- Automotive Components & Materials

- Electric Parking Brake Market

Electric Parking Brake Market Size, Trend, Share, and Growth Forecast, 2026 - 2033

Electric Parking Brake Market by System (Cable-pull systems, Electric-hydraulic caliper systems, Caliper integrated EPB and Others), Vehicles (Passenger cars, Light commercial vehicles, Heavy commercial vehicles and Electric Vehicles), Sales Channel (OEM and Aftermarket), and Regional Analysis for 2026 - 2033

Electric Parking Brake Market Size and Trends Analysis

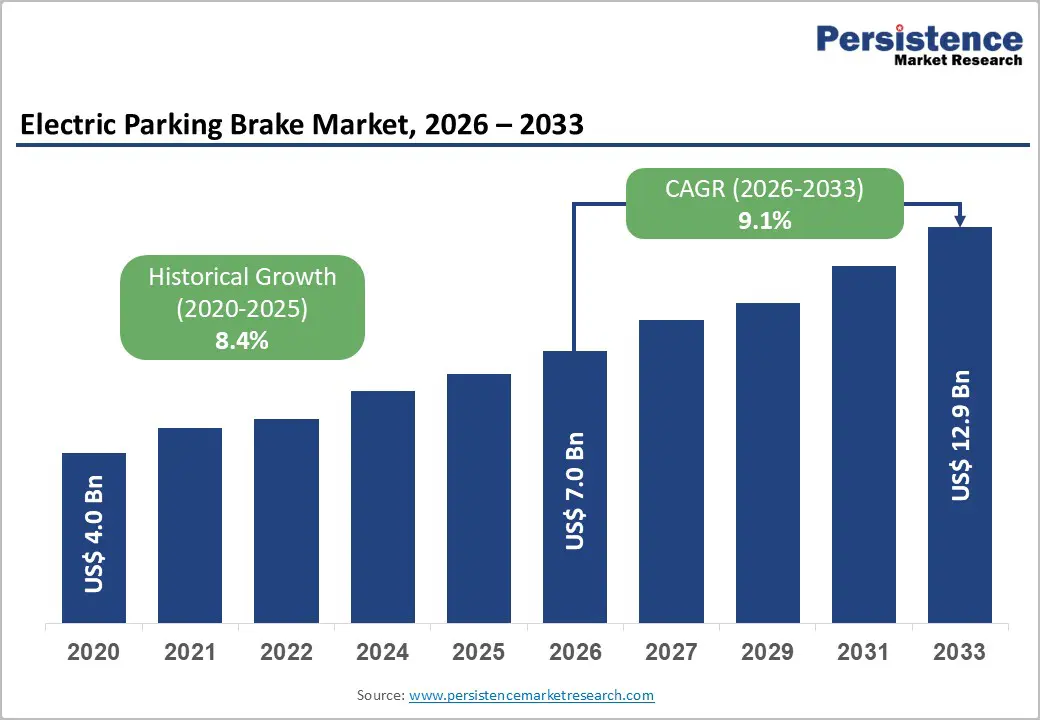

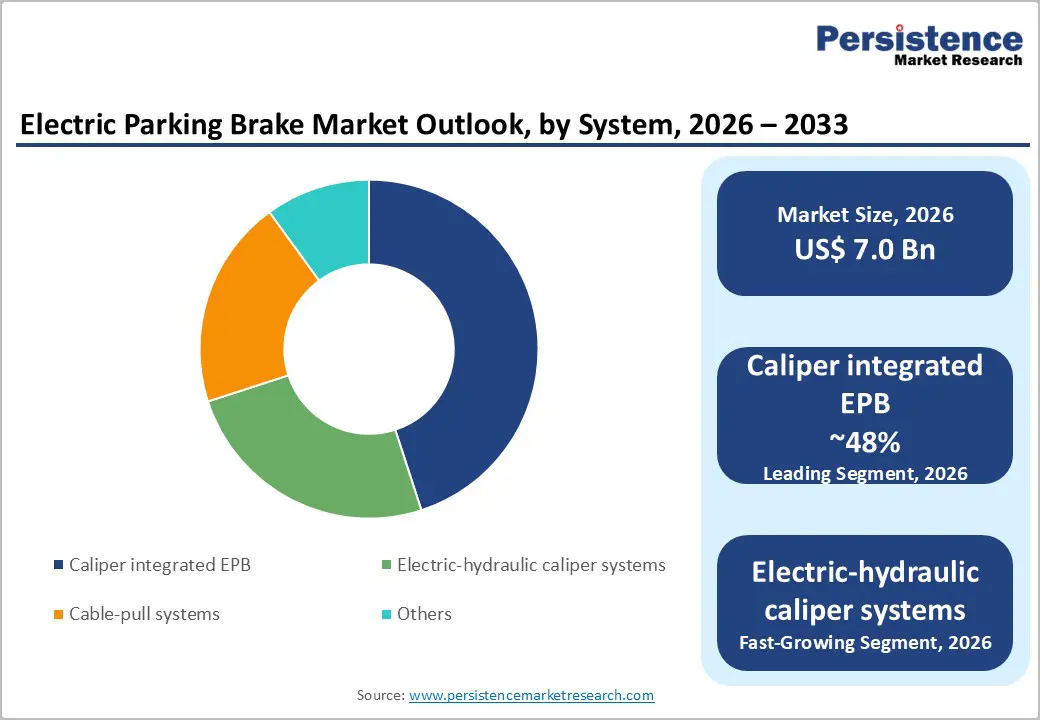

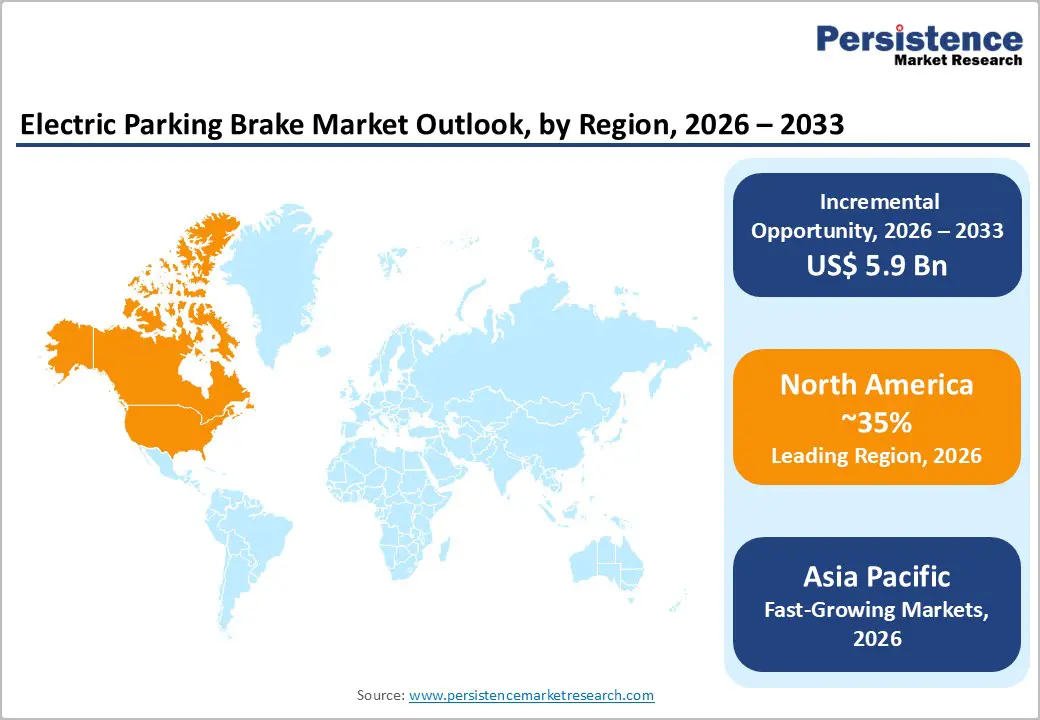

The global electric parking brake market size is likely to be valued at US$ 7.0 billion in 2026 and is projected to reach US$ 12.9 billion by 2033, growing at a CAGR of 9.1% between 2026 and 2033. The market is driven by the need for replacement of traditional mechanical parking brakes with electronically controlled systems across automotive segments, expanded EV infrastructure supporting regenerative braking integration, and increasing consumer demand for convenience features, including auto-hold and hill-assist capabilities.

Key Industry Highlights:

- Leading System Type: Caliper-integrated EPB dominates with 48% market share, driven by packaging efficiency and integration advantages; Electric-hydraulic caliper systems are the fastest-growing at a 12% CAGR, driven by premium vehicle and autonomous system deployment.

- Dominant Vehicle Type: Passenger cars maintain 58.4% market share through consumer preference and high-volume production; Electric vehicles are the fastest-growing segment at a 13% CAGR, driven by platform electrification requirements and regulatory compliance.

