- Electric Mobility

- Europe Electric Vehicle Market

Europe Electric Vehicle Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Europe Electric Vehicle Market by Vehicle Type (Passenger Vehicle, Light Commercial Vehicle, Heavy Commercial Vehicle), Propulsion Type (BEV, HEV, PHEV, and FCEV), Range (Up to 150 Km, 151 to 300 Km, 301 to 500 Km, above 500 Km), and Regional Analysis for 2026 - 2033

Europe Electric Vehicle Market Size and Trends Analysis

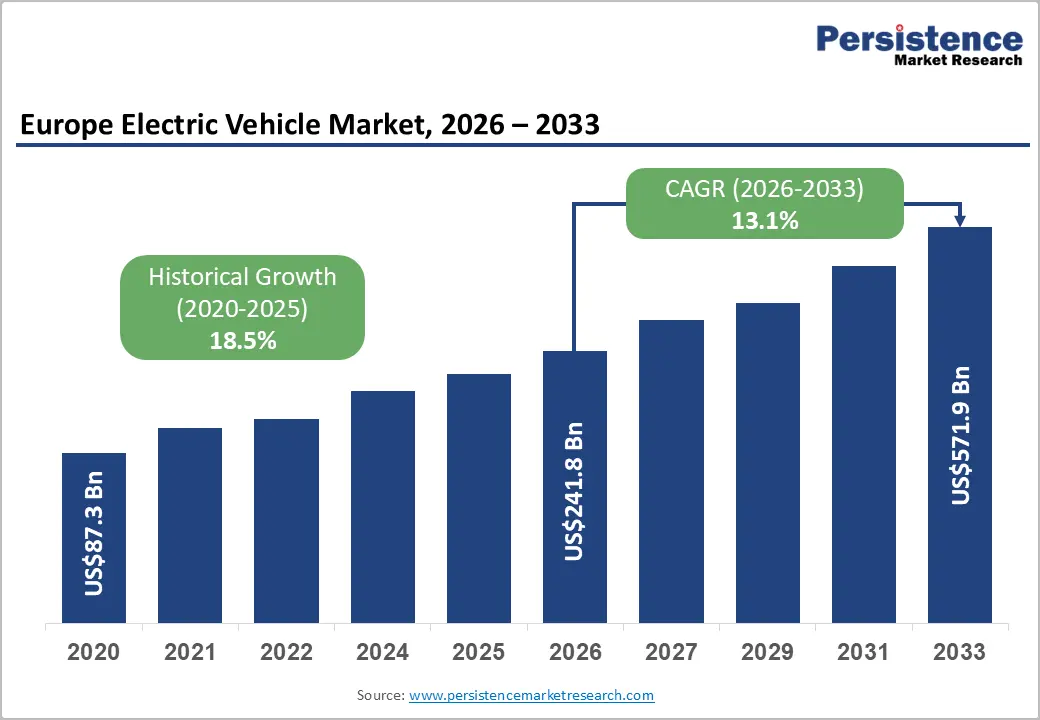

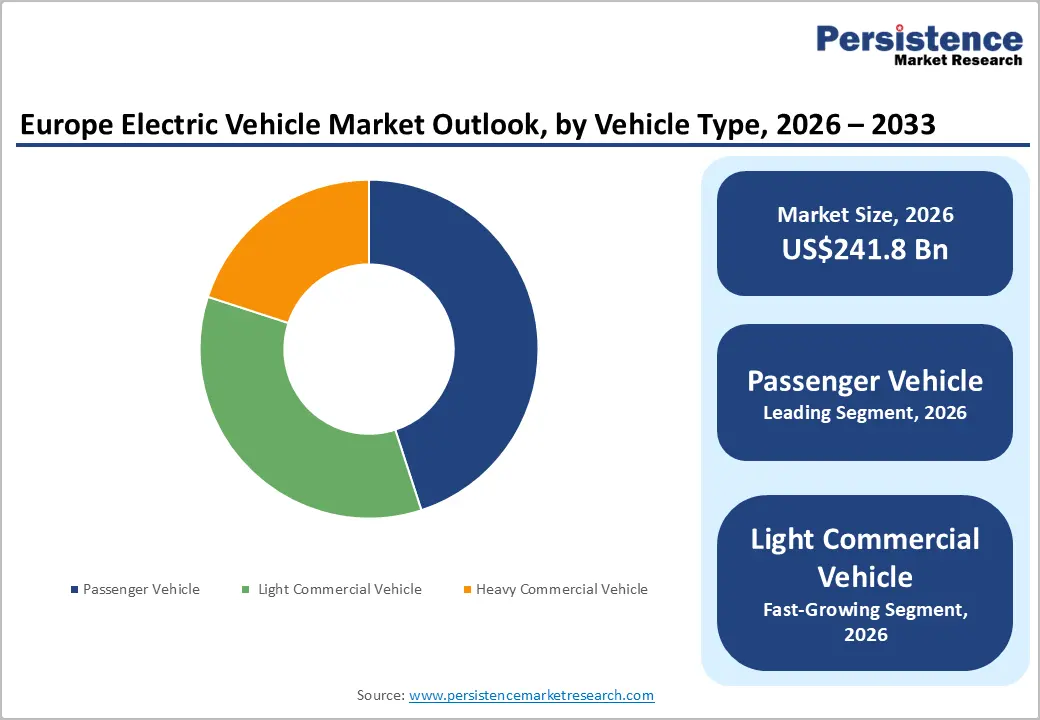

The Europe electric vehicle market size is likely to be valued at US$ 241.8 billion in 2026 and is projected to reach US$ 571.9 billion by 2033, registering a strong CAGR of 13.1% from 2026 to 2033, following an accelerated historical growth rate of 18.5% during 2020 - 2025.

The market represents the full ecosystem of battery-powered road transportation across Europe, covering Battery Electric Vehicles (BEVs), Plug-in Hybrid Electric Vehicles (PHEVs), and Hybrid Electric Vehicles (HEVs) across passenger, commercial, and specialty segments. It spans vehicle production, sales, and adoption, alongside critical enabling infrastructure such as battery systems, charging networks, power electronics, and vehicle software platforms that collectively support large-scale electrification.

Regionally, Germany maintained its position as Europe's largest BEV market, supported by strong consumer incentives and a broad portfolio of electric models. France recorded solid growth, driven by rising public awareness and rapid expansion of charging infrastructure. The Netherlands and Sweden continued to post above-average BEV penetration rates, driven by supportive policy frameworks and consumer alignment with zero-emission mobility. Southern European markets such as Spain and Italy also reported notable gains, progressively narrowing the adoption gap with Northern and Western Europe.

Key Industry Highlights:

- Battery Recycling Momentum: As end-of-life EV batteries rise, investments in recycling technologies and circular-economy models are accelerating across Europe.

- Recycling Leadership Europe: Germany and Sweden are leading battery recycling capacity, enabling efficient recovery of lithium, cobalt, and nickel while reducing import dependence.

- Second-Life Batteries: Repurposed EV batteries are emerging as cost-effective energy storage solutions for residential, commercial, and renewable energy applications.

- Rural Charging Expansion: Expanding charging infrastructure in rural and underserved regions is becoming a critical lever for widening EV adoption beyond major cities.

- Government Infrastructure Support: France and Italy are advancing rural EV charging through public-private initiatives, mobile chargers, and solar-powered stations.

- Passenger Vehicle Dominance: Passenger EVs account for over 45% of the market, supported by subsidies, emissions regulations, and strong consumer demand.

- Norway Adoption Benchmark: Norway continues to lead Europe, with more than 80% of new vehicle sales being electric.

- Optimal Range Preference: The 301-500 km range segment leads the market, offering the best balance between affordability, usability, and charging convenience.

- BEV Market Leadership: Battery-electric vehicles dominate long-term growth, with OEMs like Volkswagen scaling platforms and forging partnerships.

