- Automation & Robotics

- Gas Delivery Systems Market

Gas Delivery Systems Market Size, Share, and Growth Forecast, 2026 - 2033

Gas Delivery Systems Market by Product Type (Signal Station Systems, Others), Application (Industrial, Chemical, Others), End-use Industry (Semiconductor Manufacturing, Healthcare, Chemicals, Electronics), and Regional Analysis for 2026 – 2033

Gas Delivery Systems Market Size and Trends Analysis

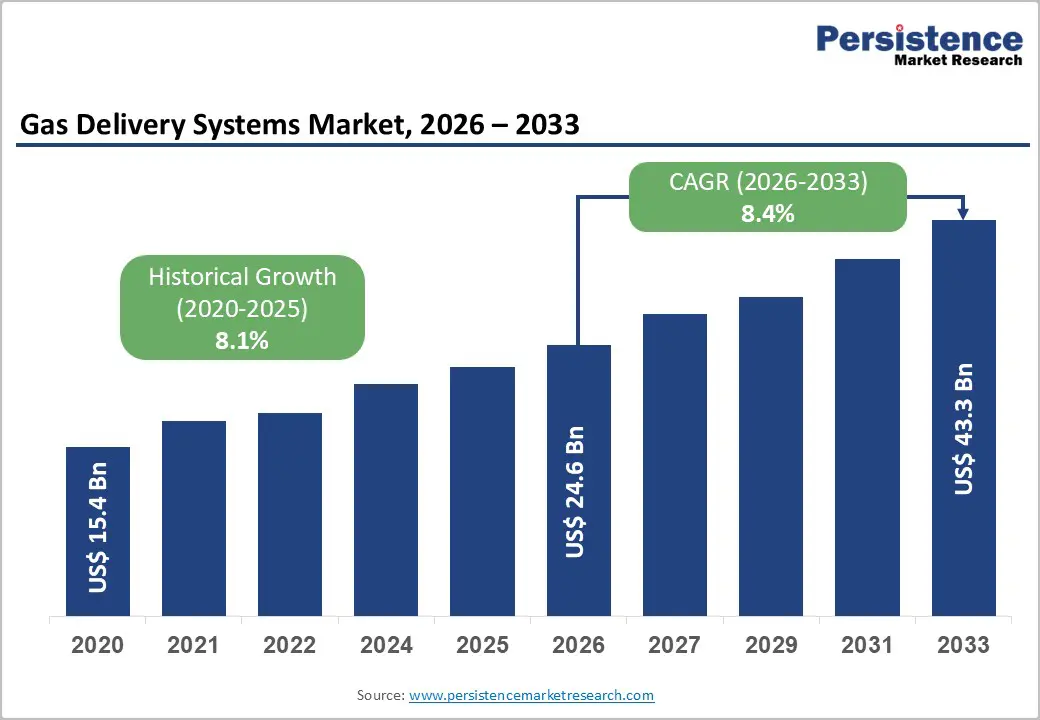

The global gas delivery systems market size is likely to be valued at US$24.6 billion in 2026, and is expected to reach US$43.3 billion by 2033, growing at a CAGR of 8.4% during the forecast period from 2026 to 2033, driven by the increasing prevalence of ultra-high-purity gas requirements in semiconductor fabs, rising demand for uninterrupted specialty gas supply in healthcare facilities, and advancements in fully automatic programmable switchover systems with IoT integration.

Growing demand for reliable, zero-downtime gas delivery systems, especially fully automatic programmable switchover systems for semiconductor manufacturing, is accelerating adoption across end-use industries. Advances in semi-automatic and signal station designs are further boosting uptake by offering cost-effective redundancy for mid-scale operations. Increasing recognition of gas delivery systems as critical for production continuity, yield protection, and safety compliance in emerging high-tech and medical markets remains a major driver of market growth.

Key Industry Highlights:

