- Chemicals and Materials

- High Speed Diesel (HSD) Market

High Speed Diesel (HSD) Market Size, Share, and Growth Forecast, 2026-2033

High Speed Diesel (HSD) Market by Product Type (Ultra-Low Sulfur Diesel, Low Sulfur Diesel, and High Sulfur Diesel), By Application (Automotive, Industrial, Marine, Agriculture, and Others), By Distribution Channel (Direct Sales, Indirect Sales), and Regional Analysis for 2026 – 2033

High Speed Diesel (HSD) Market Size and Trends Analysis

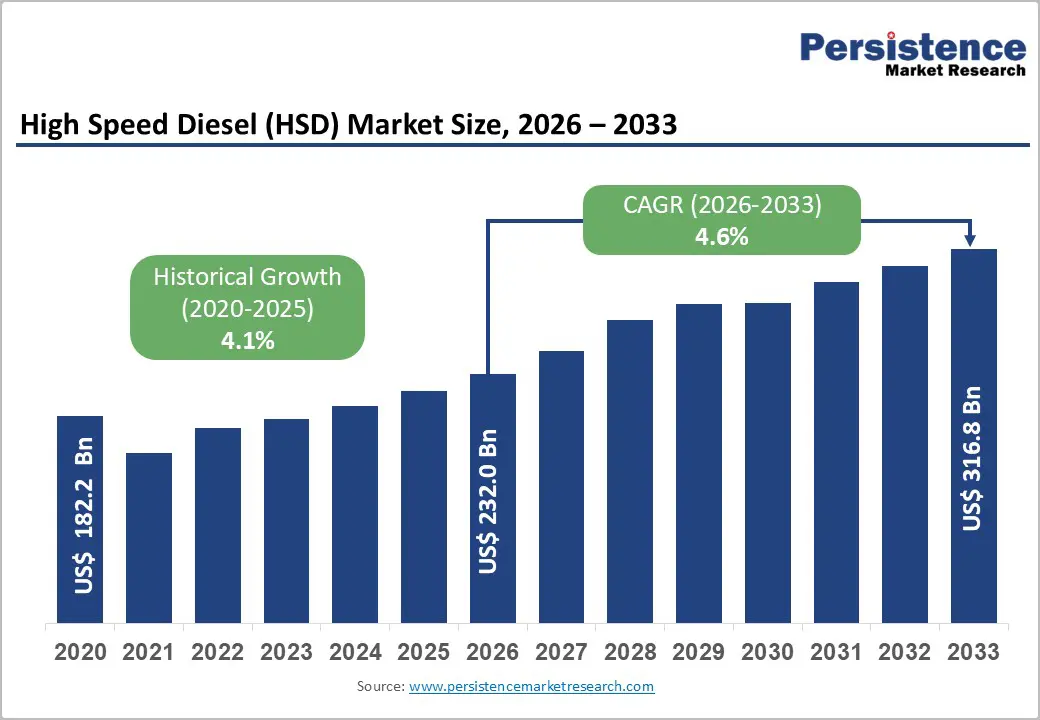

The global high speed diesel (HSD) market size was valued at US$ 182.2 billion in 2020 and reached US$ 232 billion in 2026, projected to reach US$ 316.8 Billion by 2033, growing at a CAGR of 4.6% during the forecast period (2026-2033). This growth trajectory reflects sustained demand from automotive transportation, industrial machinery operations, and agricultural mechanization across emerging and developed economies.

The market expansion is primarily driven by rising global vehicle production (particularly commercial vehicles), increased industrial activity in developing nations, and growing mechanization in the agricultural sector. The transition toward ultra-low sulfur diesel formulations and the ongoing evolution of emission standards continue to shape product mix evolution. Regional demand variations, particularly strong growth in Asia Pacific and North America, indicate divergent market maturity levels and regulatory environments influencing market structure.

