- Display Technologies

- Micro LED Display Market

Micro LED Display Market Size, Share, and Growth Forecast 2026 – 2033

Micro LED Display Market by Product Type (Wearable Displays, Digital Signage, Others), Technology Type (Active Matrix Micro LED, Transparent Micro LED, Others), Application (Consumer Electronics, Automotive Displays, Others), and Regional Analysis 2026 – 2033

Micro LED Display Market Size, Share, and Growth Forecast 2026 – 2033

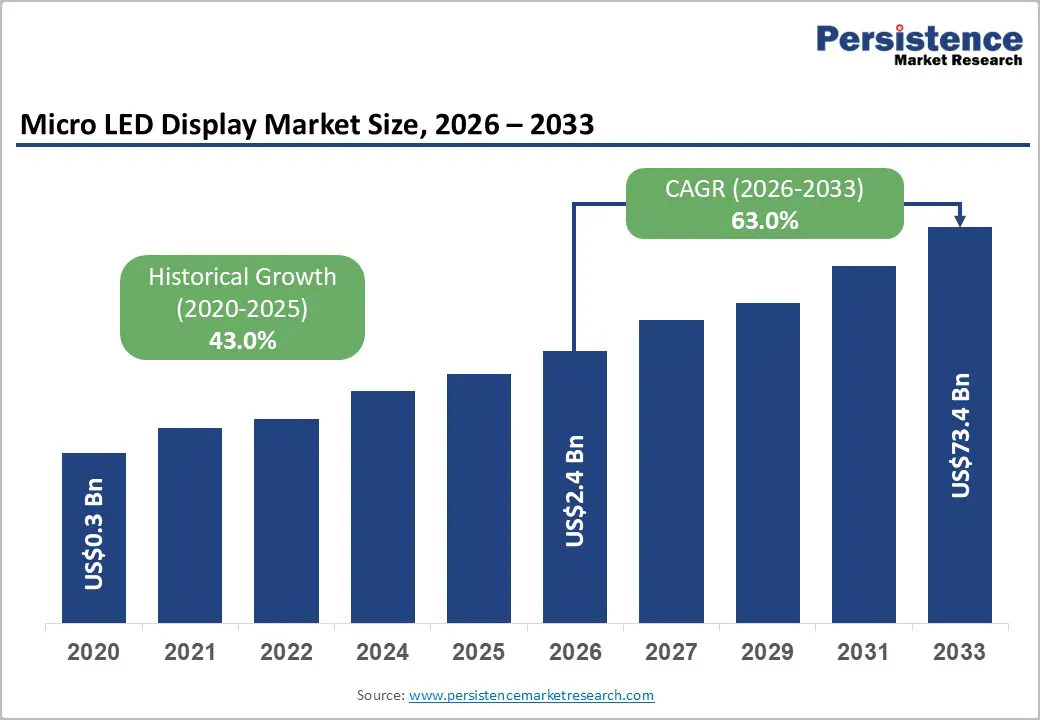

The global micro LED display market size is likely to be valued at US$2.4 billion in 2026 and is projected to reach US$73.4 billion by 2033, growing at a CAGR of 63% during the forecast period from 2026 to 2033, driven by a low adoption base, rapid proof-of-concept validation, and concentrated strategic investments, which inflated momentum during commercialization entry.

As the market evolves, inherent weaknesses such as manufacturing scalability, yield optimization, and capital intensity temper acceleration, while threats from competing display technologies and supply-chain dependencies further stabilize growth. This shift indicates market normalization and maturation rather than diminished demand, with growth increasingly governed by execution efficiency and end-market absorption capacity.

Key Industry Highlights:

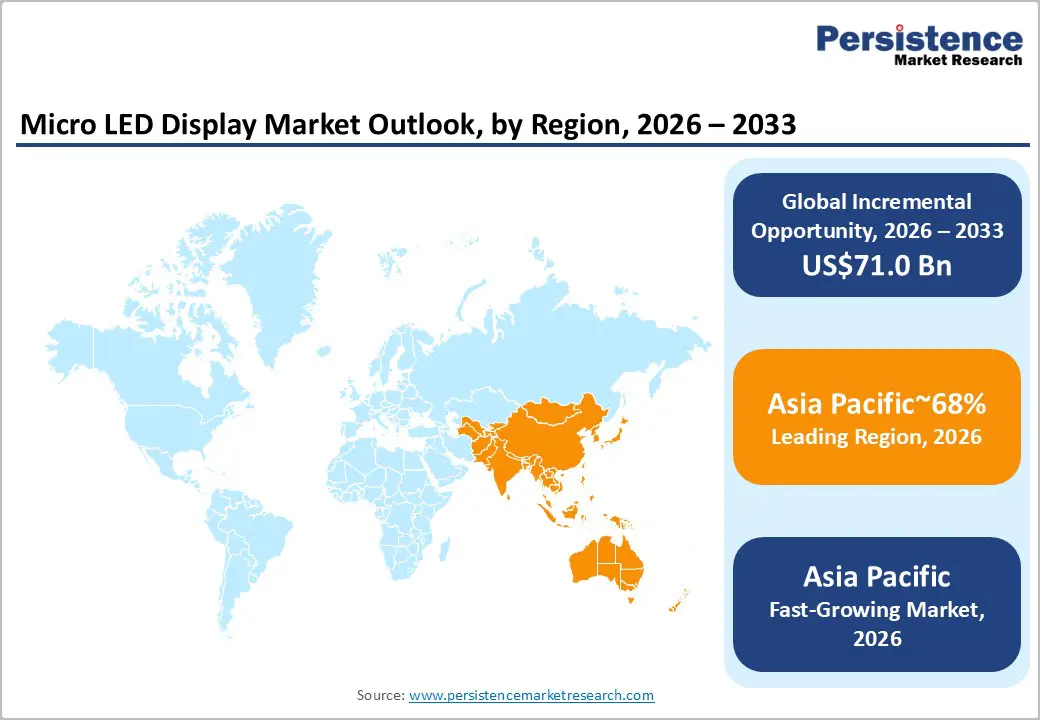

- Leading Region: Asia Pacific is projected to lead due to a deep industrial ecosystem, vertically integrated supply chains, and robust semiconductor infrastructure, accounting for approximately 68% share in 2026, supported by glass-based substrate adoption, modular foundry models, and AI-enhanced manufacturing.

- Fastest-growing Region: Asia Pacific is anticipated to grow the fastest due to rapid adoption in consumer electronics, AR/VR devices, electric vehicles, policy-backed R&D incentives, and consolidation between LED component makers and display giants.

- Leading Technology Type Active Matrix Micro-LED is expected to lead the market, accounting for approximately 66% share in 2026 through high-resolution performance, energy efficiency, seamless integration, and adoption across consumer electronics, automotive, and wearable applications.

