- Automotive

- Europe Off-road Vehicle Market

Europe Off-road Vehicle Market Size, Share, and Growth Forecast, 2026- 2033

Europe Off-road Vehicle Market by Vehicle Type (Passenger Vehicle, Light Commercial Vehicle, Heavy Commercial Vehicle), Propulsion Type (BEV, HEV, PHEV, and FCEV), Range (Up to 150 Km, 151 to 300 Km, 301 to 500 Km, above 500 Km), and Regional Analysis for 2026 - 2033

Europe Off-road Vehicle Market Size and Trends Analysis

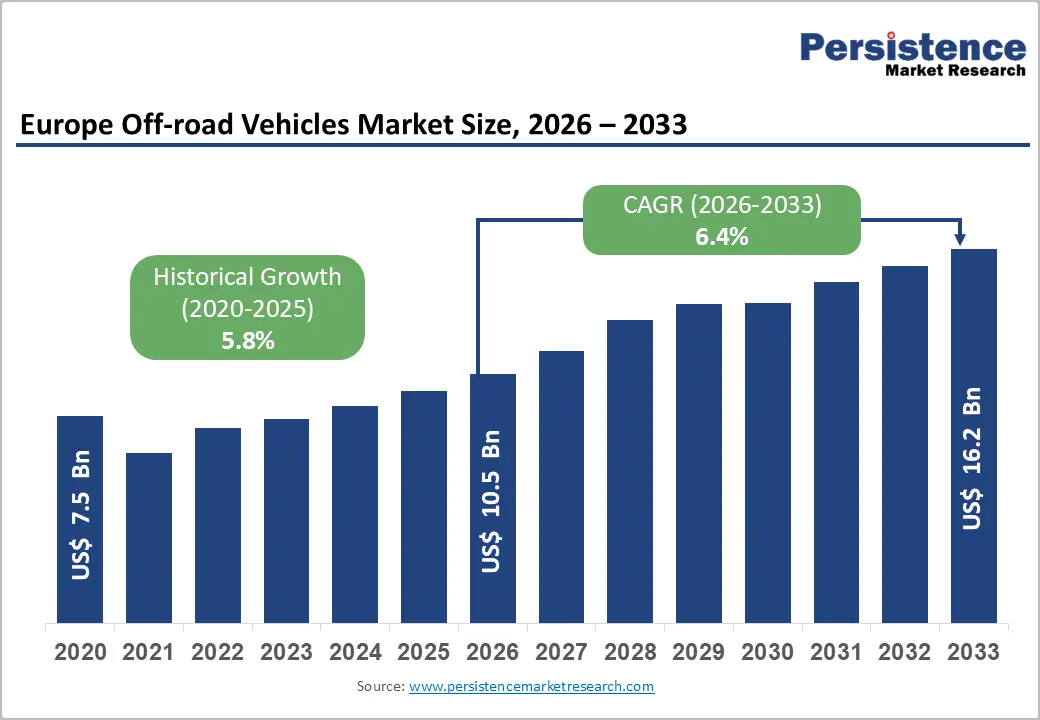

The Europe off-road vehicles (ORV) market was valued at US$ 10.5 billion in 2026 and is projected to reach US$ 16.2 billion by 2033, growing at a CAGR of 6.4% between 2026 and 2033. The market registered a historical CAGR of 5.8% from 2020 (US$ 7.5 Bn) to 2026, underscoring a sustained and accelerating demand trajectory.

