- Media & Entertainment

- Healthcare AR VR Market

Healthcare AR VR Market Size, Share, and Growth Forecast 2026 - 2033

Global Healthcare AR VR Market by Technology Type (Augmented Reality (AR) and Virtual Reality (VR)), Component (Hardware, Software, and Services), Application (Patient Care Management, Medical Training, Surgery Planning, Rehabilitation, and Others), End User (Hospitals & Clinics, Medical Research Organizations, Diagnostic Centers, and Others), and Regional Analysis

Healthcare AR VR Market Size and Share Analysis

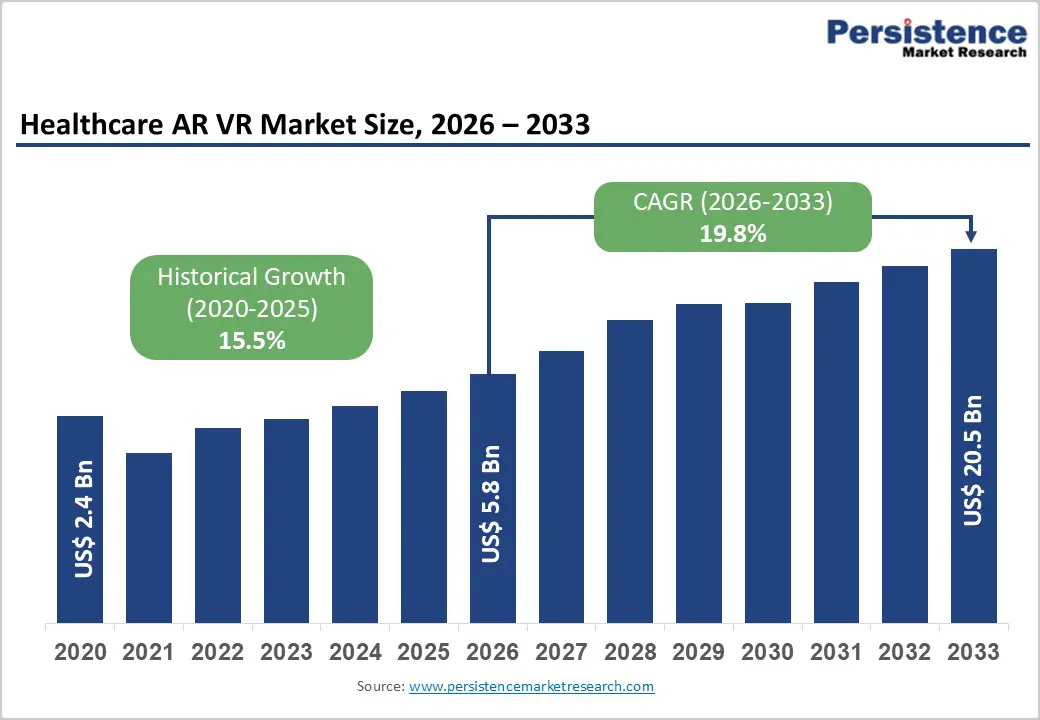

The global healthcare AR VR market size was valued at US$ 5.8 billion in 2026 and is projected to reach US$ 20.5 billion by 2033, growing at a CAGR of 19.8% between 2026 and 2033. The market's exceptional expansion is driven by unprecedented adoption of immersive technologies for medical training, surgical planning, patient care management, and therapeutic applications across healthcare systems worldwide. The integration of 5G connectivity, artificial intelligence, and advanced sensor technologies is creating unprecedented opportunities for real-time remote surgery, immersive telemedicine, and AI-powered personalized therapeutic interventions.

Key Market Highlights

- Leading Region: North America dominates with 41% market share, supported by exceptional healthcare infrastructure, substantial research investment, advanced regulatory frameworks, and pioneering institutional adoption position North America.

- Fastest Growing Region: Asia Pacific fastest-growing region at 28% CAGR, driven by rapid digital transformation, surging medical technology investments, and accelerating healthcare infrastructure modernization across China, India, and Southeast Asia.

- Dominant Application: Surgery Planning dominates applications with 38% market share with exceptional clinical value in preoperative planning, intraoperative navigation, and surgical guidance drives market leadership.

