- Home Care & Utilities

- Gas Masks Market

Gas Masks Market Size, Share, and Growth Forecast, 2026- 2033

Gas Masks Market by Product Type (Air Purifying Respirators (APRS), Powered Air Purifying Respirators (PAPRS), Duct Mask, Self-Contained Breathing Apparatus (SCBAS), and Emergency Escape Hoods), by Application (Oil and Gas, Mining, Healthcare, Military, Fire Service, Industrial Sector, and Others), and Regional Analysis for 2026 – 2033

Gas Masks Market Size and Trends Analysis

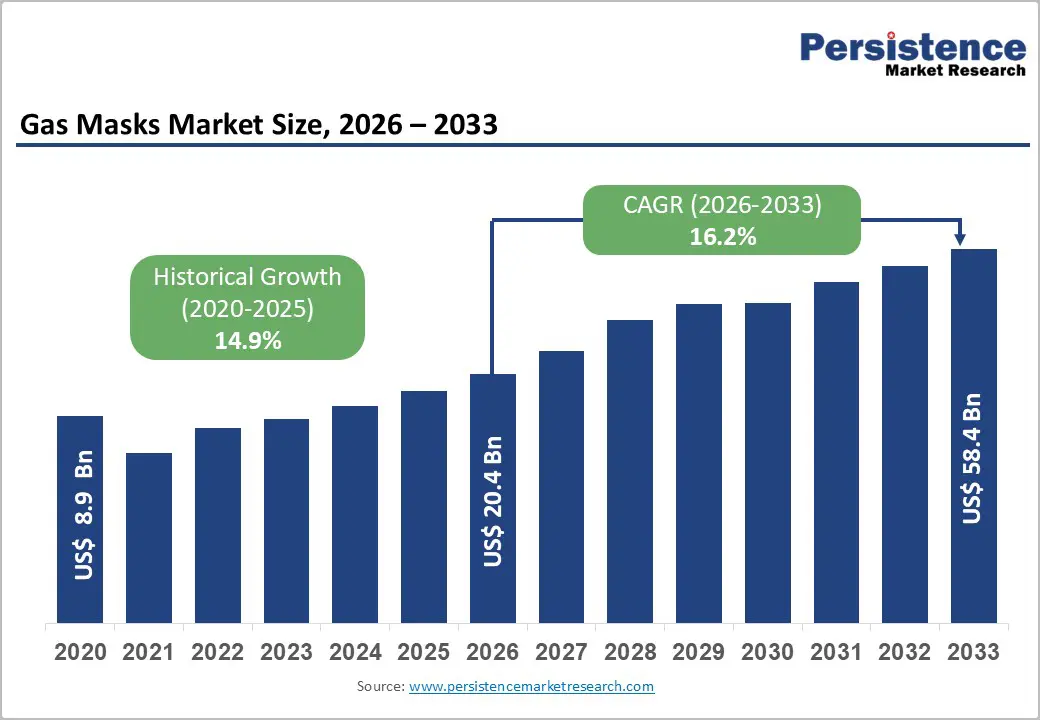

The global gas masks market size was valued at US$ 20.4 billion in 2026 and is projected to reach US$ 58.4 billion by 2033, growing at a CAGR of 16.2% between 2026 and 2033.

This trajectory builds on strong historical growth from US$ 8.9 billion in 2020, reflecting heightened emphasis on occupational safety, stricter regulatory mandates, and recurring public health and industrial risk scenarios. Demand is underpinned by intensive use in oil and gas, mining, fire services, military, and healthcare, where exposure to toxic gases, particulates, and biological agents is structurally high. The market is further shaped by technology migration from conventional air-purifying respirators (APRs) toward more advanced powered air-purifying respirators (PAPRs) and self-contained breathing apparatus (SCBA), as employers and governments align with OSHA, NIOSH, EU-OSHA, ILO and WHO guidance on respiratory protection and emergency preparedness.