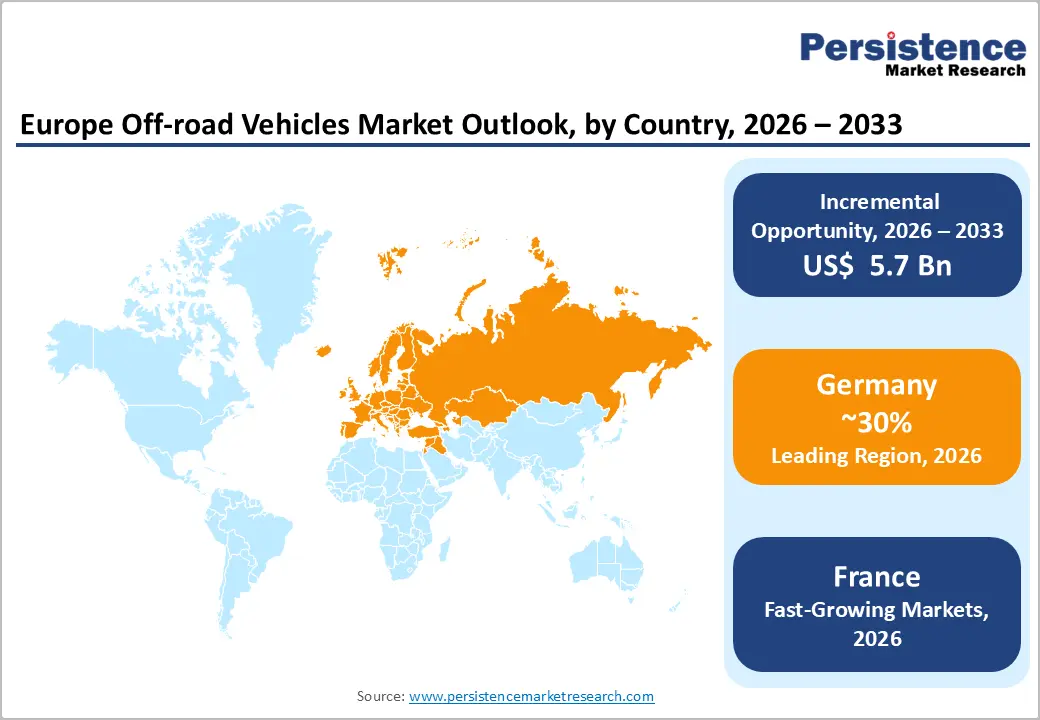

The market's growth is primarily driven by rising demand for recreational and utility off-road vehicles across both developed and emerging European economies. Increasing adoption of electric propulsion technologies, supportive government policies for sustainable mobility, and expanding military modernisation programmes are key catalysts. Germany leads regional revenue at over 30% share, while France emerges as the fastest-growing country with a 7.5% CAGR, reflecting robust domestic investment and shifting consumer preferences toward adventure mobility and outdoor recreation.

Key Industry Highlights:

- Product Type Analysis: Utility Terrain Vehicles lead product type revenue with above 40% market share in 2026; All-Terrain Vehicles are the fastest-growing product type at a 7.0% CAGR through 2033.

- Electric Propulsion Leads Growth: Electric ORVs are expanding at the fastest propulsion CAGR of 7.2%, driven by EU Green Deal mandates, OEM electrification strategies, and declining battery costs.