- Growing Technology: Virtual Reality fastest-growing technology at 58% market share, VR's exceptional effectiveness in surgical training, therapeutic pain management, and rehabilitation applications drives technology dominance.

- Dominant Component: Hardware segment commands 67% market share with software as fastest-growing component, driven by advanced head-mounted displays, spatial computing platforms, and specialized medical-grade visualization devices drive hardware dominance.

| Report Attribute | Details |

|---|---|

|

Global Healthcare AR VR Market Size (2026E) |

US$ 5.8 Bn |

|

Market Value Forecast (2033F) |

US$ 20.5 Bn |

|

Projected Growth CAGR (2026-2033) |

19.8% |

|

Historical Market Growth (2020-2025) |

15.5% |

Market Dynamics

Market Growth Drivers

Growing Adoption of Immersive Medical Training and Surgical Simulation Platforms

The healthcare industry is undergoing a fundamental transformation in medical education and surgical skill development through immersive virtual reality training platforms. Surgical simulation adoption has emerged as the fastest-growing application segment, with 77% of healthcare organizations surveyed reporting implementation of VR to support medical training or planning to do so. Osso VR, the leading procedural-skills training platform, is utilized by more than 100,000 healthcare professionals across 35 countries, with published research demonstrating trainees achieve 230% to 300% greater proficiency compared to traditional training methodologies.

The superior learning outcomes, reduced training costs, and elimination of inherent risks associated with live-patient practice create compelling economic justification for healthcare systems prioritizing surgical excellence and resident competency acceleration. Virtual reality surgical simulations enable deliberate practice, immediate feedback, and customizable scenario-based learning that traditional operating room observation cannot replicate. Medical schools and residency programs increasingly recognize immersive training as essential infrastructure, with universities integrating VR anatomy visualization and emergency response protocols into standard curricula, fundamentally reshaping how healthcare professionals acquire foundational clinical competencies.

FDA Regulatory Approval and Reimbursement Recognition of Therapeutic VR Applications

Regulatory approval milestones are significantly accelerating commercial adoption of therapeutically efficacious AR/VR applications through expanded reimbursement pathways and clinical validation frameworks. The FDA's November 2021 authorization of AppliedVR's EaseVRx (now RelieVRx) as a prescription-use immersive virtual reality system for chronic lower back pain treatment represented a historic inflection point, establishing virtual reality as a legitimate medical therapeutic modality eligible for clinical reimbursement. Clinical evidence demonstrates RelieVRx achieves pain reduction in over 60% of chronic pain patients, with outcomes particularly compelling for patient populations seeking non-pharmacological alternatives to opioid interventions.

The FDA has progressively expanded its approval framework, with 92 AR/VR medical devices now authorized for marketing, representing 68% cumulative annual growth in cleared submissions from 2015 through 2024. This regulatory momentum is driving substantial venture capital investment into therapeutic VR companies, with AppliedVR securing USD 36 million in Series B funding and establishing clinical research partnerships with prominent healthcare institutions including Cedars-Sinai, Cleveland Clinic, and National Institutes of Health (NIH) divisions.

Market Restraints

Substantial Capital Investment Requirements and Complex Regulatory Pathway Barriers

Healthcare AR/VR technology implementation faces significant financial and regulatory barriers limiting adoption rate acceleration across smaller healthcare institutions, underserved markets, and emerging economies. Hardware systems including advanced head-mounted displays, spatial computing platforms, and integration infrastructure typically require capital expenditures of USD 50,000 to 250,000 per installation, creating prohibitive financial barriers for resource-constrained healthcare facilities, rural hospitals, and developing market healthcare systems. The FDA's complex regulatory classification framework creates uncertainty regarding whether specific applications require 510(k) clearance, de novo pathway approval, or regulatory exemption, necessitating specialized regulatory expertise and extending time-to-market significantly for innovators.

Smaller healthcare organizations lacking dedicated health informatics and regulatory affairs expertise face substantial compliance complexity, with regulatory submissions requiring clinical validation studies, substantial quality documentation, and evidence of substantial equivalence to predicate devices, consequently extending development timelines and substantially increasing commercialization costs.