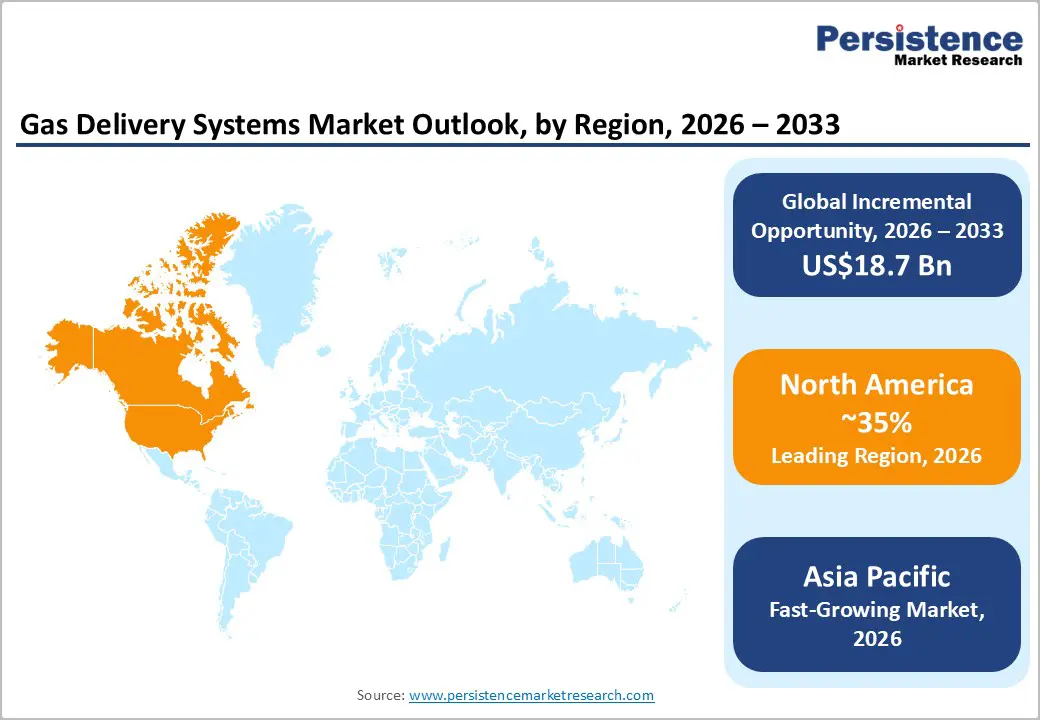

- Leading Region: North America is projected to dominate, account for nearly 35% of the market in 2026, driven by the region’s advanced semiconductor ecosystem, strong research and development capabilities, and high public awareness of uptime benefits.

- Fastest-growing Region: Asia Pacific, fueled by rapid 3nm/2nm fab ramp-up, expanding healthcare infrastructure, and growing specialty gas consumption in chemicals.

- Dominant Product Type: Fully automatic programmable switchover systems, to hold approximately 45% of the market share, as they deliver the highest uptime and automation level.

- Leading Application: The industrial segment is expected to account for over 55% of the market revenue, due to broad manufacturing and process gas usage.

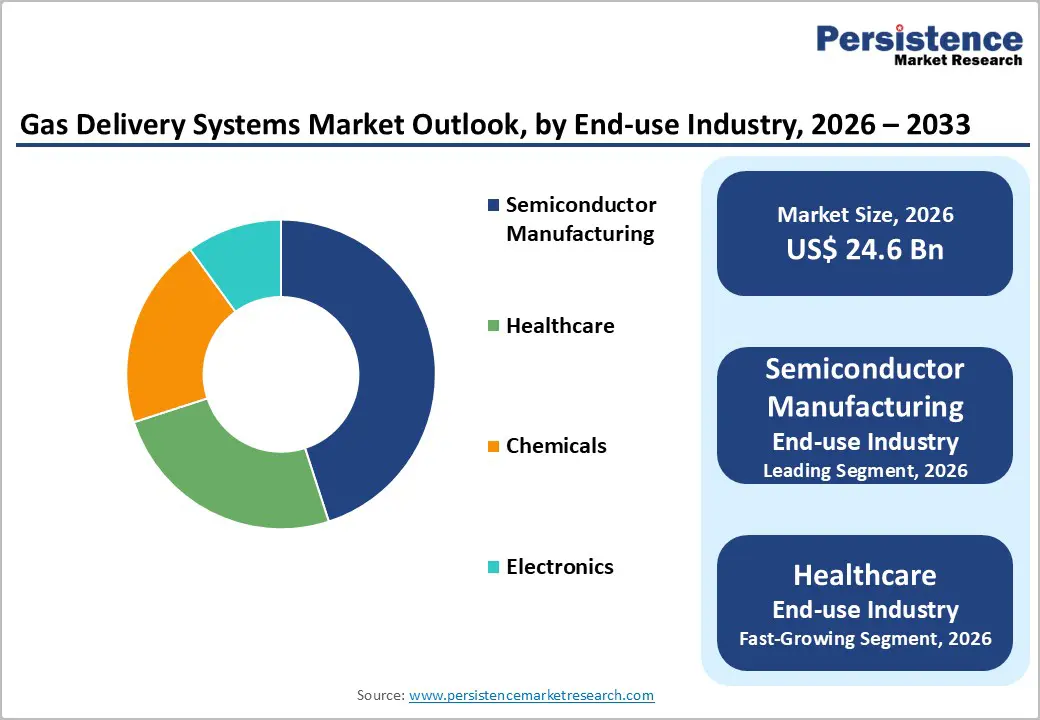

- Leading End-use Industry: Semiconductor manufacturing, to contribute nearly 40% of the market revenue, due to stringent purity and continuity requirements.

