- Oil & Gas

- Integrated Gas System Market

Integrated Gas System Market Size, Share, and Growth Forecast, 2026-2033

Integrated Gas System Market by Valve Type (Pneumatic Valves, Manual Valves, Metering Valves, Check Valves), Gas Type (Natural Gas, Hydrogen, Industrial Gases), Application (Semiconductor & Electronics Manufacturing, Chemical Processing, Energy & Power Generation), and Regional Analysis for 2026-2033

Integrated Gas System Market Share and Trends Analysis

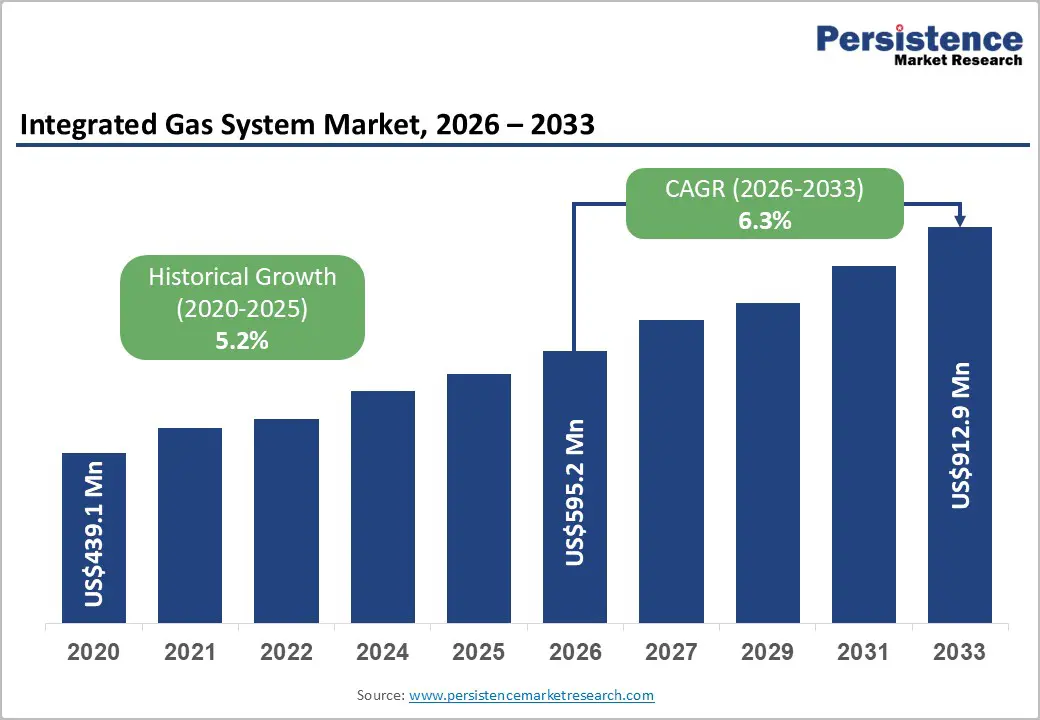

The global integrated gas system market size is likely to be valued at US$595.2 million in 2026, and is projected to reach US$912.9 million by 2033, growing at a CAGR of 6.3% during the forecast period 2026–2033. This robust market growth is driven by the rising demand for advanced gas control and distribution solutions across high-precision industries, including semiconductors, chemical processing, and energy generation.

Manufacturers increasingly implement integrated gas systems to ensure precise flow control, real-time monitoring, and automated safety management, which are essential for maintaining product quality and operational efficiency. The ongoing expansion of semiconductor fabrication facilities, coupled with the global transition toward cleaner energy sources such as hydrogen, and the accelerated adoption of industrial automation technologies, collectively enhance system deployment. These solutions enable safer, more efficient, and highly reliable gas delivery for critical industrial operations.

