container designs capable of withstanding elevated temperatures and internal vacuum pressure. Retrofitting existing cold-fill infrastructure to hot-fill operations involves substantial capital expenditure and extended downtime. For mid-sized and regional packers, payback periods can extend several years, limiting flexibility in product launches and capacity expansion. High upfront investment requirements constrain smaller entrants, increase operational risk, and lengthen time-to-market for new SKUs.

Material and Logistical Trade-Offs

While PET provides cost and weight advantages, glass remains preferred for premium positioning and maximum shelf-life protection. Transitioning away from glass can introduce trade-offs related to perceived quality and the availability of recycling infrastructure, which varies significantly by region. Supply chain volatility, including resin price fluctuations and transportation disruptions, further affects input cost stability. Periodic price swings can materially affect operating margins, particularly for high-volume beverage producers with limited pricing flexibility.

Opportunity Analysis - Premiumization through Glass and Hybrid Packaging Formats

The premium beverage and gourmet food categories increasingly use glass packaging to communicate quality, authenticity, and sustainability. Glass offers superior barrier properties and strong shelf appeal, enabling manufacturers to command price premiums across modern retail and direct-to-consumer channels. Premium hot-fill glass packaging represents a multi-hundred-million-dollar opportunity by 2030, particularly in developed markets where consumers demonstrate willingness to pay for product differentiation and sustainable packaging credentials.

Expansion of Pouches and Single-Serve Convenience Formats

Flexible pouches, including spouted and retortable hot-fill variants, address demand for portability, portion control, and reduced packaging weight. These formats reduce transportation costs, improve shelf efficiency, and support the growth of single-serve product categories such as sauces, soups, and RTD concentrates. Cost efficiency and convenience position pouches as the fastest-growing product type, with significant total addressable market expansion as private-label brands and emerging manufacturers adopt flexible packaging solutions.

Category-wise Analysis

Product Type Insights

Bottles are projected to remain the leading product type in the hot-fill packaging market, representing approximately 31.5% of total market share in 2026. This segment is expected to sustain its dominance throughout the forecast period, supported by the widespread use of rigid PET and glass bottles, which provide reliable mechanical strength, effective oxygen and moisture barrier properties, and seamless compatibility with high-speed automated filling and capping lines. These attributes make bottles the preferred choice for carbonated-adjacent beverages, fruit juices, sauces, and condiments produced at an industrial scale.

Purpose-engineered bottle formats incorporating reinforced neck finishes, vacuum panels, and heat-set PET resins ensure dimensional stability during thermal filling and post-fill cooling. Major beverage and food brands continue to rely on hot-fill PET bottles for shelf-stable juice lines and ambient sauces, particularly in North America and the Asia Pacific, where distribution efficiency and retail shelf visibility remain critical commercial considerations.

Pouches are expected to represent the fastest-growing product type in the hot-fill packaging market, driven by rising demand for single-serve convenience, portion control, and sustainability-aligned packaging formats. Their lightweight structure significantly reduces material usage, transportation costs, and associated emissions when compared with rigid alternatives.

Advances in multilayer barrier laminates and spouted pouch designs now enable reliable hot-fill processing while maintaining seal integrity and shelf stability. Adoption is accelerating across sauces, soups, broths, and ready-to-mix beverage concentrates, particularly among private-label manufacturers and emerging food brands seeking lower capital investment and faster commercialization. Retailers increasingly favor hot-fill pouches for value-oriented SKUs and e-commerce distribution due to reduced breakage risk and improved space efficiency.

Application Insights

Fruit juices and nectars are projected to be the largest application segment in the hot-fill packaging market, accounting for an estimated 36.8% share in 2026, and this dominance is expected to continue throughout the forecast period. The naturally acidic profile of fruit juices, combined with particulate content in pulpy variants, makes hot-fill processing a highly effective method for microbial control and shelf-life extension without chemical preservatives. High-volume production of multi-serve juice formats amplifies economies of scale, reinforcing the segment’s leadership position.