| Global Market Attributes | Key Insights |

|---|---|

| Gas Delivery Systems Market Size (2026E) | US$24.6 Bn |

| Market Value Forecast (2033F) | US$43.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 8.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Increasing Demand for Ultra-High-Purity Gas Requirements and Uninterrupted Delivery

The increasing demand for ultra-high-purity (UHP) gas requirements and uninterrupted delivery is being driven by the rapid expansion of precision-driven industries where even trace-level contamination can compromise performance, safety, and yield. Sectors such as semiconductor manufacturing, pharmaceuticals, biotechnology, and advanced materials rely heavily on gases with extremely low impurity levels for processes such as wafer fabrication, drug formulation, and laboratory analysis. As manufacturing nodes become smaller and processes more complex, tolerance for impurities continues to shrink, pushing suppliers to deliver gases that meet increasingly stringent purity specifications.

Uninterrupted gas delivery has become mission-critical for continuous and high-value production environments. Any disruption in gas supply can lead to equipment shutdowns, batch losses, and significant financial impact. This has led end users to prioritize suppliers capable of providing robust storage systems, redundant distribution networks, and real-time monitoring solutions that ensure consistent flow and pressure. The growing adoption of automated and 24/7 production lines further amplifies the need for reliability, as manual intervention is minimized and process stability becomes essential.

Supply Chain Disruptions and Fluctuating Raw Material Costs

Supply chain disruptions and fluctuating raw material costs represent a significant restraint for the gas delivery systems market, as these systems depend on highly specialized components and precision-engineered materials. Key inputs such as stainless-steel tubing, specialty alloys, valves, seals, sensors, and electronic control units must meet strict quality and safety standards. Any interruption in the availability of these materials caused by logistics delays, trade restrictions, geopolitical uncertainty, or transportation bottlenecks can slow manufacturing timelines and delay system installations for end-users.

Volatility in raw material prices further complicates cost planning for manufacturers and system integrators. Sudden increases in the prices of metals, polymers, or electronic components directly impact production costs, often forcing suppliers to revise pricing or absorb margin pressure. This uncertainty makes long-term contracts and project budgeting more challenging, particularly for large-scale or customized gas delivery installations. In industries where pricing stability is critical, frequent cost fluctuations can lead customers to postpone investments or seek lower-cost alternatives.

Expansion of Customization and Modular Systems

Customization and modularity in gas delivery systems are emerging as significant opportunities for market growth, driven by the diverse and evolving requirements of end users. Industries ranging from semiconductors and pharmaceuticals to chemical processing and healthcare require gas delivery solutions customized to meet their unique operational, safety, and purity standards. Standardized systems often fall short in meeting these unique needs, creating a market for suppliers who can design flexible, application-specific solutions.

Modular systems offer scalability and adaptability, allowing users to expand or reconfigure their gas networks as production volumes or processes change. For instance, a manufacturing facility can start with a compact module and gradually integrate additional units to support higher throughput without major infrastructure overhauls. This approach reduces capital expenditure and installation time while enhancing operational efficiency. Modular and customizable systems improve maintenance and uptime. Individual modules can be serviced or replaced without shutting down the entire network, minimizing production disruptions.

Category-wise Analysis

Product Type Insights

Fully automatic programmable switchover systems are expected to lead the market, capturing around 45% of the market share in 2026. Their widespread adoption is driven by their ability to maintain a continuous gas supply by automatically switching between primary and backup cylinders or tanks without the need for manual intervention. These systems improve operational efficiency, minimize downtime, and enhance safety, making them well-suited for industries that require uninterrupted gas flow, including healthcare, electronics, and chemical processing. A stainless steel fully automatic gas switchover manifold system ensures seamless gas delivery by automatically transferring supply between two-cylinder banks once one is depleted. Designed for high-purity and industrial gases such as oxygen, nitrogen, helium, and acetylene, these systems are ideal for applications demanding zero downtime, including laboratories, clean rooms, and industrial processes.

