- Electrical Equipment & Services

- Gas Leak Detector Market

Gas Leak Detector Market Size, Share, and Growth Forecast, 2025 - 2032

Gas Leak Detector Market By Product Type (Electrochemical, Catalytic Bead Sensors, Photo-ionization), Installation (Fixed, Portable), Application (Residential, Commercial/Industrial), and Regional Analysis for 2025 - 2032

Gas Leak Detector Market Size and Trends Analysis

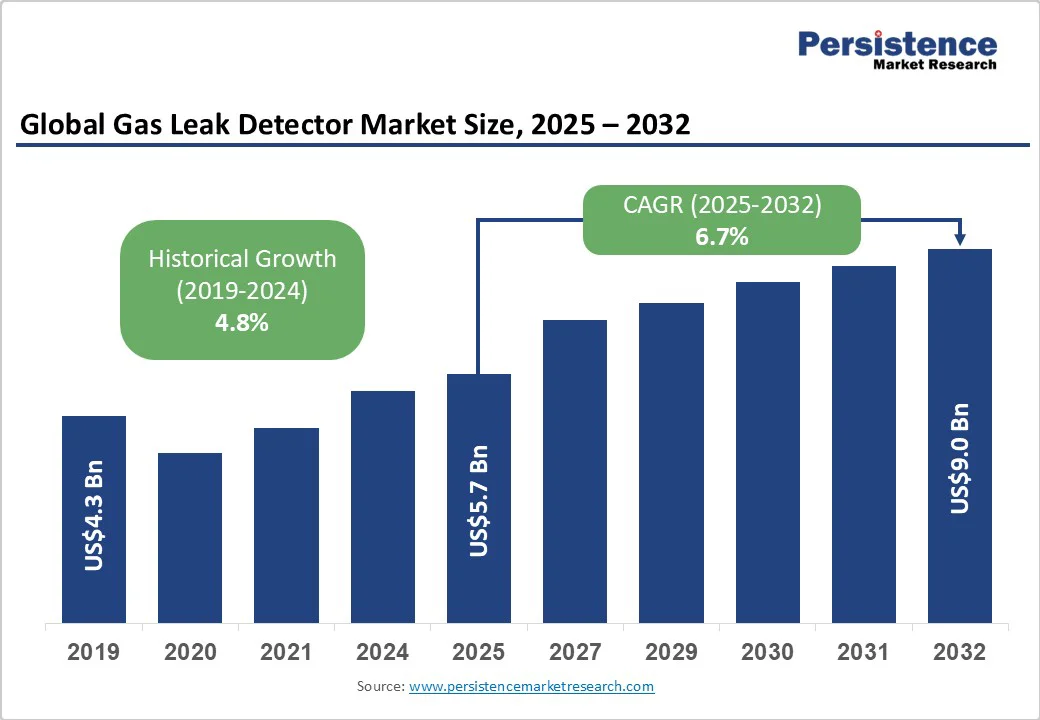

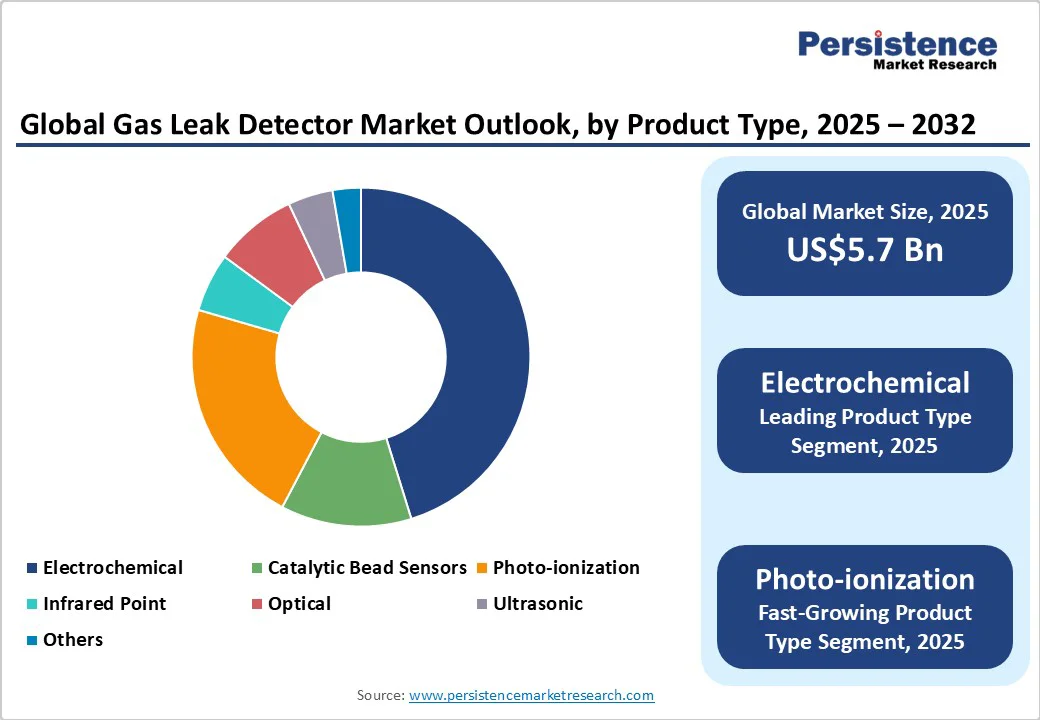

The global gas leak detector market size is likely to be valued at US$5.7 Billion in 2025 and is estimated to reach US$9.0 Billion in 2032, growing at a CAGR of 6.7% during the forecast period 2025-2032, driven by the rising need to prevent catastrophic accidents, protect human lives, and comply with stringent safety regulations. Expansion in the oil and gas and manufacturing sectors further spurs demand.

Key Industry Highlights

- Leading Product Type: Electrochemical gas detection technology holds nearly 45.2% share in 2025, as it provides low maintenance and high accuracy.

- Dominant Installation: Portable detectors, approximately 63.8% of the market share in 2025, due to their mobility and real-time personal safety.

- Key Application: Commercial/industrial recorded about 73.1% of the market share in 2025, with the urgent need to prevent accidents and ensure regulatory compliance.