- Sales Channel Distribution: OEM dominates with 85% market share through primary new vehicle integration; Aftermarket represents the fastest growing at 8% CAGR, driven by retrofit demand and aging fleet modernization.

- Regional Market Dominance and Growth: North America maintains 35% global market share driven by regulatory mandates and premium vehicle penetration; Asia-Pacific demonstrates the fastest regional growth at 12% CAGR, expanding from 30% current share to 38% by 2033.

- Technology and Market Innovation Momentum: Top 10 suppliers control 60-% market share (Bosch, Continental, ZF leading); Autonomous-grade EPB systems meeting fail-operational requirements; AI-enabled diagnostics supporting predictive maintenance; EV optimization enabling regenerative braking integration.

| Key Insights | Details |

|---|---|

|

Electric Parking Brake Size (2026E) |

US$ 7.0 Bn |

|

Market Value Forecast (2033F) |

US$ 12.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

9.1% |

|

Historical Market Growth (CAGR 2020 to 2024) |

8.4% |

Market Dynamics

Drivers - Regulatory Mandates for Advanced Safety Systems and ADAS Integration

Government regulatory bodies across major automotive markets have mandated advanced braking technology integration establishing proportionate EPB demand. The European Union General Safety Regulation (EU) 2019/2144, effective July 2024, requires all new car models to incorporate automated braking functionality and driver assistance systems, indirectly driving systematic EPB adoption. The United States National Highway Traffic Safety Administration (NHTSA) is expanding its standards for electronic control components to enhance parking and emergency braking reliability.

Global automotive safety standards increasingly recognize EPB systems as essential components for autonomous driving readiness and ADAS compatibility. Regulatory compliance pressure, with vehicle manufacturers required to implement EPB systems that meet fail-safe performance standards, drives systematic market expansion. Safety certification requirements, with independent testing agencies validating EPB system performance across temperature, humidity, and durability metrics, establish a technology validation framework.

Vehicle Electrification and Regenerative Braking System Integration

Electric vehicle proliferation, with global EV sales reaching 13-15 million units annually and growing 25-30% year-over-year, creates proportionate EPB demand for electrified platforms. Regenerative braking requirements, with EV and hybrid platforms requiring coordinated braking control for energy recovery optimization and efficiency improvement of 15%, establish a technical necessity for electronic brake systems. EV architectural advantages, with electric platforms featuring simplified chassis designs and centralized electronic control systems enabling seamless EPB integration without traditional mechanical linkages, support rapid adoption.

Hybrid vehicle expansion, with plug-in hybrid electric vehicles (PHEVs) representing the fastest-growing vehicle segment at 35% annual growth, drives proportionate EPB system demand. The economics of battery-powered vehicles, with EPB systems enabling cabin space optimization and a 8-12 kg weight reduction compared to traditional handbrake systems, justify equipment investment. Charging infrastructure expansion, with government investment in 5-10 million EV charging stations globally through 2033, to establish a proportionate foundation for electric vehicle deployment.

Restraints - High System Integration Complexity and Legacy Vehicle Compatibility Challenges

Integration complexity barriers, including retrofitting older vehicle platforms to accommodate EPB systems that require significant modifications to hydraulic, mechanical, and electrical architectures, limit aftermarket adoption. Legacy vehicle incompatibility, with 55-65% of vehicles on European and North American roads exceeding 10 years of age and structurally incompatible with all-electronic braking layouts, constrains the retrofit addressable market. Supply chain modification requirements, including existing vehicles that require component redesign and ECU recalibration, increase implementation costs by 20-30%.

Technician training requirements, with specialized diagnostic and maintenance training required for EPB systems, are currently available to <40% of service centers in emerging markets, limiting service accessibility. System redundancy complexity, with fail-safe and dual-channel requirements increasing component costs and system complexity, compresses manufacturer margins. Interoperability challenges arise from non-standardized EPB implementations across OEM platforms, creating compatibility and servicing challenges for aftermarket providers.

High Capital Equipment Costs and Aftermarket Price Barriers

System acquisition costs, with EPB retrofit systems commanding US$ 1,500-3,500+ pricing for quality installations versus

Opportunity - Autonomous Driving System Integration and Level 3+ Vehicle Deployment

Autonomous vehicle development acceleration, with Level 3+ autonomous vehicle testing programs proliferating globally and requiring sophisticated EPB system integration for fail-operational safety, establishes specialized equipment demand. Safety-critical system requirements, with autonomous platform development mandating redundant braking capability and fail-safe EPB operation, drive premium-priced specialized system development. Regulatory testing framework expansion, with governments establishing autonomous vehicle testing programs in 50+ cities globally and requiring certified EPB systems meeting fail-operational standards, create systematic demand. V2X integration opportunities, with vehicle-to-infrastructure communication enabling coordinated EPB operation across autonomous vehicle fleets, establishing an emerging capability segment.