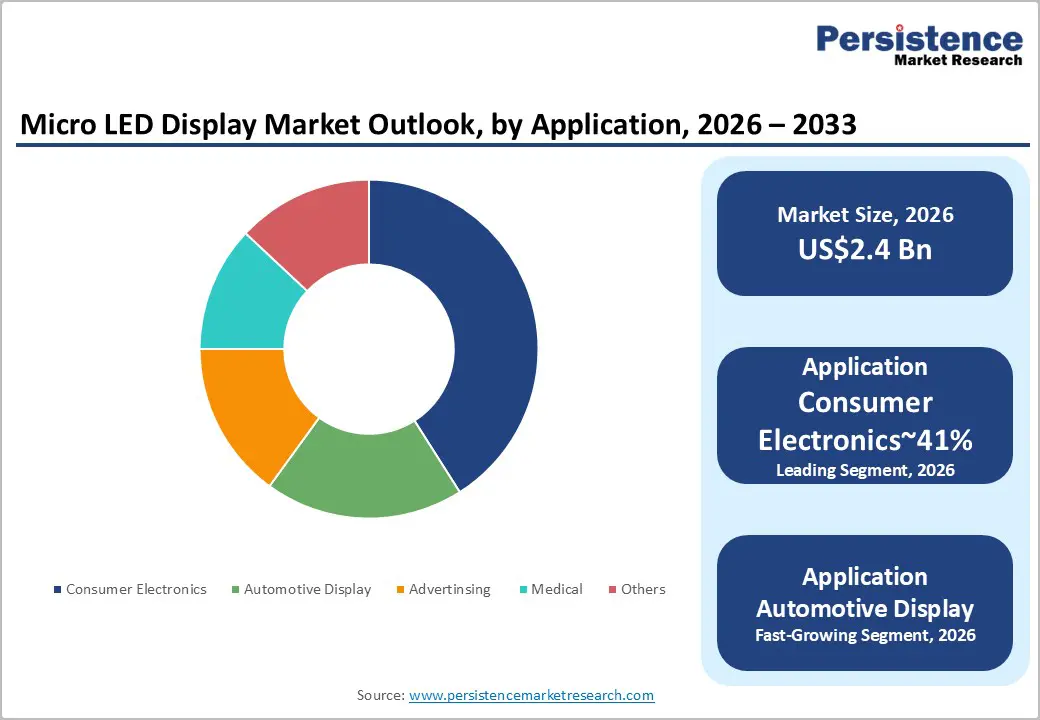

- Leading Application: Consumer electronics is projected to dominate for simplicity, high-value deployment, energy efficiency, and functional use across key sectors, holding approximately 42% share in 2026, driven by the replacement of OLED in premium televisions, wearables, and smartphones.

| Key Insights | Details |

|---|---|

|

Micro LED Display Market Size (2026E) |

US$2.4 Bn |

|

Market Value Forecast (2033F) |

US$73.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

63% |

|

Historical Market Growth (CAGR 2020 to 2025) |

43% |

Market Factors –Growth, Barriers, and Opportunity Analysis

Growth Analysis – Emerging Applications in Transparent and Flexible Displays

The expansion of transparent micro LED technology into non-traditional display environments is emerging as a powerful market driver. Unlike conventional display technologies, Micro LEDs enable high optical transparency while maintaining strong luminance and durability, making them well-suited for integration into architectural glass, retail storefronts, transportation interiors, and automotive glazing. These capabilities support entirely new use cases such as interactive shop windows, information overlays in public transit, and augmented vehicle side windows, where visibility and design integration are critical. As a result, demand is shifting beyond consumer electronics toward infrastructure, mobility, and commercial design applications.

This transition materially alters the competitive landscape of the display market. By targeting specialized, application-driven deployments, manufacturers can reduce exposure to commoditized consumer segments and their associated price pressures. Transparent and flexible displays also attract buyers focused on functionality, customization, and long-term value rather than unit cost alone. As adoption expands across retail, urban infrastructure, and smart mobility projects, these emerging applications act as a structural growth engine, supporting higher margins and encouraging sustained investment while the core display technology continues to mature. In July 2024, VueReal Inc. and RiTdisplay Corp announced a strategic partnership to enable access to advanced micro-LED displays. The collaboration combines high performance, low power consumption, and high transparency, creating opportunities for OEMs in consumer electronics, wearables, and automotive applications.

Barrier Analysis – Mass Transfer Alignment Precision Limits

Mass transfer alignment remains one of the most critical structural restraints in micro LED manufacturing, directly constraining scalability and cost efficiency. The process requires extreme placement precision during the transfer of microscopic emitters from donor wafers onto target backplanes, where even minor deviations can result in pixel defects, yield losses, or display non-uniformity. This challenge is amplified in heterogeneous integration environments, where differences in material properties between substrates introduce instability during high-throughput operations. As panel sizes increase, maintaining consistent alignment across the entire surface becomes exponentially more difficult, limiting reliable expansion into large-format consumer displays.

Thermal expansion mismatches further intensify this constraint by causing positional drift during processing, particularly under high-speed, high-volume manufacturing conditions. These effects force manufacturers to rely on complex and capital-intensive corrective techniques, such as laser-assisted transfer and real-time alignment compensation, which significantly increase production complexity and costs. As a result, mass transfer precision acts as a fundamental bottleneck rather than a solvable efficiency issue, delaying commercialization timelines and reinforcing barriers to entry for new players while slowing broader market adoption.

Opportunity Analysis – Convergence with Wearable Health Monitoring

The convergence of micro LED display technology with advanced biometric sensing represents a high-impact opportunity within next-generation wearable devices. Micro LEDs’ inorganic structure enables tighter integration with embedded sensors, allowing biometric components to be placed directly beneath or between pixels without compromising luminance, lifespan, or color stability. This structural advantage over organic display technologies enables full-screen sensing architectures, including under-display imaging and continuous biometric tracking, while preserving display clarity and durability.

