- Nutraceuticals & Functional Foods

- Europe Oat Drinks Market

Europe Oat Drinks Market Size, Share, Growth, and Regional Forecast, 2025 to 2032

Europe Oat Drinks Market By Flavor (Natural, Vanilla, Chocolate, Strawberry, Others), Nature (Organic, Conventional), Packaging (Cartons, Bottles, Jar, Others), Distribution Channel (Hypermarket & Supermarket, Convenience Store, Online Retail, Others), and Country Analysis from 2025 to 2032

Europe Oat Drinks Market Share and Trends Analysis

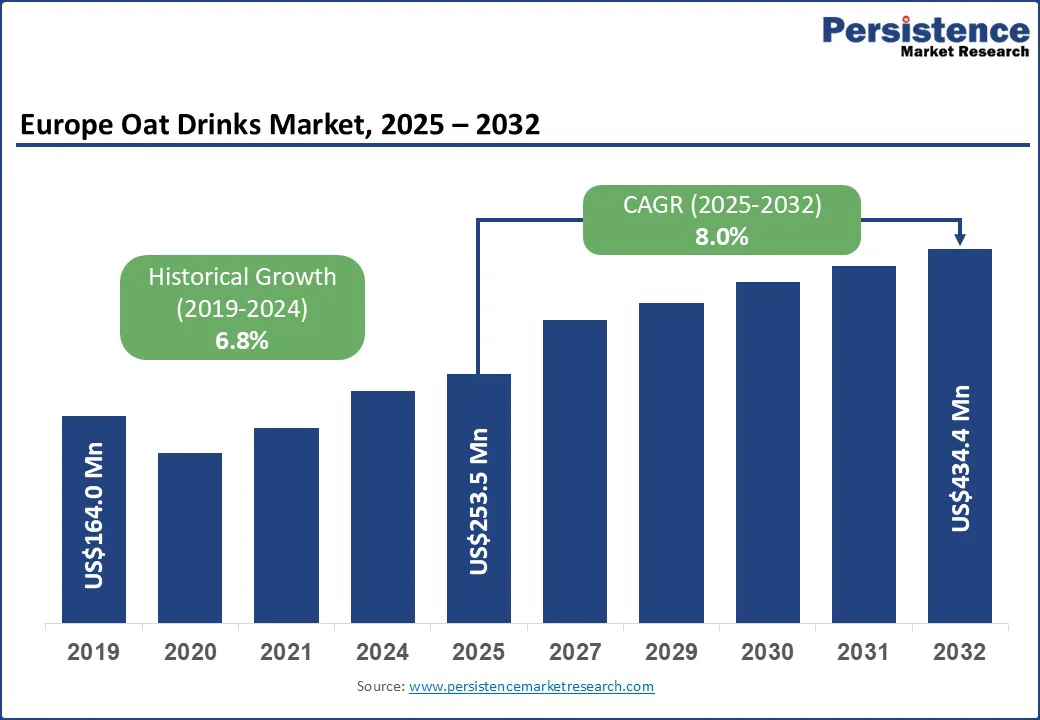

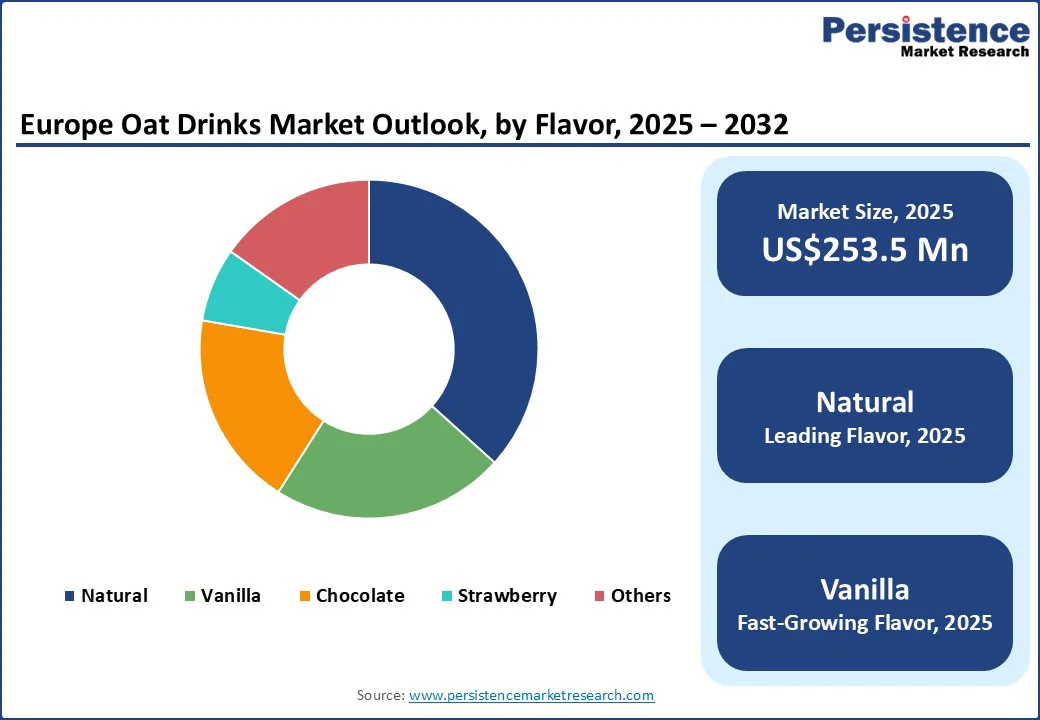

The Europe oat drinks market size is likely to be valued at US$253.5 Mn in 2025 and is expected to reach US$434.4 Mn by 2032, growing at a CAGR of 8.0% during the forecast period from 2025 to 2032, driven by rising consumer demand for plant-based, lactose-free, and sustainable dairy alternatives.

Growing health awareness, increasing cases of lactose intolerance, and the adoption of vegan and flexitarian diets are key factors fueling the Europe oat drinks market expansion.

Key Industry Highlights

- Leading Packaging Segment: Cartons, holding approximately 51.2% market share in 2025, supported by strong retail penetration, cost efficiency, wide availability in supermarkets, and consumer preference for recyclable, eco-friendly formats.

- Fastest-growing Distribution Channel Segment: Online Retail, fueled by rising e-commerce adoption, subscription models, direct-to-consumer brand strategies, and growing digital grocery platforms across Europe.

- Investment Plans: Flavor Innovation, focusing on vanilla and functional blends, with support from consumer demand for fortified options, cross-border R&D in taste and texture improvement, and multi-million-euro investments by leading plant-based beverage brands.

- Leading Nature: Conventional dominates with over 63.5% of market revenue, supported by strong café culture, widespread use in premium coffee chains, and consumer preference for oat drinks as the go-to non-dairy milk in specialty beverages.

| Key Insights | Details |

|---|---|

| Europe Oat Drinks Market Size (2025E) | US$253.5 Mn |

| Market Value Forecast (2032F) | US$434.4 Mn |

| Projected Growth (CAGR 2025 to 2032) | 8.0% |

| Historical Market Growth (CAGR 2019 to 2024) | 6.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Health & Dietary Preferences

Health and dietary preferences are a major driver of the Europe oat drinks market, with statistics highlighting this shift. Around 5-15% of Europeans are lactose intolerant, leading many to seek lactose-free options such as oat drinks that are easier to digest. Surveys also show that 51% of Europeans are actively reducing their consumption of meat and milk, with nearly 47% citing health reasons as the main motivation.