- Competitive Intensity Rising: BYD overtaking Tesla in registrations highlights intensifying price competition and market restructuring.

| Key Insights | Details |

|---|---|

| Electrical Vehicle Market Size (2026E) | US$ 241.8 Bn |

| Market Value Forecast (2033F) | US$ 571.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 13.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 18.5% |

Market Dynamics

Key Growth Drivers

Regulatory Support and Incentives Propel Electric Vehicle Adoption in Europe

The regulatory framework in Europe plays a crucial role in driving the adoption of electric vehicles (EVs), with governments setting stringent emission targets and offering financial incentives to facilitate the shift from internal combustion engine vehicles. Countries such as Germany and France are leading this initiative, implementing policies aimed at promoting sustainable transportation solutions.

Germany's ambitious strategy to phase out the sale of new fossil fuel cars by 2031 demonstrates a strong commitment to lowering carbon emissions and bolstering the EV market. In France, the “Bonus écologique” program offers financial bonuses to consumers who purchase electric vehicles, significantly lowering the total cost of ownership. Such initiatives make EVs more appealing, especially to budget-conscious buyers, effectively driving demand within the market.

As regulations tighten, they create a fertile environment for EV manufacturers to thrive and innovate. The combination of regulatory pressure and generous incentives fosters a competitive landscape encouraging both manufacturers and consumers to prioritize electric mobility. This dynamic not only contributes to a green environment but also positions Europe as a global leader in the EV market.

Infrastructure Development Remains a Key Driver for Market Growth

Infrastructure development is crucial for the sustained growth of the European electric vehicle market, with governments and private sectors investing significantly in charging networks. The UK, for instance, has committed to significantly expanding its public charging infrastructure, aiming to install thousands of new charging points over the forecast period. This commitment addresses one of the most significant barriers to EV adoption, like range anxiety.

By ensuring convenient access to charging stations, the UK is paving the way for broader acceptance of electric vehicles. The Netherlands has positioned itself as a leader in charging infrastructure, with one of the highest charging point densities globally. This comprehensive network not only serves existing electric vehicle (EV) owners but also attracts potential consumers to explore electric mobility options.

The proactive strategy adopted by the Netherlands illustrates how a strong infrastructure can significantly enhance the attractiveness of EVs, making them a practical choice for daily use. Moreover, as charging technology advances, the introduction of ultra-fast charging stations is further enhancing convenience for EV users. This development allows drivers to recharge their vehicles quickly, significantly reducing downtime and encouraging more people to switch to electric. As infrastructure continues to expand and evolve, it will play a pivotal role in shaping the future of the EV market in Europe, ultimately supporting the region's sustainability goals.

Accelerating electrification in industrial and energy systems

The shift toward electrified, digitally controlled industrial and energy infrastructure is a primary growth engine for the Electric Vehicle market. Governments and utilities are investing heavily in smart grids, renewable integration, and power quality monitoring, which depend on accurate current sensing for protection, billing, and grid stability. Industrial automation, including motor drives, variable frequency drives, and robotics, requires high-precision Electrical Vehicles to optimize efficiency and prevent equipment failures. As global electricity demand continues to grow in line with GDP and urbanization trends, and as industries pursue energy efficiency and predictive maintenance, demand for reliable, isolated Electrical Vehicles in medium- and high-voltage systems will continue to expand, supporting the uplift from a 3.6% historical CAGR to 5.1% going forward.

Market Restraining Factors

High Initial Purchase Price of Electric Vehicles

The high upfront cost of electric vehicles relative to traditional internal combustion engine vehicles may hinder EV sales in Europe. While government incentives help offset costs, many consumers remain deterred by the upfront costs of EVs. For instance, even with subsidies, the price of popular models can exceed the budgets of average consumers, particularly in countries like Germany and France. This financial barrier hampers widespread adoption limiting the Europe electric vehicle market growth potential.

Limited Charging Infrastructure in Rural Areas Hinders EV Adoption

Limited charging infrastructure poses a significant challenge for the Europe electric vehicle market. Despite efforts to expand charging networks, many regions, particularly rural areas, still lack sufficient charging stations. This scarcity can lead to range anxiety among potential buyers, discouraging them from switching to electric vehicles. For example, while urban centers in the UK and the Netherlands boast robust charging networks, rural consumers often face difficulties in accessing charging points, hindering the overall growth of the EV market in these countries.

