- Renewable Energy

- Thin-film Photovoltaic Market

Thin-film Photovoltaic Market Size, Share, and Growth Forecast, 2026 - 2033

Thin-film Photovoltaic Market by Material Type (Cadmium Telluride, Copper Indium Gallium Selenide, Amorphous Silicon and Others), By Film Type (Rigid and Flexible), By Component (Module, Inverter and BOS), By End Use (Residential, Commercial, and Utility), and Regional Analysis for 2026 - 2033

Thin-film Photovoltaic Market Size and Trends Analysis

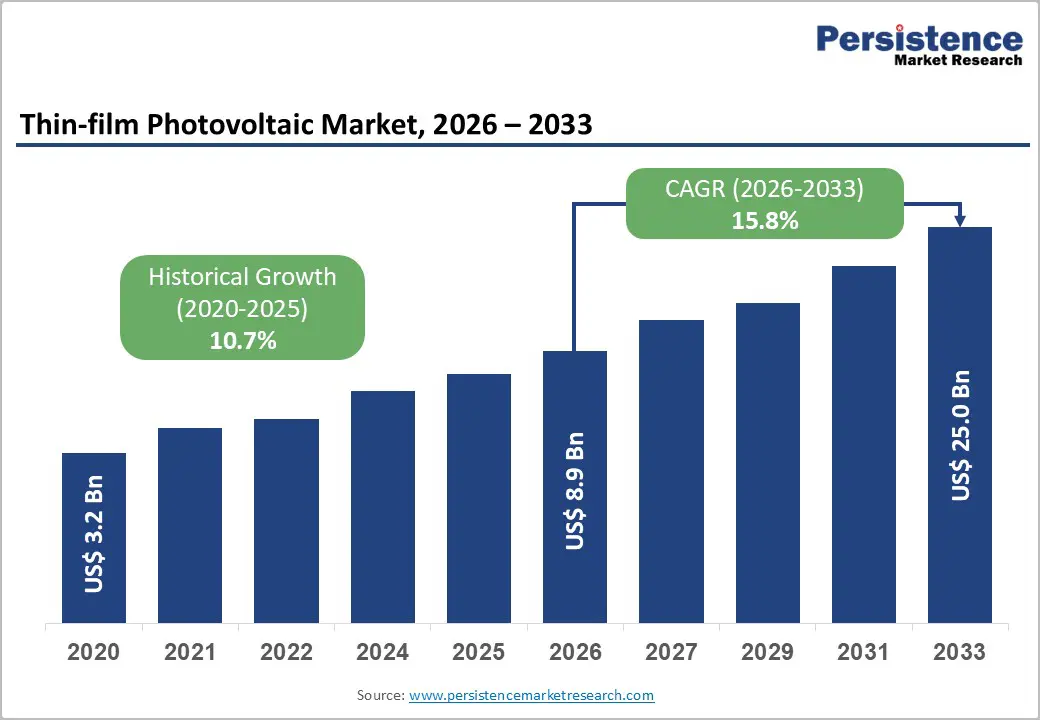

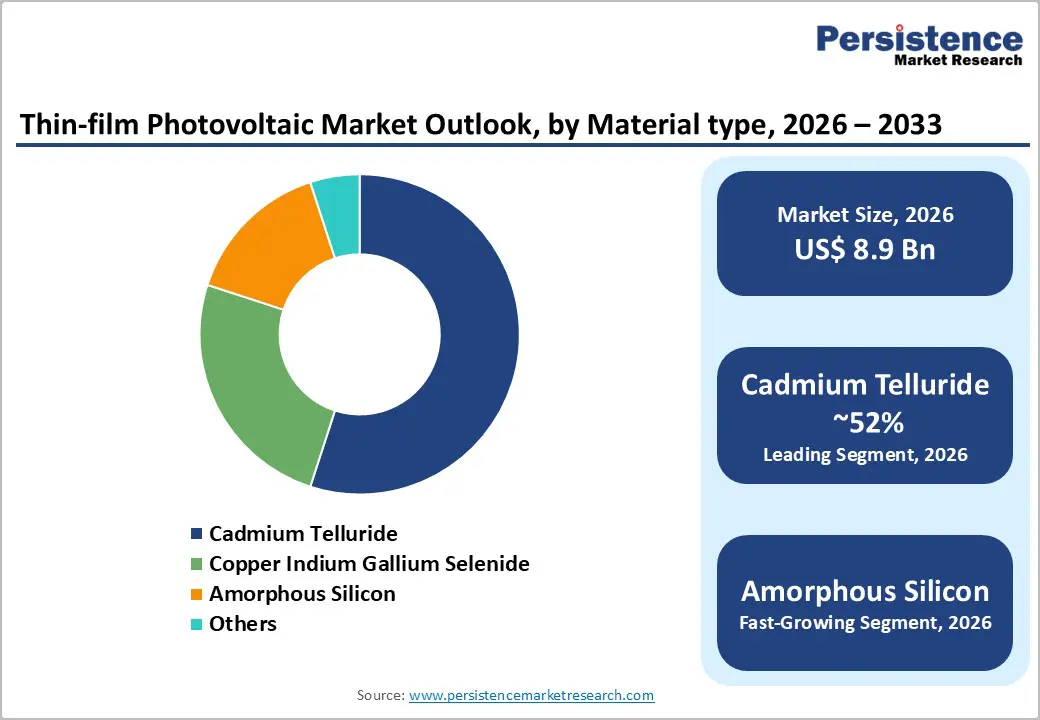

The global thin-film photovoltaic market size is likely to be valued at US$ 8.9 billion in 2026 and is projected to reach US$ 25.0 billion by 2033, growing at a CAGR of 15.8% between 2026 and 2033.

The market is driven by aggressive national solar targets mandating clean energy deployment, superior performance in high-temperature and low-light environments, differentiating thin-film from crystalline silicon, and rapid adoption in lightweight and flexible applications addressing architectural integration requirements.

Key Industry Highlights:

- Leading Material Type: Cadmium telluride dominates with 52% market share, driven by commercial maturity and cost-effectiveness; Amorphous silicon and perovskite are the fastest-growing, with a 21% CAGR, driven by efficiency breakthroughs exceeding 25% and environmental advantages.

- Dominant Film Type: Rigid substrates maintain 68% market share through proven durability and utility-scale optimization; Flexible film substrates represent the fastest-growing segment at a 28% CAGR, driven by BIPV architectural integration and transportation applications.

- Leading Component: Modules command 47% end-use focus through primary revenue concentration; Balance-of-system (BOS) components represent the fastest-growing at 22% CAGR, driven by system integration complexity and intelligent monitoring requirements.

- Dominant Application: Utility-scale installations maintain 43.2% deployment share through economies of scale and LCOE competitiveness; Commercial rooftop represents the fastest-growing at 20% CAGR, driven by net-zero building mandates and regulatory requirements.

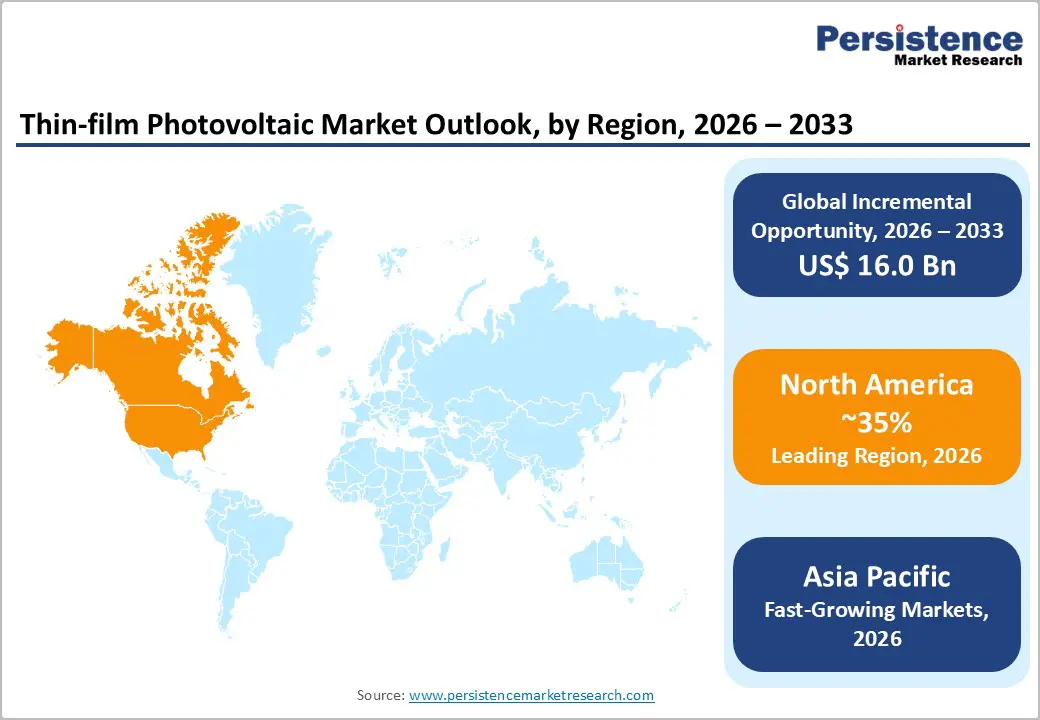

- Regional Market Dominance and Growth: North America maintains 35% global market share driven by First Solar manufacturing dominance and US incentive programs; Asia Pacific demonstrates the fastest regional growth at 18% CAGR, expanding from 30% current share to 45% by 2033.