Interoperability Challenges and Integration Complexity with Existing Healthcare Information Systems

Implementation barriers related to system interoperability and electronic health records integration present significant constraints on widespread healthcare AR/VR platform adoption. Most healthcare organizations operate heterogeneous information technology ecosystems with multiple incompatible electronic health record platforms, picture archiving and communication systems, and legacy infrastructure requiring complex interface development and validation.

AR/VR platforms must seamlessly integrate patient-specific medical imaging data, surgical planning information, real-time intraoperative guidance systems, and comprehensive training documentation through standardized healthcare data exchange protocols including DICOM, HL7, and FHIR, requiring substantial software development investment. Healthcare institutions conducting pilots experience technical implementation challenges averaging 6 to 12 months for complete systems integration, substantially delaying return-on-investment realization and creating organizational resistance to adoption despite acknowledged clinical benefits.

Market Opportunities

Rapid Expansion of Therapeutic VR Applications for Chronic Disease Management and Mental Health Treatment

The emergence of therapeutically validated virtual reality interventions targeting chronic pain, mental health disorders, and post-traumatic stress disorders present exceptional market growth opportunities for early-stage VR therapeutic platform developers. Chronic pain conditions, affecting approximately 100 million adults in the United States alone according to NIH data, represent a massive addressable market for non-pharmacological interventions, with VR pain distraction techniques demonstrating efficacy comparable to conventional pharmacological interventions while avoiding opioid-related addiction risks. Clinical evidence demonstrates that immersive VR pain management applications reduce perceived pain intensity by 69% during therapeutic sessions and provide sustained long-term pain reduction benefits through neuroplasticity mechanisms.

Mental health applications including cognitive behavioral therapy modules, exposure therapy platforms for anxiety and phobia disorders, and immersive wellness applications targeting depression and loneliness show exceptional promise in clinical pilot programs. AppliedVR's partnership with Komodo Health to conduct real-world evidence research using de-identified healthcare data represents an emerging trend of validating therapeutic VR value through rigorous health economic analysis and clinical outcomes documentation, positioning therapeutically validated VR platforms for accelerated reimbursement adoption and healthcare system integration.

Integration of Artificial Intelligence, 5G Connectivity, and Remote Surgical Collaboration Capabilities

The convergence of augmented reality, artificial intelligence, ultra-fast 5G connectivity, and advanced sensors is creating unprecedented opportunities for remote surgical procedures, AI-assisted diagnostics, and real-time collaborative clinical decision-making across geographic boundaries. Project Convergence, a partnership between Microsoft, Verizon, and Medivis, has established the nation's first 5G-enabled hospital infrastructure at VA Palo Alto Health Care System, enabling transmission of real-time 3D holographic surgical visualizations and enabling surgeons to perform complex procedures with AI-assisted guidance and real-time remote expert collaboration. Magic Leap 2 MedTech Edition integrated with NVIDIA IGX Orin processors enables medical professionals to visualize complex vasculature with AI-enhanced precision during mechanical thrombectomy procedures for stroke patients, improving intervention speed and clinical outcomes.

The integration of machine learning algorithms with surgical AR visualization systems enables predictive identification of anatomical anomalies, real-time anomaly detection during procedures, and personalized surgical planning based on patient-specific anatomical characteristics. Remote surgical training capabilities enable leading surgeons and specialists to mentor distributed surgical teams in underserved geographic regions, substantially expanding access to specialized surgical expertise and improving clinical outcomes in regions with limited surgical specialist availability.

Category-wise Insights

Technology Type Analysis

Virtual Reality (VR) dominates the healthcare AR VR market with approximately 58% market share, reflecting its established clinical applications in surgical training, pain management, rehabilitation therapy, and immersive patient education. Virtual reality's complete environmental immersion capability enables highly realistic simulation of complex surgical procedures, allowing trainees to practice repetitively without patient safety risks and receive immediate feedback on performance metrics. Clinical research consistently demonstrates VR training superiority over traditional methods, with studies showing trainees using Osso VR achieve proficiency scores 230% to 300% higher than control groups receiving conventional training. The FDA-authorization of AppliedVR's RelieVRx for chronic pain management and the subsequent expansion of therapeutic VR applications across depression, anxiety, and post-traumatic stress disorder treatments have substantially broadened VR's clinical relevance beyond surgical education.