Electrical Vehicle Market Trends and Opportunities

Expansion of Battery Recycling and Second-Life Applications

A significant futuristic opportunity in the European electric vehicle market lies in the expansion of battery recycling and second-life applications. As the number of EVs on the road increases, so does the volume of used batteries that require sustainable disposal or repurposing.

Companies are increasingly investing in innovative recycling technologies to recover valuable materials like lithium, cobalt, and nickel, which are essential for new battery production. Countries such as Germany and Sweden are already leading the way in establishing efficient battery recycling facilities that not only support environmental sustainability but also foster a circular economy for battery materials.

The concept of second-life applications for EV batteries presents another lucrative opportunity. Used batteries can be repurposed for energy storage in residential and commercial settings, supporting the integration of renewable energy. For example, businesses can use these batteries to store solar energy, providing a reliable power source during peak demand times.

As Europe continues to push for sustainability, the development of robust battery recycling and second-life markets will be pivotal in enhancing the overall EV ecosystem.

Growth in Charging Infrastructure for Rural Areas

The growth of charging infrastructure, especially in rural and underserved regions, presents a significant opportunity for the European electric vehicle (EV) market. As urban areas become saturated with EVs, expanding charging networks into rural locales can significantly enhance EV adoption rates.

Governments and private companies are beginning to recognize this need and are likely to invest in charging-station development to ensure that rural populations are not left behind in the transition to electric mobility. Initiatives in countries like France and Italy are already underway to bolster charging availability in less populated areas, making EVs more appealing to potential buyers.

The integration of innovative charging solutions, such as mobile charging units and solar-powered charging stations,s can further enhance access in remote locations. These advancements not only address range anxiety but also align with the European Union’s sustainability goals by promoting green energy solutions. As infrastructure continues to expand, the opportunity to capture a broad consumer base in rural areas will be instrumental in driving the growth of the EV market across the region.

Europe Electric Vehicle Market Insights and Trends

Vehicle Type Insights - Passenger Vehicle Segment to Remain Leading Value Creator

The passenger vehicle segment dominates the European electric vehicle market, accounting for more than 45% of the market value in 2025. This growth is driven by increasing consumer demand for environmentally friendly transportation options supported by government incentives and strict emission regulations.

Leading countries in Europe such as Germany and Norway are at the forefront of electric vehicle adoption with substantial investments in infrastructure and innovation. In particular, Germany has established itself as a key market hub with leading automakers such as Volkswagen and BMW accelerating their production of electric models to meet both domestic and international demand.

Norway leads in EV penetration, with over 80% of new car sales being electric, spurred by favorable policies and tax exemptions. Further, the rise of SUVs and luxury electric vehicles is also significant in the passenger segment driven by consumer preferences for large, premium models equipped with advanced features.

Range Insights - Rapid Growth of the 301 to 500 km Range Segment Accelerates Market Growth

The 301 to 500 km leads the European electric vehicle market by range segment with more than 35% market revenue shares in 2026. This range is favored by consumers as it strikes a balance between cost-effectiveness and extended driving capacity, meeting the demands of both urban and long-distance travellers.

The growing network of fast-charging infrastructure across Europe, particularly in countries like Germany and France, has further supported the adoption of vehicles in this range.

In France, the government’s push for wider EV adoption has led to increased sales in the mid-range segment, where models such as the Renault Zoe and Peugeot e-208 offer competitive driving distances at accessible price points. Similarly, the Netherlands, with its dense charging infrastructure, supports this segment's growth, enabling drivers to travel comfortably across the country. This range is also ideal for European SUVs and family cars, as manufacturers prioritize enhancing battery efficiency while keeping costs in check.