This opportunity is especially pronounced in smartwatches and medical-grade wearables, where device size constraints and reliability requirements are most acute. By combining high-visibility displays with integrated health diagnostics, manufacturers can deliver multifunctional devices that support both real-time communication and continuous physiological monitoring. Such convergence directly addresses unmet demand for compact, clinically relevant wearables capable of long-duration use without performance degradation. As healthcare systems increasingly shift toward remote monitoring and preventative care, Micro LED-enabled wearables offer a credible pathway to accelerated adoption in regulated health and wellness applications. In September 2025, AUO and Garmin collaborated on the f-nix 8 Pro, the world's first Micro-LED smartwatch. Featuring a 1.4-inch panel with 326 PPI, high brightness, and durability, this marks a milestone in wearables, driving consumer interest in premium micro LED devices.

Category–wise Analysis

Technology Insights

Active matrix (AM) is expected to lead the market, accounting for approximately 66% share in 2026, underpinned by its entrenched role in delivering high-resolution, high-performance displays across consumer electronics, automotive, and wearable devices. Adoption remains anchored by pixel-level control, extreme luminance, and energy efficiency, with providers prioritizing operational advantages such as seamless integration and optimized battery performance in AR/VR headsets and smartwatches. Brands like Samsung Electronics, LG Electronics, and AUO Corp., along with innovators such as Jade Bird Display and PlayNitride, are expanding their ecosystems, locking in workflows, and demonstrating technological leadership. This combination of mature infrastructure, ecosystem integration, and predictable demand sustains Active Matrix’s dominance within structured deployment models.

Transparent Micro-LED is expected to be the fastest-growing segment market, driven by emerging needs for high-transparency, bright, and energy-efficient displays across automotive HUDs, AR wearables, and retail vitrines. Growth is being catalyzed by chip-on-glass substrates, invisible wiring, and hybrid interactive glass, which materially improve clarity, interactivity, and thermal management. Samsung Electronics, Jade Bird Display, and Innolux are actively deploying transparent Micro-LED platforms into automotive, consumer, and architectural use cases to capture early-cycle demand and embed switching advantages. As vehicle safety standards, energy efficiency mandates, and military display requirements align, this segment is projected to outpace overall market growth over the forecast period.

Application Insights

Consumer electronics are anticipated to lead the market, accounting for approximately 42% share in 2026, underpinned by their entrenched role in replacing OLED across premium televisions, wearables, and smartphones. Adoption remains anchored by energy efficiency, long lifespan, and superior outdoor visibility, with providers prioritizing operational advantages such as modular form factors, AI-enhanced pixel driving, and hybrid QD-MicroLED integration in high-volume production lines. Ongoing platform evolution, including flexible and rollable substrates, 4K/8K resolution panels, and low-blue-light hardware integration, continues to reinforce replacement cycles and consumer adoption. Brands such as Samsung Electronics, LG Electronics, Sony Corporation, Garmin, and Apple Inc. are expanding their product portfolios, locking in ecosystems and demonstrating technological leadership.

Automotive displays are expected to be the fastest-growing segment in the micro LED display market, driven by emerging needs for high-brightness, resilient, and flexible displays across dashboards, head-up displays, and interactive smart windows. Growth is being catalyzed by transparent and curved panel designs, haptic integration, and extreme luminance capabilities, which materially improve visibility, safety, and user interaction. Continental AG, LG Display, AUO Corporation, and Jade Bird Display are deploying advanced micro LED platforms into luxury and electric vehicles to capture early-cycle demand and embed switching advantages. As regulatory visibility and energy-efficiency requirements align, this segment is projected to outpace overall market growth over the forecast period.

Regional Insights

Asia Pacific Micro LED Display Market Trends

Asia Pacific is expected to remain the leading market for micro-LED displays, accounting for approximately 68% of global revenue in 2026, underpinned by its deep industrial ecosystem, vertically integrated supply chains, and robust semiconductor infrastructure. The region’s dominance is anchored in full-stack production capabilities, spanning epitaxial wafer fabrication, backplane assembly, and mass-transfer equipment deployment, while government-backed R&D incentives and subsidies further strengthen technological leadership. Demand is projected to be driven by the rapid adoption of consumer electronics, AR/VR devices, and electric vehicles, with firms leveraging glass-based substrates, modular foundry models, and AI-enhanced manufacturing to optimize yield and performance. Consolidation between LED component makers and display giants, alongside strategic deployment of large-format TVs and automotive dashboards, is likely to reinforce Asia Pacific’s structural advantage.