Global and regional juice producers rely heavily on hot-fill PET and glass bottles for ambient distribution, particularly in emerging markets where cold-chain infrastructure remains limited. This application continues to anchor baseline demand for hot-fill packaging systems worldwide.

Ready-to-drink beverages are likely to be the fastest-growing application segment, driven by urbanization, on-the-go consumption, and expanding functional beverage portfolios. Hot-fill technology enables shelf-stable distribution of teas, functional drinks, plant-based infusions, and vitamin-fortified beverages without refrigeration, delivering both cost efficiency and formulation flexibility. Growth momentum is particularly strong in Asia-Pacific markets, where demand for ambient RTD teas and health-oriented beverages continues to rise.

The increasing use of hot-fill-compatible pouches and lightweight PET bottles further accelerates innovation cycles, allowing brands to launch new SKUs rapidly while maintaining food safety and regulatory compliance.

Regional Insights

North America Hot Fill Packaging Market Trends - Regulation-Driven Innovation in Hot-Fill PET and Glass for National RTD Distribution

North America remains a strategically important hot-fill packaging market, underpinned by high per-capita consumption of ready-to-drink (RTD) beverages, sophisticated retail infrastructure, and stringent food safety oversight. The U.S. accounts for the majority of regional demand, supported by an extensive ecosystem of beverage co-packers and contract fillers capable of high-volume hot-fill operations. Leading juice, tea, and functional beverage brands continue to rely on hot-fill PET and glass bottles to achieve ambient shelf stability while meeting national distribution requirements.

Regulatory rigor plays a defining role in shaping packaging design and validation. Oversight from the U.S. Food and Drug Administration (FDA) under Current Good Manufacturing Practices (cGMP) and the Food Safety Modernization Act (FSMA) reinforces demand for packaging formats with proven thermal resistance and seal integrity. State-level recycling mandates, particularly in California and the Northeast, are also influencing material economics by accelerating the adoption of recycled PET (rPET) in hot-fill bottles.

Beverage leaders such as Coca-Cola North America and PepsiCo have publicly committed to increasing recycled content across packaging portfolios, driving upstream investment in food-grade rPET supply chains compatible with hot-fill performance requirements. Innovation investment remains focused on heat-set PET resins, lightweight glass bottles, and enhanced oxygen barrier technologies, supported by suppliers such as Owens-Illinois, Amcor, and Berry Global. These developments reinforce North America’s position as a stable, innovation-driven market, with sustained demand across juices, RTD teas, sauces, and shelf-stable functional beverages.

Europe Hot Fill Packaging Market Trends - Sustainability-Led Adoption of Recyclable and Lightweight Hot-Fill Formats

European demand for hot-fill packaging is concentrated in Western Europe, where sustainability regulations, premium brand positioning, and circular-economy targets strongly influence packaging selection. Countries including Germany, the U.K., France, and Spain demonstrate consistent demand for recyclable, high-barrier hot-fill solutions across juices, sauces, and ambient beverages. Consumers in these markets exhibit a strong preference for packaging formats that align with environmental credentials, reinforcing the role of glass and mono-material PET designs.

The regulatory environment is a key structural driver. Harmonized frameworks under the European Union’s Packaging and Packaging Waste Directive (PPWD) and evolving recycled-content mandates promote the use of design-for-recycling principles and the incorporation of higher levels of recycled material. This has accelerated investment in hot-fill-compatible rPET bottles and lightweight glass containers, particularly among European beverage and food producers seeking compliance without compromising shelf life or product safety.

Packaging suppliers such as Tetra Pak, Ardagh Group, and Gerresheimer continue to expand capabilities in lightweight glass and recyclable rigid formats suitable for hot-fill conditions. In parallel, flexible packaging producers are advancing mono-material pouch structures to meet recyclability requirements while maintaining thermal resistance. These developments position Europe as a global reference point for sustainable hot-fill packaging innovation, where regulatory clarity and premium branding reinforce long-term market resilience rather than volume-driven growth alone.

