- Beauty & Personal Care

- Face Shields Market

Face Shields Market Size, Share, and Growth Forecast 2026 - 2033

Face Shields Market by Product Type (Full Face Shield and Half Face Shield), Material Type Polycarbonate, Cellulose Acetate, Steel Mesh, Nylon, and PETG), Industry (Healthcare, Chemical, Oil & Gas, Construction, Manufacturing, and Others), and Regional Analysis for 2026 to 2033

Face Shields Market Size and Share Analysis

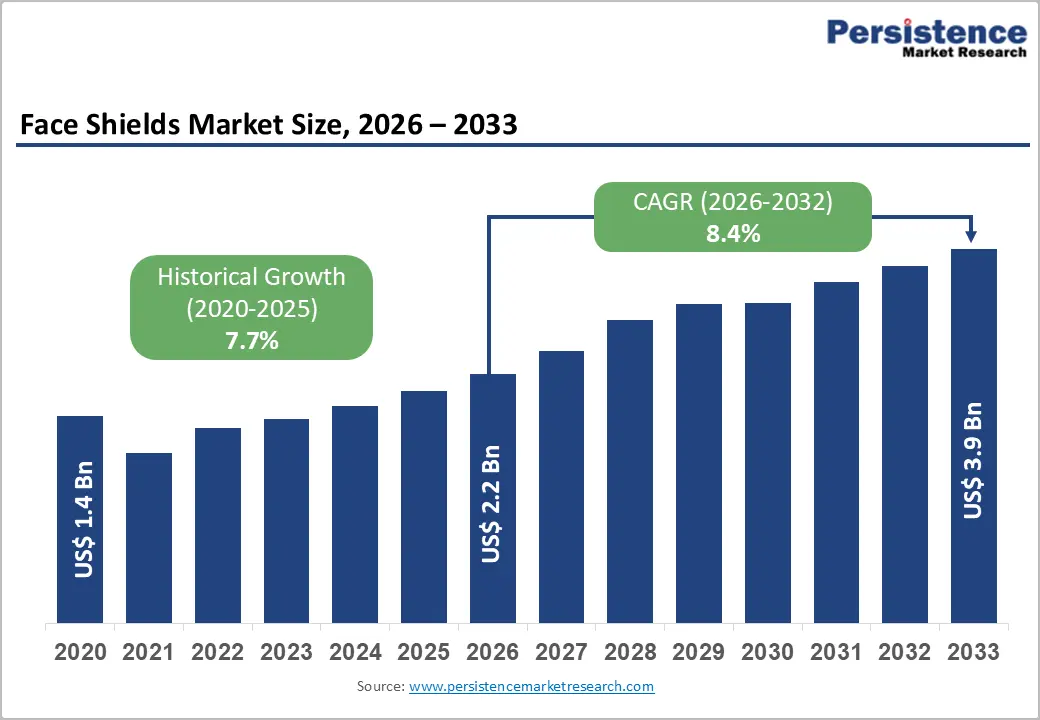

The global face shields market size is likely to be valued at US$ 2.2 billion in 2026 and is projected to reach US$ 3.9 billion by 2033, growing at a CAGR of 8.4% between 2026 and 2033.

Market expansion is driven by embedded post-pandemic behavioral practices that have established sustained demand for personal protective equipment across healthcare, construction, and industrial sectors, combined with stringent infection-prevention protocols and regulatory mandate enforcement by OSHA, CDC, and national public-health authorities, creating structural market growth.

Technological advancements in anti-fog coatings, impact-resistant materials, and lightweight, reusable designs further boost market expansion over the forecast period.