Key Industry Highlights:

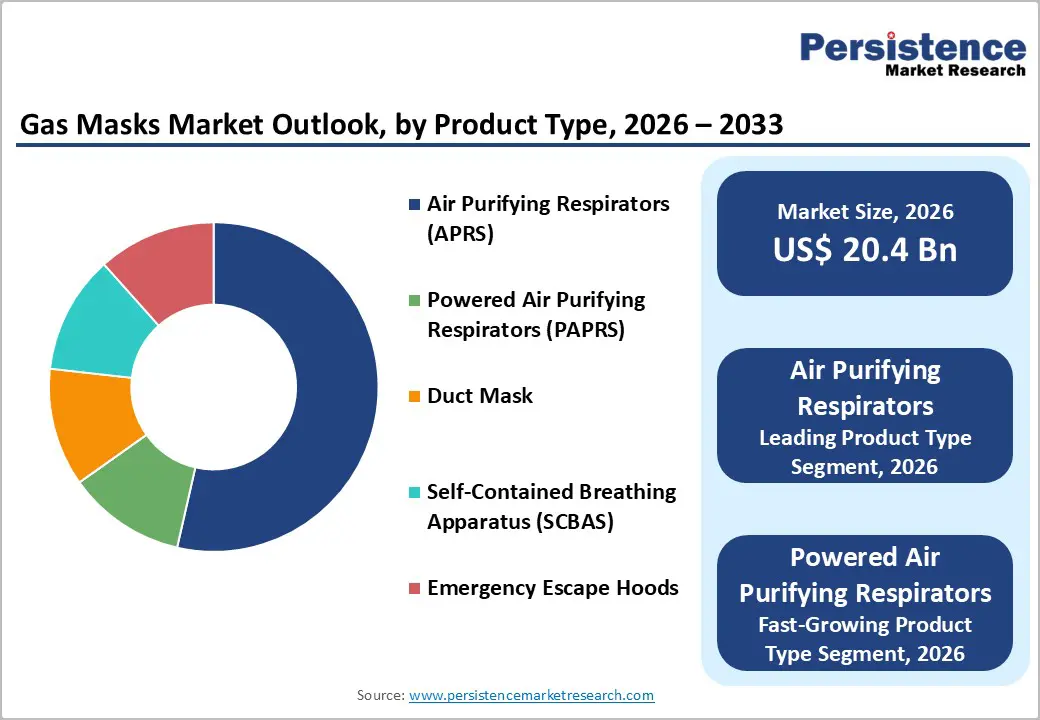

- Product Type Analysis: Air Purifying Respirators (APRs) account for above 60% of total revenues, driven by broad industrial and institutional usage, while Powered Air Purifying Respirators (PAPRs) are the fastest-growing product type with a CAGR of about 7.1%.

- Application Analysis: Oil and gas is the leading application segment with over 33% revenue share, reflecting intensive respiratory protection needs across exploration, refining and petrochemicals; mining is the fastest-growing application, expanding at around 7.3% CAGR.