Semi-automatic switchover systems are the fastest-growing segment, offering an effective balance of cost, reliability, and operational control. In these systems, switching from an empty to a full gas source requires minimal human intervention, while pressure indicators and alarms alert operators to act at the appropriate time, reducing downtime and guesswork. This makes them particularly suitable for small to medium-sized laboratories, regional medical facilities, and industrial workshops that require a dependable gas supply without the higher cost of fully automatic systems. For example, the GCE Group BMD 202-39 Semi-Automatic Switch-Over Panel is designed to ensure uninterrupted acetylene supply by transferring flow from an empty cylinder bank to a reserve source when primary pressure drops. The system supports multiple cylinders and incorporates safety features such as a flashback arrestor and an optional low-pressure alarm, exemplifying the functionality and safety of semi-automatic gas switchover technology in industrial applications.

Application Insights

The industrial segment is projected to lead the market, accounting for approximately 55% of the share in 2026, driven by its dependence on consistent, high-volume gas usage. Sectors such as chemicals, metals, electronics, energy, and manufacturing rely on gases for core operations, including processing, heating, cutting, and quality control. The demands of continuous production cycles and stringent safety requirements encourage industrial users to invest in reliable gas delivery and control systems. For instance, Gulf Cryo supplies industrial gases like oxygen, nitrogen, and argon to steel and metal industries across the Middle East, offering solutions such as on-site pipeline systems and bulk deliveries for welding, cutting, and refining operations, demonstrating how gas delivery underpins large-scale manufacturing processes.

The chemical segment is expected to be the fastest-growing, driven by the increasing use of specialized gases in chemical manufacturing for reactions, synthesis, heat treatment, and safety applications. As producers move toward more complex, high-value chemicals, precision in gas purity and delivery becomes critical for maintaining product quality and process efficiency. The expansion of petrochemical plants and the growth of advanced materials manufacturing are fueling demand for industrial gases. Additionally, regulatory requirements to reduce emissions and enhance operational safety encourage investment in advanced gas delivery systems. For example, Linde plc provides pipeline-based delivery of gases such as nitrogen and carbon monoxide directly to chemical plants, enabling large-volume feedstock supply and supporting complex chemical processes and safety inerting.

End-use Industry Insights

The semiconductor manufacturing segment is projected to dominate the market, accounting for nearly 40% of revenue in 2026, due to its heavy reliance on ultra-high-purity gases and precisely controlled delivery systems. Chip fabrication processes, including deposition, etching, doping, and cleaning, require a continuous supply of specialty gases with extremely low contamination levels. As device geometries shrink and production nodes advance, tolerance for impurities becomes increasingly stringent, driving demand for sophisticated gas delivery solutions. Matheson Tri-Gas, Inc. provides industrial and specialty gases, along with precision gas handling and delivery equipment tailored for semiconductor fabrication facilities. Their ultra-high-purity gases, such as nitrogen, hydrogen, and rare gases, are delivered through engineered systems designed to support critical wafer fabrication processes, including deposition, etching, and purge operations.

The healthcare segment is expected to be the fastest-growing, fueled by medical facilities’ increasing reliance on specialized gases for patient care and clinical procedures. Gases such as oxygen, nitrous oxide, and medical-grade air are vital for surgeries, respiratory therapy, emergency care, and intensive care units. Rising demand is driven by aging populations and expanded access to healthcare services worldwide, creating a need for reliable systems that ensure safety, purity, and uninterrupted flow. Additionally, the growth of home healthcare and outpatient clinics requires flexible and easily installed solutions. Linde’s healthcare division designs and implements Medical Gas Pipeline Systems (MGPS) to supply critical gases, including oxygen, nitrous oxide, medical air, and nitrogen, directly to hospitals and healthcare facilities. These systems ensure continuous, safe, and regulated delivery from central sources to bedside outlets, supporting surgical procedures, ICU care, and respiratory therapy.

Regional Insights

North America Gas Delivery Systems Market Trends

North America is projected to dominate, account for nearly 35% of the market share in 2026, driven by the region’s advanced semiconductor ecosystem, strong research and development capabilities, and high public awareness of uptime benefits. Deployment systems in the U.S. and Canada provide extensive support for gas programs, ensuring wide accessibility of gas switchover stations across semiconductor manufacturing, healthcare, and chemicals populations. Increasing demand for fully automatic programmable, convenient, and easy-to-integrate forms is further accelerating adoption, as these formats improve reliability and reduce barriers associated with manual changeover.