Propulsion Type Insights - BEV Dominance Accelerates as Hybrids Sustain Transitional Market Momentum Globally

The expanded propulsion type analysis highlights the accelerating dominance of Battery Electric Vehicles (BEVs) while positioning hybrid powertrains as a critical transitional technology. BEVs accounted for 13.6% of global vehicle registrations in 2024, representing nearly 60% of total EV sales, with volumes reaching 1.4 million units. Penetration remains strongest in advanced markets such as Norway, where BEVs achieved 88% share, and Denmark at 51%, underscoring regulatory and infrastructure readiness. OEM performance further reinforces this trend, with Volkswagen delivering 427,000 BEVs and securing a 21.5% market share globally.

Strategic partnerships are strengthening BEV growth prospects in the long term. In November 2024, Volkswagen entered a USD 5.8 billion joint venture with Rivian, leveraging Rivian’s software-defined vehicle architecture and EV platforms. Initial models are expected from 2027, with testing planned for early 2026, supporting next-generation launches such as ID.EVERY1.

Meanwhile, Hybrid Electric Vehicles (HEVs) emerged as the fastest-growing segment, rising 19.6% year-on-year to 4.07 million units. Lower average prices (€42,222 vs. €62,709 for BEVs) and reduced infrastructure dependence continue to drive adoption. Plug-in hybrids (PHEVs), which are expanding at a 15% CAGR, remain essential for meeting interim decarbonization targets through 2033.

Regional Insights

Germany Takes the Charge in the Europe Electric Vehicle Market

Germany leads the market, securing a 15.2% CAGR of the Europe electric vehicle market in 2025. As the largest automotive market in Europe, Germany is a hub for EV production and adoption, supported by robust government incentives, including subsidies and tax exemptions aimed at boosting EV sales.

German cities like Hamburg, Munich, and Berlin have extensive charging infrastructure, making EV ownership increasingly attractive. Major players such as Volkswagen, BMW, and Mercedes-Benz have accelerated their EV initiatives, with Volkswagen planning to increase the share of EVs in its lineup to 50% by the forecast period.

The country’s dedication to cutting carbon emissions and meeting EU environmental targets has further driven growth in the EV market. Despite this, Germany faces challenges such as high production costs and increasing competition from Chinese manufacturers entering the European market.

Automakers in Germany are expected to focus more on high-end segments leaving volume sales vulnerable to foreign competitors. However, opportunities remain significant with continued investment in EV infrastructure particularly fast-charging stations, and advancements in battery technology.

The Europe EV market is forecast to maintain significant growth with a projected CAGR of 15.9% from 2026 to 2033, driven by continued innovation in both passenger and commercial electric vehicles.

UK Electric Vehicle Market Soars with Supportive Policies

The UK has emerged as one of the fastest-growing EV markets in Europe with a prominent CAGR of 16.3% in 2033. The UK government’s ambitious goal to ban the sale of new petrol and diesel cars by 2031 has significantly accelerated the adoption of electric vehicles.

Automakers such as Nissan and Jaguar Land Rover are at the forefront of EV production, supported by government-backed incentives like grants and subsidies for EV purchases. The country’s public charging infrastructure is also expanding with nearly 40,000 public charging points as of 2023 making EV ownership increasingly convenient for British consumers.

The UK faces challenges in its EV transition, including the need for further investment in charging infrastructure, particularly in rural areas, and the rising cost of raw materials for battery production. Despite these hurdles, the European electric vehicle market presents opportunities for growth, particularly in the expansion of battery production facilities and advancements in energy storage technologies.

The UK’s EV market is poised for continued expansion with a forecasted increase in EV sales and a growing focus on sustainability and zero-emission transport solutions

Competitive Landscape

Europe’s EV landscape saw intensified product launches, policy support, and strategic recalibration. BYD expanded aggressively by launching its lowest-priced U.K. model, the Dolphin Surf, and overtook Tesla in European BEV registrations for the first time. Germany rolled out a broad incentive framework under its “Responsibility for Germany” programme to accelerate EV adoption from July 2025. France relaunched social leasing in 2025, enabling low-income households to access affordable BEVs. OEM momentum remained strong, with Volkswagen Group, Toyota, Suzuki, Hyundai, and Lynk & Co expanding BEV and PHEV portfolios, even as policymakers reassessed EV timelines amid a short-term ICE resurgence.

