- Pharmaceuticals

- Dry Eye Syndrome Treatment Market

Dry Eye Syndrome Treatment Market Size, Share, Trends Growth, and Regional Forecast, 2025 - 2032

Dry Eye Syndrome Treatment Market by Product (Cyclosporine, Topical Corticosteroids, Artificial Tears, Punctal Plugs, Omega Supplements, and Others), Prescription Type (Rx, OTC, and Medical Devices), Distribution Channel, Regional Analysis, 2025 - 2032

Dry Eye Syndrome Treatment Market Share and Trends Analysis

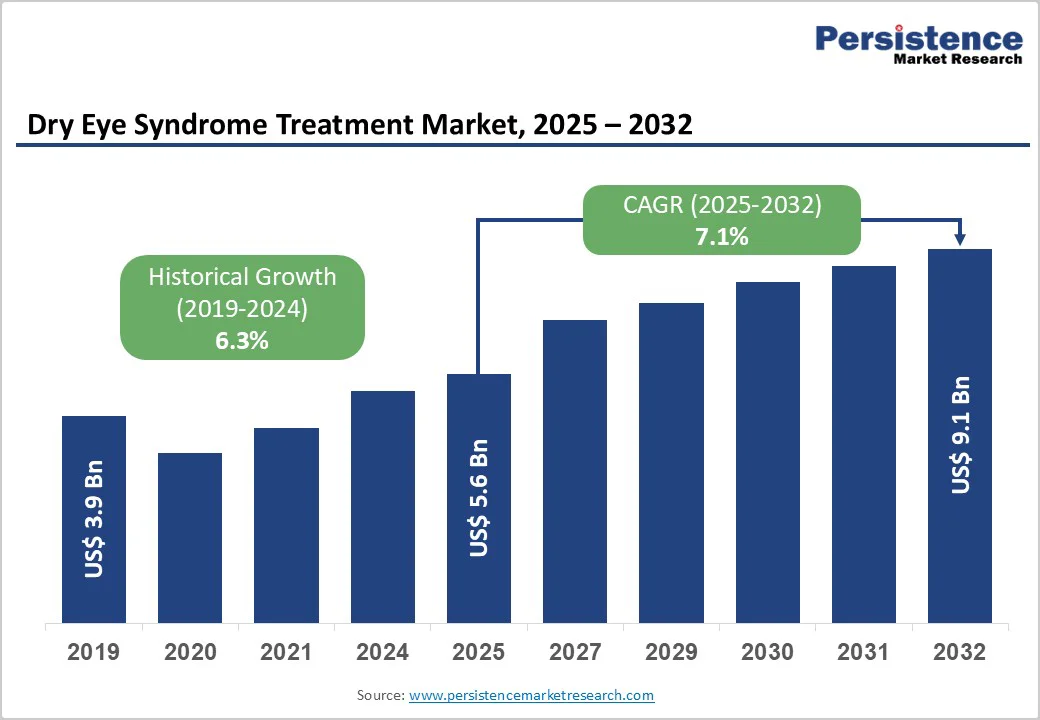

The global dry eye syndrome treatment market size is valued at US$ 5.6 billion in 2025 and projected to reach US$ 9.1 billion, growing at a CAGR of 7.1% during the forecast period from 2025 to 2032. Lack of lubrication and tear formation on the eye surface is the cause of dry eye syndrome. As a result, the eye becomes dry, irritated, and inflammatory. There are numerous treatment options, including oral medications, topical medications, and surgical procedures.

The multifactorial condition known as dry eye disease causes the tear film and ocular surface to lose equilibrium, leading to symptoms such as eye irritation, dryness, and impaired vision. About 5–50% of people worldwide suffer from such a condition. The prevalence of dry eye disorder varies depending on the diagnostic criteria used, the location, the age range, and the gender.