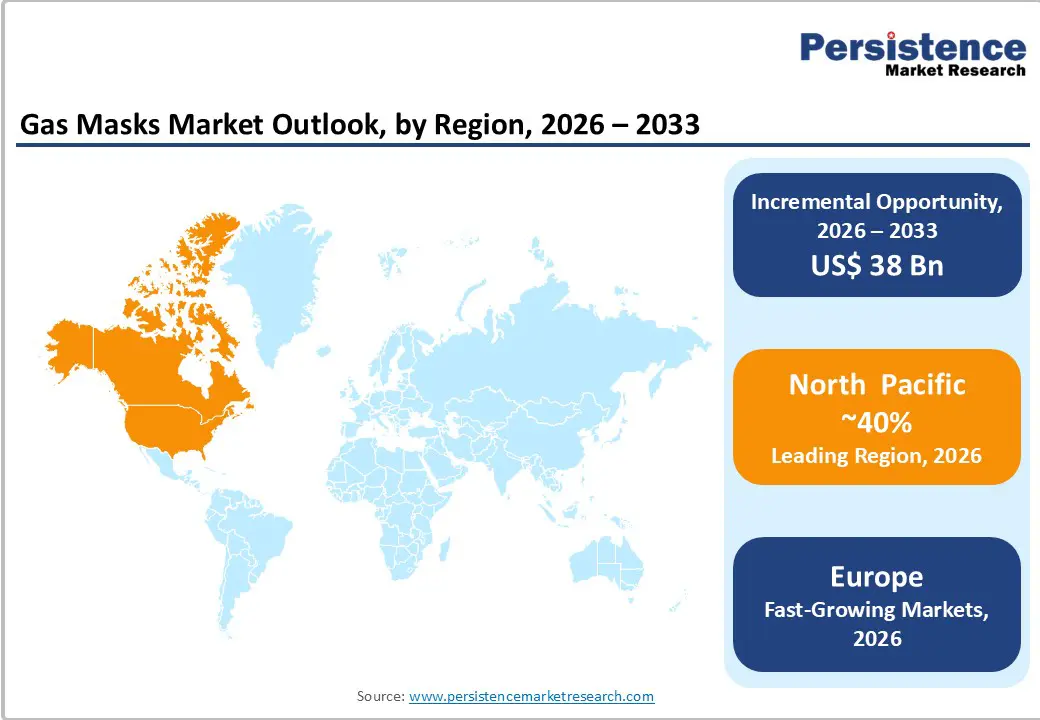

- Regional Analysis: North America captures more than 40% of global gas mask revenues, supported by OSHA/NIOSH-driven compliance and strong public-safety funding; Asia Pacific is the fastest-growing region, with an estimated 7.5% CAGR on the back of rapid industrialization.

- Trend Analysis: Technology upgrades toward smart SCBA and advanced PAPRs, featuring integrated communications and telemetry, are reshaping competitive dynamics and increasing average selling prices in regulated segments.

- Competitive Analysis: The market structure is moderately consolidated at the high end, with 3M, Honeywell, MSA Safety, and Drägerwerk among the leading players, while numerous regional manufacturers compete in commodity APRs and escape devices.

| Report Attribute | Details |

|---|---|

|

Gas Masks Market Size (2026E) |

US$ 20.4 Bn |

|

Market Value Forecast (2033F) |

US$ 58.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

16.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

14.9% |

Market Dynamics

Key Growth Drivers

Strengthening occupational safety regulation and enforcement

Global growth in gas masks is closely linked to stricter enforcement of workplace safety regulations. In the United States, OSHA estimates that around 5 million workers are required to wear respirators as part of their jobs, reflecting regulatory obligations in sectors such as oil and gas, mining, chemicals, and construction. In parallel, EU directives (e.g., Directive 89/656/EEC on personal protective equipment) require employers to provide certified respiratory protective equipment (RPE) for hazardous exposures. Internationally, NIOSH, ILO, and WHO guidelines reinforce the need for respiratory protection in high-risk workplaces. These frameworks translate into recurring procurement cycles, standardisation of performance requirements, and a structural shift from basic filtering masks to certified gas masks and SCBA systems. As regulatory scrutiny intensifies and penalties for non-compliance rise, institutional and industrial buyers increasingly prioritise high-performance gas mask solutions that support sustained double-digit value growth.

Rising incidence of industrial accidents, hazardous releases, and CBRN risks

The frequency and impact of chemical spills, industrial fires and toxic releases have increased, particularly in densely industrialised regions. UNEP data indicate 800+ reported chemical spills globally as of 2023, with about 40% occurring in industrialised regions, underscoring persistent process-safety gaps and the need for robust emergency response equipment. In parallel, global oil and gas production, petrochemical expansion, and urban infrastructure development heighten exposure to flammable gases, hydrogen sulfide, and volatile organic compounds. On the security side, continued investment in CBRN (chemical, biological, radiological, nuclear) defence by military and civil-protection agencies reflects concerns around terrorism, battlefield threats and large-scale industrial incidents. Together, these factors drive institutional demand for full-face gas masks, emergency escape hoods and SCBA to protect first responders, fire services and industrial emergency crews, translating into robust replacement and upgrade cycles.

Market Restraining Factors

Compliance complexity and product certification hurdles

Gas masks must comply with multiple regulatory and performance standards (e.g., NIOSH 42 CFR Part 84, EN 136/EN 137/EN 14387, and various national CBRN specifications). Achieving and maintaining certification requires extensive testing, quality management systems and documentation, raising entry barriers for smaller manufacturers. For end-users, the complexity of selecting appropriate equipment for specific hazards (toxic gases, oxygen-deficient atmospheres, particulates, biological agents) can result in mis-specification, under-utilisation, or non-compliance. These structural frictions slow procurement cycles and can temporarily constrain demand in markets undergoing regulatory transition or standard harmonisation.

Gas Masks Market Trends and Opportunities

Multi-Sector Expansion Driving Advanced Respiratory Protection Demand

Rapid industrialization across the Asia Pacific and Latin America, combined with structurally higher healthcare safety requirements and digital transformation of industrial safety, is creating a single, high-impact growth opportunity for the global gas masks market. Large clusters of oil & gas, petrochemicals, metals, cement, mining, and wastewater treatment facilities in China, India, ASEAN, and Latin America are generating sustained exposure to toxic gases, dust, and fumes, driving mandatory adoption of certified respiratory protection as regulators align with OSHA, EU-OSHA, and ILO standards.

