- Non-food Packaging

- Display Pallets Market

Display Pallets Market Size, Share, and Growth Forecast, 2026 - 2033

Display Pallets Market by Product Type (Full Pallet Display, Quarter Pallet Display, Others), Material Type (Corrugated & Paper Board, Plastic, Others), Orientation, End-user Industry, and Regional Analysis for 2026 - 2033

Display Pallets Market Size and Trends Analysis

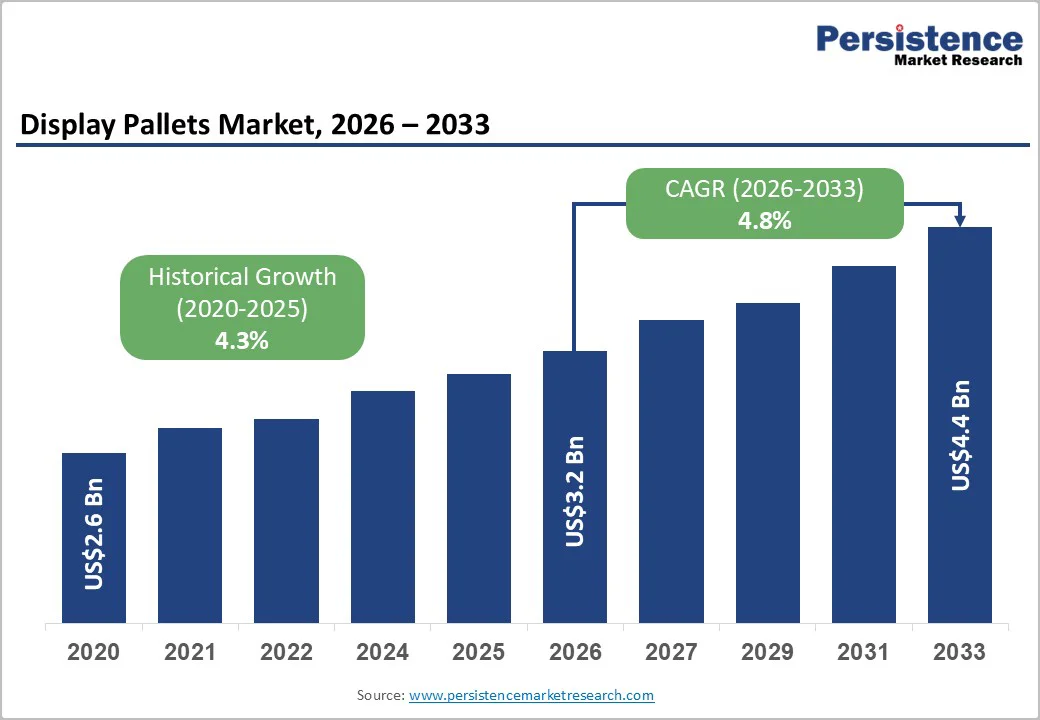

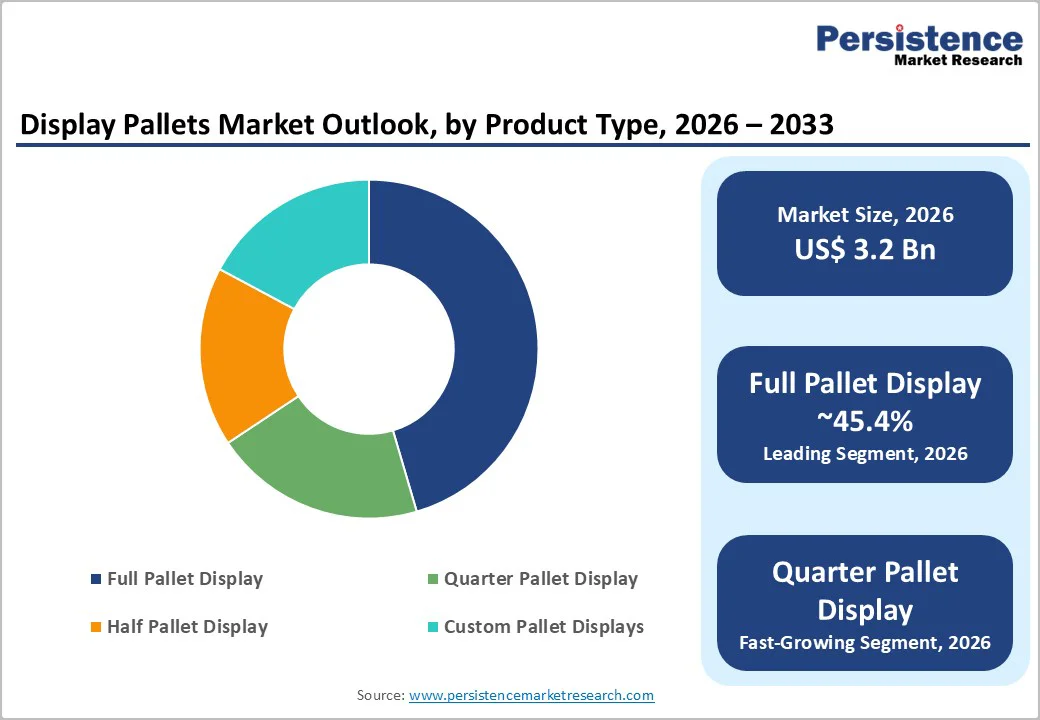

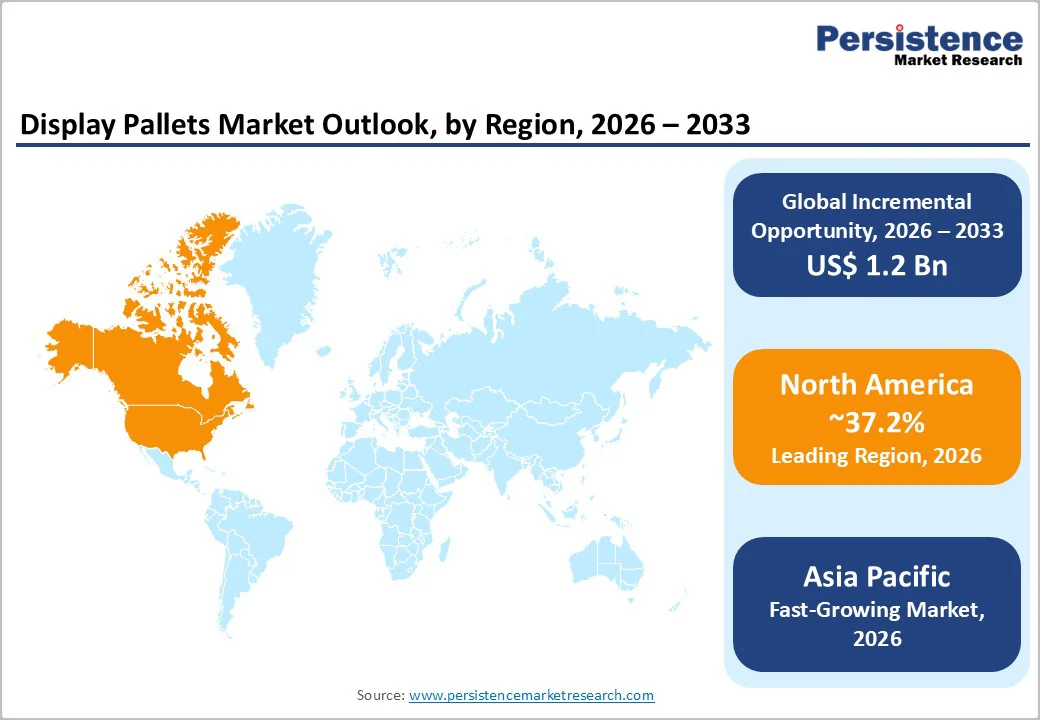

The global display pallets market size is likely to be valued at US$3.2 billion in 2026. It is expected to reach US$4.4 billion by 2033, growing at a CAGR of 4.8% between 2026 and 2033, driven by rising investments in modern retail merchandising, the continued integration of omnichannel retail models, and the increasing use of in-store promotional displays to drive conversion.

A move toward recyclable corrugated and polypropylene display systems, motivated by sustainability goals and changing packaging regulations, is influencing material choices. Concurrently, the broader use of modular quarter and half-pallet formats is streamlining supply chains and enhancing store-level execution efficiency.

Key Industry Highlights

- Leading Region: North America is projected to account for approximately 37.2% of global market revenue, supported by high promotional intensity, mature modern retail infrastructure, and widespread adoption of pallet pooling.

- Fastest-growing Region: Asia Pacific, projected to register the highest growth rate through the forecast period, driven by the rapid expansion of organized retail, strong e-commerce volumes, and cost-competitive corrugated manufacturing across China, India, and ASEAN markets.

- Investment Plans: Ongoing investments are concentrated in pooled and reusable plastic display pallets, automation-compatible pallet designs, and fiber-engineered corrugated solutions, as well as in digital tools that integrate promotional display planning with logistics and reverse-logistics execution.