- Technology and Market Innovation Momentum: Top 10 suppliers control 60% market share (First Solar, Oxford PV, Hanwha Q Cells leading); Perovskite efficiency achievements reaching 26% laboratory efficiency; Flexible substrate capability at 23.64% efficiency with 100,000+ flex cycle durability; multi-junction tandem advancement charting 30%+ efficiency pathways.

| Key Insights | Details |

|---|---|

| Thin-film Photovoltaic Market Size (2026E) | US$ 8.9 Bn |

| Market Value Forecast (2033F) | US$ 25.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 15.8% |

| Historical Market Growth (CAGR 2020 to 2024) | 10.7% |

Market Dynamics

Drivers - Rising Demand for Renewable Energy Spurs Market Growth

The global transition toward renewable energy sources is a leading growth driver for the thin-film PV industry. Countries worldwide are implementing policies to reduce greenhouse gas emissions and combat climate change.

As a clean, sustainable, and abundant resource, solar energy has emerged as a preferred choice for achieving these goals. Thin-film photovoltaics, with their lightweight and flexible nature, are increasingly integrated into solar farms, residential rooftops, and off-grid solutions.

Asia Pacific, particularly China and India, has shown significant adoption, driven by government incentives and large-scale installations. This high demand for renewable energy accelerates thin-film PV deployment and fosters investments in research and development, further enhancing the market’s growth trajectory.

Supportive Government Policies and Incentives Act as a Key Driver

Governments worldwide are promoting renewable energy adoption through favorable policies and financial incentives, which are significantly driving the thin-film PV industry. Subsidies, tax breaks, and feed-in tariffs make renewable energy projects more attractive to investors and consumers.

Initiatives like India's National Solar Mission and China's subsidies for solar energy projects have propelled the adoption of thin-film PV systems. These policies also encourage investment in infrastructure development and manufacturing capabilities, particularly in regions aiming to meet ambitious carbon-reduction targets.

Mandates for renewable energy integration into national grids and the rising emphasis on energy security are spurring the development of large-scale solar installations, including those using thin-film technologies. These measures ensure a robust market growth environment, fostering long-term adoption and innovation. For example,

- In 2024, China’s solar panel manufacturers sought government intervention to curb rampant investment and enhance industry collaboration, aiming to stabilize the market and ensure sustainable growth.

Restraints - Lower Efficiency Compared to Crystalline Silicon PV May Restrict Growth

One significant growth restraint for the thin-film photovoltaic industry is the comparatively lower efficiency of thin-film technologies compared to conventional crystalline silicon PV systems. Innovations have improved the efficiency of thin-film materials such as Cadmium Telluride (CdTe) and Copper Indium Gallium Selenide (CIGS).

They, however, still lag behind the 22-24% efficiency achieved by crystalline silicon panels. This gap limits the adoption of thin-film PV in applications where space efficiency is critical, such as residential rooftops.

Lower efficiency translates to a higher cost per watt for installation, making thin-film PV less attractive for cost-sensitive projects. Despite its advantages, such as flexibility and lightweight properties, the efficiency disparity remains a significant barrier to its widespread adoption, particularly in competitive solar energy markets.

Manufacturing Scale Constraints and Capital Intensity

High capital requirements, with thin-film manufacturing facilities requiring US$500 million- 1.5 billion investment per gigawatt capacity, limit new entrant participation and consolidate the supplier base. Technology risk perception, with end-users and investors viewing thin film as emerging compared to mature crystalline silicon, reducing financing availability and accelerating deployment commitment. Yield optimization complexity, with thin-film manufacturing requiring continuous process optimization and quality control establishing higher operational complexity versus crystalline silicon production. Supply chain constraints, with specialty material procurement (cadmium, indium, gallium, selenium) requiring long-lead-time ordering and geopolitical supply uncertainty affecting production planning.

Market size limitation, with thin film currently representing 3% global PV deployment versus 97% crystalline silicon, constrains investment capital allocation and manufacturer commitment. Competitive displacement risk, with crystalline silicon continuing to improve efficiency and reduce costs, maintaining a performance advantage in standard applications, limiting thin-film market penetration.