Key Industry Highlights:

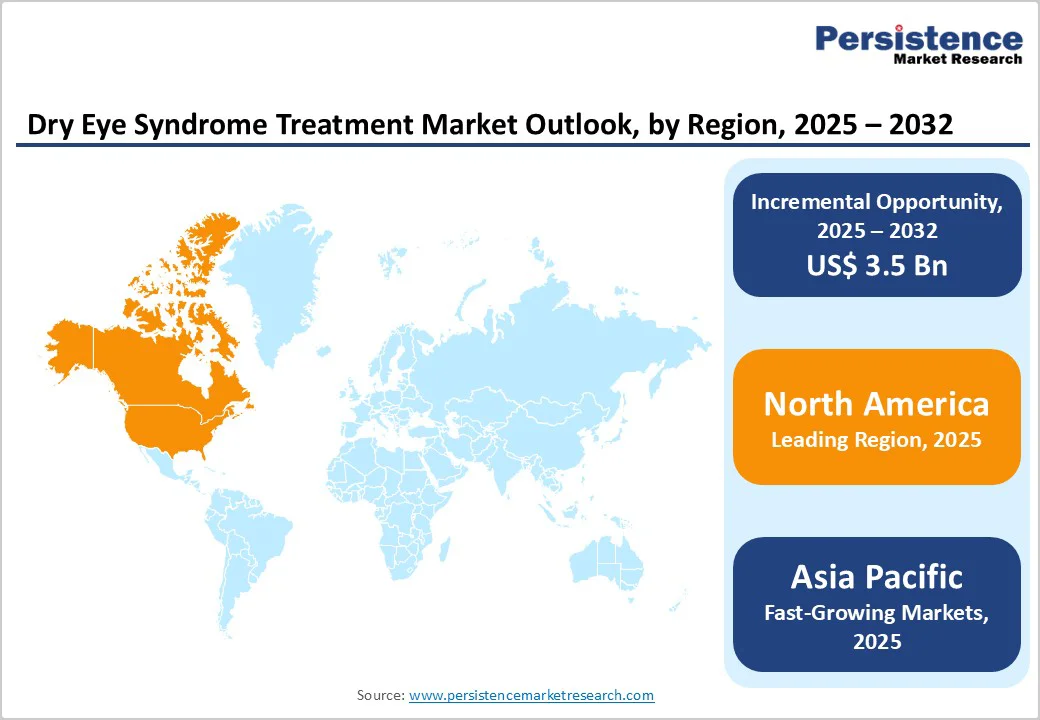

- Leading Region: North America leads the dry eye syndrome treatment market due to advanced healthcare systems and robust regulatory support.

- Fastest Growing Region: Asia Pacific is the fastest growing region, driven by increasing prevalence, and improving healthcare infrastructure.