Aftermarket Retrofit and Fleet Electrification Acceleration

Commercial fleet modernization demand, with logistics and transportation companies upgrading aging fleets to reduce operating costs and emissions, driving 25-30% annual fleet replacement rates, establishes a proportionate aftermarket opportunity. Used vehicle market expansion, with secondary market vehicle transactions growing 20-25% annually and aftermarket buyers seeking advanced safety features, drive retrofit equipment demand. Rental fleet EPB integration, with major rental car companies standardizing EPB-equipped vehicles across international fleets, ensuring customer familiarity, and establishing volume demand. Taxi and rideshare fleet requirements, with transportation network companies mandating advanced safety features including EPB systems for driver safety, create a systematic fleet purchasing opportunity.

Category-wise Analysis

EPB System Type Insights

The caliper-integrated EPB segment holds 48% market share, driven by technical efficiency and compact packaging. By integrating electric actuators directly into brake calipers, these systems eliminate mechanical linkages, reducing component count and system complexity. This design enables 10–15 liters of interior space savings versus cable-pull systems, supporting OEM cabin optimization. High manufacturing standardization and scale have achieved cost parity with conventional solutions while delivering enhanced functionality and reliability. Shorter signal paths and fewer failure points improve system durability, reinforcing widespread OEM adoption.

In contrast, the electric-hydraulic caliper EPB segment is the fastest growing, expanding at 12% CAGR through 2033. Growth is driven by adoption in premium, hybrid, and electric vehicles requiring advanced braking control, redundancy, and precise modulation. Electric-hydraulic systems support ABS, ESC, autonomous parking, and regenerative braking optimization, making them ideal for EV architectures. Ongoing technology maturation, improving reliability and cost efficiency, enabling broader deployment beyond luxury vehicles, accelerating segment growth.

Vehicle Type Insights

The passenger car segment holds 58.4% market share, driven by its dominance in global vehicle production and strong consumer demand for convenience features. Passenger cars account for 55% of global vehicle manufacturing, creating a solid volume base for EPB adoption. Affluent consumers increasingly prioritize comfort and safety technologies, while premium brands such as BMW, Mercedes-Benz, and Audi have standardized EPB systems across model ranges, accelerating mainstream acceptance. The passenger car aftermarket representing 70% of total vehicle service revenue further supports retrofit potential, while established retail networks enable rapid penetration of EPB-equipped models.

The electric vehicle (EV) segment is the fastest-growing, projected to expand at a 15% CAGR through 2033. EPB adoption is effectively mandatory in EV architectures to support regenerative braking and centralized electronic control. Strong regulatory support for decarbonization, massive investment in charging infrastructure, advances in battery performance, and EV-optimized electronic platforms that enable features such as auto-hold and predictive braking are driving accelerated EPB integration in electric vehicles.

Sales Channel Insights

The OEM sales channel accounts for 85% market share, driven by its direct integration into new vehicle production. OEM sourcing enables systematic deployment of EPB systems across vehicle platforms, establishing a strong volume demand base. High-volume procurement provides a 20% cost advantage over aftermarket channels, while platform standardization reduces complexity and manufacturing costs. Long-term OEM supplier partnerships support joint R&D investment and capacity planning, strengthening competitive positioning. As EPB adoption is primarily tied to new vehicle sales, OEM dominance reflects production-led market growth.

In contrast, the aftermarket channel is the fastest-growing, projected to expand at a 10% CAGR through 2033. Growth is driven by rising retrofit demand from aging vehicle fleets seeking safety compliance and feature upgrades. Increasing consumer interest in convenience features, higher aftermarket margins, fleet modernization requirements, and improved standardization of retrofit solutions through service networks are accelerating aftermarket adoption.

Regional Insights

North America Electric Parking Brake System Market Insights & Trends

North America commands approximately 32-36% of global Electric Parking Brake market share, valued at approximately US$ 2.24-2.52 billion in 2026 with projections approaching US$ 4.1-4.8 billion by 2033. The United States represents dominant regional market contributor, accounting for 82-86% of North American market value, driven by premium vehicle market penetration and regulatory safety mandates.