Opportunity - Growth of Building-integrated Photovoltaics is Set to Shape the Market

One of the most significant trends in the thin-film photovoltaic industry is the rising adoption of Building-Integrated Photovoltaics (BIPV). Thin-film PV technologies, with their lightweight, flexible, and customizable features, are particularly well-suited for integration into building materials such as windows, facades, and roofs.

Unlike traditional solar panels, BIPV solutions seamlessly blend into a building's architecture, serving both aesthetic and functional purposes. This trend is gaining momentum as governments worldwide enforce strict energy-efficiency regulations and green building standards. The European Union's push for zero-energy buildings by 2030 has encouraged widespread adoption of integrated solar solutions, including thin-film PV.

Technology’s ability to generate clean energy while reducing reliance on external power grids makes it highly attractive for urban environments with limited space. As more architects and developers incorporate sustainable energy solutions into their designs, demand for BIPV systems is set to drive growth in the thin-film PV industry. For instance,

- In April 2023, Ascent Solar Technologies, a developer of flexible thin-film solar modules, acquired the manufacturing equipment and licensed associated intellectual property from Flisom AG. It is a Swiss company specializing in lightweight, flexible thin-film solar modules.

Emerging Markets Manufacturing Localization and Cost Reduction

Asian manufacturing expansion, with India announcing 10 GW domestic thin-film capacity additions and Southeast Asia establishing tariff-free trade blocs attracting new fab investment, will establish a regional production foundation. Cost advantage opportunity, with regional production achieving 30-40% cost reduction versus developed-market manufacturing, enabling emerging market pricing and penetration. Labor efficiency benefit, with lower labor costs in emerging markets, reduces manufacturing operational expenses and improves overall supply chain economics. Technology transfer partnerships, with developed-market manufacturers establishing joint ventures and technology partnerships with emerging-market partners enabling knowledge transfer and capacity multiplication. Supply chain diversification, with geopolitical considerations driving manufacturers toward emerging market production reducing China dependency and establishing resilient supply chains.

Category-wise Analysis

Material Type Insights

Cadmium telluride (CdTe) dominates the market due to its high efficiency, established manufacturing processes, and cost-effectiveness compared to other thin-film technologies.

CdTe is estimated to hold the majority of the thin-film photovoltaic market share, accounting for nearly 52% of global installations. This dominance stems from its well-established supply chain, mature manufacturing processes, and extensive adoption by key players such as First Solar, a leading manufacturer of CdTe panels.

- Laboratory-scale CdTe solar cells have achieved efficiencies up to 21.5%, which is competitive with traditional crystalline silicon panels and other thin-film technologies, according to a 2023 NREL report.

- Commercially available CdTe modules exhibit efficiencies around 18 to 19%. These offer higher energy yields in real-world conditions compared to other thin-film options like CIGS and a-Si, especially under low-light conditions.

Depending on installation location, CdTe has the shortest energy payback time among all photovoltaic technologies, ranging from 8 to 12 months. Utilizing thin layers of cadmium and tellurium materials reduces material costs compared to other thin-film options. It often requires rare and expensive materials, such as indium and gallium.

Film Type Insights

The rigid type dominates the market due to its durability, mechanical stability, and suitability for large-scale installations. The segment is likely to hold a 68% share in 2026.

Rigid films are favored in utility-scale projects and commercial applications, contributing to their substantial market presence. Constructed on solid substrates such as glass, rigid films offer greater mechanical stability and longevity than their flexible counterparts.

Rigid films often achieve higher efficiency due to the use of stable substrates that support optimal thin-film deposition. The established manufacturing processes for rigid films reduce production costs, making them economically viable for large installations. Their robustness and efficiency also make these films ideal for utility-scale solar farms and commercial rooftops.

End-user Insights

Utility-scale applications hold 43.2% market share, driven by large deployment volumes and strong economies of scale. Cost competitiveness is a key factor, with CdTe thin-film systems achieving LCOE of US$ 20-25/MWh, matching or outperforming crystalline silicon in favorable climates. Performance advantages in high-temperature and low-light conditions deliver 3-5% higher energy output, supporting technology selection for large solar farms. Grid-scale expansion, with over 1,000 utility projects operating across North America, Europe, and Asia, reinforces market leadership. Standardized power purchase agreements and mature supply chains further strengthen investor confidence.

Commercial and residential rooftops are the fastest-growing segment, expanding at 20% CAGR through 2033. Net-zero building mandates, rooftop solar regulations, urban space constraints, aesthetic flexibility, thermal performance benefits, and the potential to offset BIPV costs are accelerating adoption, making rooftops the key growth engine.

