- Pharmaceuticals

- Biological Drugs Market

Biological Drugs Market Size, Share, and Growth Forecast, 2025 - 2032

Biological Drugs Market By Product Type (Monoclonal Antibodies (mAbs), Immune Checkpoint Inhibitors, Biosimilars, Others), Therapeutic Area (Oncology, Cardiovascular Diseases, Others), Delivery Method (Injectable, Oral), and Regional Analysis for 2025 - 2032

Biological Drugs Market Share and Trends Analysis

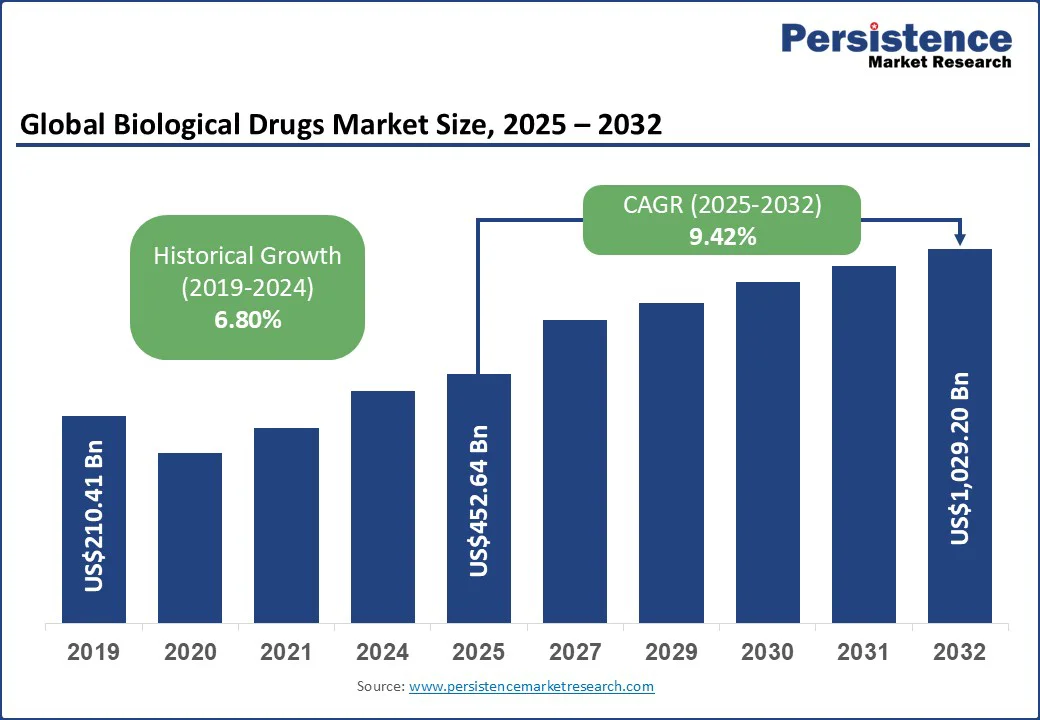

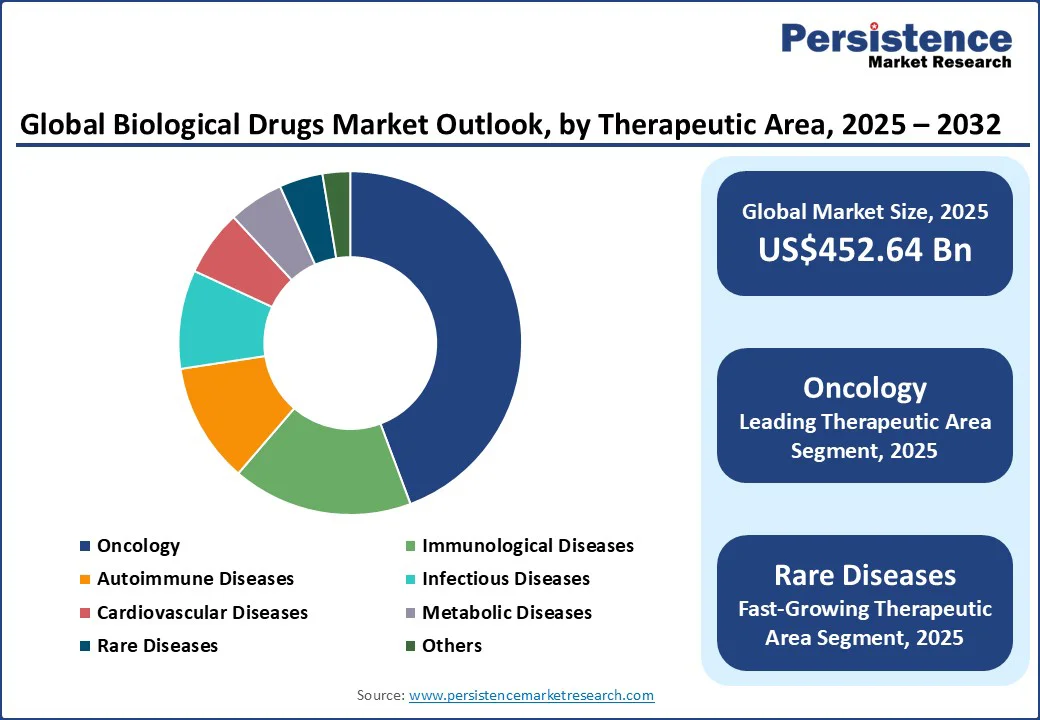

The global biological drugs market size is likely to reach US$452.64 Bn in 2025 and is expected to reach US$1,029.20 Bn by 2032 growing at a CAGR of 9.42% during the forecast period from 2025 to 2032.

Rising adoption of gene therapies, personalized immunotherapies, and the surge in biosimilars are key drivers fueling market growth.

Biological drugs, comprising complex therapies engineered from living cells, are redefining the pharmaceutical landscape with unparalleled precision and effectiveness, especially in oncology, rare diseases, and autoimmune disorders. Advanced biotechnologies, such as monoclonal antibodies and mRNA vaccines, enable ground-breaking treatments that traditional drugs often cannot provide.

Globally, the biological drugs market is poised for dynamic growth, driven by the rising global burden of cancer and rare diseases, increasing demand for targeted biologics, and a rapidly expanding biosimilars sector. Recent milestones, such as novel antibody-drug conjugate launches and accelerated mRNA vaccine deployment, have propelled R&D investments and spurred cross-industry collaborations. With advances in smart, modular manufacturing streamlining production, the market is primed for unforeseen opportunities.

Key Industry Highlights:

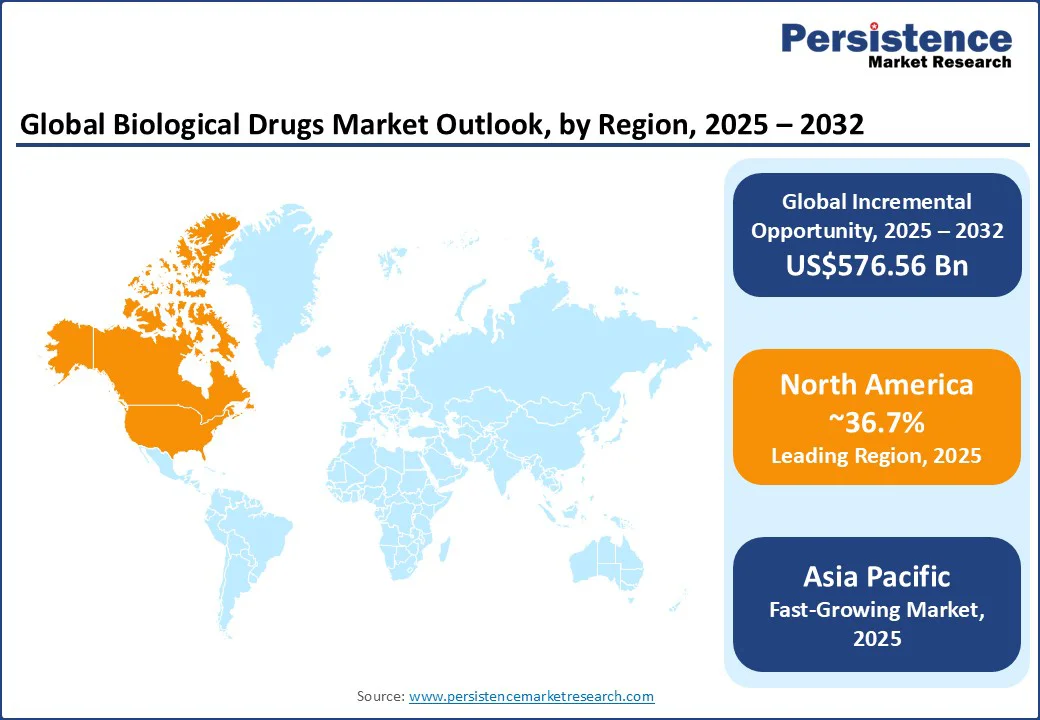

- Dominant Region: North America is projected to dominate, holding a share of approximately 36.7% in 2025, supported by advanced healthcare infrastructure, regulatory support for novel therapeutics, and strong R&D investments in biopharmaceuticals.

- Fastest-growing Regional Market: Asia Pacific is the fastest-growing regional market with an expected CAGR of 11.5% through 2032, driven by expanding access to modern healthcare solutions, rising chronic disease prevalence, and favorable government policies in India and China.

- Leading Therapeutic Area: Oncology is projected to lead the therapeutic area segment in 2025 with a share of approximately 44.3%, mainly owing to the explosion of new cancer cases over the past few decades across the globe.

- Fastest-growing Therapeutic Area: The rare diseases segment is likely to display the highest CAGR of approximately 16% through 2032, driven by a surge in orphan drug development and growing awareness of rare conditions.

- Investment Focus: Innovations in next-generation biologics, including gene and cell therapies, bispecific antibodies, and mRNA vaccines, represent high-return growth opportunities in the biologics market.

|

Global Market Attribute |

Key Insights |

|

Biological Drugs Market Size (2025E) |

US$452.64 Bn |

|

Market Value Forecast (2032F) |

US$1,029.20 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

9.42% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.80% |

Market Dynamics

Driver - Increasing Prevalence of Chronic and Rare Diseases Worldwide to Drive the Demand for Targeted Therapeutics

The biological drugs market growth is set for an upward trajectory owing to the escalating prevalence of chronic and rare diseases, particularly cancer, autoimmune disorders, and metabolic conditions, creating an urgent global demand for highly targeted, efficacious biologic therapies. According to the World Health Organization (WHO), nearly 10 million cancer deaths occurred in 2023, while autoimmune diseases afflict over 20 million people worldwide.

As per the International Diabetes Federation (IDF), diabetes currently affects 589 million adults globally, and the number is expected to hit 853 million by 2050. This growing disease burden has necessitated the development of precision medicines such as monoclonal antibodies and gene therapies that biologics uniquely provide, offering superior treatment outcomes over conventional small-molecule drugs.

For example, in the case of cancer, biological therapies work by stimulating the immune system to attack cancer cells or by making them easier for the immune system to detect. In essence, biological drugs have emerged as a transformative tool in combating diseases that were previously considered incurable.

Restraint - Supply Chain Vulnerabilities and Manufacturing Scalability Issues to Hamper Market Prospects

Intricate supply chain vulnerabilities and scalability limitations inherent in biologics manufacturing are two of the biggest challenges hindering the forward movement of this market. Unlike conventional pharmaceuticals, biologics require highly specialized raw materials, strict cold chain logistics, and complex multi-step production processes that are sensitive to contamination and variability. Disruptions at any stage, from sourcing bioreagents or cell lines to fill-finish operations, can delay product availability and triggers costs.

Sudden global events, such as the COVID-19 pandemic and recent tariff wars, have caused supply disruptions and raw material shortages, highlighting these vulnerabilities. Moreover, scaling biologics production to meet the soaring global need for targeted therapeutics remains technologically and economically demanding, as the current single-use bioreactors and bioprocessing facilities are functioning at limited capacity. This complex interplay of supply chain fragility and manufacturing scale-up constraints poses a formidable barrier to market expansion and operational efficiency in the biopharmaceutical sector.

Opportunity - Precision Medicine and Next-Generation Therapeutics to be Upcoming Growth Frontiers

An incredibly lucrative opportunity for players in the biological drugs market lies in the rapidly expanding domain of precision medicine and next-generation biologics, including gene and cell therapies, bispecific antibodies, and mRNA-based treatments. This niche is transforming patient care by enabling highly targeted interventions tailored to individual genetic and molecular profiles, considerably improving therapeutic outcomes in oncology, rare genetic disorders, and autoimmune diseases.