- Dominant Product Type: Full pallet displays to hold approximately 45.4% market share, owing to their extensive use in high-volume promotions across grocery, club, and big-box retail formats.

- Leading Material Type: Corrugated and paperboard materials are estimated to account for approximately 56.7% of total material usage, owing to their recyclability, cost efficiency, and suitability for short-cycle promotional display applications.

| Key Insights | Details |

|---|---|

| Display Pallets Market Size (2026E) | US$3.2 Bn |

| Market Value Forecast (2033F) | US$4.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Omnichannel Retailing and In-Store Activation

Retailers are increasingly leveraging in-store merchandising as a complement to digital and e-commerce channels, recognizing that physical displays remain critical for impulse purchases, bulk buying, and brand visibility. Display pallets enable rapid deployment of promotional assortments, ensuring consistency across stores and reducing merchandising labor.

Standardized pallet-compatible formats allow retailers to synchronize distribution center operations with store-level execution, supporting faster replenishment cycles. The growing use of modular quarter- and half-pallet configurations further enhances layout flexibility, particularly in urban and smaller-format stores. As omnichannel strategies mature, display pallets continue to play a central role in bridging digital planning with physical retail execution.

Sustainability and Regulatory Pressure Favoring Recyclable Materials

Packaging regulations and sustainability mandates are accelerating the transition toward recyclable and low-impact materials across retail supply chains. Display pallets, as a form of tertiary packaging, are increasingly scrutinized for recyclability, material efficiency, and end-of-life recovery. This environment has strengthened demand for corrugated and paperboard display pallets and for recycled-content plastic alternatives.

Brands are increasingly shifting away from mixed-material or single-use wooden pallets toward designs that align with corporate environmental commitments and regulatory compliance. These changes are influencing procurement decisions, supplier qualification standards, and product development priorities across the display pallets ecosystem.

Pallet Pooling and Circular Supply-Chain Models

Reusable pallet pooling systems are gaining traction as retailers and consumer goods manufacturers seek to reduce total landed cost and packaging waste. Pooled display pallets, particularly those made from durable plastics or reinforced corrugated materials, enable repeated use across promotional cycles while improving asset utilization.

Circular supply-chain models reduce disposal costs, simplify reverse logistics, and support environmental reporting requirements. The expansion of pooling services to include display-grade pallets has increased adoption among large retailers and brand owners, reinforcing demand for standardized, reusable display solutions.

Barrier Analysis - Raw Material and Recycling Infrastructure Volatility

Corrugated and paperboard materials account for the majority of display pallet usage, but recovered fiber supply, regional recycling rates, and processing capacity influence fluctuations in their availability and pricing. Shifts in recycling collection systems and export restrictions can constrain feedstock availability, leading to short-term price volatility.

These fluctuations raise production costs for display pallet manufacturers and complicate inventory planning for promotional campaigns. In regions with limited recycling infrastructure, corrugated input costs can increase by mid-single-digit percentages over short periods, compressing margins and limiting pricing flexibility.

Seasonal Demand Patterns and Channel Complexity

Display pallet demand is closely tied to retail promotional calendars, resulting in pronounced seasonality. Peak promotional periods require rapid scale-up in production capacity, while off-peak periods often lead to underutilization. This imbalance increases per-unit manufacturing costs and operational inefficiencies for suppliers.

Retailers also face risks from last-minute promotional changes, which can trigger expedited production and freight costs. During peak-demand windows, short-term cost increases in logistics and manufacturing can reach double-digit levels, affecting both supplier profitability and retailer promotional budgets.

Opportunity Analysis - Modular Quarter and Half Pallet Systems

Quarter-pallet displays are the fastest-growing product type, driven by their suitability for space-constrained retail formats and micro-fulfillment environments. These systems improve shelf-to-floor conversion and reduce in-store handling requirements.

If quarter pallets capture an incremental 6-8% of global display pallet volumes by 2030, this would translate into an incremental revenue opportunity of several hundred million U.S. dollars based on current market baselines. Retailers benefit from improved placement speed and flexibility, while brands gain the ability to localize promotions more efficiently across diverse store formats.

Circular Pooled Display Systems and Recycled Plastics

The use of pooled display pallets manufactured with high levels of post-consumer recycled content presents a compelling value proposition for large consumer goods companies. These systems reduce lifecycle costs, improve environmental performance metrics, and support compliance with emerging packaging regulations.

If 10-20% of display pallets transition from one-way use to pooled or reusable models in key grocery and mass retail channels by 2030, the resulting cost savings and emissions reductions would represent a multi-hundred-million-dollar value pool globally. Early adopters can secure long-term supply stability and favorable pricing through strategic pooling agreements.