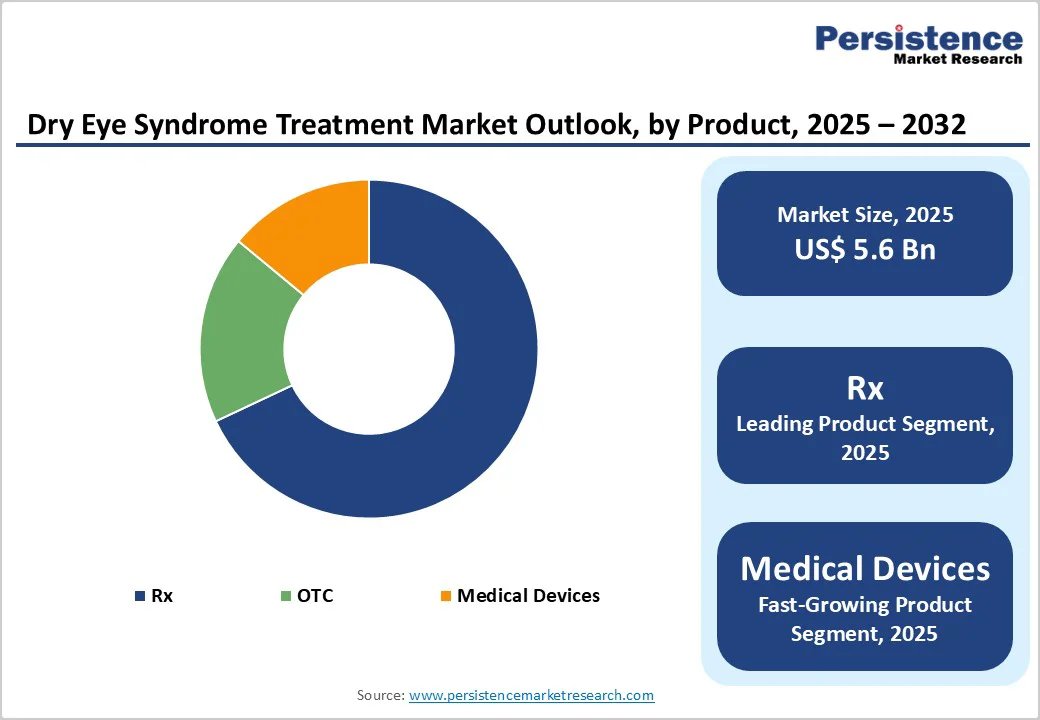

- Dominant Segment: Artificial tears dominate the product category with a 60% market share, favored for ease of use and broad OTC availability.

- Fastest Growing Segment: The medical devices segment is the fastest growing, driven by rising adoption of IPL systems, thermal pulsation devices, meibomian gland therapies, and in-office procedures offering longer-lasting relief for dry eye patients.

| Key Insights | Details |

|---|---|

|

Dry Eye Syndrome Treatment Market Size (2025E) |

US$ 5.6 Bn |

|

Market Value Forecast (2032F) |

US$ 9.1 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.1% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.3% |

Market Dynamics

Driver - Increasing Number of LASIK Surgeries and Growing R&D Initiatives and Growing Number of Drug Candidates to Consolidate Business

According to recent 2025 research by NVISION, LASIK continues to be one of the most widely performed vision-correction procedures in the U.S., with nearly 800,000 surgeries conducted annually and over 10 million people treated since FDA approval. With a 98.5% patient satisfaction rate, the procedure maintains strong demand among individuals seeking freedom from spectacles and contact lenses. However, dry eye remains a significant postoperative concern. Clinical data indicate that 25–30% of patients experience clinically meaningful dry eye within the first three months after LASIK, while symptoms may persist in 8–12% of cases long-term, fueling sustained need for therapeutic intervention.

This rising surgical volume directly expands the patient pool requiring treatment, encouraging manufacturers to invest in targeted formulations for post-LASIK dry eye management. Parallel to this trend, the market is witnessing robust R&D acceleration. Global pharmaceutical spending on ocular surface disorders has increased by 8–10% annually, while the number of active clinical trials for dry eye therapeutics has grown by over 20% in the past five years. Promising candidates such as Aldeyra Therapeutics’ Reproxalap (Phase III) reflect a strong pipeline, with 15+ novel molecules currently progressing across phases. Together, these developments support market consolidation and long-term growth.

Restraints - Dry Eye Syndrome Treatment Lack of Awareness Will Constrain Market Expansion

Limited public awareness about dry eye symptoms continues to restrict timely diagnosis and appropriate treatment adoption across many regions. A large proportion of individuals interpret persistent eye irritation, burning, or blurred vision as minor, temporary issues rather than indicators of a chronic condition. Due to this misconception, many patients delay seeking medical advice or depend on basic home remedies, which do not address the underlying causes. The absence of standardized diagnostic protocols across clinics and hospitals further contributes to inconsistent identification of the condition, especially in primary care settings.

In several emerging economies, low eye-health literacy and inadequate outreach programs mean that dry eye often remains undetected until symptoms significantly worsen. This underdiagnosis results in fewer patients entering the treatment pathway, limiting demand for prescription therapies, advanced devices, and long-term management solutions. Consequently, reduced patient awareness directly dampens market penetration efforts, slows product uptake, and restricts the overall growth potential of the dry eye syndrome treatment market.