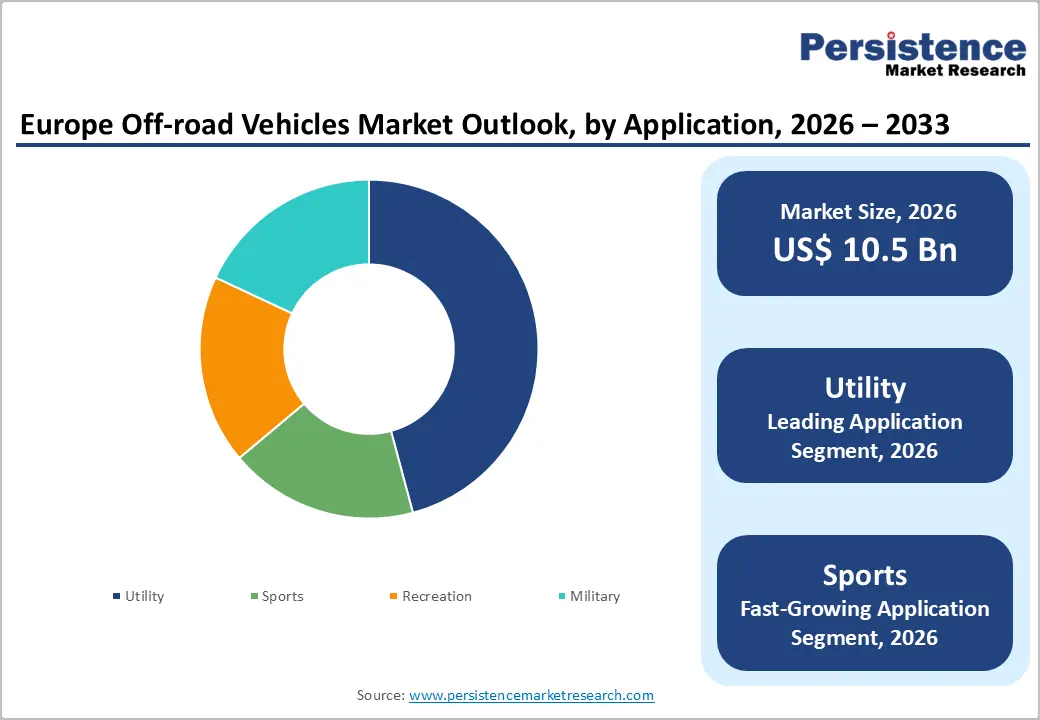

- Utility Application Dominates: Sports Outpaces All: Utility remains the largest application with above 45% revenue share, while the Sports segment grows fastest at 7.1% CAGR, reflecting Europe's expanding recreational motorsport culture.

- Country Analysis: Germany commands above 30% of European ORV revenue in 2026; France is the fastest-growing country at 7.5% CAGR, driven by adventure tourism, EV incentives, and military procurement.

- Competitive Dynamics: Top players (Polaris, BRP, Honda, Yamaha, Textron) hold 55-65% market share; Chinese entrants (CFMOTO, Segway Powersports) are disrupting value segments through Eastern European manufacturing and competitive pricing.

- Strategic Imperatives: Electrification, digital connectivity, and distribution network deepening are the defining strategic battlegrounds for European ORV market leadership through 2033.

| Key Insights | Details |

|---|---|

| Europe Off-road Vehicle Market Size (2026E) | US$ 10.5 Bn |

| Market Value Forecast (2033F) | US$ 16.2 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.8% |

Market Dynamics

Drivers - Rising Recreational Outdoor Activity and Adventure Tourism Fuelling Sustained ORV Demand

Europe has seen a significant uptick in outdoor recreational participation post-pandemic, with the European Outdoor Group reporting that participation in outdoor activities rose by more than 20% between 2020 and 2024. This behavioural shift directly correlates with increased consumer spending on ATVs and UTVs for recreational use. The adventure tourism market in Europe, valued at approximately US$ 69 billion, continues to generate ancillary demand for off-road capable vehicles.

Governments across Germany, France, and Scandinavia have expanded off-road trail infrastructure and recreational zones. The sports application segment is growing at a 7.1% CAGR, validating the structural shift in demand. Rising disposable incomes among European households further enable premium ORV purchases, sustaining long-term market momentum.

Electrification Wave and Regulatory Push Accelerating Adoption of Zero-Emission ORVs

The European Union's Green Deal and Fit for 55 legislative package mandate a 55% reduction in CO2 emissions from road transport by 2030, compelling ORV manufacturers to accelerate the integration of electric powertrains. The electric ORV segment is projected to expand at a CAGR of 7.2%, the fastest among all propulsion types, as manufacturers like Polaris and BRP introduce battery-electric UTVs and ATVs. EU state subsidies for electric vehicle adoption, including purchase incentives in France (Bonus Écologique) and Germany (Umweltbonus), are actively reducing the total cost of ownership for electric ORVs. Industry bodies such as the European Association of Motorcycle Manufacturers (ACEM) have flagged regulatory tailwinds as a key competitive frontier for OEMs through 2033.

Restraint - High Acquisition and Ownership Costs Limiting Mass-Market Penetration of Premium ORVs

The average selling price of utility terrain vehicles in Europe ranges between €15,000 and €35,000, creating a significant affordability barrier for price-sensitive consumer segments. Insurance, maintenance, and storage costs further elevate total ownership expenses. In markets like Spain and Italy, where per-capita disposable income remains below the EU average, demand penetration remains structurally constrained. Additionally, the transition to electric powertrains, while demand-accretive in the long term, currently commands a 20-35% price premium over equivalent combustion-engine models, slowing near-term volume conversion and limiting addressable market expansion.