Key Industry Highlights

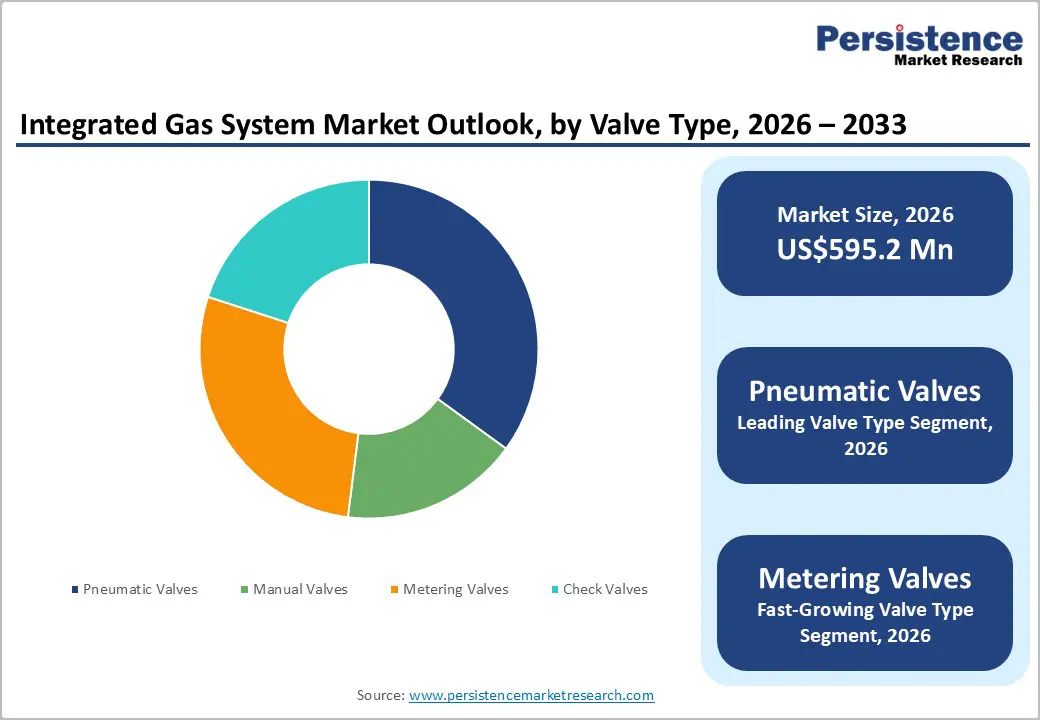

- Dominant Valve Types: Pneumatic valves are poised to dominate with roughly 35% revenue share in 2026, while metering valves are likely to grow the fastest through 2033, driven by rising precision and safety requirements.

- Leading Gas Types: Natural gas is expected to lead with an estimated 48% share in 2026, while hydrogen systems are likely to record the highest 2026-2033 CAGR, fueled by clean energy adoption.

- Dominant Applications: Semiconductor & electronics manufacturing are set to command nearly 42% revenue share in 2026, while energy & power generation applications are slated to grow the fastest at an 8.6% CAGR through 2033, reflecting global energy transition.