In addition, nutrition professionals across Europe widely recognize fortified oat drinks as a healthy choice; for example, in some countries, more than 90% of dietitians agree they can be part of balanced diets. Consumer habits are also changing rapidly, with about 17% of Europeans consuming plant-based milk, including oat drinks, four or more times per week, while another 11% consume them one to three times weekly. These patterns show that oat drinks are no longer niche, but a mainstream health-driven alternative.

Higher Production & Retail Costs

Higher production and retail costs are a significant restraint in the Europe oat drinks market, squeezing margins and making consumer prices less competitive. Food inflation across the EU has remained elevated; for example, by mid-2025, the cost of food in the EU was rising at about 3.9% year-on-year, compared to long-run averages near 2.7%. This persistent inflation results from multiple cost inputs, raw agricultural materials (oats), energy, labor, packaging that all feed into production.

Meanwhile, agricultural commodity price indices show sizable volatility for cereals, including oats, and for inputs such as seeds, pesticides, and farm labor, raising costs upstream. On the retail side, differences in food price levels across countries are stark. In recent studies, some EU member states show supermarket food baskets costing 30-50% more than in lower-cost countries. These differences make oat drinks particularly sensitive to cost pressures, since they often carry a “premium” over traditional dairy. When input and operational expenses rise (transport, packaging), producers either absorb the costs, squeezing margins, or pass them on, making oat drinks expensive relative to substitutes.

Product Innovation and Diversification

Product innovation and diversification present significant opportunities for the Europe oat drinks market. The market has witnessed a surge in demand, with oat drinks showing the largest growth and being the most commonly consumed among plant-based beverages in the U.K. This growth is driven by consumer preferences for healthier and more sustainable alternatives to dairy products.

Companies are responding by introducing a variety of oat drink products, including flavored options, fortified versions with added vitamins and minerals, and barista-friendly formulations designed to froth well for coffee applications. Such innovations cater to diverse consumer tastes and dietary needs, expanding the market reach.