Augmented Reality (AR) represents approximately 42% market share and is experiencing accelerated adoption particularly in surgical guidance, intraoperative navigation, and medical imaging applications. AR technology's capacity to overlay critical diagnostic information, surgical planning data, and anatomical guidance directly onto patient anatomy during procedures offers exceptional value for minimally invasive surgery precision and complex cardiovascular or neurosurgical interventions. The FDA authorization of 92 AR/VR devices demonstrates AR's diverse clinical applicability across radiology, orthopedics, and neurology specialties.

Component Analysis

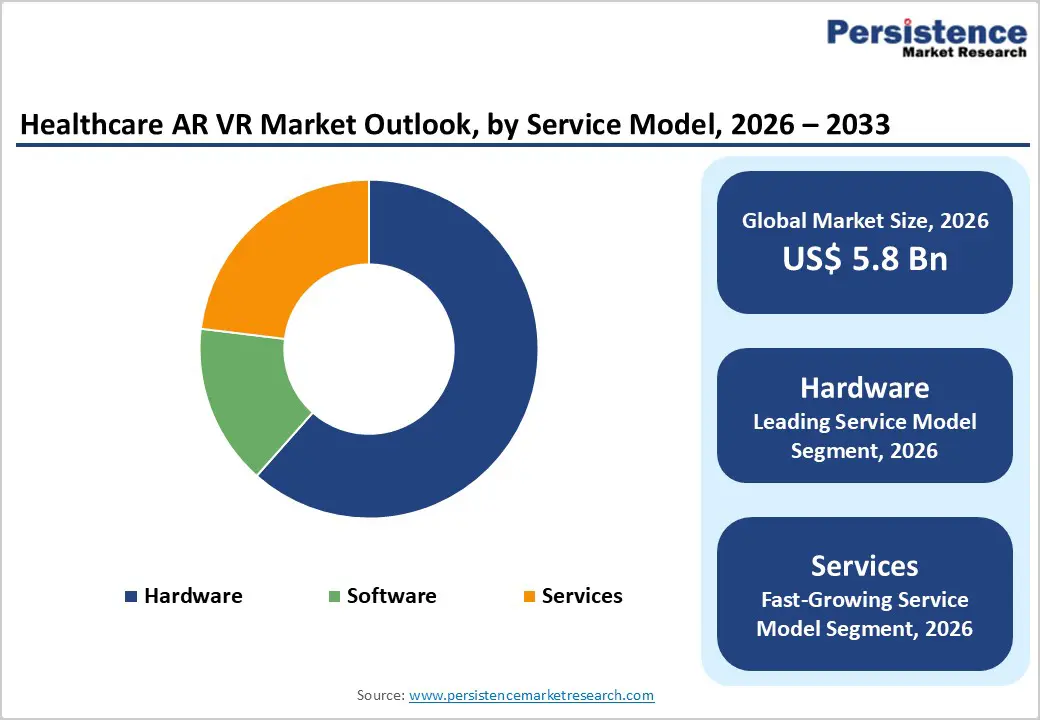

Hardware maintains market dominance with approximately 67% market share, driven by essential infrastructure requirements including head-mounted displays, spatial computing platforms, gesture recognition systems, and specialized medical-grade visualization devices. Advanced head-mounted displays such as Microsoft HoloLens 2, Magic Leap 2 MedTech Edition, and Meta Quest professional models represent critical hardware enabling immersive surgical visualization, telemedicine capabilities, and training simulations. High-resolution optical displays with 1440 x 1400 pixels per eye, advanced hand-tracking sensors enabling gesture-based interface interaction, and integrated processors supporting complex medical imaging visualizations establish technical standards for clinical-grade hardware. The integration of spatial audio systems, infrared eye-tracking technology, and advanced depth sensors supporting sub-millimeter precision tracking creates essential capabilities for surgical navigation and intraoperative guidance applications.

Specialized surgical planning software, AI-powered diagnostic algorithms, telemedicine platforms, and enterprise clinical integration solutions drive software segment expansion as healthcare organizations transition from pilot deployments to large-scale institutional implementation. Subscription-based software licensing models with recurring revenue streams create sustainable monetization mechanisms compared to hardware-dependent business models. Services components, including professional implementation, staff training, technical support, and clinical validation research, represent approximately 5% market share but are expected to expand substantially as healthcare institutions require comprehensive deployment support and change management expertise.