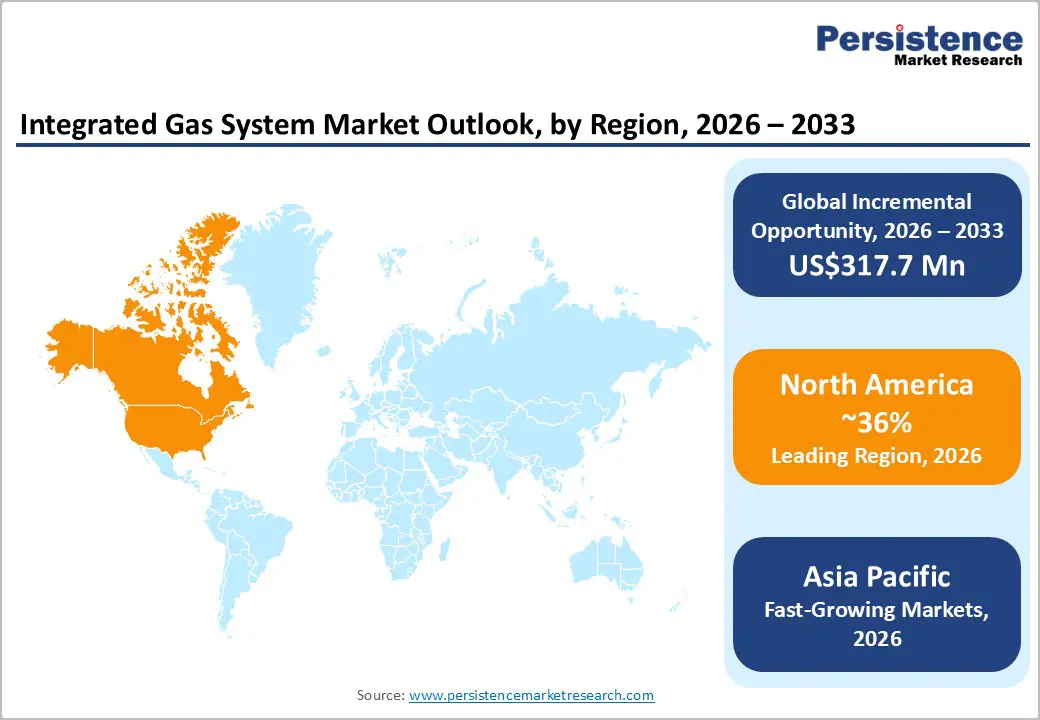

- Regional Leadership: North America is poised to retain the largest market share at 36% in 2026, while Asia Pacific is expected to be the fastest-growing market at 8.9% CAGR through 2033, driven by massive semiconductor investments.

- Competitive Environment: Strategic focus centers on hydrogen-ready system launches, IoT-enabled monitoring integration, and regional mergers & acquisitions (M&A), enabling market players to diversify service offerings and amplify geographic presence.

| Key Insights | Details |

|---|---|

| Integrated Gas System Market Size (2026E) | US$ 595.2 Bn |

| Market Value Forecast (2033F) | US$ 912.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Expansion of Semiconductor, Electronics, and Industrial Applications

The increasing global demand for semiconductors, driven by consumer electronics, 5G infrastructure, advanced AI hardware, and automotive engine control units (ECUs), continues to fuel large-scale fab construction and technology upgrades worldwide. Governments are actively supporting next-generation semiconductor capacity. For instance, Japan’s Ministry of Economy, Trade and Industry (METI) announced incentives in 2025 to attract foreign capital and bolster domestic chip manufacturing, a move aimed at reducing supply chain dependencies and accelerating production of advanced nodes. This expansion further elevates demand for high-purity gas delivery infrastructure, which is essential for lithography, etching, doping, and deposition processes where even minor contamination can disrupt yields.

Integrated gas systems play a critical role in these environments by providing stable, precise, high-purity gas delivery that directly influences manufacturing yields and defect reduction, a top priority for fab operators. As semiconductor supply chains diversify geographically, raw material and gas supply resilience have come into sharper focus; for instance, Reuters reported in March 2026 that helium price volatility increased after production delays in Qatar’s LNG facilities, underscoring the need for robust gas handling and backup systems across fabs and critical industrial sites. These factors combined make integrated gas management systems indispensable infrastructure for high-precision manufacturing.

Energy Transition and Technological Advancements in Gas Management

Global energy transitions, particularly the shift toward natural gas, LNG infrastructure expansion, and low-carbon hydrogen adoption, are driving substantial spending on integrated gas solutions across energy landscapes. National energy plans emphasize cleaner fuel portfolios with natural gas and hydrogen as key transition fuels; for example, the Electricity Generating Authority of Thailand (EGAT) reaffirmed in late 2025 that natural gas and LNG remain central to Thailand’s Net Zero pathway, balancing reliability with emissions reductions. This creates a sustained need for integrated gas systems capable of handling pressure regulation, safety interlocks, and real-time monitoring in large, complex energy infrastructures.

The rapid developments in digital monitoring and automation technologies, including IoT sensors, predictive analytics, and automated flow control platforms, are enhancing system performance, safety, and operational efficiency. These capabilities provide real-time visibility into gas performance parameters, enable early fault detection, and support lifecycle optimization across facilities. In the broader energy sector, global LNG capacity expansions projected for 2026 and beyond are expected to increase downstream demand for advanced gas handling and distribution systems, reinforcing the role of integrated gas solutions in next-generation energy networks. This technology-driven evolution is transforming gas infrastructure into an intelligent, responsive ecosystem.

High Capital Investment Requirements

The acquisition and implementation of advanced Integrated Gas Systems require substantial upfront capital, particularly for facilities that demand high-purity gas handling, automated control systems, and multi-layered safety redundancy. This initial investment can exceed available budgets for smaller manufacturing plants, laboratories, and mid-tier industrial facilities, slowing system deployment. Large-scale projects in gas infrastructure, power generation, and energy sectors hinge on cost-intensive equipment such as specialized compressors, sensors, valves, and digital control modules, elevating financial barriers for many adopters.