Regulatory Fragmentation and Stringent Environmental Access Restrictions Across European Markets

Despite EU-level harmonisation efforts, off-road vehicle usage regulations remain fragmented across member states. Countries including France, Germany, and Austria impose strict restrictions on ORV operation in national parks, protected natural areas (Natura 2000 network covering ~18% of EU land), and mountain regions. Varying homologation requirements across markets increase OEM compliance costs. The European Environment Agency's escalating focus on biodiversity preservation is expected to tighten land-access rules further by 2027, potentially limiting growth in recreational demand in ecologically sensitive regions and complicating route planning for adventure tourism operators relying on ORV experiences.

Opportunity- Connected and Autonomous ORV Technology Creating Premium Differentiation and New Revenue Streams

The integration of telematics, IoT connectivity, and semi-autonomous navigation systems into ORVs presents a material opportunity for product differentiation for OEMs. Fleet management solutions for commercial and utility ORV operators including rental companies, agriculture operators, and defense contractors are projected to generate incremental software-as-a-service (SaaS) revenue streams. According to estimates aligned with McKinsey's mobility technology assessments, connected vehicle software revenue in the ORV segment could reach US$ 400-600 million across Europe by 2030. OEMs that invest early in proprietary digital ecosystems and over-the-air update capabilities will establish defensible competitive moats and superior customer retention metrics.

Growth of ORV Rental and Sharing Economy Models in European Tourist Destinations

The sharing economy model is gaining meaningful traction in European adventure tourism corridors, particularly in Alpine regions (Austria, Switzerland, France) and Nordic countries (Norway, Finland). ORV rental operators are expanding their fleets, creating B2B demand from OEMs offering commercial fleet pricing and service packages. The European short-term vehicle rental market grew at approximately 8% annually between 2022 and 2025. This model reduces individual consumer price sensitivity, enabling penetration of premium electric ORV models at a lower per-session cost. Manufacturers offering fleet leasing, predictive maintenance packages, and charging infrastructure support will gain preferred-supplier status with growing rental operators.

Growth in Charging Infrastructure for Rural Areas

The growth of charging infrastructure, especially in rural and underserved regions, presents a significant opportunity for the European electric vehicle (EV) market. As urban areas become saturated with EVs, expanding charging networks into rural locales can significantly enhance EV adoption rates.

Governments and private companies are beginning to recognize this need and are likely to invest in developing charging stations to ensure that rural populations are not left behind in the transition to electric mobility. Initiatives in countries like France and Italy are already underway to bolster charging availability in less populated areas, making EVs more appealing to potential buyers.

The integration of innovative charging solutions, such as mobile charging units and solar-powered charging stations, can further enhance access in remote locations. These advancements not only address range anxiety but also align with the European Union’s sustainability goals by promoting green energy solutions. As infrastructure continues to expand, the opportunity to capture a broad consumer base in rural areas will be instrumental in driving the growth of the EV market across the region.

Category-wise Analysis

Product Type Insights

Utility Terrain Vehicles (UTVs) are the dominant product segment, accounting for above 40% of total market revenue in 2026. UTVs' dominance is anchored in their versatility across agricultural, industrial, and military applications, making them the preferred workhorse for fleet buyers and institutional customers. Their higher payload capacity, cabin enclosures, and accessory compatibility drive premium average selling prices, maximising per-unit revenue contribution. Key end-users include European farm operators, construction site managers, and government procurement agencies.

All-Terrain Vehicles (ATVs) represent the fastest-growing product segment, expanding at a CAGR of 7.0% through 2033. Rising demand from recreational riders, growing ORV club memberships across Germany and the Nordic countries, and the introduction of compact, entry-level ATV models by leading OEMs are the primary drivers of growth. The expansion of dedicated ATV trail networks and adventure parks across Europe further stimulates retail demand. Snowmobiles and three-wheelers represent niche but strategically important segments, particularly in Nordic and Alpine markets.

Propulsion Type Insights

Gasoline-powered ORVs maintain the largest propulsion-type share, above 45% of 2026 revenue. Their established supply chain, widespread fuelling infrastructure, and superior power-to-weight ratio ensure continued dominance through the near-to-medium term. Consumer familiarity and a lower initial purchase price relative to electric alternatives sustain gasoline's market leadership. Diesel-powered models hold a secondary position, particularly in heavy-duty utility and military applications, where torque and low-speed range are operationally critical.