Key Industry Highlights:

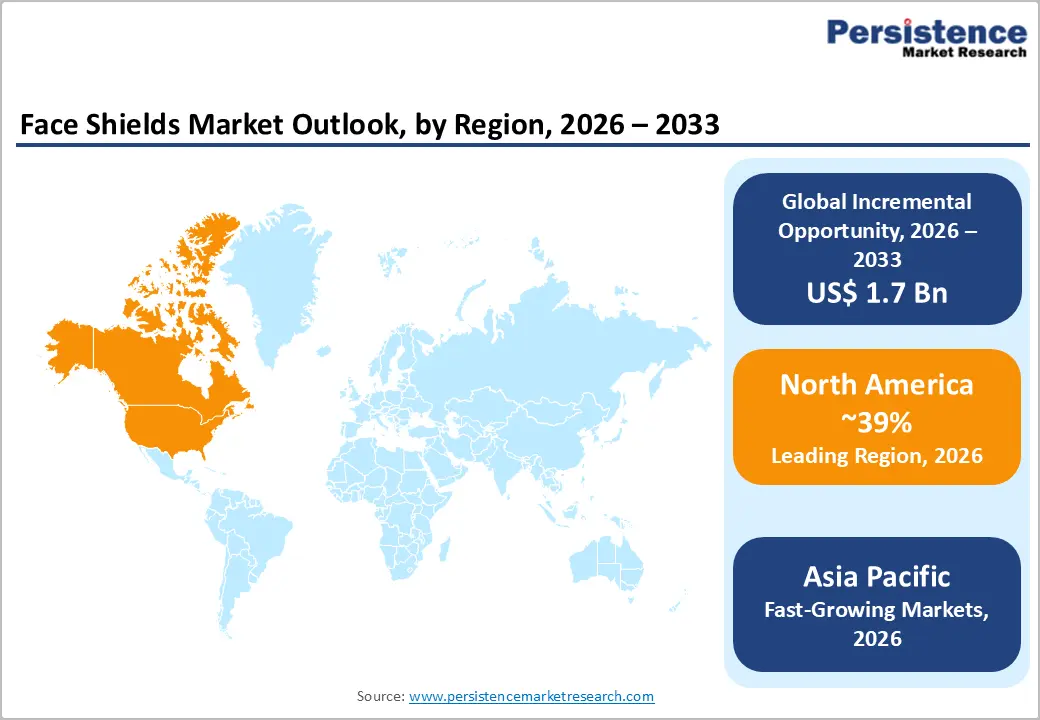

- Leading Region: North America maintains market leadership anchored by the United States healthcare infrastructure dominance with 860 million annual physician visits, 130 million emergency department visits, a stringent OSHA and CDC regulatory framework enforcement, and established domestic manufacturing capacity for face shield production.

- Fastest-Growing Region: Asia Pacific commands the fastest expansion, driven by China's 60% global manufacturing dominance, India's 50 million monthly diagnostic tests, and 1.4 billion population urbanization, Southeast Asia's healthcare infrastructure expansion, and government digital health initiatives promoting healthcare worker protection.

- Dominant Product Type: Full-face shields command market dominance with a 75% share, driven by comprehensive forehead-to-chin protection requirements, healthcare disposables preference at 65.2%, industrial application prevalence, and OSHA occupational-safety standard compliance mandates.