Capital intensity becomes even more pressing amid broader energy sector cost fluctuations. In late 2025, major tariffs on imported raw materials and components, including steel, aluminum, and copper, were highlighted by Reuters as factors likely to raise costs and delay oil and gas projects into 2026, effectively compressing margins and deterring investment decisions across energy infrastructure supply chains. This environment compels firms to reallocate budgets toward core operations or resilience planning rather than gas system modernization, further constraining adoption in cost-sensitive markets.

Technical Complexity and Skilled Labor Shortages

Integrated gas systems combine sophisticated control automation, safety interlocks, precision instrumentation, and real-time monitoring technologies, all of which require highly specialized technical expertise to install, calibrate, and maintain. This complexity presents a significant challenge for widespread deployment, particularly in regions with limited access to trained technicians, engineers, and automation specialists. Workforce shortages can undermine system reliability, safety compliance, and operational efficiency, increasing both direct costs and dependency on external support.

This constraint is reinforced by recent findings from the International Energy Agency (IEA), which reported that global energy employment surged to 76 million in 2024, yet more than half of energy firms identify critical skills shortages that threaten infrastructure build-out and project timelines. The report highlights acute demand for applied technical roles, including electricians, engineers, and plant operators, which are foundational to installing and maintaining advanced systems like integrated gas platforms. Without substantial workforce development and training investment, these labor gaps risk slowing adoption in emerging markets and delaying critical infrastructure upgrades.

Hydrogen Economy Integration & Clean Energy Expansion

Policy support for hydrogen production, storage, and refueling infrastructure continues to expand as governments pursue decarbonization targets and cleaner energy security. Integrated Gas Systems engineered for hydrogen service are well positioned to benefit from these infrastructure build-outs, which address hydrogen’s unique properties and require advanced safety, monitoring, and material handling. In 2026, the U.K. government approved construction of the West Wales Hydrogen plant, a renewable powered facility expected to produce around 2,000 tons of low-carbon hydrogen annually, with long-term guarantees and funding support under national hydrogen allocation rounds.

Investments in hydrogen infrastructure are also evident in southern Europe, where a € 1.2 billion green hydrogen project in Spain’s Andalusian Green Hydrogen Valley secured European Union (EU) subsidies and grid connections, underscoring policy-driven expansion of hydrogen ecosystems in industrial and energy value chains. These developments demonstrate active government facilitation of hydrogen hubs, advancing build-out of production, storage, and distribution networks.

As public support and commercial offtake agreements grow, integrated gas system suppliers capable of safe hydrogen delivery will capture new market demand across energy, transportation, and industrial sectors, enhancing revenue potential throughout the forecast period.

Smart Gas Management, Predictive Analytics & Healthcare Integration

The digitalization of gas management presents sizable opportunities for solution providers to extend value through smart monitoring, analytics, and predictive services beyond traditional hardware sales. IoT-enabled platforms and predictive maintenance tools now support industrial operations with real-time visibility into equipment health, enabling early fault detection and reliability improvements across distributed assets. Advanced IoT connectivity technologies, including edge computing and scalable network protocols, are increasingly integral for building robust, secure data streams that support operational automation and optimized asset performance.

Parallel to industrial adoption, healthcare infrastructure modernization further amplifies demand for reliable gas systems integrated with analytics and compliance tracking. While direct healthcare news on gas systems is limited, U.S. hospitals and providers are accelerating digital transformation through cloud and AI-enabled solutions to improve operational efficiency and care delivery, indicating openness to integrated digital systems that enhance reliability and safety.

As hospitals expand technology investments, integrated gas systems with analytics, remote monitoring, and compliance automation will align with broader digital priorities. These trends signal a sustained market opportunity for smart gas management solutions that reduce risk, elevate safety, and provide differentiated service value.

Category-wise Analysis

Valve Type Insights

Pneumatic valves are anticipated dominate with an approximate 35% of the integrated gas system market revenue share in 2026, due to their reliability, fast actuation, and compatibility with automation. They are essential in high-pressure environments and critical industries such as chemical processing, semiconductor gas delivery, and energy infrastructure, where precise control and safety are crucial. Their robustness under continuous operation and ability to integrate with automated control systems makes them the preferred choice for large-scale industrial setups.