Opportunity - Expansion in Over the Counter (OTC) Treatments

The growing shift toward self-management of eye discomfort is opening strong opportunities within the OTC dry eye treatment category. Consumers increasingly rely on artificial tears, lubricating gels, and nutritional supplements for routine relief, driven by ease of access through pharmacies, optical channels, and expanding e-commerce platforms. Affordable pricing and the availability of multiple product formats further encourage frequent purchase and trial.

Manufacturers are strengthening this trend through focused educational initiatives. For example, Alcon’s digital awareness programs on social media and eye-health portals highlight early signs of dry eye and promote consistent use of OTC lubricants for everyday relief. Similar campaigns by Bausch + Lomb, which include online symptom checklists and short educational videos, help consumers identify dryness early and choose suitable OTC options. These initiatives have improved awareness of preventive care and increased confidence in self-directed treatment.

In emerging regions, improved online reach and expanding pharmacy networks are making OTC solutions more accessible. As education and self-care awareness continue to grow, the OTC segment is positioned for faster adoption and strong, sustained market growth.

Category-wise Analysis

By Product Insights

Artificial tears continue to represent the strongest product category, accounting for nearly 60% of total share in 2025. Their leadership is driven by wide availability, low treatment barriers, and the ability to deliver quick symptom relief for a broad patient population. The segment includes a variety of formulations ranging from basic lubricating drops to advanced preservative-free, gel-based, lipid-based, and nanoemulsion solutions, allowing consumers and clinicians to match products to individual severity levels. Easy access through retail pharmacies, supermarkets, and online platforms reinforces their appeal, particularly among individuals preferring self-care over clinical intervention. The increasing shift toward chronic use for digital screen fatigue, environmental exposure, and contact-lens-related dryness further boosts demand. Continuous product upgrades, such as long-lasting moisture retention technologies and formulations mimicking natural tear components, are enhancing comfort and therapeutic value. Together, these factors secure artificial tears as the dominant contributor to the overall dry eye treatment market.

By Prescription Insights

Prescription therapies retain a commanding 68% share in the dry eye treatment landscape, supported by their essential role in managing moderate to severe cases where inflammation and glandular dysfunction require targeted medical intervention. Drugs such as cyclosporine, lifitegrast, corticosteroids, and novel anti-inflammatory agents help address underlying ocular surface damage rather than offering temporary relief, making them the preferred choice for long-term disease control. Growing access to ophthalmologists, improved diagnostic precision, and rising awareness of chronic disease progression contribute to sustained prescription demand.

Alongside this, medical devices are emerging as the fastest-growing segment as clinicians increasingly adopt technologies like thermal pulsation systems, Intense Pulsed Light (IPL) therapy, meibomian gland heating devices, punctal plugs, and neurostimulation tools. These procedures offer longer-lasting benefits, particularly for meibomian gland dysfunction, driving rapid uptake across specialty clinics. Higher clinical efficacy, expanding reimbursement support, and technology advancements are positioning device-based therapies as a strong growth engine.

Region-wise Insights

North America Dry Eye Syndrome Treatment Market Trends

North America continues to lead the dry eye syndrome treatment market, supported by well-established healthcare systems, high diagnostic capabilities, and a strong base of specialty eye-care providers. The region benefits from extensive awareness initiatives that encourage early identification of symptoms and timely treatment. In the U.S., the burden of dry eye remains substantial, driven by an aging demographic, widespread use of digital screens, and increased environmental triggers such as air conditioning and pollution. These factors contribute to strong demand for both prescription therapies and advanced device-based treatments. Regulatory agencies, particularly the FDA, have also played an important role by enabling faster evaluation and approval of innovative formulations and technologies, which keeps the treatment landscape highly dynamic.