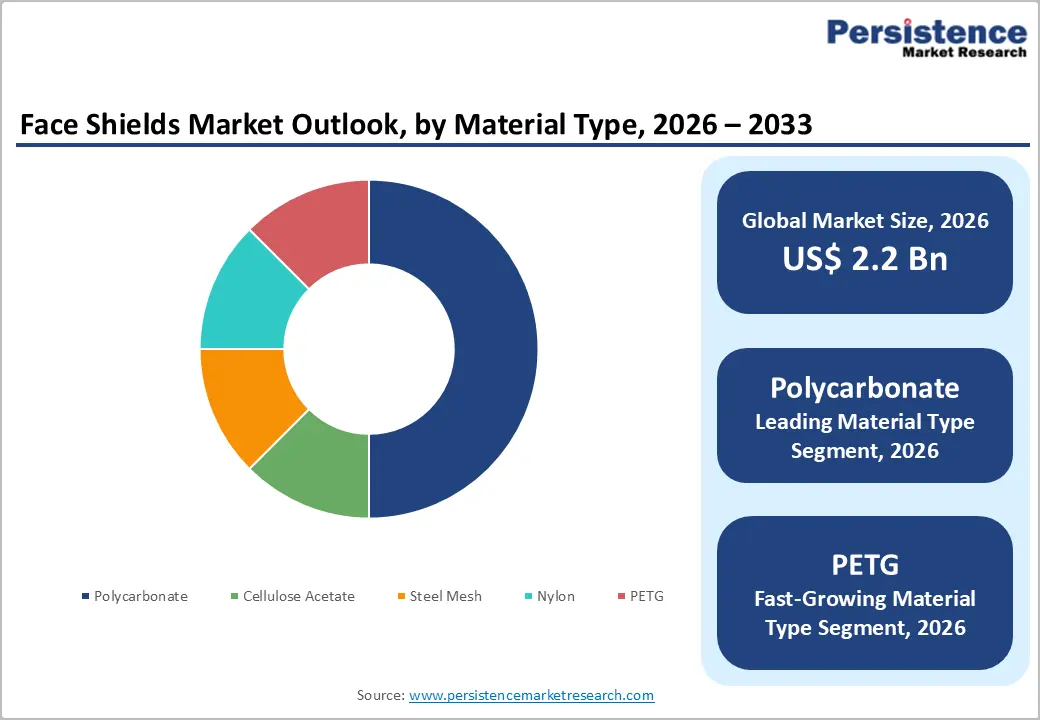

- Growing Material Type: Polycarbonate materials are experiencing the fastest growth momentum with advanced anti-fog coating technology and specialized heat-resistant applications, propelled by Honeywell's January 2024 breakthrough innovations, BASF's Ultrason E thermoplastic introduction, and industry-specific performance customization.

- Key Market Opportunity: Asia-Pacific emerging-market penetration, with India's exceptional fastest-growing market trajectory; Southeast Asia's healthcare infrastructure expansion; cost-competitive manufacturing advantage enabling aggressive pricing; and government digital health initiatives promoting diagnostic testing and healthcare worker protection, and infrastructure development.

| Key Insights | Details |

|---|---|

| Face Shields Market Size (2026E) | US$ 2.2 Bn |

| Market Value Forecast (2033F) | US$ 3.9 Bn |

| Projected Growth CAGR (2026 - 2033) | 8.4% |

| Historical Market Growth (2020 - 2025) | 7.7% |

Market Dynamics

Drivers - Healthcare-Associated Infection Prevention and Occupational Safety Regulatory Mandate Enforcement

The critical healthcare worker protection requirement, driven by healthcare-associated infections affecting 7% of patients in high-income regions and 15% in low- and middle-income countries, according to WHO epidemiological data, establishes a fundamental medical necessity for continuous face shield deployment. Aerosol-generating procedures, including intubation, bronchoscopy, dental drilling, suctioning, and nasopharyngeal swabbing, documented by CDC research, are associated with 3.4 times higher exposure risk in aerosol-heavy environments, warranting mandatory protective measures. Regulatory framework enforcement by OSHA and CDC mandates requiring face and eye protection for aerosol-generating interventions, combined with 200,000 plus dental practices across the United States and Canada performing high-aerosol-exposure procedures, establishes sustained high-volume demand.

Post-pandemic behavioral embedding, where face shields became an integrated standard PPE component in hospitals, laboratories, and emergency response systems, creates structural market persistence beyond the temporary COVID-19 surge demand. Diagnostic testing infrastructure expansion, particularly in the Asia-Pacific region, with India performing over 50 million diagnostic tests monthly, establishes sustained healthcare-sector demand growth, ensuring a multi-year market expansion trajectory through the forecast period.

Industrial Sector Expansion and Occupational Hazard Protection Necessity

Explosive construction and manufacturing industry growth, particularly in Asia-Pacific emerging markets such as China and Southeast Asia, is driving substantial demand for face shields to protect workers from impact hazards, chemical splashes, and thermal exposures. Chemical processing industry expansion with accelerating growth in Asia-Pacific and Latin America regions, creating specialized demand for impact and chemical-resistant face shield materials, including polycarbonate and cellulose acetate variants optimized for splash protection in hazardous environments.

Oil and gas sector operations requiring heat-resistant and thermal-protective face shields, including specialized high-heat reflective variants using 99.99% fine gold coating for molten substance splash protection, establish a premium market segment. Automotive and transportation manufacturing, including vehicle assembly, welding, and parts processing operations, is driving widespread shield deployment across production facilities. Digitalization in the construction industry and emerging-market infrastructure buildout, particularly in India, Southeast Asia, and Latin America, are creating long-term construction project pipelines that support sustained multi-year face shield demand, ensuring industrial-sector growth sustainability through the forecast period.