In July 2025, Air Liquide invested € 250 million in new gas production units in Dresden, Germany, supplying ultra-pure gases to semiconductor fabs, highlighting the reliance on pneumatic valves for operational stability, contamination prevention, and digital integration. This investment illustrates how major industrial expansions continue to depend on pneumatic technology to manage high-purity gas flow efficiently and safely across critical processes.

Metering valves are expected to grow at roughly 7.8% CAGR through 2033, driven by rising demand for precision control and enhanced safety in high-purity processes. Metering valves allow exact dosing of gases critical in semiconductor and chemical processing, while check valves prevent backflow and contamination, safeguarding system integrity and uptime. As manufacturing processes become more exacting and purity standards tighten, these valves are increasingly incorporated into next-generation gas architectures.

In October 2025, GlobalFoundries announced a €1.1 billion expansion of its Dresden fab, emphasizing the need for advanced gas delivery systems and specialized valves capable of supporting complex, contamination-sensitive operations. Adoption of metering and check valves in high-tech environments is accelerating, highlighting their strategic role in both new installations and retrofitted facilities.

Application Insights

The semiconductor and electronics manufacturing segment is poised to lead applications, commanding an estimated 42% of the integrated gas system market share in 2026, powered by ultra-high-purity gas delivery and strict contamination control requirements. Gas systems support critical stages including photolithography, etching, and deposition, directly impacting yields, device performance, and production quality. The high cost and technical complexity of semiconductor fabs drive significant investments in integrated gas systems as part of core manufacturing infrastructure.

Integrated gas solutions in this domain provide reliable control, monitoring, and safety features, enabling fabs to achieve regulatory compliance and maintain uninterrupted high-volume production under exacting quality standards.

Energy & power generation applications are slated to be the fastest-growing, projected to achieve a CAGR of about 8.6% through 2033, fueled by modernizing natural gas pipelines, LNG terminals, and hydrogen-ready power plants. Integrated gas systems improve safety, distribution efficiency, and regulatory compliance in power generation and industrial energy operations.

In October 2025, India designated three ports, Deendayal, Paradip, and V.O. Chidambaranar, as Green Hydrogen Hubs under the National Green Hydrogen Mission, accelerating infrastructure development and hydrogen adoption. These initiatives underscore the growing importance of advanced gas delivery and monitoring systems to handle high-pressure, high-purity, and multi-gas applications safely. Utilities and industrial operators increasingly rely on integrated solutions to meet sustainability targets, optimize energy output, and ensure long-term operational reliability across evolving energy networks.

Regional Insights

North America Integrated Gas System Market Trends

North America is expected to account for an estimated 38% of the integrated gas system market value in 2026, supported by advanced industrial infrastructure, widespread semiconductor manufacturing, and stringent regulatory oversight. The United States leads due to strong energy networks, investments in automation, and increasing deployment of high-purity gas systems across chemical, energy, and high-tech sectors. Regulatory frameworks established by the Occupational Safety and Health Administration (OSHA) and the Environmental Protection Agency (EPA) ensure that modern gas delivery and control systems meet rigorous safety and environmental standards, driving system upgrades and adoption across facilities. The combination of mature industrial infrastructure and growing clean energy initiatives reinforces North America’s sustained market dominance.

Real-world developments reinforce this leadership. In September 2025, for example, the U.S. Department of Energy (DOE) launched the “Speed to Power Initiative” to accelerate grid modernization and multi-gigawatt energy projects, expanding infrastructure that relies on integrated gas systems for safe, reliable fuel delivery. This initiative, aimed at speeding deployment of power and gas infrastructure, signals continued government support for energy infrastructure projects where gas system reliability is essential.

Strategic partnerships, innovation clusters in California, Texas, and New York, and ongoing upgrades to automation and monitoring technologies further anchor North America’s leading position in both technology adoption and operational excellence.

Europe Integrated Gas System Market Trends

Europe is a mature and highly regulated market, driven by harmonized industrial standards, safety protocols, and proactive energy transition policies. Integrated gas systems are widely adopted across Germany, the U.K., France, and Spain, particularly in chemical processing, energy distribution, and advanced manufacturing, where compliance with EU safety and emissions directives is essential. Industrial automation and the drive for carbon-neutral energy generation further accelerate the deployment of advanced gas handling and monitoring systems across industrial facilities.

Strong engineering expertise and established infrastructure support the ongoing modernization of gas networks and energy plants.