For instance, a 2022 review published by a team of Canadian researchers in Frontiers in Pharmacology highlights that biologic therapies targeting eosinophilic (Type 2) inflammation, such as monoclonal antibodies against IgE, IL-4, and IL-5, have shown the greatest success in improving outcomes for severe asthma patients, though many still experience only modest reductions in exacerbation rates and some show sub-optimal responses.

These variations underscore the growing need for precision medicine by tailoring treatments based on each patient’s distinct immunological profile. Recent breakthroughs such as the FDA approval of innovative CAR-T therapies and the widespread adoption of mRNA vaccines reiterate the commercial and clinical potential of precision biologics. Furthermore, AI-driven drug discovery and modular manufacturing technologies have enabled the optimization of development timelines and reduced costs, enhancing accessibility and scalability.

Category-wise Analysis

Therapeutic Area Insights

The leading therapeutic area segment in 2025 for the biological drugs market is oncology, expected to command an estimated share of around 44.3%. Oncology biologics dominate, due to the rapidly rising incidence of cancer worldwide, with new cases projected to reach 30 million by 2030, as per the WHO, and the lengthy pipeline of targeted monoclonal antibodies, antibody-drug conjugates, and immune checkpoint inhibitors that offer improved efficacy and survival.

Drugs such as pembrolizumab (Keytruda) and nivolumab (Opdivo) have revolutionized cancer treatment, fueling market growth. This segment also benefits from accelerated regulatory approvals and public-private R&D investments focused on personalized medicine and immunotherapy advancement.

The rare diseases segment is likely to exhibit the highest CAGR of around 16% through 2032, on account of the surge in orphan drug development and increasing awareness about rare illnesses. Rare disease biologics offer personalized, often first-in-class therapies addressing genetic disorders and unmet clinical needs, supported by incentivizing orphan drug policies globally.

Recent FDA approvals for gene therapies such as Zolgensma for spinal muscular atrophy signify unprecedented breakthroughs that command premium pricing and market expansion. Advancements in next-generation sequencing technology are accelerating rare disease diagnosis and empowering the development of targeted therapies, further driving segment growth.

Product Type Insights

Monoclonal Antibodies (mAbs) are anticipated to dominate with an approximate revenue share of 65% in 2025, driven by their targeted efficacy against complex diseases such as cancers, rheumatoid arthritis, and multiple sclerosis. The specificity of mAbs in binding to cancer cell antigens (HER2 in breast cancer) enables superior clinical outcomes compared to conventional therapies.

Innovations related to bispecific antibodies and antibody-drug conjugates (ADCs) further amplify the therapeutic and commercial appeal of monoclonal antibodies. For instance, ADCs such as Trastuzumab emtansine (Kadcyla) combine selective targeting with cytotoxic payload delivery, broadening treatment horizons in oncology.

The cell and gene therapy segment is set to register a meteoric CAGR from 2025 to 2032, powered by breakthroughs in CAR-T therapies, CRISPR-based editing, and viral vector technologies. These therapies offer curative potential for hematologic malignancies, rare genetic disorders, and certain metabolic diseases, transcending symptomatic treatment to address the root causes of diseases.

The U.S. FDA’s rapid approvals of CAR-T products such as Kymriah and Yescarta have galvanized investments and commercialization efforts. The concurrent integration of artificial intelligence in therapy design and scalable manufacturing innovations, including modular, single-use bioreactors, is further elevating feasibility and expanding market reach.

Regional Insights

North America Biological Drugs Market Trends

North America is the leading regional market in 2025, estimated to hold approximately 36.7% of the share. This top position of the region is due to its robust healthcare infrastructure, early adoption of cutting-edge biotechnological solutions, a mature and highly regulated pharmaceutical ecosystem, and substantial venture capital funding for R&D purposes.

The U.S., representing nearly 89% of the North America biologics market, benefits significantly from timely regulatory approvals and broad biosimilar adoption, thereby lowering costs and boosting accessibility. Oncology and immunology biologics lead the demand, aided by increasing cancer incidence and autoimmune diseases in the region. Strategic collaborations between biotech startups and established pharma companies will continue to bolster pipeline innovation among public and private players across the U.S. and Canada.

