- Food Packaging

- Europe Conductive Polymer Coatings Market

Europe Conductive Polymer Coatings Market Size, Share, and Growth Forecast for 2025 - 2032

Europe Conductive Polymer Coatings Market By Polymer Type (Polyaniline (PANI), Polypyrrole (PPy), Polythiophene (PEDOT & derivatives), and Others), Application (Electronics, Energy Storage, Smart Textiles) and Regional Analysis for 2025 - 2032

Europe Conductive Polymer Coatings Market Size and Trends Analysis

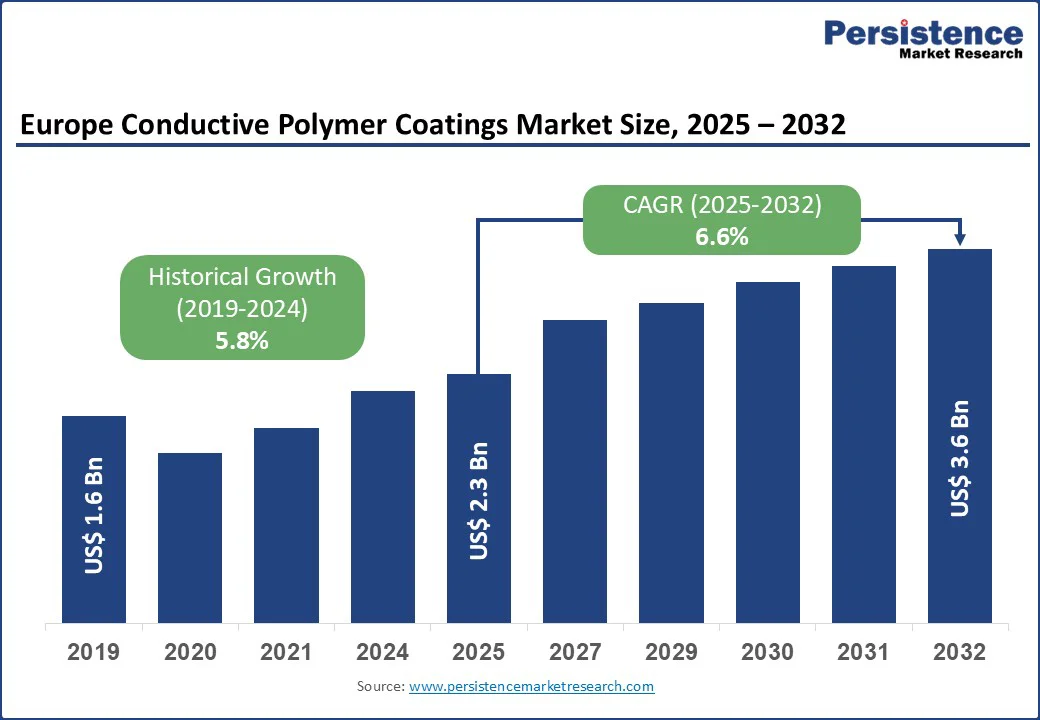

Europe Conductive Polymer Coatings market size is likely to be valued at US$ 2.3 Bn in 2025 and projected to reach US$ 3.6 Bn with a CAGR of 6.6% in the forecast period between 2025 and 2032. due to the rising adoption in electronics, automotive, and energy storage applications, supported by stringent EU regulations promoting sustainable and low-VOC materials.

Key Industry Highlights:

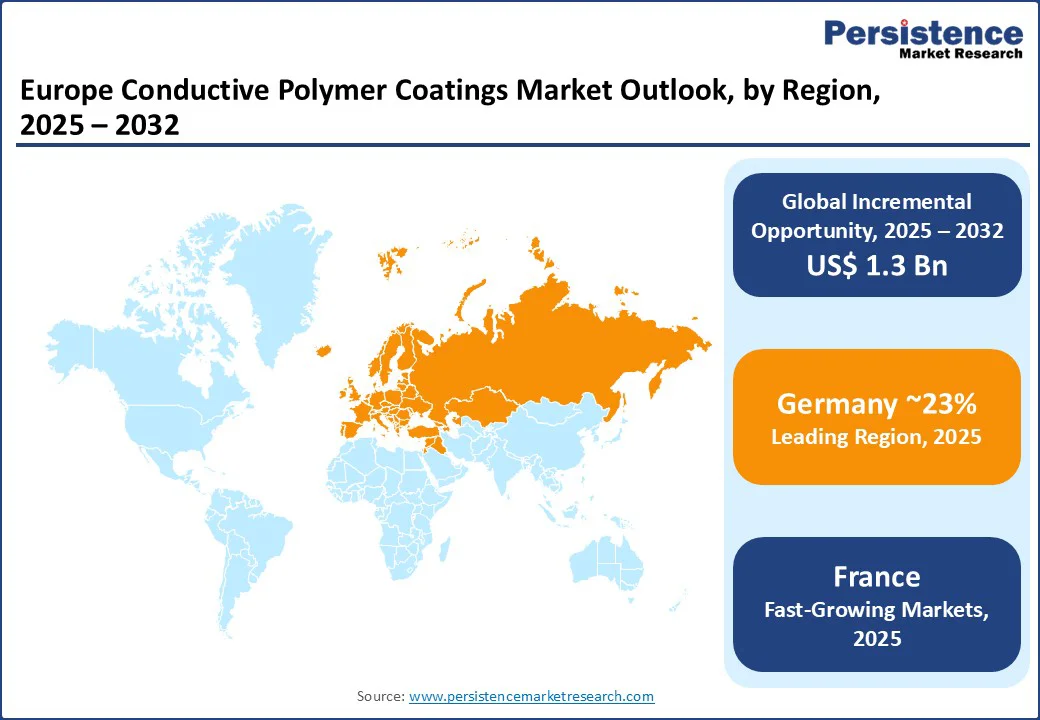

- Leading Country: Germany leads the regional market with a 23% share, driven by government-funded surface engineering research and strong adoption in the automotive and electronics industries.

- Dominant Application: Electronics is the leading application category, expanding at a 7.2% CAGR through 2032, supported by strong EU investments in flexible and printed electronics.

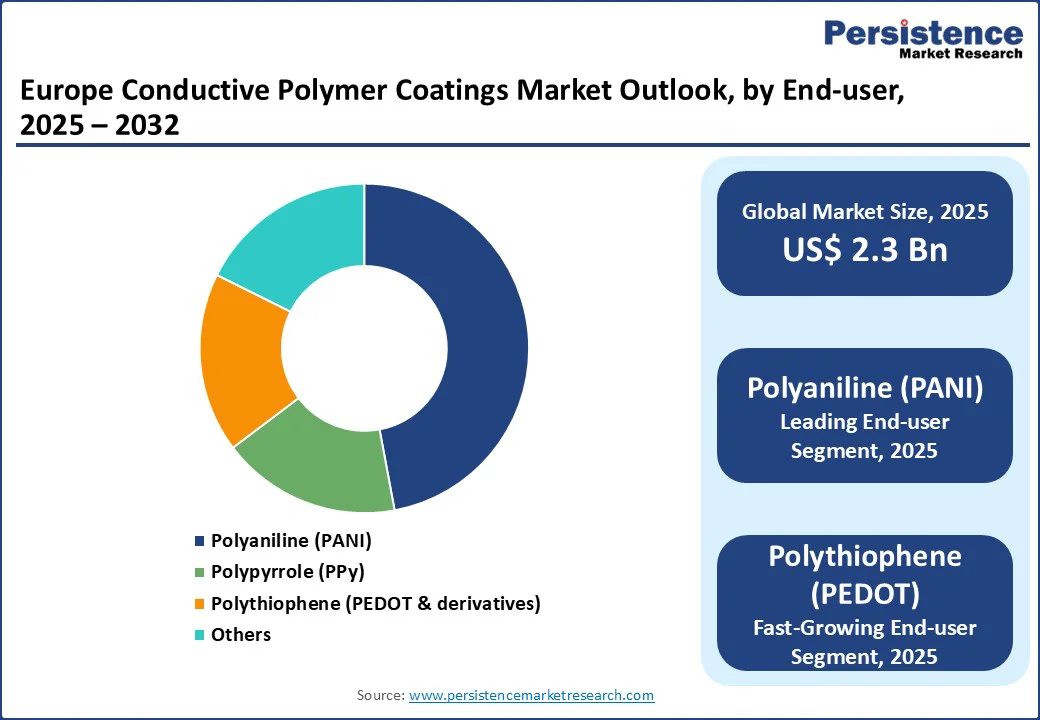

- Leading Polymer Type: Polyaniline (PANI) holds a 40% market share in Europe in 2025, reinforced by its use in EMI shielding, corrosion protection, and energy storage applications.