NHTSA regulatory mandate enforcement, with evolving safety standards requiring electronic braking component certification and deployment, establish systematic OEM adoption foundation. Premium vehicle market concentration, with North American consumers allocating 40-50% of vehicle spending to premium segments valuing advanced features including EPB systems, drive purchasing preference. EV market acceleration, with US EV sales growing 30-35% annually and supporting infrastructure investment expanding proportionally, establish technical requirement foundation.

Europe Electric Parking Brake System Market Analysis

Europe represents approximately 22% of the global Electric parking brake market share, valued at approximately US$ 1.82 billion in 2026. Germany, the United Kingdom, France, and Spain collectively represent 70% of the European market value, reflecting an advanced regulatory environment and technology leadership.

The EU General Safety Regulation (EU) 2019/2144, with mandatory ADAS and advanced braking requirements, drives systematic EPB adoption across all manufacturers. Vehicle electrification leadership, with the European EV market representing 20-25% of total vehicle sales and growing 15-20% annually, establishes proportionate EPB demand. Premium vehicle market dominance, with luxury vehicle manufacturers concentrated in Germany and establishing EPB as a standard feature, creating aspirational adoption, supporting market penetration. Retrofit market maturity, with established aftermarket infrastructure and consumer demand for safety feature upgrades in aging vehicle fleet, create retrofit opportunity.

Asia Pacific Electric Parking Brake System Market Analysis

Asia Pacific demonstrates robust growth dynamics, commanding approximately 30% market share with projections increasing to 38% by 2033. The region valued at approximately US$ 2.24 billion in 2026 is anticipated to reach US$ 5.0 billion by 2033, representing the fastest-growing regional market with an estimated CAGR of 11%.

Vehicle electrification acceleration, with China, India, Japan, and South Korea collectively producing 8-10 million EVs annually and growing 30-40% year-over-year, establishes proportionate EPB demand. Manufacturing capability dominance, with Chinese and Indian EPB manufacturers achieving 30-40% cost advantages through regional production and localization, enable market penetration at accessible price points. Modular architecture adoption, with Asian OEMs standardizing chassis control modules enabling scalable EPB solutions across vehicle segments, support platform standardization.

Competitive Landscape

The global electric parking brake market demonstrates moderate to high consolidation with established automotive component suppliers and specialized braking system manufacturers maintaining competitive positions. The top 10 suppliers, including Bosch, Continental, ZF, Hyundai Mobis, Wabco, Hitachi, Nexteer, Akebono, Advics, and Brembo, collectively control approximately 60% of global market share, reflecting technology leadership, manufacturing scale, and established OEM relationships.

Market structure reflects bifurcation between large multinational tier-1 automotive component suppliers offering comprehensive braking solutions and specialized EPB system manufacturers focusing exclusively on parking brake development.

Key Industry Developments

- In April 2025, Hitachi Astemo introduced a compact EPB module for hybrid and electric vehicles, featuring advanced controls and predictive diagnostics for automated braking and autonomous driving.

- In February 2025, Knorr-Bremse introduced an upgraded EPB system for heavy-duty trucks and buses, enhancing actuator reliability and integration with braking and stability control systems for fleets in Europe and North America.

- In December 2024, Robert Bosch launched its new EPB series, boasting improved energy efficiency and integration features tailored for hybrid and electric vehicles. This system, equipped with compact actuators and sophisticated diagnostics, helps OEMs meet global electrification and safety benchmarks.

Companies Covered in Electric Parking Brake Market

- Aisin Seiki

- Akebono Brake Industry

- Brembo

- Continental

- Hitachi Astemo

- Hyundai Mobis

- Knorr-Bremse

- Mando

- Robert Bosch

- ZF Friedrichshafen

- Others Key Players

Frequently Asked Questions

The Electric Parking Brake market is estimated to be valued at US$ 7.0 Bn in 2026.

The key demand driver for the Electric Parking Brake (EPB) market is the rapid adoption of advanced vehicle safety, comfort, and electronic control systems, driven by regulatory mandates and vehicle electrification.

In 2026, the North America region will dominate the market with an exceeding 35% revenue share in the global Electric Parking Brake market.

Among the System, Caliper integrated EPB holds the highest preference, capturing beyond 48% of the market revenue share in 2026, surpassing other System type.

The key players in Electric Parking Brake are Aisin Seiki, Brembo, Continental and Hitachi Astemo.