Application Analysis

Surgery Planning represents the leading application segment with approximately 38% market share, reflecting exceptional clinical value in pre-operative planning, intraoperative navigation, and real-time surgical guidance. Surgeons utilizing preoperative AR/VR visualization platforms achieve substantially improved procedural precision, reduced operative time, and enhanced patient safety outcomes through comprehensive anatomical understanding before surgical intervention. Patient Care Management applications command approximately 32% market share, encompassing immersive therapeutic interventions, pain distraction during medical procedures, rehabilitation guidance, and personalized patient education platforms.

Medical Training applications represent approximately 22% of the market share, driven by institutional adoption across medical schools, residency programs, and continuing professional development initiatives. Rehabilitation represents approximately 8% market share but represents the fastest-growing application category, expanding at approximately 29% CAGR through 2031, driven by recognition of VR-enabled rehabilitation's capacity to improve patient motivation, accelerate functional recovery, and enable home-based telerehabilitation programs. Clinical evidence demonstrates VR-guided rehabilitation exercises produce outcomes comparable or superior to traditional physical therapy for stroke recovery, orthopedic rehabilitation, and neurological disorder management.

End User Analysis

Hospitals & Clinics command approximately 55% market share, reflecting their role as primary healthcare delivery institutions implementing AR/VR technologies across surgical departments, training centers, diagnostic imaging services, and patient care units. Major academic medical centers and teaching hospitals are pioneering advanced AR/VR implementations, with institutions including Great Ormond Street Hospital (London), UConn Health, Mount Vernon Hospital, and Mayo Clinic establishing comprehensive immersive training programs and patient care applications. Medical Research Organizations represent approximately 18% market share, leveraging AR/VR platforms for clinical trial simulation, drug development visualization, and innovative therapeutic protocol development.

Diagnostic Centers command approximately 15% market share, with radiology, pathology, and orthopedic imaging centers adopting AR visualization platforms for enhanced diagnostic precision and collaborative case review. Rehabilitation Centers represent approximately 12% market share but demonstrate the fastest growth trajectory at approximately 29% CAGR, driven by recognition of immersive technology's exceptional effectiveness in motivating patient participation and accelerating functional recovery outcomes compared to traditional rehabilitation methodologies.