- Strategic Aspects: Regulatory restrictions under EU REACH on solvents like N-Methyl-2-pyrrolidone (NMP) are raising compliance costs, pushing manufacturers toward water-borne PEDOT PSS and low-VOC formulations.

|

Global Market Attribute |

Key Insights |

|

Europe Conductive Polymer Coatings Market Size (2025E) |

US$ 2.3 Bn |

|

Market Value Forecast (2032F) |

US$ 3.6 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.8% |

Market Dynamics

Driver - EV Electronics Densification Boosts EMI/ESD Coating Demand

"Europe’s accelerated electrification is a prime demand catalyst for conductive polymer coatings used for EMI shielding, antistatic and ESD control, sensors, and capacitors across automotive electronics and battery systems. The Europe Electric Vehicle Market is expanding rapidly, with battery-electric cars capturing 15.6% of EU registrations by mid-2025, up from about 12.5% a year earlier. This signals a larger installed base of in-vehicle power electronics and wiring that require lightweight, corrosion-resistant coatings compared to metal meshes or carbon-filled paints.

In parallel, leading European suppliers have scaled PEDOT:PSS platforms for antistatic and conductive protective layers in displays, capacitors, and printed circuitry aligned with vehicle HMI, ADAS, and interior electronics. This convergence of higher BEV adoption and broader electronics per vehicle is expected to drive demand for PEDOT:PSS, PANI, and PPy coatings in Automotive & Aerospace and Electronics applications, strengthening mid-term growth prospects for European producers.

Restraint - REACH Solvent Restrictions Raise Compliance Costs

A key restraint in the Europe conductive polymer coatings market is regulatory stringency around processing solvents, particularly N-Methyl-2-pyrrolidone (NMP), which has been widely used in dispersions and coating steps for conductive polymers. Under REACH Annex XVII (Entry 71), NMP use in the EU is restricted and subject to strict worker exposure limits, monitoring, and risk management measures.

For coaters and OEMs, this translates into additional engineering controls, training, and documentation or reformulation toward alternative solvents and aqueous systems. These requirements add time and cost to qualification cycles in Electronics, Energy Storage, and Smart Textiles applications. While many suppliers are advancing water-borne PEDOT:PSS and low-VOC systems, the compliance burden continues to slow scale-up and deters smaller converters from entering, moderating short-term growth despite robust downstream demand.

Opportunity - Surge in EU-Backed Smart Textiles and Printed Electronics

Smart textiles, medical & healthcare represent a strong opportunity as Europe mobilizes funding and industry alignment for flexible and printed electronics, where PEDOT:PSS, PANI, and PPy coatings enable breathable and washable conductivity. The Organic and Printed Electronics Association (OE-A) reports that 77% of members expect printed-electronics growth in 2025, with a 19% revenue increase forecast, reflecting rising demand in sensors for automotive, medical, sports, and building applications.

Horizon Europe is financing e-textile and flexible-electronics projects such as UPWEARS and STELEC while dedicating multi-million-euro calls to advanced materials for conformable electronics. This support creates pilot-to-scale pathways and encourages adoption in the healthcare and apparel industries. EURATEX also projects the EU e-textiles market to reach around €1.5 Bn in 2025, highlighting significant commercialization potential for conductive polymer coatings in garments, wearables, and patient monitoring.

Category-wise Analysis

Polymer Type Insights

Polyaniline is the dominant conductive polymer coating type with 40% share in 2025 in Europe, valued for its high conductivity, chemical stability, and ease of synthesis. It accounts for a significant share of the market, driven by its widespread use in antistatic finishes, electromagnetic interference shielding, and corrosion protection for printed circuit boards and electronic packaging.

European research programs under Horizon Europe are also supporting projects that enhance polyaniline’s functionality in sustainable electronics and energy storage systems. These factors consolidate PANI’s leadership position across Electronics, Energy Storage, and Automotive segments, making it the most reliable and scalable conductive polymer choice in Europe.

Application Type Insights

Electronics segment emerges as the largest and fastest-growing end-use category with 7.2% CAGR through 2032 in the Europe conductive polymer coatings market. Conductive coatings are increasingly adopted in flexible electronics, sensors, capacitors, and printed circuitry, where they offer lightweight protection, EMI shielding, and antistatic performance.

Supported by EU innovation initiatives under Horizon Europe, the region is investing heavily in printed and wearable electronics that integrate PEDOT:PSS and PANI coatings. The rising need for miniaturization, device durability, and sustainable materials is further boosting demand. With Europe at the forefront of advanced electronics and semiconductor innovation, the Electronics segment is set to remain the primary growth driver for conductive polymer coatings.

Regional Insights and Trends

Germany Conductive Polymer Coatings Market Trends

Germany holds the largest share of 23% in the European conductive polymer coatings market. Germany is advancing strongly in conductive polymer coatings through cutting-edge surface engineering research. The Leibniz Institute of Surface Engineering (IOM) in Leipzig, funded by federal and state government programs, is pioneering thin-film and coating technologies, including non-thermal and functional surface treatments relevant to conductive polymers.