Simultaneously, post-pandemic healthcare, pharmaceutical, and biotechnology sectors have institutionalized high-efficiency respiratory protection for infection control and exposure to active pharmaceutical ingredients, with healthcare-related RPE demand growing at double-digit rates. Gas masks and PAPRs, offering superior filtration and fit, are increasingly favored over conventional masks.

This demand is further amplified by the integration of smart and connected safety technologies. IoT-enabled gas masks with telemetry, environmental sensors, and biometric monitoring support real-time safety management and command-center oversight. Together, these forces position emerging industrial markets, healthcare infrastructure, and smart safety solutions as a multi-billion-dollar, high-margin opportunity within the projected US$ 58.4 billion gas masks market by 2033.

Gas Masks Market Insights and Trends

Product Type Insights

Air Purifying Respirators Dominate While PAPRs Drive Market Growth

The global gas masks market demonstrates clear segmentation by product type, with Air Purifying Respirators (APRs), Powered Air Purifying Respirators (PAPRs), duct masks, Self-Contained Breathing Apparatus (SCBA), and emergency escape hoods addressing varied protection requirements. APRs dominate the market, accounting for over 60% of global revenue, supported by their extensive adoption across industrial maintenance, construction, healthcare, and light manufacturing sectors. Their relatively low cost, ease of use, and suitability for environments with adequate oxygen levels make APRs the preferred solution for routine particulate and gas or vapour exposure. Regulatory norms emphasizing baseline respiratory protection and large-volume procurement by oil & gas companies, industrial operators, and public institutions further reinforce their leadership.

In contrast, PAPRs represent the fastest-growing product segment, expanding at an estimated CAGR of 7.1%. Their powered airflow systems offer higher assigned protection factors and superior wearer comfort, making them ideal for prolonged use in healthcare, pharmaceutical production, chemical processing, and high-dust industrial settings. Recommendations from agencies such as OSHA and NIOSH increasingly support PAPRs where negative-pressure APRs may be insufficient. As employers prioritize both worker safety and productivity, PAPRs are expected to steadily gain market share over the forecast period.

Application Insights

Oil and Gas Dominates While Mining Emerges as Fastest Growth Application

Application-wise, the market spans oil and gas, mining, healthcare, military, fire services, industrial operations, and other high-risk sectors, each shaped by distinct exposure profiles and regulatory frameworks. The oil and gas segment leads the market, accounting for over 33% of total revenue, supported by sustained demand across upstream exploration, refining, gas processing, and petrochemicals. These environments frequently involve hydrogen sulfide, hydrocarbons, corrosive gases, and oxygen-deficient atmospheres, making respiratory protection mandatory for confined space work, plant shutdowns, and emergency response. Strict occupational safety regulations in major producing regions such as North America, the Middle East, and the Asia Pacific further drive high per-worker usage and recurring replacement of filters, cartridges, and emergency escape devices.

The mining sector represents the fastest-growing application, expanding at a CAGR of around 7.3%. Increasing mechanisation, deeper underground operations, and tighter enforcement of mine-safety regulations in countries including China, India, Australia, and South Africa are significantly raising respiratory protection intensity per worker. Gas masks, SCBA, and escape hoods are becoming standard in high-risk zones, reinforcing above-average growth despite a smaller base.

Other applications, including military, fire services, healthcare, and general industry, exhibit specialised demand patterns, driving product differentiation, advanced certifications, and the need for broad, application-specific portfolios among leading manufacturers.

Regional Insights and Trends

North America Leads Global Gas Mask Market Through Regulation

North America represents the largest and most technologically advanced regional market for gas masks, accounting for over 40% of global revenues. This dominance is driven by stringent regulatory frameworks, high safety awareness, and sustained public- and private-sector spending on occupational and emergency protection. The United States serves as the primary demand hub, supported by robust enforcement of OSHA respiratory protection standards, NIOSH certification requirements, and NFPA mandates for SCBA use in firefighting and emergency response. Strong federal and state investments in homeland security and CBRN preparedness further reinforce demand.

Canada contributes incremental growth through occupational safety regulations aligned with CSA standards, particularly across oil sands, mining, chemicals, and heavy industrial operations. Market growth is sustained by continuous replacement cycles of legacy SCBA units in municipal fire departments and rising adoption of smart, telemetric SCBA systems that enhance firefighter safety and operational monitoring.