Key Industry Highlights:

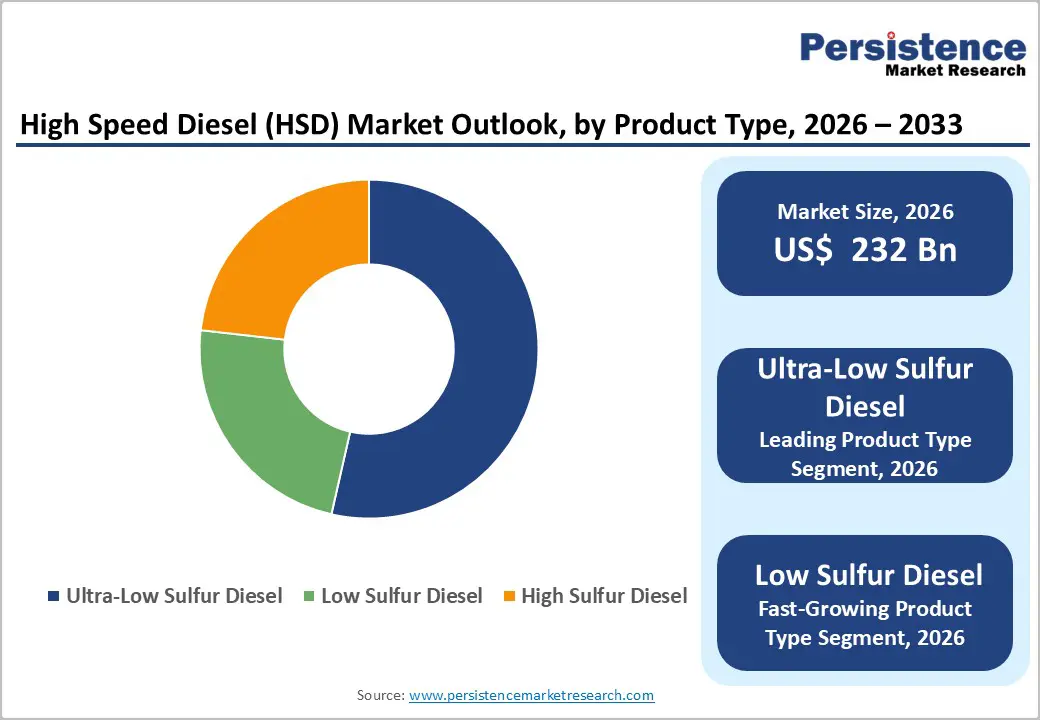

- Product Type Analysis: Ultra-Low Sulfur Diesel dominates the product mix with a 55%+ revenue share, while Low Sulfur Diesel is the fastest-growing segment at a 5.4% CAGR, reflecting the regulatory compliance transition and market segmentation across development levels.

- Application Analysis: Automotive applications command a 45%+ revenue share, with commercial vehicles representing the primary demand driver, while Industrial applications demonstrate a 5.6% CAGR, driven by manufacturing mechanization and backup power requirements in emerging markets.

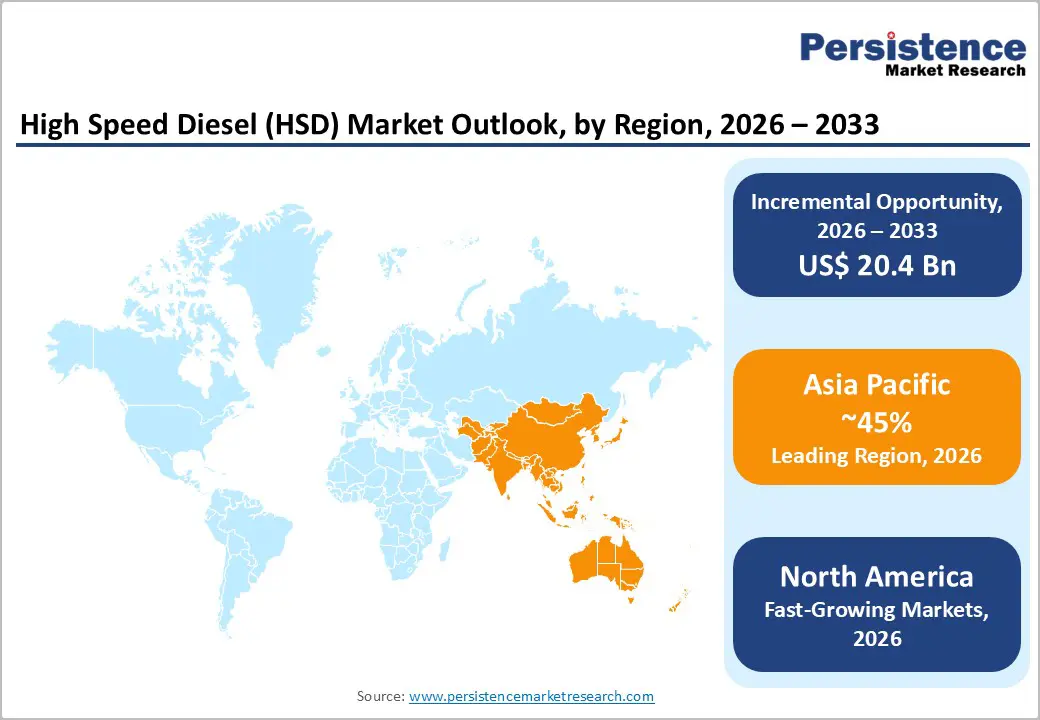

- Regional Analysis: Asia Pacific maintains a 45%+ global market share, driven by robust demand from China, India, and Southeast Asia, while North America is the fastest-growing region at a 5.3% CAGR, reflecting divergent regulatory trajectories and electrification adoption rates.