Additionally, the increasing availability of oat drinks in various retail channels, including supermarkets, health food stores, and online platforms, enhances consumer access and convenience. These factors contribute to the continued growth and diversification of the market.

Category-wise Analysis

Flavor Insights

Natural-flavored oat drinks lead the European market with a 36.7% share in 2025, due to their alignment with consumer preferences for clean-label, minimally processed products. This preference is further supported by the clean label trend, where approximately 61% European consumers favor products made with natural and botanical flavor ingredients, associating them with better environmental sustainability.

Brands such as Lima and The Bridge offer oat drinks that are organic, lactose-free, and contain no added sugars, emphasizing their natural taste. In the U.K., oat milk has become increasingly popular, with sales showing noticeable growth over the past year, reflecting rising consumer preference for plant-based and healthier alternatives, driven by its perceived health benefits and superior taste.

These factors collectively underscore the dominance of natural-flavored oat drinks in the European market.

Packaging Insights

Carton packaging leads the Europe oat drinks market with a 51.2% share in 2025, as it aligns with consumer priorities for sustainability, convenience, and practicality. Cartons are often made from renewable or recyclable materials, which appeals to environmentally conscious shoppers and supports Europe’s broader goals for reducing packaging waste.

They also provide extended shelf life for oat drinks, allowing products to remain fresh without refrigeration, making them convenient for both retailers and consumers.

Additionally, cartons are lightweight, easy to store, and simple to pour from, enhancing the user experience at home. With increasing awareness about sustainable packaging and a preference for products that minimize environmental impact, cartons have naturally become the dominant packaging choice, supporting both market growth and consumer satisfaction in the European oat drinks segment.

Country Insights

Germany Oat Drinks Market Trends

Germany’s oat drinks market has been steadily growing, driven by increasing consumer interest in plant-based and sustainable alternatives. Rising health consciousness has prompted many

Germans to reduce dairy consumption, with per capita cow’s milk intake declining from around 60 kg in the mid-1990s to approximately 46 kg in 2023, reflecting a shift toward plant-based options. Environmental awareness is also influencing choices, as consumers seek products with lower carbon footprints and more sustainable production practices.

Surveys show that nearly four out of ten German households now include plant-based milk in their regular purchases, with oat drinks being the most popular due to taste, creaminess, and versatility. Widespread availability in supermarkets, health stores, and cafés further supports this growth, making oat drinks a mainstream, convenient, and environmentally conscious choice for German consumers.

Competitive Landscape

The Europe oat drinks market is growing as companies innovate with flavors, fortified and barista-friendly formulations, and sustainable packaging. Established brands enhance taste and nutrition, while emerging players target niche segments such as organic and low-sugar options. Strategic partnerships, café collaborations, and expanded retail and e-commerce availability strengthen competitiveness, driving wider consumer adoption across Europe.

Key Industry Developments

- In September 2025, Organic Valley introduced two new beverages made with organic oats sourced from its family farms, emphasizing sustainability and local sourcing. The launch aimed to expand the company’s plant-based offerings while highlighting the use of organic ingredients. This initiative showcased Organic Valley’s commitment to innovation in the oat drinks segment and provided consumers with nutritious, eco-friendly beverage options.

- In June 2025, Country Delight launched its new oats beverage, offering a wholesome and affordable plant-based alternative to traditional dairy. The product aimed to cater to health-conscious consumers seeking nutritious and sustainable options. By introducing this beverage, Country Delight expanded its portfolio in the plant-based segment, making oat-based drinks more accessible to a wider audience.

- In April 2025, U.K.-based plant-based brand Minor Figures launched a new line of colorful, flavored oat drinks, reportedly a first in the category.

- In March 2025, Danone’s Alpro announced a major investment in the U.K. by switching to British-grown oats for its products. The move aimed to support local agriculture, reduce the brand’s carbon footprint, and strengthen supply chain sustainability.

Companies Covered in Europe Oat Drinks Market

- Oatly Group AB

- Alpro (Danone)

- Emmi (Beleaf)

- Velike! (Black Forest Nature GmbH)

- Minor Figures

- share GmbH

- Oatstanding

- Naarmann

- Nutrigold

- OATS UP

Frequently Asked Questions

Europe oat drinks market is projected to be valued at US$253.5 Mn in 2025.

Rising health awareness, lactose intolerance, veganism, sustainability concerns, and clean-label preferences drive Europe’s growing oat drinks market demand.

Europe oat drinks market is poised to witness a CAGR of 8.0% between 2025 and 2032.

Product innovation, flavored and fortified oat drinks, sustainable packaging, e-commerce expansion, and café collaborations drive key opportunities in Europe.

Major players in the Europe oat drinks market are Oatly Group AB, Alpro (Danone), Emmi (Beleaf), Velike! (Black Forest Nature GmbH), Minor Figures, and share GmbH.