The region hosts several leading manufacturers, including 3M, Honeywell, MSA Safety, and Avon Protection, resulting in a consolidated yet innovation-driven competitive landscape. Ongoing capital expenditure in oil and gas, petrochemicals, wastewater treatment, and pharmaceuticals continues to support strong demand for APRs, PAPRs, and escape hoods. Regulatory stability and high compliance levels ensure North America’s long-term market leadership.

Europe Gas Mask Market Driven by Regulation and Premium Demand

Europe’s gas mask market is characterised by regulatory-driven demand, high product standards, and stable replacement cycles. Harmonised EU occupational health and safety regulations—particularly Directive 89/656/EEC—along with national fire, civil-protection, and industrial safety norms, form the backbone of sustained adoption across the region. Key markets such as Germany, the United Kingdom, France, and Spain show consistent demand from industrial manufacturing, chemicals, automotive, energy, and public-sector emergency services.

Germany’s strong industrial base, combined with stringent Berufsgenossenschaften (BG) accident insurance requirements, supports steady uptake of certified air-purifying respirators (APRs) and self-contained breathing apparatus (SCBA). Similarly, the U.K.’s Health and Safety Executive (HSE) enforcement and structured procurement by fire brigades and emergency responders reinforce long-term demand visibility. Market growth remains moderate but resilient, supported by ageing SCBA fleet replacement, continuous compliance with CBRN preparedness programs, and investment in advanced industrial safety systems.

Europe also benefits from the presence of innovation-driven manufacturers such as Drägerwerk and Interspiro, fostering competition in premium, ergonomically advanced products. Although CAGR trails Asia Pacific, high unit values, strict certification, and premium positioning ensure Europe remains a critical profit region for global vendors.

Gas Masks Market Competitive Landscape

The gas masks market is moderately consolidated at the high end, with global leaders such as 3M, Honeywell, MSA Safety and Drägerwerk holding significant shares in SCBA, PAPRs and advanced APRs, while numerous regional and niche manufacturers compete in the mid- and low-end segments. Market concentration is relatively higher in regulated categories (e.g., SCBA for fire services, CBRN military masks), where certification and R&D barriers are substantial, and more fragmented in commodity industrial APRs. Competitive positioning increasingly hinges on technology integration, compliance portfolio breadth, and the ability to support large, multi-year procurement programmes across North America, Europe and the Asia Pacific. Leading gas mask suppliers emphasise innovation-led differentiation, regulatory compliance leadership, and geographic expansion into high-growth industrial regions. Common strategic themes include development of smart, connected SCBA and PAPRs; optimisation of cost and supply-chain resilience; and expansion of service, training and lifecycle-management offerings to deepen customer lock-n and support long-term contracts with industrial, military and public-safety agencies.

Key Industry Developments

- In 2025, the United Kingdom Ministry of Defence confirmed a new supply of military-grade gas masks for Ukraine, aimed at strengthening protection against chemical, biological, radiological, and nuclear (CBRN) threats.

- Reported by Defense Blog on June 23, the procurement is valued at £10.2 million and will be manufactured by Avon Technologies.

- In 2024, Smart SCBA was launched by leading vendors: In 2024, major SCBA manufacturers such as MSA Safety and Honeywell expanded their portfolios with smart SCBA systems integrating telemetry, biometric monitoring and cloud-connected diagnostics, aiming to enhance firefighter safety and fleet management.

Companies Covered in Gas Masks Market

- AirBoss of America Corp.

- KCWW

- RPB Safety

- Johnson Controls

- 3M

- Drägerwerk AG & Co. KGaA

- MSA

- Honeywell International Inc.

- Avon Protection

- RSG Safety

- Other Market Players

Frequently Asked Questions

The Gas Masks market is estimated to be valued at US$ 20.4 Bn in 2026.

The primary demand driver for the gas masks market is the tightening of occupational safety, defense, and emergency-response regulations amid rising chemical, biological, radiological, and nuclear (CBRN) risk exposure.

In 2026, the North America Pacific region will dominate the market with an exceeding 40% revenue share in the global Gas Masks market.

Among applications, oil and gas have the highest preference, capturing beyond 33% of the market revenue share in 2026, surpassing other applications.

KCWW, RPB Safety, Johnson Controls, 3M, Drägerwerk AG & Co. KGaA, and MSA There are a few leading players in the Gas Masks market.