- Distribution Channel Analysis: Direct sales channels dominate with 65%+ revenue share, while Indirect sales through retail networks expand at 5.6% CAGR, reflecting ongoing market professionalization and retail infrastructure expansion.

- Strategic market developments emphasize renewable fuel integration, supply chain digitalization, and partnerships in commercial vehicle electrification, positioning market leaders for post-2033 transition scenarios while capturing near-term conventional fuel demand.

| Key Insights | Details |

|---|---|

| High Speed Diesel (HSD) Market Size (2026E) | US$ 232 Bn |

| Market Value Forecast (2033F) | US$ 316.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Dynamics

Key Growth Drivers

Rising Global Commercial Vehicle Production and Transportation Demand

Commercial vehicle registrations have demonstrated consistent growth, particularly in developing economies, where the expansion of logistics infrastructure drives diesel consumption. India's commercial vehicle market, for instance, recorded approximately 1.9 million units in 2022 (Society of Indian Automobile Manufacturers data), with diesel variants representing 55-60% of total commercial vehicle sales. The Asian Development Bank projects regional freight transportation volume growth of 6-7% annually through 2030, directly correlating to HSD demand expansion. Heavy-duty vehicles, including trucks, buses, and commercial construction equipment, remain highly dependent on diesel fuel due to its superior fuel efficiency, extended range, and engine durability. The global commercial vehicle market is projected to reach 35 million units annually by 2030, reflecting a compound growth rate that supports HSD consumption.

Market Restraining Factors

Stringent Environmental Regulations and Emission Standards

Global regulatory frameworks, including Euro VI (Europe), Bharat Stage VI (India), and California Air Resources Board (CARB) standards, impose significant compliance requirements on diesel fuel formulations and vehicle emissions. These standards necessitate investments in fuel-refining infrastructure, advanced engine technologies, and aftertreatment systems, thereby increasing production costs. The compliance burden disproportionately affects smaller refineries and distributors, creating market consolidation pressures. Environmental regulations simultaneously accelerate the transition toward alternative fuels (electric vehicles, hydrogen), potentially reducing long-term HSD market expansion rates.

High Speed Diesel (HSD) Market Trends and Opportunities

Advanced Diesel Formulations and Renewable Content Integration

Biodiesel blending mandates, implemented in over 60 countries globally, create opportunities for HSD product innovation and sustainability positioning. The European Union's renewable energy directive (RED III) mandates advanced biofuel targets of 5.5% by 2030, creating market expansion for renewable diesel blends. Global biodiesel production capacity, currently at approximately 48 million tons annually, is projected to reach 65+ million tons by 2033, directly creating demand for blending infrastructure and compatible diesel formulations. Synthetic diesel and hydrogenated vegetable oil (HVO) technologies represent premium-margin product categories, particularly in developed markets prioritizing carbon reduction objectives.

High Speed Diesel (HSD) Market Insights and Trends

Product Type Insights

Ultra-Low Sulfur Diesel Dominance and Low Sulfur Diesel Growth Dynamics

The global High-Speed Diesel (HSD) market demonstrates a clear structural shift toward cleaner fuel grades, driven by tightening emission norms and evolving engine technologies. Ultra-Low Sulfur Diesel (ULSD) currently dominates the market, accounting for over 55% of global revenue. This leadership reflects stringent regulatory mandates across developed economies and accelerating adoption in emerging markets. With sulfur content capped at 10 ppm, ULSD complies with advanced emission standards such as Euro VI and Bharat Stage VI. India’s nationwide BS VI transition in 2020 significantly boosted ULSD penetration, which now exceeds 85% among major refiners. Beyond regulation, ULSD benefits from superior emission performance, compatibility with advanced aftertreatment systems like diesel particulate filters and selective catalytic reduction units, and lower long-term maintenance costs. These advantages support a price premium of 8–15% over conventional diesel and drive structural demand, as OEMs increasingly mandate ULSD usage to maintain vehicle warranties.