Germany’s broader industrial innovation policies and its focus on sustainable materials in the automotive and electronics sectors are driving businesses to adopt lightweight, corrosion-resistant conductive coatings as alternatives to traditional metallic layers. This synergy between government-supported R&D and strong OEM demand positions Germany at the forefront of applied conductive polymer innovation in Europe.

United Kingdom Conductive Polymer Coatings Market Trends

In the United Kingdom, commercial adoption of advanced coatings is accelerated through government-supported projects. A notable example is the CeraBEV project, led by Zircotec in collaboration with Cranfield University, which focuses on developing coatings for electric vehicle battery systems.

These solutions offer enhanced EMI shielding, electrical insulation, and thermal protection in lightweight designs, aligning with the UK’s electrification goals. Such initiatives reflect national priorities toward electric vehicle safety and efficiency. With strong public funding and industry-academia collaboration, the UK market is evolving rapidly and demonstrating leadership in developing conductive polymer and hybrid coating solutions for high-performance applications.

France Conductive Polymer Coatings Market Trends

France’s conductive polymer coatings market resembles fastest growth with 7% CAGR through 2032 and is gaining momentum, supported by public incentives and growing demand from consumer electronics and healthcare sectors. Government programs, including R&D tax breaks and funding schemes, are encouraging innovation and technology transfer in advanced materials.

France is also experiencing steady growth in smart-device and connected-electronics adoption, with the smart home solutions market revenue projected to reach approximately US$ 3.5 billion by 2025. This surge in connected consumer products is creating demand for conductive coatings in sensors, antistatic layers, and EMI-protected components. The combination of favorable policy measures and robust end-market consumption underscores France’s rising importance in the European conductive polymer coatings landscape.

Competitive Landscape

Europe conductive polymer coatings market is characterized by strong competition among global and regional players focused on innovation, sustainability, and advanced material performance. Key companies such as Heraeus Holding, Evonik Industries, BASF SE, Merck KGaA, and Henkel AG & Co. KGaA are leading the market with investments in conductive polymers like PEDOT:PSS, polyaniline, and polypyrrole.

Their strategies include expanding water-borne and low-VOC formulations to meet REACH compliance, developing high-performance coatings for electronics and energy storage, and collaborating with automotive and aerospace OEMs to deliver lightweight EMI shielding solutions. These supplier-side initiatives are shaping market development, strengthening Europe’s position in next-generation conductive coatings.

Latest Industry Developments:

- In June 2025, Evonik Industries expanded production of its water-borne PEDOT:PSS conductive dispersions at its German coating materials facility. This ramp-up was aimed at meeting rising EU demand for low-VOC, environmentally compliant conductive coatings in automotive and smart textile applications, reinforcing Evonik’s supply leadership.

- In March 2025, Heraeus Epurio and Japanese startup AI Silk introduced LEAD SKIN® smart textiles coated with Clevios™ PEDOT, enabling conductive fibers for washable, wearable garments that can monitor heartbeat and stimulate muscles. This innovation bolsters Heraeus’s leadership in conductive polymer applications for smart textiles, reinforcing its role in the European market for wearable electronics.

Companies Covered in Europe Conductive Polymer Coatings Market

- Heraeus Holding GmbH

- Covestro AG

- BASF SE

- AkzoNobel N.V.

- Solvay S.A.

- Henkel AG & Co. KGaA

- Evonik Industries AG

- PolyOne Europe GmbH

- Nanocyl S.A.

- Clariant AG

- AGFA-Gevaert N.V.

- DSM

- Arkema S.A.

- Conductive Compounds Ltd

- Merck KGaA

Frequently Asked Questions

Europe conductive polymer coatings market is valued at US$ 2.3 billion in 2025 and is projected to grow at a CAGR of 6.6% to reach US$ 3.6 billion by 2032.

Growth is driven by rising adoption in electronics, automotive, and energy storage applications, supported by EU sustainability regulations and the electrification of vehicles across the region.

Strict solvent regulations under EU REACH, particularly restrictions on N-Methyl-2-pyrrolidone, raise compliance costs and extend qualification cycles, slowing short-term market expansion.

Polyaniline dominates the Europe conductive polymer coatings market with around 40% share in 2025, driven by its conductivity, stability, and use in EMI shielding and corrosion protection.

Electronics segment is the largest and fastest-growing application area, expanding at a 7.2% CAGR, fueled by demand for flexible electronics, sensors, and printed circuitry.

Germany leads with a 23% market share, followed by strong growth in the United Kingdom and France, supported by government-backed R&D programs, EV innovation, and rising demand for connected consumer electronics.