The electric propulsion segment is growing at the fastest CAGR of 7.2%, propelled by EU emissions regulations, OEM electrification commitments, and improving battery energy density. Companies including Polaris (RANGER EV), Textron (Cushman EV), and emerging EV-native startups are introducing electric UTVs and ATVs targeting both recreational and utility buyers. Declining lithium-ion battery costs have decreased approximately 80% over the past decade, progressively closing the price gap with combustion models, accelerating adoption timelines.

Application Insights

Utility Applications Anchor Revenue Base While Sports Segment Captures Fastest Growth

The Utility application segment leads the market with a revenue share above 45% in 2026. Demand is driven by agriculture, mining, construction, and government/defence procurement, where operational durability and cargo capability are paramount. European agricultural mechanisation trends, backed by CAP subsidies, continue to generate recurring demand for fleet replacement. Military contracts across NATO member states provide a stable, high-value revenue stream within the utility application category, insulating this segment from consumer spending cyclicality.

The Sports application segment is the fastest-growing at a CAGR of 7.1%, reflecting Europe's expanding recreational motorsport culture. Growing ORV racing events, including cross-country rallies, enduro championships, and regional off-road racing circuits, are fuelling demand for performance-grade ATVs and sport UTVs. The Recreation segment also shows healthy growth as lifestyle-driven consumers invest in off-road capable vehicles for weekend leisure. OEMs targeting the sports segment are increasingly launching limited-edition, high-performance models to capture premium pricing power.

Regional Insights and Trends

Germany Stands as Europe’s Powerhouse for Off-Road Vehicle Manufacturing And Demand

Germany commands over 30% of Europe's ORV market revenue in 2026, making it the undisputed regional leader by value. The German ORV market is estimated at approximately US$ 3.15 Billion in 2026, supported by strong production capacity, industrial demand, and a high-income consumer base. Germany's role as the EU's largest automotive manufacturer translates into deep ORV supply chain capabilities, enabling local production of key components including drivetrains, suspension systems, and vehicle electronics.

From a production standpoint, Germany hosts manufacturing and assembly facilities for several global ORV OEMs and Tier-1 suppliers, benefiting from its world-class precision engineering workforce. ORV sales are driven by three primary channels: agricultural institutional buyers (supported by CAP EU subsidies), defence procurement (Bundeswehr vehicle tenders), and premium consumer retail (Bavaria, Baden-Württemberg, and Saxony). Consumer trends indicate a growing appetite for connected UTVs with telematics and driver assistance features, preferences consistent with Germany's premium automotive culture.

The regulatory environment in Germany is characterised by strict TÜV certification requirements for commercial off-road vehicles and growing Länder-level restrictions on ORV operation in Natura 2000 protected zones. However, the German government's commitment to electric vehicle adoption, including dedicated subsidies under the Klimaschutzprogramm, is actively stimulating demand for electric ORV models, particularly in fleet and institutional procurement contexts. Competitive dynamics favour established multinational OEMs, with Polaris, Can-Am (BRP), and CFMOTO holding significant market presence. Investment trends indicate rising R&D spending on electric powertrains and digital platform integration among Germany-based ORV distributors.

France Emerges as Europe’s Fastest-Growing Off-Road Vehicle Market, Fueled by Outdoor Lifestyle Trends and Strong Policy Support

France is one of Europe's most strategically significant ORV markets, distinguished by its position as the fastest-growing country, with a CAGR of 7.5% through 2033. France's ORV market is valued at approximately US$ 1.6-1.8 billion in 2026 and is projected to exceed US$2.8 billion by 2033. France's strong adventure tourism industry, mountainous terrain, and proactive EV policy framework collectively position it as the most dynamic ORV growth market in Europe.

French production statistics indicate growing local assembly activity, particularly for electric ATV and UTV models by European-aligned manufacturers. Sales data from the Comité Français des Constructeurs et Importateurs de Motocycles et Véhicules à Moteur (CSIAM) indicate sustained growth in ATV and UTV registrations, with electric models gaining share annually. Key demand drivers include: the Alpine and Pyrenean adventure tourism ecosystem, precision viticulture (requiring compact UTVs in vineyards), and French Army vehicle procurement under LPM 2024-2030.