In contrast, Low Sulfur Diesel (LSD) is the fastest-growing segment, projected to expand at a CAGR of 5.4% during the forecast period. Containing 50–500 ppm sulfur, LSD serves as a transitional fuel in developing economies adopting intermediate emission standards. Countries moving gradually toward stricter norms, such as parts of Southeast Asia, are driving LSD demand, particularly for secondary commercial fleets and agricultural machinery. Its lower production cost compared to ULSD and adequate regulatory compliance make LSD an attractive option for price-sensitive markets, supporting its rapid growth trajectory.

Application Insights

Automotive Dominance and Rapid Industrial Growth Shape Global HSD Demand

The application landscape of the High-Speed Diesel (HSD) market is primarily defined by the automotive and industrial sectors, together accounting for the bulk of global consumption. The automotive segment remains the dominant application, contributing over 45% of total HSD revenue. This leadership is largely driven by commercial vehicles such as trucks, buses, and light commercial pickups, where diesel engines offer structural advantages. High torque output, 15–25% higher fuel efficiency than gasoline engines, and lower operating costs make HSD indispensable for long-haul freight, public transport, and logistics operations. In India alone, annual diesel consumption for automotive use is estimated at 65–70 million kiloliters, with commercial vehicles accounting for nearly 55–60% of this demand. In Europe, although diesel passenger-car penetration has declined from its 2015 peak, diesel still accounts for 60–70% of commercial-vehicle sales, underscoring its continued relevance.

In contrast, the industrial segment represents the fastest-growing application, expanding at an estimated CAGR of 5.6%. Growth is fueled by manufacturing expansion, rising reliance on diesel-based captive and standby power generation, and increased mechanization. Industrial diesel generators remain critical in regions with unreliable grid infrastructure, particularly across South Asia and Sub-Saharan Africa. Additionally, agricultural mechanization, especially diesel-powered irrigation pumps, numbering 35–40 million units in South Asia, continues to support steady HSD consumption due to limited electrification alternatives in dispersed rural settings.

Sales Channel Insights

Direct Sales Dominance and Rapid Growth of Indirect Fuel Distribution Channels

The distribution channel structure of the fuel market is strongly shaped by its B2B-oriented consumption pattern, with direct sales emerging as the clear market leader. Direct sales account for over 65% of total revenue, reflecting the dominance of bulk fuel procurement by commercial fleet operators, industrial users, power generators, and large agricultural consumers. Oil marketing companies typically maintain long-term, direct relationships with these customers through dedicated delivery infrastructure such as tankers and on-site storage facilities. This channel supports volume-based pricing, flexible credit terms, and long-term supply contracts, which are essential for customers with predictable, high-volume fuel consumption. In several emerging economies, government-owned fuel retailers rely heavily on direct sales to manage bulk distribution efficiently while ensuring pricing transparency, supply security, and regulatory oversight.

In contrast, indirect sales channels primarily retail fuel stations and authorized distributors represent the fastest-growing segment, expanding at an estimated CAGR of 5.6%. Growth is driven by the rapid expansion of retail pump networks, particularly in developing markets where annual outlet growth ranges between 4% and 6%. These channels cater to fragmented demand from small farmers, local transport operators, and small industrial users. Additionally, the adoption of digital payment systems, fuel cards, and prepaid fuel management platforms is strengthening the role of retail infrastructure by improving transaction convenience, transparency, and accessibility, thereby accelerating indirect channel growth.

Regional Insights and Trends

Asia Pacific Dominance Driven by Industrial, Transport, and Agricultural Diesel Demand

Asia Pacific is the most dominant regional market in the global High-Speed Diesel (HSD) landscape, accounting for over 45% of total revenue. This leadership position is underpinned by the region’s expansive industrial base, strong transportation demand, and continued reliance on diesel-powered equipment across agriculture and manufacturing. China remains the single largest contributor within the region, with annual diesel consumption estimated at approximately 110–115 million tons. The country’s demand is heavily concentrated in industrial operations, freight transportation, construction activity, and large-scale infrastructure development, reinforcing diesel’s role as a critical energy source despite ongoing energy transition efforts.