Category-wise Analysis

Product Type Insights

Full-pallet displays are expected to remain the dominant product type, accounting for approximately 45.4% of market revenue. These displays are extensively used for high-volume and fast-moving consumer goods that benefit from strong floor presence, including carbonated beverages, bottled water, packaged food staples, paper products, and household cleaning supplies.

Their standardized dimensions allow seamless integration with forklifts, pallet jacks, and automated warehouse systems, enabling efficient movement from manufacturing plants to retail floors without repacking.

Large-format supermarkets, warehouse clubs, and discount retailers continue to rely on full pallet displays for seasonal promotions, bulk pricing events, and end-cap activations. The higher unit value per display, combined with repeat usage across recurring promotional cycles, supports consistent procurement volumes. Their structural stability also allows stacking and long dwell times on the sales floor, reinforcing their position as the leading product type in the market.

Quarter pallet displays are emerging as the fastest-growing product type, driven by changing retail layouts and increasing store density in urban markets. Their compact footprint makes them well-suited for convenience stores, neighborhood supermarkets, pharmacies, and specialty retail outlets, where floor space is limited but promotional visibility remains critical.

These displays enable more precise planogram execution and allow retailers to test localized promotions without committing to full pallet volumes.

Growth is further supported by sustainability-driven designs, particularly corrugated quarter-pallets and lightweight, recycled-plastic variants that reduce material use and transportation emissions. Common applications include snack foods, confectionery, personal care items, and seasonal impulse products positioned near checkout areas or high-traffic aisles.

Retailers adopting quarter pallet formats report faster setup times, improved inventory turnover, and greater merchandising flexibility, contributing to above-average growth rates for this segment.

Material Type Insights

Corrugated and paperboard materials are expected to dominate the market, accounting for approximately 56.7% of the revenue share in 2026. Their widespread adoption is supported by low material costs, ease of customization, and strong recyclability, making them ideal for one-way and short-duration promotional displays.

These materials are commonly used in food and beverage promotions, seasonal retail campaigns, and limited-time product launches, where rapid deployment and simple disposal are key considerations.

Corrugated display pallets also enable high-quality printing and branding, allowing manufacturers to integrate promotional messaging directly onto the pallet structure. The increasing use of post-consumer recycled fiber and water-based inks has further improved their environmental profile, aligning with retailers' sustainability commitments. As a result, corrugated and paperboard pallets remain the preferred choice for high-volume, cost-sensitive promotional applications.

Plastic display pallets, particularly those manufactured from polypropylene and high recycled-content resins, are expanding rapidly due to their durability, moisture resistance, and suitability for reusable and pooled applications. These pallets maintain structural integrity in cold-chain, high-humidity, and outdoor retail environments, making them well-suited for beverages, dairy products, and garden or home-improvement categories.

Plastic pallets are increasingly adopted in multi-cycle promotional programs and pallet pooling systems, where repeat usage reduces total lifecycle cost despite higher upfront pricing. Their dimensional consistency and compatibility with automated handling and robotic systems also support deployment in advanced distribution centers.

As retailers and manufacturers place greater emphasis on reuse, waste reduction, and operational efficiency, plastic display pallets are gaining traction as a long-term alternative to single-use materials.

Regional Insights

North America Display Pallets Market Trends - Retail Promotion Intensity and Reusable Pallet Pooling Adoption

North America is projected to lead the market with a 37.2% market share in 2026, supported by a highly developed retail ecosystem, the dominance of large-format stores, and sophisticated pallet pooling infrastructure. The U.S. accounts for the majority of regional demand, driven by high promotional intensity across mass merchants, warehouse clubs, and grocery chains.

Retailers such as Walmart, Costco, and Target continue to rely heavily on full-pallet and quarter-pallet displays for seasonal and high-velocity product promotions, reinforcing consistent baseline demand.

The region has seen accelerated adoption of pooled and reusable plastic display pallets, led by providers such as CHEP (Brambles Group) and PECO Pallet, which have expanded reusable pallet and display-ready solutions aligned with closed-loop logistics models.

At the regulatory level, evolving extended producer responsibility (EPR) frameworks in U.S. states such as California, Maine, and Oregon are reinforcing demand for recyclable and reusable display materials.

In response, manufacturers are investing in automation-compatible designs, RFID-enabled pallets, and digitally integrated display planning tools, enabling tighter coordination between merchandising execution and distribution efficiency across North American retail supply chains.

Europe Display Pallets Market Trends - PPWR-Driven Shift to Fiber-Based and Recyclable Display Pallets

Europe represents a mature yet innovation-driven display pallets market, characterized by early adoption of recyclable materials and strong regulatory alignment across member states. Germany, the U.K., France, and Spain remain the core demand centers, supported by highly organized retail networks and strict packaging sustainability mandates.