Asia Pacific Hot Fill Packaging Market Trends - High-Volume Growth Fueled by Urbanization and Ambient Beverage Demand

Asia-Pacific is projected to lead the global hot-fill packaging market, accounting for an estimated 39.4% regional share in 2026 and remaining the fastest-growing region through 2033. Growth is driven by rapid urbanization, rising disposable incomes, and expanding penetration of modern retail across China, Japan, India, and the ASEAN economies. Hot-fill packaging is widely adopted for fruit juices, RTD teas, functional beverages, sauces, and soups, where ambient distribution is critical in markets with uneven cold-chain infrastructure.

China represents the largest single-country contributor, supported by large-scale beverage manufacturing clusters and strong domestic demand for shelf-stable RTD products. Major regional beverage brands and multinational players operating in Asia Pacific rely heavily on hot-fill PET bottles and increasingly on spouted pouches for portion-controlled offerings. Japan continues to emphasize quality assurance and packaging precision, sustaining demand for high-performance hot-fill bottles in premium teas and functional drinks.

The region benefits from economies of scale in manufacturing, with ongoing investment in PET resin, preform, and glass container production across China, India, and Southeast Asia. Companies such as Amcor, Indorama Ventures, and regional glass manufacturers have expanded capacity to support both domestic consumption and export-oriented packaging supply. Regulatory maturity varies across markets, creating challenges for recycling infrastructure and opportunities for localized circular initiatives. As governments strengthen food safety and packaging waste regulations, the Asia Pacific is expected to remain the primary volume and growth engine for the global hot-fill packaging market.

Competitive Landscape

The global hot fill packaging market exhibits moderate concentration among large global suppliers, alongside fragmentation at the regional and local converter level. Leading players differentiate through integrated material science, closure systems, and filling-line expertise. Ongoing consolidation and vertical integration are reshaping competitive dynamics and strengthening scale advantages.

Key strategies include vertical integration, sustainability-driven product innovation, and geographic expansion through mergers and partnerships. Market leaders focus on technical support, shorter product development cycles, and supply chain transparency to strengthen customer relationships and competitive positioning.

Key Industry Developments

- In August 2025, UMETASS, a China-based advanced packaging manufacturer, announced the launch of its 80°C hot-fill PET Bottle Series, designed for liquid seasonings, sauces, syrups, and dips, featuring optimized thermal and vacuum panel designs to improve performance.

Companies Covered in Hot Fill Packaging Market

- Amcor plc

- Berry Global Group, Inc.

- Owens-Illinois, Inc.

- Ardagh Group S.A.

- Tetra Pak International S.A.

- Ball Corporation

- Crown Holdings, Inc.

- Graham Packaging Company

- Gerresheimer AG

- Silgan Holdings Inc.

- ALPLA Group

- Plastipak Holdings, Inc.

- RPC Group (Berry Global)

- DS Smith Plc

- AptarGroup, Inc.

- Scholle IPN

- Comar, LLC

- Huhtamaki Oyj

Frequently Asked Questions

The global hot fill packaging market size is valued at US$68.5 billion in 2026.

By 2033, the hot fill packaging market is expected to reach US$94.5 billion.

Key trends include the rising adoption of heat-set PET bottles, increasing use of recycled PET (rPET) for regulatory compliance, rapid growth of hot-fill-compatible pouches, and sustained demand for shelf-stable RTD beverages across Asia Pacific and North America.

By product type, bottles are projected to lead the hot-fill packaging market, accounting for approximately 31.5% of the market share in 2026. Their dominance is supported by strong durability, thermal resistance, and compatibility with high-speed automated filling systems. By application, fruit juices are expected to represent the largest segment with an estimated 36.8% share, driven by the need for effective preservation and extended shelf life.

The hot fill packaging market is projected to grow at a CAGR of 4.7% between 2026 and 2033.

Major players include Amcor plc, Berry Global Group, Inc., Owens-Illinois, Inc., Tetra Pak International S.A., and Ardagh Group S.A.