The U.S. accounted for over 80% of the North American market in 2025 due to its large patient pool, better healthcare access, and higher treatment adoption. Major manufacturers are increasing engagement efforts through education-focused campaigns. For example, Novartis launched its “Not Today, Dry Eye” initiative to highlight the role of inflammation in disease progression and encourage individuals to seek appropriate care at earlier stages.

Asia Pacific Dry Eye Syndrome Treatment Market Analysis

Asia Pacific has emerged as the fastest-growing region in the dry eye syndrome treatment market, driven by rapid urbanization, lifestyle changes, and rising exposure to environmental pollutants. Increased screen time, heavy digital device use, and long working hours are contributing to a steady rise in dry eye symptoms across major countries such as China, Japan, South Korea, and India. Expanding middle-class populations and improving access to healthcare services are also encouraging more patients to seek timely treatment. Governments across the region are investing in healthcare infrastructure, while local manufacturers continue to strengthen production capabilities, making treatments more affordable and widely available.

India remains particularly attractive due to its large population and growing healthcare expenditure. Many global and regional players have set up manufacturing facilities in the country, supported by a strong workforce and competitive production costs. With the United Nations projecting that nearly 20% of India’s population will be above 60 years in the next three decades, the demand for dry eye treatments is expected to rise sharply.

China is also witnessing structural changes in its pharmaceutical sector. Although the industry is fragmented with many small and mid-sized companies, government initiatives under the 14th Five-Year Plan aim to raise R&D spending and improve product quality. Strong distribution networks led by companies like Sinopharm and Shanghai Pharmaceuticals support market expansion, while multinational firms such as AstraZeneca and Novartis maintain notable market presence.

Competitive Landscape

The major companies in the market for treating dry eye syndrome are concentrating on growing their product portfolio through ongoing product research and development and launches. To strengthen the market presence for expanding the of dry eye syndrome treatment lines, various pharmaceutical companies are forming strategic partnerships with mid-sized or small-size players and also focusing on expanding their production facilities. This strategy is anticipated to increase their sales footprint in the global dry eye syndrome treatment industry.

Key Industry Developments:

- In July 2025, Aldeyra Therapeutics, Inc. announced that the U.S. FDA has accepted the resubmitted New Drug Application (NDA) for topical ocular reproxalap, a first-in-class investigational therapy, for the treatment of signs and symptoms of dry eye disease.

- In May 2025, Alcon announced that the FDA had approved TRYPTYR (acoltremon ophthalmic solution) 0.003% for treating the signs and symptoms of dry eye disease.

- In October 2024, Novaliq and Laboratoires Théa reported that the European Commission granted approval for Vevizye for the treatment of dry eye disease in adults.

Companies Covered in Dry Eye Syndrome Treatment Market

- Allergan Plc.

- Novartis AG

- Otsuka Pharmaceutical Co.,Ltd.

- Santen Pharmaceutical Co Ltd.

- Bausch Health Companies Inc.

- Akorn, Inc.

- Johnson & Johnson, Inc.

- Thea Pharmaceuticals Limited

- OASIS Medical

- Altaire Pharmaceuticals Inc.

- Boiron USA

- Similasan Corporation

- Scope Ophthalmics Ltd.

- Reckitt Benckiser Group PLC

- Medicom Healthcare Ltd

- FDC Limited.

- Lupin Limited

- Jamjoom Pharmaceuticals Co.

- Sentiss Pharma Private limited

Frequently Asked Questions

The global dry eye syndrome treatment market is projected to be valued at US$ 5.6 Bn in 2025.

Growing screen time, aging population, Meibomian Gland Dysfunction (MGD) prevalence, new Rx therapies, OTC adoption, and rising procedural device usage.

The global market is poised to witness a CAGR of 7.1% between 2025 and 2032.

Expansion of device-based therapies, innovative prescription launches, emerging-market access, digital diagnostics, and personalized treatment protocols for chronic dry eye.

Allergan Plc., Novartis AG, Johnson & Johnson. Inc., Reckitt Benckiser Group Plc., and Lupin Limited are the top five manufacturers of dry eye syndrome treatment products.