Restraint - Post-Pandemic Demand Normalization and Purchasing Behavior Correction

The global face shields market is experiencing a structural slowdown following the exceptional demand spike during the COVID-19 pandemic. During the crisis period, governments, hospitals, and healthcare institutions procured face shields in unusually high volumes to build emergency stockpiles. As these inventories were largely replenished by 2022-2023, procurement patterns have normalized, significantly reducing repeat purchase frequency. Many healthcare systems are currently prioritizing consumption of existing stock before initiating new procurement cycles, thereby directly suppressing short-term market demand.

The healthcare budgets, especially in emerging and price-sensitive markets, have tightened post-pandemic, leading to increased focus on cost containment. This has led to a shift toward low-cost or reusable alternatives and a reduced willingness to pay premiums for advanced or branded face shield products. Consequently, manufacturers face pressure on both sales volumes and margins, limiting near-term growth momentum.

Supply Chain Disruption and Raw Material Availability Constraints

Face shield production remains vulnerable to disruptions in the supply of key raw materials such as polycarbonate and cellulose acetate. These materials are often sourced from a limited number of regions, creating dependency risks and constraining manufacturing scalability during periods of supply volatility. Fluctuations in raw material availability directly affect production schedules and cost structures, restricting manufacturers’ ability to optimize pricing.

Moreover, import-export regulations, trade compliance requirements, and tariff fluctuations, particularly for companies reliant on Asian raw material suppliers, further complicate the supply chain. These factors increase procurement costs and price uncertainty, making it difficult for manufacturers to maintain stable pricing in global markets. Collectively, these challenges act as a restraint on market expansion, especially for small and mid-sized face shield producers.

Opportunity - Advanced Material Innovation and Specialized Application Segment Development

Technological advancement in anti-fog coating chemistry is demonstrated by Honeywell's January 2024 impact-resistant design breakthrough, combined with BASF's Ultrason E high-performance thermoplastic introduction for reusable shields, creating a differentiation opportunity, enabling premium pricing for technologically advanced products. Lightweight and foldable face shield design innovation addressing portability and reusability requirements, particularly for healthcare and informal-sector workers in emerging markets, creating a cost-effective product category.

Heat-resistant and high-temperature specialized shield development for foundry operations, steelworking, and oil-and-gas thermal hazard environments, establishing a premium niche market segment. Medical-grade material certification expansion, including FDA approval pathways for advanced thermoplastic and polycarbonate variants, enabling healthcare-specific product positioning. Laser safety face shield emerges as a specialized application niche with an estimated USD 105.2 million market (2025) in additive manufacturing and advanced materials processing, establishing an emerging category opportunity, creating a multi-segment expansion opportunity through the forecast period.

Integration of Face Shields into Routine Infection Control and Industrial Safety Protocols

The expanding adoption beyond pandemic-driven emergency use into routine infection prevention and occupational safety applications presents a key opportunity for the global face shields market. Healthcare facilities are increasingly incorporating face shields as standard protective equipment for procedures involving splash, spray, or close patient contact, particularly in emergency care, dentistry, laboratories, and outpatient clinics. This shift from episodic procurement to protocol-driven usage creates a more stable and recurring demand base.

Beyond healthcare, industries such as pharmaceuticals, food processing, chemicals, and manufacturing are strengthening workplace safety standards to comply with evolving occupational health regulations. Face shields are gaining traction as a complementary protective solution alongside masks and goggles, especially in environments requiring full-face protection and improved visibility. The growing emphasis on employee safety, regulatory compliance, and risk mitigation in these sectors supports sustained market growth.

Product innovations, such as lightweight reusable shields, anti-fog coatings, enhanced optical clarity, and ergonomic designs, offer manufacturers opportunities for differentiation and value-added pricing. As organizations prioritize durability, comfort, and long-term cost efficiency, suppliers that align their face shield offerings with routine safety protocols and industrial standards are well positioned to capture incremental demand and improve market resilience.