Regional Insights

North America Thin-film Photovoltaic Market Analysis

North America commands approximately 35% of global Thin-Film Photovoltaic market share, valued at approximately US$ 3.6 billion in 2026 with projections approaching US$ 8.1 billion by 2033. The United States represents dominant regional market contributor, accounting for 85-88% of North American market value, while Canada and Mexico contribute emerging deployment contributions.

Utility deployment leadership, with First Solar's domestic manufacturing of 14 GW capacity and US utility pipelines in Southwest exploiting thin-film superior heat tolerance establishing 24% utility-scale deployment share. Incentive program acceleration, with Section 45X investment tax credits reducing module costs 30-40% and domestic-content requirements supporting regional manufacturing expansion. Regulatory framework support, with state-level solar mandates and net-zero building codes requiring 50% on-site renewable generation, establish systematic deployment demand. Agricultural integration, with agrivoltaic pilots pairing flexible laminates with crop cultivation, demonstrating dual-use land efficiency, and establishing emerging application sector.

Europe Thin-film Photovoltaic Market Analysis

Europe accounts for approximately 22% of the global thin-film photovoltaic market, valued at approximately US$ 2.5 billion in 2026. Germany, the United Kingdom, France, and Spain collectively account for 70% of the European market value, reflecting advanced regulatory frameworks and sustainability leadership.

Regulatory mandate implementation, with EU Solar Standard requiring rooftop PV on new buildings and building retrofits establishing 8,000-12,000 annual facility demand. Sustainability prioritization, with circular economy principles and environmental compliance supporting thin-film adoption through closed-loop recycling validation. Building renovation wave, with EU-funded modernization programs retrofitting 20-30 million buildings through 2033, establishing a massive integration opportunity. BIPV architecture growth, with European architects and engineers specifying thin film for aesthetic and performance advantages, drives premium positioning.

Asia Pacific Thin-film Photovoltaic Market Share and Trends

Asia Pacific demonstrates robust growth dynamics, commanding approximately 30% market share with projections increasing to 45% by 2033. The region valued at approximately US$ 2.76 billion in 2026 is anticipated to reach US$ 8.0 billion by 2033, representing the fastest-growing regional market with an estimated CAGR of 20%.

Manufacturing localization, with India announcing 10 GW of domestic capacity and China's established production dominance enabling cost-competitive pricing and a 30-40% regional manufacturing advantage, establishes a supply-chain foundation. Technology leadership investment, with Japan committing US$ 1.5 billion to perovskite research and commercialization, supporting a 20 GW deployment target by 2040. Emerging market affordability, with regional production and cost reduction, enables emerging economy adoption and solar democratization.

Competitive Landscape

The thin-film photovoltaic (PV) industry is highly competitive, driven by technological developments and rising applications. Key players such as First Solar, Ascent Solar Technologies, Solar Frontier, and Mitsubishi Electric dominate the market. They are leveraging expertise in Cadmium Telluride (CdTe), Copper Indium Gallium Selenide (CIGS), and Amorphous Silicon (a-Si) technologies.

Emerging players are investing in research and development to enhance efficiency and reduce costs. Asia Pacific, led by China, dominates production, while North America and Europe focus on integration into renewable energy policies.

Key Industry Developments

- In July 2024, First Solar, based in the U.S., initiated investigations into potential patent infringement by rival manufacturers involving the Tunnel Oxide Passivated Contact (TOPCon) technology.

- In December 2024, India announced that starting June 2026, clean energy companies must use photovoltaic (PV) modules made with locally produced cells from a list of government-approved companies.

Companies Covered in Thin-film Photovoltaic Market

- Global Solar Energy

- MiaSole

- Avancis GmbH

- Solar Frontier K.K.

- First Solar

- Kaneka Corporation

- Ascent Solar Technologies, Inc.

- Oxford Photovoltaics Ltd.

- Sharp Corporation

- Trony

- Others Key Players

Frequently Asked Questions

The Thin-film Photovoltaic market is estimated to be valued at US$ 8.9 Bn in 2026.

The key demand driver for the Thin-film Photovoltaic (PV) market is the rapid expansion of large-scale solar installations requiring lightweight, cost-efficiency, and flexible energy solutions.

In 2026, the North America region will dominate the market with an exceeding 35% revenue share in the global Thin-film Photovoltaic market.

Among the Material type, Cadmium Telluride holds the highest preference, capturing beyond % of the market revenue share in 2026, surpassing other Material type.

The key players in Thin-film Photovoltaic are Global Solar Energy, MiaSole, Avancis GmbH, Solar Frontier K.K. and First Solar.