Regional Insights

North America Healthcare AR VR Trends

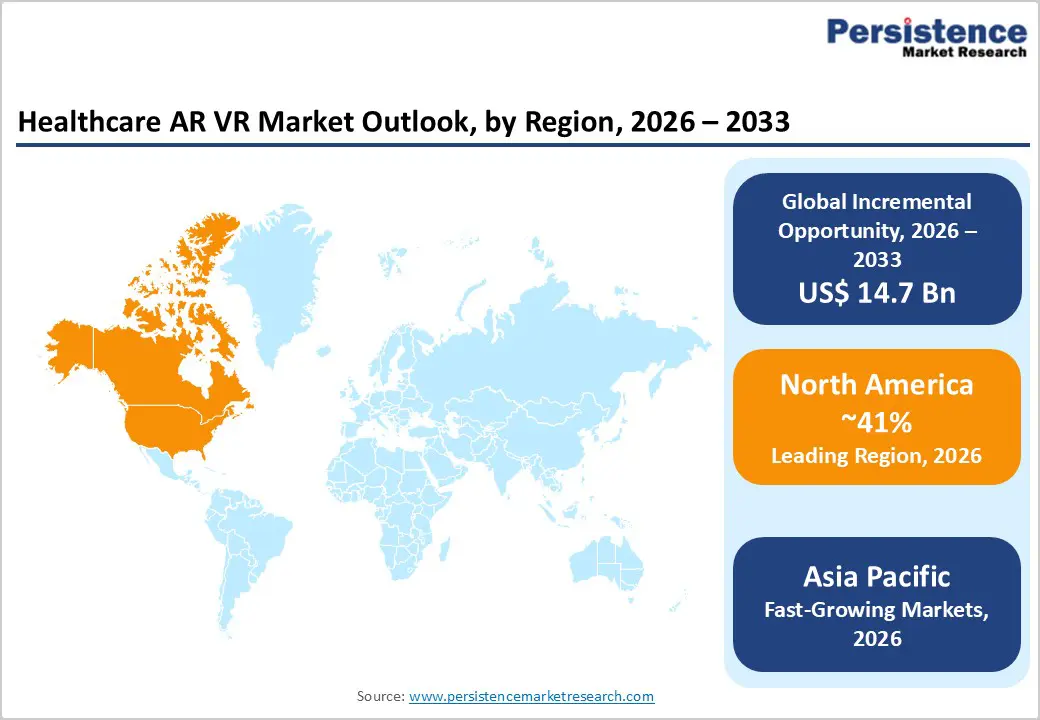

North America dominates the global healthcare AR VR market, commanding approximately 41% market share driven by exceptional healthcare infrastructure, substantial research and development investment, sophisticated regulatory frameworks, and pioneering institutional adoption. The United States represents approximately 65% of regional market value, supported by leading academic medical centers, extensive venture capital funding for healthcare AR/VR startups, and robust FDA approval infrastructure enabling rapid commercialization of innovative technologies. Strategic partnerships between technology giants including Microsoft, Meta, and Google with leading healthcare institutions have established North America as the epicenter of healthcare AR/VR innovation and commercialization.

Canada's healthcare system increasingly adopts AR/VR technologies for surgical training and patient care applications, with Canadian medical institutions establishing collaborative partnerships with leading AR/VR developers. Healthcare provider networks across North America are aggressively implementing VR-based training programs to address documented surgical skills deficiencies and accelerate resident proficiency development. The extensive presence of AR/VR healthcare technology companies including AppliedVR, Osso VR, Surgical Theater, ImmersiveTouch, and Medical Realities reflects the region's concentration of entrepreneurial innovation and clinical validation expertise.

Europe Healthcare AR VR Trends

Europe represents the second-largest regional market with approximately 28% global market share, characterized by leading-edge research infrastructure, strong government support for digital health innovation, and progressive regulatory harmonization initiatives. Germany leads European adoption with approximately 26% regional market share, driven by exceptional research capabilities, strong industrial tradition in medical technology innovation, and government investments exceeding EUR 8 billion in AR/VR technologies as of 2022. Germany's Federal Ministry of Health reports that VR-based therapies have achieved 25% treatment cost reduction while improving recovery rates by 30%, catalyzing rapid institutional adoption across German healthcare systems.

France and Spain demonstrate accelerating AR/VR adoption, with French institutions exploring AR/VR applications for surgical navigation, pain management, and rehabilitation. The European Union's Horizon Europe program has allocated EUR 93.5 billion for research and innovation from 2021-2027, with substantial funding supporting digital health and AI-driven AR/VR healthcare technologies. Europe's emphasis on healthcare digitization, aging population management, and chronic disease burden has created compelling investment rationale for AR/VR healthcare solutions addressing rehabilitation, patient engagement, and remote monitoring.

Asia Pacific Healthcare AR VR Trends

Asia Pacific emerges as the fastest-growing regional market, expanding at approximately 28% CAGR and projected to represent approximately 22% of global market value by 2032, driven by rapid digital transformation, surging investments in advanced medical technologies, and accelerating healthcare infrastructure modernization. China leads Asia Pacific adoption, accounting for approximately 40% regional market share, driven by extraordinary government support for healthcare digitization, massive venture capital investment into immersive technology startups, and rapid institutional adoption across major academic medical centers.

India demonstrates accelerating adoption growth at approximately 31% CAGR, driven by expanding healthcare infrastructure investments, government digitalization initiatives including the National Digital Health Mission, and exceptional opportunities for medical training in regions experiencing surgical specialist shortages. Southeast Asian nations including Thailand, Vietnam, and Malaysia are increasingly adopting AR/VR technologies for medical training and patient care applications, capitalizing on cost advantages and rapidly expanding healthcare infrastructure investments.

Competitive Landscape for the Healthcare AR VR Market

The healthcare AR/VR market exhibits moderate consolidation with dominant technology giants including Microsoft, Google, Meta (Oculus), and Samsung commanding substantial market influence through comprehensive hardware-software ecosystems and deep healthcare partnerships, complemented by specialized healthcare-focused innovators including Osso VR, AppliedVR, Surgical Theater, Magic Leap, and ImmersiveTouch. Market leaders pursue growth through strategic acquisition of specialized healthcare software companies, establishing enterprise partnerships with hospital systems and medical device manufacturers, and investing substantially in clinical validation research demonstrating compelling return-on-investment metrics for healthcare customers.