Category-wise Analysis

Product Type Insights

Full face shields hold a dominant market position, with an estimated 75% share, driven by comprehensive forehead-to-chin coverage that provides maximum protection against splashes, aerosols, and impact hazards. Healthcare application prevalence: disposable medical shields capture 65.2% market share, reflecting infection-prevention protocol requirements in hospitals, outpatient departments, and diagnostic facilities. Industrial applications are particularly prevalent in construction, manufacturing, chemical processing, and thermal environments that require maximum worker protection.

OSHA and occupational-safety standards mandate full-face protection for aerosol-generating procedures and high-risk operations, supporting a full-shield category preference. Psychological acceptance, where complete facial coverage provides users with a superior sense of protection, driving consumer preference despite higher cost versus half-shield alternatives, maintains full-shield market leadership throughout the forecast period.

Material Type Insights

Polycarbonate materials command an estimated 55% market share, driven by superior impact resistance with excellent protection against high-speed particles and mechanical hazards. Heat resistance capability up to 130 degrees Celsius, enabling applications in thermal environments, including automotive manufacturing and welding operations. Optical clarity and visibility advantage supporting worker productivity in production-intensive environments.

Manufacturing flexibility enabling injection molding and specialized coating applications, including anti-fog treatments and gold reflective heat-protective coatings. 3M W series and PELTOR polycarbonate shield dominance reflecting market leader positioning through established supply chains and quality reputation. Cost-competitive production supporting mass-market affordability across emerging markets, maintaining polycarbonate material leadership throughout the forecast period.

Industry Insights

Healthcare commanding an estimated 45% market share, driven by hospital pharmacy distribution capturing 48.9% market share, and disposable medical shield preference of 65.2%. The infection-prevention protocol mandates continuous use of face shields in intensive care units, operating rooms, emergency departments, and infectious-disease wards. Dental practice prevalence: 200,000+ practices across the United States and Canada performing high-aerosol-exposure procedures that require mandatory eye and face protection.

Post-pandemic behavioral embedding establishes long-term adoption across hospitals, laboratories, and diagnostic facilities. Telemedicine expansion and remote patient care growth creating emerging healthcare segment opportunity.Construction and manufacturing combined, capturing 35% market share, driven by worker protection requirements in high-risk operational environments with impact hazards, chemical splashes, and thermal exposures. Chemical sector capturing 15% share with specialized splash-protection requirements and chemical-resistant material necessity, ensuring multi-sector industrial growth sustainability through forecast period.

Regional Insights

North America Face Shields Market Trends

North America maintains developed market maturity with the United States commanding regional leadership through extensive healthcare infrastructure, including 860 million annual physician office visits, 130 million emergency department visits, and 200,000-plus dental practices, establishing exceptionally high-volume face shield demand. Strict occupational-safety regulatory framework enforced by OSHA and CDC mandates requiring mandatory eye and face protection in aerosol-generating procedures, driving consistent healthcare-sector adoption.

Domestic manufacturing capacity development including 3M, Honeywell, MSA, and specialized manufacturers establishing supply chain resilience and innovation leadership. Established quality standards and certification pathways enabling rapid product development and commercialization, supporting sustained market leadership through the forecast period.

Europe Face Shields Market Trends

Europe face shields market continues to be shaped by stringent regulatory environments and a strong emphasis on occupational health and safety. The European Union’s PPE regulations mandate rigorous performance standards, which have driven demand for certified, high-quality face shields across healthcare and industrial sectors. Countries such as Germany, the UK, and France lead regional consumption, supported by extensive hospital networks and robust manufacturing sectors that integrate face shields into routine safety protocols beyond pandemic spikes. This regulatory backdrop, alongside increasing awareness of workplace safety and infection control, continues to stabilize demand even as post-COVID normalization progresses.

European market trends highlight a preference for reusable, ergonomic, and advanced face shield designs that align with sustainability goals and long-term cost efficiency. Growth is not limited to healthcare; sectors like construction, manufacturing, and laboratories are increasingly adopting face shields as part of comprehensive PPE kits to protect workers from chemical splashes, debris, and airborne particulates. Innovation in features such as anti-fog coatings and adjustable fittings is enhancing user comfort and broadening appeal across diverse end-use applications. Europe’s market is projected to grow steadily at a moderate CAGR, driven by regulatory compliance, industrial safety standards, and ongoing investments in health infrastructure.