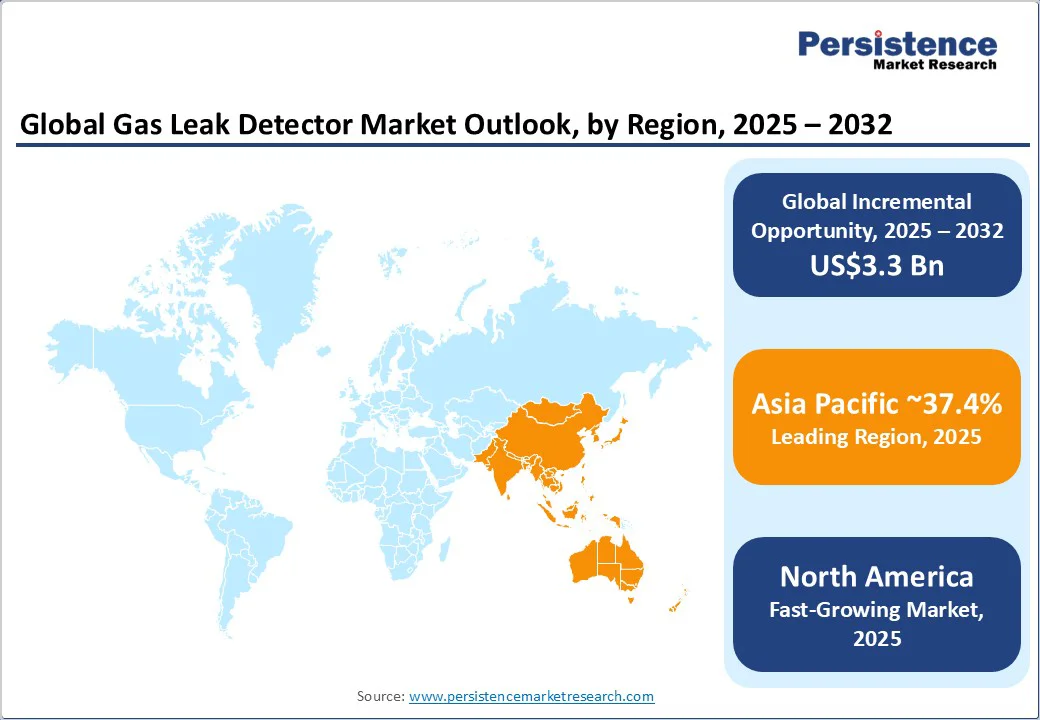

- Leading Region: Asia Pacific, with about 37.4% share in 2025, owing to expanding oil and gas infrastructure and increasing safety awareness.

- Fastest-growing Region: North America, boosted by the adoption of novel detection technologies and strict safety regulations.

- Product Demonstration: INFICON recently demonstrated its ELT Vmax leak testing system at The Battery Show North America. The product helps detect microscopic electrolyte leaks in lithium-ion and sodium-ion battery cells and fully assembled modules.

| Key Insights | Details |

|---|---|

|

Gas Leak Detector Market Size (2025E) |

US$5.7 Bn |

|

Market Value Forecast (2032F) |

US$9.0 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.7% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Protection against Explosions and Fire Hazards

Gas leak detectors play a key role in preventing disastrous incidents such as explosions and fires, which can have devastating consequences for homes, workplaces, and industrial facilities. By providing early detection of flammable gases such as methane or propane, these devices allow timely evacuation and corrective measures, minimizing property damage and loss of life.

Industrial safety regulations in North America and Europe often mandate the use of gas detectors in chemical plants, oil refineries, and manufacturing units. For example, Honeywell’s fixed gas detectors are widely used in refineries to continuously monitor gas concentrations, helping avert potential explosions. This protective function makes gas detectors indispensable in sectors where flammable gases are present.

Early Detection of Invisible Toxic Gases

Various hazardous gases, such as carbon monoxide and hydrogen sulfide, are colorless, odorless, and difficult to detect without specialized equipment. Gas leak detectors provide an early warning system, alerting occupants before exposure reaches life-threatening levels. Carbon monoxide, for instance, binds with hemoglobin and prevents oxygen from reaching vital organs, leading to potentially fatal outcomes if undetected.

Modern detectors, including Kidde’s CO alarms, use unique electrochemical sensors to provide real-time alerts, enabling timely ventilation or evacuation. In residential and industrial settings, this early detection capability drastically reduces the risk of severe illness or fatalities. It is further driving demand for smart, reliable, and connected gas detection systems that integrate with home automation or industrial safety networks.

Barrier Analysis - Frequent Calibration and Maintenance Requirements

Gas leak detectors require consistent calibration and upkeep to ensure accurate readings, which can be both time-consuming and costly for industrial users. Inaccurate calibration may lead to false alarms or undetected leaks, posing safety hazards.

Various industries, especially small and medium enterprises, find it challenging to allocate resources for routine maintenance. Additionally, specialized personnel or service contracts are often necessary to perform these tasks properly, further increasing operational costs. For example, Honeywell emphasizes periodic calibration for its multi-gas detectors, highlighting the urgent requirement for maintenance to meet safety standards.

Sensor Degradation and Susceptibility to Contamination

The sensors in gas leak detectors have a finite lifespan and are vulnerable to degradation over time, reducing their sensitivity and accuracy. Certain gases, dust, or chemical vapors can poison the sensors, leading to faulty readings or complete sensor failure.