In 2025, the European Parliament adopted the EU Gas Network Modernization Directive, mandating upgrades to gas infrastructure to enhance efficiency, safety, and reduce emissions. This regulation drives investments in advanced integrated gas systems, including digital monitoring and automated control solutions, to ensure compliance with stringent EU standards. Complementing this, France commissioned the Normandy LNG Terminal expansion in September 2025, increasing capacity for clean fuel distribution and industrial gas supply. These initiatives highlight Europe’s commitment to modern, reliable, and environmentally responsible gas infrastructure while fostering a competitive and innovation-driven market environment.

Asia Pacific Integrated Gas System Market Trends

Asia Pacific is likely to be the fastest-growing regional market for integrated gas systems, expanding at an 8.9% CAGR through 2033, driven by rapid industrialization, rising energy demand, and expanding semiconductor ecosystems. China, Japan, and ASEAN nations are investing heavily in gas infrastructure as part of broader industrial modernization and energy transition initiatives. In China, accelerated development of pipeline connectivity, storage facilities, and LNG terminals supports industrial growth and energy security, driving demand for integrated gas systems across manufacturing and power generation sectors.

ASEAN countries are progressing with national LNG and gas strategies, focusing on domestic supply reliability and industrial demand. For example, in July 2025, Singapore officially commissioned its Jurong Island LNG Terminal expansion, increasing storage and regasification capacity to support chemical, energy, and industrial hubs. Complementing this, Japan continues investing in precision gas delivery and monitoring systems for its electronics and chemical industries, improving operational efficiency and safety. Government incentives, low-cost manufacturing, and skilled labor further accelerate adoption, positioning Asia Pacific as a pivotal growth engine for integrated gas systems.

Competitive Landscape

The global integrated gas system market structure is moderately consolidated, with leading players such as Air Liquide, Linde, Honeywell, Emerson, and Yokogawa collectively controlling a significant portion of market revenue. These established vendors leverage extensive industrial relationships, compliance expertise, and integrated hardware-software platforms to deliver high-purity gas control, automation, and safety solutions. They continue to invest heavily in R&D, IoT-enabled monitoring, predictive maintenance, and digital control technologies to maintain technological leadership and address evolving energy, semiconductor, and chemical processing needs.

Regional and niche competitors, including Messer Group, Hitachi Energy, and Mitsubishi Electric, focus on specialized applications, geographic strongholds, and industry-specific solutions. High entry barriers such as complex system integration, stringent safety regulations, and capital intensity limit new players, though software-focused companies are increasingly entering through cloud-based gas management platforms and remote analytics services.

Market consolidation is expected to increase gradually as global leaders pursue acquisitions to expand geographically and technologically, while technology partnerships continue enabling innovation in smart, automated, and hydrogen-ready integrated gas systems.

Key Industry Developments

- In February 2026, ABB launched its first fully integrated gas analyzer for carbon capture, utilization, and storage (CCUS) that enables real-time monitoring and optimization of CO2 capture processes, helping industries improve accuracy, efficiency, and compliance with decarbonization targets.

- In November 2025, INOX Air Products signed a long-term onsite gas supply agreement with Grew Energy to support its solar cell manufacturing facility in Madhya Pradesh, ensuring a reliable supply of industrial gases for production.

- In April 2025, Linde announced it will build its eighth on-site Air Separation Unit at Samsung’s Pyeongtaek fab, supplying ultra-high purity gases and hydrogen for DRAM, NAND, and logic chip production.

Companies Covered in Integrated Gas System Market

- Linde plc

- Air Products & Chemicals, Inc.

- Praxair Technology, Inc.

- Honeywell International Inc.

- Matheson Tri-Gas

- Messer Group GmbH

- Taiyo Nippon Sanso Corporation

- Air Liquide S.A.

- Showa Denko K.K.

- Parker Hannifin Corporation

- Swagelok Company

- WIKA Alexander Wiegand SE & Co. KG

- INOXCVA

- Hitachi Metals

- BOC Ltd.

Frequently Asked Questions

The global integrated gas system market is projected to reach US$ 595.2 million in 2026.

The surging demand for high-precision gas control in semiconductor, chemical, and energy sectors is driving market growth.

The market is poised to witness a CAGR of 6.3% from 2026 to 2033.

Expanding hydrogen infrastructure and smart gas management systems are creating significant growth opportunities.

Air Liquide, Linde, Honeywell, Emerson, and Yokogawa are some of the leading market players.