Asia Pacific Face Shields Market Trends

Asia-Pacific commands the fastest regional growth at 7.7% CAGR, driven by China establishing global manufacturing dominance with 60% global PPE production capacity and economies-of-scale cost advantage. India is experiencing exceptional, fastest-growing market conditions, with 50 million monthly diagnostic tests requiring face shield protection, combined with a 1.4 billion population and rapid urbanization, creating a massive addressable market.

Southeast Asia healthcare system expansion in Vietnam, Indonesia, the Philippines, and Thailand, creating sustained demand growth from developing-market hospital buildout. Government digital health initiatives promoting diagnostic testing infrastructure development and healthcare worker protection, establishing a multi-year demand growth trajectory, and ensuring Asia-Pacific market leadership dominance through the forecast period.

Competitive Landscape

The face shields market exhibits moderate to high fragmentation with tier-one global diversified manufacturers, including 3M, Honeywell, and MSA, commanding substantial market share through comprehensive product portfolios, established supply chains, and regulatory expertise. Specialized regional manufacturers, including KARAM, Pyramex, and Aspen Surgical, are establishing competitive positions through industry-specific product innovation and regional distribution networks.

Material suppliers, including Curbell Plastics, BASF, and DuPont Teijin Films, differentiate through advanced material development and customization capabilities. Consolidation trend evident through strategic acquisitions and manufacturing capacity expansion, demonstrating market maturation and competitive intensity, supporting sustained innovation-driven competition.

Key Developments:

- In February 2025, Aspen Surgical expanded manufacturing capabilities with advanced US-based production facilities, enhancing supply chain resilience and meeting rising demand across healthcare sectors with technologically advanced face shields.

- In January 2024, Honeywell unveiled advanced anti-fog coating technology and impact-resistant design innovations, raising safety standards across the healthcare and industrial sectors globally and establishing competitive differentiation through performance advancements.

- In January 2022, BASF introduced Ultrason E thermoplastic material offering superior transparency, durability, and chemical resistance, boosting innovation in the protective face shields market and supporting reusable product development in emerging markets.

Companies Covered in Face Shields Market

- 3M

- Honeywell International Inc.

- AlphaProTech

- CASCO BAY MOLDING

- KCWW

- Lakeland Inc.

- MSA

- Aspen Surgical Products, Inc.

- Prestige Ameritech

- Pyramex

- DuPont Teijin Films

- Medline Industries

- Radians

- Kimberlay-Clark

- KARAM

Frequently Asked Questions

The global Face Shields Market is projected to reach US$ 3.9 billion by 2033, expanding from US$ 2.2 billion in 2026 at a CAGR of 8.4%, driven by healthcare-associated infection prevention, occupational safety regulatory compliance, Asia-Pacific industrial expansion, and advanced material technology innovation including anti-fog coatings and specialized thermal-protective variants.

Market demand growth is driven by multiple converging factors including post-pandemic behavioral embedding establishing sustained PPE demand, WHO-documented healthcare-associated infections affecting 7-15% of patients, CDC-documented 3.4 times higher exposure risk in aerosol environments, OSHA and CDC regulatory mandate enforcement, Asia-Pacific healthcare infrastructure expansion with India performing 50 million monthly diagnostic tests, construction and manufacturing industry growth particularly in emerging markets, and technological advancement in anti-fog coatings and impact-resistant materials.

Full face shields command market leadership with estimated 75% market share, driven by comprehensive forehead-to-chin protection requirement, healthcare disposable preference at 65.2%, industrial application prevalence in high-risk environments, and OSHA occupational-safety standard compliance mandate for maximum facial coverage.

North America maintains market leadership anchored by United States healthcare infrastructure dominance with 860 million annual physician visits and 130 million emergency department visits, 200,000 plus dental practices, stringent OSHA and CDC regulatory framework enforcement, and established domestic manufacturing capacity for face shield production.