For instance, electrochemical sensors, used for detecting toxic gases, such as carbon monoxide may degrade quickly in environments with high sulfur compounds. This limitation compels frequent sensor replacements, adding to operational costs and complicating maintenance schedules.

Opportunity Analysis - Novel MEMS Microphone Arrays for Early Leak Detection

Emerging Micro-Electro-Mechanical Systems (MEMS) microphone arrays are transforming gas leak detection by identifying faint acoustic signals generated by small leaks that traditional detectors often miss. These highly sensitive arrays can pick up the unique sound signatures of escaping gas even at very low pressures, allowing preventive measures before leaks escalate into hazardous situations.

For instance, Sensit Technologies and Emerson are experimenting with MEMS-based acoustic sensors integrated into industrial monitoring systems, enabling continuous, real-time leak detection across pipelines and storage tanks. This development creates opportunities for industries to improve safety standards while reducing maintenance costs.

Fiber Optic Sensing for Continuous Pipeline Monitoring

Fiber optic cables provide a novel approach to gas leak detection by monitoring temperature fluctuations and vibrations along pipelines in real-time. These sensors can detect anomalies caused by escaping gas or mechanical stress, allowing immediate intervention even in remote or hazardous locations.

Picarro and Fotech have implemented distributed fiber optic sensing systems along oil and gas pipelines, providing continuous coverage over tens of kilometers with minimal maintenance. This technology not only improves safety by detecting leaks earlier than conventional methods but also enables predictive analytics for pipeline integrity management.

Category-wise Analysis

Product Type Insights

Electrochemical gas detection technology is predicted to lead with nearly 45.2% of the market share in 2025, spurred by its precision, longevity, and versatility. This method allows for the detection of gases such as carbon monoxide, hydrogen sulfide, and ammonia at parts-per-million (ppm) levels, ensuring early warning in hazardous environments.

Photo-Ionization Detection (PID) technology is gaining popularity owing to its ability to detect a wide range of Volatile Organic Compounds (VOCs) and some inorganic vapors at very low concentrations, even down to parts-per-billion (ppb) levels. It functions by using ultraviolet light to ionize gas molecules, producing charged particles that can be measured to determine gas concentration.

Installation Insights

Portable detectors are speculated to account for approximately 63.8% of the market share in 2025, owing to their mobility and ability to provide personal safety in dynamic environments. These handheld devices are designed for use in areas where gas hazards may be transient or unpredictable, such as during maintenance, inspections, or confined space entries. Their compact size and lightweight nature allow workers to carry them easily, ensuring continuous monitoring of the immediate surroundings.

Fixed detectors are integral to maintaining continuous safety in environments with consistent exposure to hazardous gases. Installed in strategic locations, these systems provide 24/7 monitoring, ensuring that any gas leaks are detected promptly, and appropriate measures are taken. Their ability to monitor multiple gases simultaneously and integrate with other safety systems improves their effectiveness in preventing accidents.

Application Insights

The commercial/industrial segment is estimated to register a market share of around 73.1% in 2025, as gas leak detectors are required for safety, regulatory compliance, and operational continuity. Industries such as oil and gas, chemicals, and power generation operate in environments where hazardous gas leaks can lead to catastrophic incidents, including explosions or toxic exposures.

The residential application of gas leak detectors is experiencing steady growth, primarily due to increased awareness about home safety and the risks associated with undetected gas leaks. Homeowners are becoming more conscious of the potential hazards posed by combustible gases such as natural gas and carbon monoxide, leading to a high demand for detection devices.

Regional Insights

Asia Pacific Gas Leak Detector Market Trends

Asia Pacific is expected to account for approximately 37.4% of the market share in 2025, owing to ongoing industrialization and infrastructure development. China and India are investing heavily in sectors such as oil and gas, petrochemicals, and utilities, leading to an increased demand for gas detection systems. India’s gas demand is projected to triple by 2040, necessitating the expansion of pipeline networks and the implementation of novel leak detection technologies.