| Sr. No | Company | Core Strategy | Strategic Actions in Europe |

|---|---|---|---|

| 1 | BYD | Aggressive price-led market entry | Launched Dolphin Surf in the UK at USD 21,650; surpassed Tesla in European BEV registrations (April 2025) |

| 2 | Volkswagen Group | Entry-level electrification & scale leadership | Expanded family of small, affordable EVs; reinforced dominance in compact EV segment |

| 3 | Toyota | Localized BEV manufacturing | Announced BEV production and battery assembly in Czech Republic |

| 4 | Lynk & Co | Electrified transition via PHEVs | Launched 08 PHEV with 200 km electric range |

| 5 | Suzuki | Phased BEV market entry | Introduced first BEV (e VITARA), targeting Europe from 2025 |

| 6 | Hyundai | Product premiumization in EVs | Planned launch of largest EV at Brussels Motor Show (Dec 2025) |

| 7 | Xiaomi | Delayed entry with ecosystem leverage | Planned European EV launch in 2027; exploring local manufacturing |

| 8 | Tesla | Volume defense amid rising competition | Faced first-time displacement by BYD in EU BEV registrations |

Key Industry Developments

- June 2025 - Price Competition Intensifies in Europe: In June 2025, BYD introduced its most affordable model in the UK, the Dolphin Surf, priced from USD 21,650, significantly undercutting incumbent competitors. The launch followed a milestone achievement in April 2025, when BYD registered more battery electric vehicles in Europe than Tesla for the first time, underscoring the growing competitive pressure from Chinese OEMs.

- June 2025 - Germany Expands EV Incentives: Germany unveiled a comprehensive EV incentive framework under the federal “Responsibility for Germany” programme. Effective from July 2025, the package combines fiscal incentives, infrastructure investment, and structural reforms to accelerate EV adoption and align transport decarbonization with national climate objectives.

- October 2025 - France Relaunches Social EV Leasing: France announced the 2025 round of its “leasing social” programme, targeting 50,000 BEVs for modest-income households. Monthly lease payments are capped at €200, supported by government subsidies covering up to 27% of vehicle cost (maximum €7,000), reinforcing equitable EV access.

- September 2025 - OEM Capacity Expansion in Europe: Volkswagen Group strengthened its leadership in Europe’s small-EV segment through an expanded portfolio of compact electric models. In parallel, Toyota confirmed European BEV production at its Czech facility, including a new battery assembly plant, signaling long-term localization.

- 2025-2027 - Market Recalibration and New Entrants: While automakers and regulators reassessed EV timelines amid a short-term ICE rebound in Europe, new launches continued. Lynk & Co introduced its 08 PHEV with a 200 km electric range, and Suzuki announced its first BEV, the e VITARA. Meanwhile, Xiaomi confirmed plans for a European EV debut in 2027, with potential local manufacturing under evaluation.

Companies Covered in Europe Electric Vehicle Market

- Volkswagen AG

- BMW AG

- Renault S.A.

- Daimler AG

- Ford Motor Company

- Audi AG

- Porsche AG

- Stellantis N.V.

- Volvo Cars

- Skoda Auto

- Fiat Chrysler Automobiles

- Peugeot

- MG Motor

- Tesla, Inc.

- Other Market Players

Frequently Asked Questions

Europe Electrical Vehicle market is estimated to be valued at US$ 241.8 Bn in 2026.

The primary demand driver for the European electric vehicle (EV) market is stringent emissions regulation combined with strong government incentives, which together are reshaping both consumer behavior and OEM product strategies.

In 2026, Germany will dominate the market with an exceeding 40% revenue share in the Europe Electrical Vehicle market.

Among ranges, 301 to 500 Km has the highest preference, capturing beyond 35% of the market revenue share in 2026, surpassing other ranges.

Porsche AG, Stellantis N.V., Volvo Cars, Skoda Auto, Fiat Chrysler Automobiles, Peugeot, MG Motor, and Tesla, Inc. There are a few leading players in the Electrical Vehicle market.