The implementation of the EU Packaging and Packaging Waste Regulation (PPWR) has accelerated the shift toward fiber-based, recyclable, and lightweight display pallet solutions, replacing mixed-material and non-recyclable formats.

Leading packaging producers such as Smurfit Kappa, DS Smith, and Mondi have invested in advanced corrugated engineering, reinforced paperboard pallet designs, and hybrid fiber structures that deliver higher load strength while reducing material consumption.

Major European retailers, including Tesco, Carrefour, Aldi, and Lidl, increasingly specify recyclable display pallets as part of supplier compliance requirements, influencing material selection across the value chain.

Ongoing industry consolidation, including capacity rationalization and cross-border acquisitions among packaging firms, is also reshaping competitive dynamics, improving economies of scale, and concentrating innovation investment in high-performance, regulation-compliant display pallet systems.

Asia Pacific Display Pallets Market Trends - Modern Retail Expansion and Cost-Efficient Corrugated Displays

Asia Pacific is the fastest-growing regional market for display pallets, driven by the rapid expansion of modern retail formats, high manufacturing output, and rising e-commerce penetration.

China holds the largest regional share, supported by massive retail volumes and a dense logistics network serving both domestic consumption and export-oriented supply chains. Large retailers and platforms such as Alibaba (via Cainiao), JD.com, and Sun Art Retail increasingly deploy standardized palletized displays to improve store-level efficiency and reduce manual handling.

India and ASEAN markets are experiencing accelerated growth as organized retail penetration expands through chains such as Reliance Retail, DMart, Lotus’s, and Big C, creating new demand for cost-efficient and easily deployable display pallet formats. The region benefits from cost-competitive corrugated manufacturing capacity, particularly in China, Vietnam, and Indonesia, supporting widespread adoption of paperboard display pallets for promotional use.

Sustainability initiatives, including China’s packaging waste reduction policies and voluntary corporate commitments by multinational FMCG brands, are further influencing material choices. Concurrent investments in warehouse automation, smart packaging, and standardized merchandising systems are expected to sustain above-average growth rates for display pallets across the Asia Pacific.

Competitive Landscape

The global display pallets market combines consolidation among large integrated packaging companies with fragmentation across regional converters and specialized display manufacturers.

Large players dominate high-volume retail contracts, particularly in corrugated displays and pooled pallet systems, while smaller firms focus on custom and seasonal solutions. Recent mergers and acquisitions have increased scale and geographic reach for leading suppliers, intensifying competition at the global level.

Leading companies emphasize innovation in recyclable materials, cost efficiency through pooling and service-based models, and geographic expansion through acquisitions and capacity investments. Speed of deployment, sustainability credentials, and integrated logistics support are key competitive differentiators.

Key Industry Developments

- In April 2025, International Paper Company announced an agreement to acquire DS Smith, a deal aimed at strengthening its global packaging and display pallet capacity and creating a more integrated, sustainable packaging platform.

- In August 2025, CHEP Australia introduced a next-generation FMCG retail display pallet featuring enhanced safety features, anti-slip technology, and compatibility with standard manual-handling equipment to improve logistics and in-aisle deployment.

Companies Covered in Display Pallets Market

- CHEP

- PECO Pallet

- Brambles Group

- DS Smith

- Smurfit Kappa

- Mondi Group

- International Paper

- Georgia-Pacific

- WestRock

- Packaging Corporation of America

- Sonoco Products Company

- IFCO Systems

- ORBIS Corporation

- Rehrig Pacific Company

- Buckhorn (Myers Industries)

- Schoeller Allibert

- TranPak

- UFP Industries

- CABKA Group

- NEFAB Group

Frequently Asked Questions

The global display pallets market is estimated to be valued at US$3.2 billion in 2026.

By 2033, the display pallets market is projected to reach approximately US$4.4 billion.

Key trends include rising adoption of modular quarter and half pallet formats, increasing use of recyclable corrugated and recycled-content plastic materials, expansion of pallet pooling and reusable display systems, and growing integration of display pallets with automation-friendly and omnichannel retail logistics.

Full pallet displays represent the leading product segment, accounting for around 45.4% of total market revenue, driven by their extensive use in high-volume retail promotions and compatibility with standard handling systems.

The display pallets market is expected to grow at a CAGR of 4.8% between 2026 and 2033.

Major players with strong product portfolios include CHEP, International Paper, Smurfit Kappa, Mondi Group, and ORBIS Corporation.