The French government's Bonus Écologique programme provides purchase subsidies for qualifying electric light vehicles, improving the economics of electric ORV adoption. Consumer trends indicate growing interest in premium, feature-rich recreational ORVs, particularly among the 35-55 age demographic with high disposable income. The competitive landscape features a mix of global OEMs (Polaris, BRP/Can-Am, Honda) and specialist importers. Distribution is increasingly digital, with OEMs investing in e-commerce configurator tools and virtual showrooms. France's trajectory makes it a critical test market for the launch of next-generation electric ORVs targeting European consumers.

Competitive Landscape

The Europe Off-Road Vehicles market exhibits a moderately consolidated competitive structure, with the top five players Polaris Inc., BRP (Can-Am), Honda Motor Co., Yamaha Motor Co., and Kawasaki collectively accounting for an estimated 55-65% of total market revenue. The remaining share is distributed among regional specialists, Chinese entrants (CFMOTO, Segway Powersports), and niche electric-focused startups. Market leadership is sustained through brand equity, dealer network depth, and continuous product innovation.

Dominant strategic themes among market leaders include electrification leadership, distribution network expansion, and vertical integration in digital services. Key differentiators include proprietary battery management systems, dealer experience programmes, and OEM-linked telematics platforms. Emerging models include ORV-as-a-service subscriptions and fleet electrification partnerships with agricultural cooperatives.

Key Industry Developments:

- January 9, 2026 - Jeep® showcased major product developments at the Brussels Motor Show 2026, including the debut of the Avenger Black Edition, the all-new Compass lineup, and the advanced Wagoneer S, reinforcing its expanding electrified SUV portfolio in Europe.

- In November, 2025, The rugged Denza B5 plug-in hybrid SUV was confirmed for a UK launch in 2026. Positioned as a rival to the Land Rover Defender and Toyota Land Cruiser, the off-road-focused SUV is expected to be priced between £60,000-£70,000 and was recently named “Best Prospect” by Car of the Year judges.

- In November 2025, The production-spec Jeep Recon, the brand’s first fully electric “Trail Rated” 4×4, was officially revealed ahead of its public debut at the 2025 Los Angeles Auto Show. The model is scheduled to arrive in the UK and European markets in late 2026.

- In November 19, 2025, Toyota launched the 2026 Hilux double-cab pickup in Europe, responding to strong consumer demand and confirming upcoming battery electric (BEV) and hydrogen fuel-cell variants.

- In November 10, 2025, Toyota announced the all-new Hilux lineup, including the first-ever battery electric version of its iconic pickup model.

- In November 2025, the German Army placed an order for 1,500 Wolf 2 off-road vehicles, with an agreement allowing expansion of the contract to up to 5,800 units.

- In November 2023, Polaris began delivering the first shipments of its fully electric RANGER XP Kinetic to dealerships across Europe, marking a significant step in the region’s electric utility vehicle segment.

Companies Covered in Europe Off-road Vehicle Market

- MUNRO

- SHERP

- Polaris Inc.

- Yamaha Motor Co., Ltd.

- Honda Motor Co., Ltd.

- Kawasaki Heavy Industries

- CFMOTO

- Kubota Corporation

- Deere & Company (John Deere)

- Textron Inc. (Arctic Cat)

- KYMCO

- Suzuki Motor Corporation

- Daedong Corporation (KIOTI)

- Mahindra & Mahindra Ltd.

- Corvus UTV

- Land Rover

- Ineos Grenadier

- Dacia Duster

- Toyota

- Other Market Players

Frequently Asked Questions

The Europe Off-road Vehicle market is estimated to be valued at US$ 10.5 Bn in 2026.

The key demand driver for the Europe Off-Road Vehicle market is the growing adoption of utility and multifunctional vehicles across agriculture, forestry, and industrial sectors.

In 2026, Germany will dominate the market with an exceeding 30% revenue share in the European off-road vehicle market.

Among propulsion types, gasoline has the highest preference, capturing beyond 45% of the market revenue share in 2026, surpassing other propulsion types.

MUNRO, SHERP, Polaris Inc., Yamaha Motor Co., Ltd., Honda Motor Co., Ltd., Kawasaki Heavy Industries, CFMOTO, Kubota Corporation, and Deere & Company (John Deere). There are a few leading players in the Europe Off-road Vehicle market.