Asia Pacific Biological Drugs Market Trends

Asia Pacific is set to be the fastest-growing regional market with a high CAGR through 2032. Market growth in the region is driven by a rapidly strengthening medical R&D ecosystem and a robust pharmaceutical industry in India and China, alongside rising chronic disease rates, increased biopharma investments, and regulatory reforms that encourage local biologics innovation.

In China, leading with 39.2% regional revenue share, the market growth is supported by aggressive government initiatives, rising R&D activities by domestic pharma companies, and a large patient pool demanding affordable, high-quality biologics and biosimilars. On the other hand, India’s improving regulatory framework and manufacturing capabilities are envisaged to brighten market prospects.

Europe Biological Drugs Market Trends

Europe is expected to account for about 26% of the global biologics market in 2025, supported by major pharmaceutical hubs such as Germany, France, and the U.K. The expansion of the regional market is gaining momentum due to the stringent implementation of regulatory mandates emphasizing safety and sustainability in the pharma industry, significant public funding for biotechnological research, and a long history of biologics development on the continent.

Germany alone holds a sizable stake in Europe, with a higher growth rate expected from AI integration in biologics R&D and personalized medicine approaches. The rising burden of autoimmune and infectious diseases in Europe will further stoke the regional demand for biologics, alongside innovative public-private partnerships accelerating pipeline progress.

Competitive Landscape

The global biological drugs market is highly competitive, shaped by rapid technological innovations, strategic collaborations, and evolving regulatory environments. Companies are ramping up their investments in advanced manufacturing technologies such as single-use bioreactors and modular facilities, enabling scalable, good manufacturing practice (GMP)-compliant production that meets the soaring global demand for biological drugs. Growing focus on AI and machine learning is transforming biologics R&D by speeding drug discovery and optimizing protein engineering, giving companies a strong competitive edge.

Collaborative ecosystems involving biotech startups, contract development and manufacturing organizations (CDMOs), and large pharmaceutical firms are fueling robust pipelines, especially in oncology, immunology, and rare diseases, while regulatory incentives and biosimilar market penetration enhance market accessibility and cost-effectiveness.

Key Industry Developments

- In August 2025, WuXi Biologics’ Dundalk site in Ireland received European Medicines Agency (EMA) approval for its first commercial biologic launch, supporting a global client. The milestone will boost WuXi’s “Global Dual Sourcing Strategy” by enabling flexible, multi-site production.

- In June 2025, at its Oncology R&D Day, Innovent Biologics launched a dual-innovation strategy focused on next-gen IO and ADC platforms. Backed by ~10 advanced molecules and global R&D in Shanghai and San Francisco, the company targeted five assets in multi-regional Phase 3 trials by 2030, led by IBI363, a first-in-class PD-1/IL-2 fusion protein with breakthrough designations.

- In May 2025, Merck broke ground on a US$1 Bn, 470,000 sq. ft. biologics hub in Wilmington, Delaware, its first in-house U.S. site for Keytruda. The facility will produce next-gen therapies, including ADCs, with partial operations by 2028 and full-scale production by 2030. The move supported Merck’s push for domestic manufacturing and supply chain resilience.

Companies Covered in Biological Drugs Market

- Amgen Inc.

- Johnson & Johnson Services, Inc.

- Roche Holding AG

- Pfizer Inc.

- Novartis AG

- AbbVie Inc.

- Bristol-Myers Squibb Company

- Merck & Co., Inc.

- Regeneron Pharmaceuticals, Inc.

- Sanofi S.A.

Frequently Asked Questions

The biological drugs market is projected to reach US$452.64 Bn in 2025.

The rise in prevalence of chronic and rare diseases, particularly cancer, autoimmune disorders, and metabolic conditions, worldwide is driving the market.

The biological drugs market is expected to grow at a CAGR of 9.42% from 2025 to 2032.

The rapidly expanding domain of precision medicine and next-generation biologics, including gene and cell therapies, and the adoption of AI-driven drug discovery and modular manufacturing technologies by pharmaceutical companies are key market opportunities.

The key players include Amgen Inc., Johnson & Johnson Services, Inc., and Roche Holding AG.