It is further supported by stringent safety regulations and a rising focus on environmental protection, prompting industries to adopt unique gas leak detection solutions. Asia Pacific is witnessing a shift toward IoT-enabled and wireless gas leak detectors, improving real-time monitoring and remote diagnostics. Such smart systems provide advantages such as reduced maintenance costs, quick response times, and integration with existing industrial networks.

North America Gas Leak Detector Market Trends

In North America, stringent regulations are influencing the adoption of novel gas leak detection technologies. The Pipeline and Hazardous Materials Safety Administration (PHMSA) issued a final rule on January 17, 2025, mandating pipeline operators to implement unique leak detection programs. These programs require operators to detect and repair all gas leaks, including those from transmission, distribution, and gathering pipelines, within specified timeframes.

The rule emphasizes the use of best available technologies and practices to minimize gas releases, thereby improving public safety and environmental protection. The Bureau of Land Management's 2024 Waste Prevention Rule also requires oil and gas operators to develop leak detection and repair plans to avoid natural gas waste. This regulation ensures that operators take reasonable steps to prevent gas leaks and properly compensate public and Tribal mineral owners through royalty payments when natural gas loss could have been avoided.

Europe Gas Leak Detector Market Trends

Europe’s market is being propelled by stringent regulations aimed at reducing greenhouse gas emissions and improving safety standards. The European Union's Methane Emission Reduction Regulation (MERR), effective from May 2025, mandates operators to implement comprehensive Leak Detection and Repair (LDAR) programs. These programs require the identification and repair of methane leaks, with specific timelines for different leak sizes.

For instance, Type 1 leaks, defined as those emitting 17 grams per hour or 7000 ppm of methane, must be repaired promptly, while Type 2 leaks have longer timelines. This regulatory framework necessitates the adoption of cutting-edge gas leak detection technologies such as Optical Gas Imaging (OGI) cameras and Acoustic Leak Imaging (ALI) devices to comply with the stringent requirements.

Competitive Landscape

The global gas leak detector market is highly competitive, with key companies such as Honeywell, Drägerwerk, MSA Safety, and Emerson Electric leading the global landscape. These companies focus on technological developments, product reliability, and pricing strategies to maintain their market positions. Differentiation through features, including IoT connectivity, multi-gas detection, and user-friendly designs, is pivotal. Players also emphasize superior distribution channels and responsive after-sales support to improve customer satisfaction.

Key Industry Developments

- In October 2025, Sensors Inc. introduced the Bar Hole Sampler, a groundbreaking all-in-one device that redefines efficiency and precision in natural gas leak management. It combines pinpointing, purging, and quantification within a single compact system.

- In March 2024, Emerson launched the Rosemount 9195 Wedge Flow Meter. It is a fully integrated solution consisting of a wedge primary sensor element, supporting components, and a selectable Rosemount pressure transmitter.

Companies Covered in Gas Leak Detector Market

- New Cosmos Electric Co. Ltd.

- Emerson Electric Co.

- ABB

- Teledyne Technologies Inc.

- Halma Plc.

- Fortive Corporation

- Honeywell International Inc.

- Drägerwerk AG & Co. KGaA

- MSA Safety Inc.

- PCE Instruments UK Ltd.

- Riken Keiki Co., Ltd.

Frequently Asked Questions

The gas leak detector market is projected to reach US$5.7 Billion in 2025.

Rising industrial safety regulations and the need to prevent explosions are the key market drivers.

The gas leak detector market is poised to witness a CAGR of 6.7% from 2025 to 2032.

Adoption of fiber optic pipeline monitoring and rising demand for multi-gas detection technologies are the key market opportunities.

New Cosmos Electric Co. Ltd., Emerson Electric Co., and ABB are a few key market players.