Innovation in gas delivery systems technology, including stable IoT integration, improved high-purity delivery, and targeted predictive maintenance enhancement, is attracting significant investment from both public and private sectors. Government initiatives and CHIPS Act campaigns continue to promote use against yield risks, contamination concerns, and emerging fab threats, creating sustained market demand. The growing focus on healthcare grades and specialty uses, particularly for electronics and others, is expanding the target applications for gas switchover stations.

Europe Gas Delivery Systems Market Trends

Europe shows significant growth fueled by increasing awareness of reliability benefits, strong healthcare systems, and government-led advanced manufacturing programs. Countries such as Germany, France, and the Netherlands have well-established fab and medical frameworks that support routine switchover use and encourage adoption of innovative station delivery methods, including gas switchover stations. These high-purity formulations are particularly appealing for semiconductor populations, regulation-conscious operators, and chemical users, improving continuity and coverage rates.

Technological advancements in gas delivery systems development, such as enhanced automation, application-targeted delivery, and improved semi-automatic grades, are further boosting market potential. European authorities are increasingly supporting research and trials for stations against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, low-contamination options is aligned with the region’s focus on preventive quality and reducing downtime. Public awareness campaigns and promotion drives are expanding reach in both urban and rural areas, while suppliers are investing in sensors and novel variants to increase efficacy.

Asia Pacific Gas Delivery Systems Market Trends

Asia Pacific is likely to be the fastest-growing market, driven by rising semiconductor awareness, increasing government initiatives, and expanding application programs across the region. Countries such as China, Taiwan, South Korea, and India are actively promoting station campaigns to address fab growth and emerging healthcare needs. Gas switchover stations are particularly attractive in these regions due to their scalable administration, ease of integration, and suitability for large-scale cleanroom drives in both urban and rural populations.

Technological advancements are supporting the development of stable, effective, and easy-to-deploy gas switchover stations, which can withstand challenging cleanroom conditions and minimize purity dependence. These innovations are critical for reaching remote facilities and improving overall gas coverage. Growing demand for semiconductor manufacturing, healthcare, and chemicals applications is contributing to market expansion. Public-private partnerships, increased electronics expenditure, and rising investment in station research and manufacturing capacity are further accelerating growth. The convenience of station delivery, combined with improved uptime and reduced risk of contamination, positions gas switchover stations as a preferred choice.

Competitive Landscape

The global gas delivery systems market features competition between established gas equipment leaders and emerging automation suppliers. In North America and Europe, Ichor Systems and Air Liquide lead through strong R&D, distribution networks, and fab ties, bolstered by innovative, fully automatic, and high-purity programs. In Asia Pacific, Matheson (Taiyo Nippon Sanso) advances with localized solutions, enhancing accessibility. IoT-integrated delivery boosts uptime, cuts manual risks, and enables mass integrations across regions. Strategic partnerships, collaborations, and acquisitions merge expertise, expand portfolios, and speed commercialization. High-purity formulations solve contamination issues, aiding penetration in advanced node areas.

Key Industry Developments

- In December 2025, Alfa Laval announced the launch of a new fuel-conditioning module (FCM) designed to prepare liquefied natural gas (LNG) for seamless use in marine engines. This new module expands Alfa Laval’s portfolio of alternative fuel solutions, integrating cryogenic technology to provide a comprehensive and highly reliable fuel supply system for shipowners transitioning to LNG.

- In September 2025, ABB India and THINK Gas announced a strategic partnership to advance digital innovation in city gas. The collaboration focused on deploying cutting-edge digital and automation solutions to enhance the operational efficiency, monitoring, and control of THINK Gas’s distribution network. The partnership aimed to achieve end-to-end digitalization, improve asset visibility, ensure safer gas distribution, and support scalable network expansion across multiple regions.

Companies Covered in Gas Delivery Systems Market

- Ichor Systems

- HARRIS

- Praxair (Linde)

- Matheson (Taiyo Nippon Sanso)

- Air Liquide

- The Fuel Cell Store

Frequently Asked Questions

The global gas delivery systems market is projected to reach US$24.6 billion in 2026.

The rising prevalence of ultra-high-purity gas requirements in semiconductor fabs and demand for uninterrupted delivery are key drivers.

The gas delivery systems market is poised to witness a CAGR of 8.4% from 2026 to 2033.

Advancements in IoT-integrated and high-purity delivery platforms are key opportunities.

Ichor Systems, Air Liquide, Matheson (Taiyo Nippon Sanso), Praxair (Linde), and HARRIS are the key players.