India stands as the second major growth engine in the Asia-Pacific HSD market, with annual consumption ranging from 65–70 million kiloliters. The Indian market is expanding at a healthy CAGR of around 4.2%, supported by rising commercial vehicle sales, sustained logistics activity, and increasing agricultural mechanization. Diesel remains the preferred fuel for tractors, harvesters, irrigation pumps, and heavy trucks, particularly in rural and semi-urban regions where alternative fuels and electrification remain limited.

Beyond China and India, Southeast Asian economies are contributing steadily to regional growth. Expanding manufacturing hubs, export-oriented industrialization, and infrastructure investments in countries such as Indonesia, Vietnam, and Thailand are strengthening diesel demand. Collectively, these structural factors ensure Asia Pacific’s continued dominance in the global HSD market over the medium term.

North America’s Diesel Market Growth Driven by Infrastructure and Commercial Demand

North America is emerging as the fastest-growing regional market, recording an estimated compound annual growth rate (CAGR) of around 5.3%, supported by a unique balance between energy transition goals and sustained diesel demand. Unlike Europe, where commercial vehicle electrification is progressing rapidly, electrification in North America is occurring at a comparatively slower pace, particularly in the medium- and heavy-duty segments. This slower transition continues to underpin strong diesel consumption across freight transport, construction, and logistics applications.

The United States remains the primary growth engine, where steady expansion of the commercial vehicle fleet, coupled with large-scale federal and state infrastructure investment programs, is sustaining diesel demand in road construction, mining, and material handling. Significant funding for highways, bridges, ports, and energy infrastructure is translating directly into higher utilization of diesel-powered construction equipment and transport vehicles.

Canada and Mexico further reinforce regional growth through robust industrial activity, cross-border trade, and manufacturing expansion, particularly in automotive, mining, and oil & gas support services. Additionally, regulatory framework harmonization across North America is improving fuel quality consistency, encouraging the adoption of advanced and cleaner diesel formulations. This shift supports premium product positioning, enabling suppliers to capture higher margins while meeting tightening emission and performance standards. Collectively, these factors position North America as a resilient, high-value growth market within the global diesel landscape.

High Speed Diesel (HSD) Market Competitive Landscape

The global HSD market exhibits moderate consolidation characteristics, with top 10 players controlling approximately 35-40% of market supply through integrated refining and distribution operations. Oil majors (ExxonMobil, Shell, BP, TotalEnergies, Chevron) and national oil companies (Saudi Aramco, CNPC, Gazprom, Indian Oil, CNOOC) dominate supply infrastructure, leveraging integrated upstream-downstream operations and established distribution networks. Mid-tier independent refiners and specialized fuel traders occupy secondary market positioning, competing through regional distribution efficiency and specialty product formulations. Market consolidation reflects capital intensity of refining infrastructure and regulatory compliance requirements creating barriers to new entrant competition.

Key Industry Developments:

- In 2024, Shell announced expansion of renewable fuel production capacity in the Netherlands (March 2024), investing approximately US$ 800 million in conversion of hydrocracking facilities to produce sustainable aviation fuel (SAF) and renewable diesel products.

- In 2023, Indian Oil Corporation implemented advanced fuel quality monitoring systems across distribution networks in partnership with digital technology providers, enhancing supply chain transparency and fuel authenticity verific

Companies Covered in High Speed Diesel (HSD) Market

- Royal Dutch Shell Plc

- BP Plc

- Chevron Corporation

- ExxonMobil Corporation

- TotalEnergies SE

- China National Petroleum Corporation (CNPC)

- Saudi Aramco

- Kuwait Petroleum Corporation

- Petrobras

- Gazprom

- Indian Oil Corporation Ltd

- Sinopec Limited

- Phillips 66

- Valero Energy Corporation

- Petronas

- Lukoil

- Repsol S.A.

- Eni S.p.A.

- Other Market Players

Frequently Asked Questions

The High Speed Diesel (HSD) market is estimated to be valued at US$ 232 Bn in 2026.

The primary demand driver for the High Speed Diesel (HSD) market is the continued reliance on diesel-powered commercial vehicles, construction equipment, and industrial machinery, particularly in regions where electrification and gas substitution remain gradual.

In 2026, the Asia Pacific region will dominate the market with an exceeding 45% revenue share in the global High Speed Diesel (HSD) market.

Among applications, automotive has the highest preference, capturing beyond 45% of the market revenue share in 2026, surpassing other applications.

Royal Dutch Shell Plc, BP Plc, Chevron Corporation, ExxonMobil Corporation, TotalEnergies SE, China National Petroleum Corporation (CNPC), and Saudi Aramco. There are a few leading players in the High Speed Diesel (HSD) market.