Key competitive differentiators include superior surgical training platform efficacy validated through rigorous clinical research, seamless integration with existing healthcare information systems and medical imaging infrastructure, FDA regulatory approval status enabling reimbursement eligibility, and comprehensive professional services supporting enterprise implementation and change management. Emerging business model trends include shift toward subscription-based software licensing with recurring revenue streams rather than capital hardware sales, strategic partnerships combining hardware platforms with specialized healthcare software applications, and expansion of remote surgical capabilities leveraging 5G connectivity and cloud computing infrastructure.

Key Market Developments

- In May 2025, Surgical Theater Launches Advanced Precision VR Platform for Neurosurgery, Surgical Theater unveiled an enhanced version of its Precision VR platform specifically engineered for complex neurosurgical procedures, incorporating AI-based three-dimensional visualization and advanced augmented reality navigation tools enabling surgeons to achieve unprecedented precision during complex cerebral vascular and tumor interventions.

- In January 2025, Philips Healthcare Introduces AR-Enhanced Surgical Suite for Hybrid Operating Rooms, Philips Healthcare announced deployment of an augmented reality-enhanced surgical environment designed for hybrid operating rooms, substantially improving surgical workflow integration, enhancing image-guided surgical precision, and enabling seamless real-time data visualization during complex minimally invasive procedures.

- In December 2024, Magic Leap 2 MedTech Edition Enables Advanced Mechanical Thrombectomy Guidance – Magic Leap and Medical iSight demonstrated revolutionary capability enabling physicians to visualize complex cerebral vasculature with exceptional three-dimensional precision using Magic Leap 2 MedTech Edition integrated with NVIDIA IGX Orin processors, enabling AI-assisted guidance during emergency stroke interventions and dramatically improving patient outcomes.

Companies Covered in Healthcare AR VR Market

- Microsoft Corporation

- Samsung Electronics Co. Ltd

- Google Inc.

- DAQRI LLC

- Oculus VR, LLC

- Magic Leap, Inc.

- ImmersiveTouch, Inc.

- FIRSTHAND TECHNOLOGY INC.

- HTC Corporation

- SURGICAL THEATER, LLC.

- Psious

- EchoPixel, Inc.

- Osso VR

- AppliedVR, Inc.

- Medical Realities Ltd

Frequently Asked Questions

The global Healthcare AR VR market was valued at US$ 5.8 billion in 2026 and is projected to reach US$ 20.5 billion by 2033, expanding at 19.8% CAGR. This exceptional growth trajectory reflects accelerating institutional adoption of immersive technologies for surgical training, patient care, therapeutic applications, and medical education across global healthcare systems.

Primary growth drivers include rapid adoption of immersive medical training platforms, FDA regulatory approval of 92 AR/VR medical devices establishing therapeutic legitimacy and reimbursement eligibility, integration of 5G connectivity and artificial intelligence enabling remote surgical capabilities and expanding clinical evidence validating VR therapeutics for chronic pain management achieving 69% pain intensity reduction during treatment sessions.

Surgery Planning dominates with approximately 38% market share, driven by exceptional clinical value enabling surgeons to achieve superior procedural precision and enhanced patient safety outcomes through comprehensive immersive preoperative visualization. Patient Care Management represents 32% market share, while Medical Training commands 22% share, with Rehabilitation representing the fastest-growing segment at approximately 29% CAGR through 2033.

North America maintains market leadership with 41% global market share, driven by exceptional healthcare infrastructure, substantial research investment, and pioneering institutional adoption across leading academic medical centers.

Therapeutic VR applications for chronic disease management, mental health treatment, and pain management represent the most compelling market opportunity, with VR pain management achieving 69% pain intensity reduction and creating substantial addressable markets for non-pharmacological interventions serving 100 million chronic pain patients in the United States alone.

Market leaders include Microsoft Corporation, AppliedVR, Osso VR, Magic Leap, Surgical Theater, Google Inc., Samsung Electronics, HTC Corporation, Philips Healthcare, Siemens Healthineers, and specialized innovators including ImmersiveTouch, EchoPixel, Psious, and Medical Realities.