Asia Pacific is also the fastest-growing region. Taiwan is positioned to anchor Asia Pacific’s micro-LED momentum, shaping regional growth through automated 6-inch production lines, high-skilled labor availability, and cost-efficient cleanroom operations. The country’s regulatory frameworks, including the Display Innovation Act, standardize transfer yield metrics and ensure product safety, enabling vendors such as AUO, Innolux, and PlayNitride to scale output efficiently. Strategic investment flows from Taiwan, coupled with proximity to consumer electronics assembly hubs across China and South Korea, facilitate rapid technology adoption and reduced time-to-market for premium displays. Forward-looking initiatives, including integration of glass-based CoG substrates and localized mass-transfer tool development in response to export controls, are expected to sustain Asia Pacific’s combined dominance and accelerated growth trajectory in the Micro-LED display ecosystem.

Europe Micro LED Display Market Trends

Europe is expected to remain a stable and mature market for micro-LED displays, with demand primarily anchored in specialized, high-margin applications rather than mass-production deployment. The region’s positioning is reinforced by its concentration on premium automotive dashboards, defense-grade HUDs, and medical imaging displays, where performance, reliability, and precision are prioritized over volume. Core drivers include integration of Micro-LEDs into luxury vehicles, minimally invasive surgical monitors requiring exceptional color accuracy, and defense optics capable of withstanding extreme operational conditions. Leading technology and integration providers such as ams OSRAM, Porotech, Continental AG, and STMicroelectronics continue to reinforce Europe’s role as a specialized application hub.

Germany is positioned to anchor Europe’s Micro-LED momentum, shaping regional stability through automotive OEMs such as BMW, Mercedes-Benz, and Audi, which drive structural demand for dashboards and exterior digital lighting. Investments in R&D centers, wafer-level integration, and industrial partnerships enable German firms to lead innovation in GaN-on-Si and modular panel architectures, while maintaining predictable revenue streams. Forward-looking strategies, including smart architecture applications and privacy-filtered display technologies, are expected to sustain Europe’s structural stability, preserving high unit ASPs and enterprise-grade adoption despite slower consumer-scale growth relative to Asia Pacific and North America.

North America Micro LED Display Market Trends

North America is expected to remain a mature and structurally stable market for Micro-LED displays, with demand primarily anchored in replacement cycles, high-end adoption, and enterprise optimization rather than large-scale greenfield manufacturing. The region’s position is reinforced by deep expertise in system integration, R&D capabilities, and high-value deployment across defense, aerospace, and premium consumer electronics sectors. Forward-looking adoption is likely to be shaped by hybrid bonding techniques, scalable pilot modules for AR/VR wearables, and advanced microdisplay interconnects, supporting operational excellence and long-term system performance. Leading technology and display providers such as Apple Inc., Meta, VueReal Inc., and Kopin Corporation continue to define high-end benchmarks and sustain North America’s strategic role in innovation-led Micro-LED adoption.

The U.S. is positioned to anchor North America’s market stability, driving regional momentum through government-backed initiatives under the CHIPS and Science Act, which accelerate domestic microdisplay fabs in Arizona, Texas, and New York. Military and aerospace contracts, exemplified by Kopin Corporation’s soldier-worn HUD programs, reinforce structural demand and adoption of high-performance Micro-LEDs. Premium consumer segments continue to prioritize brightness, energy efficiency, and AR/VR integration, supporting scalable pilot production and hybrid bonding deployments. Forward-looking investment in automation and high-throughput assembly, alongside proximity to leading chip and AI infrastructure, is expected to maintain North America’s mature positioning.

Competitive Landscape

The global micro LED display market is moderately consolidated, with leadership concentrated among Tier 1 display giants, APAC-based foundries, and IP-rich technology disruptors such as Samsung Electronics, LG Display, Sony Corporation, AUO, BOE Technology, PlayNitride, Jade Bird Display, and VueReal. These leaders shape the market by defining functional benchmarks, controlling critical technology platforms, and influencing procurement and adoption patterns across premium consumer, automotive, and industrial applications. Tier 1 companies exert strong downstream influence through global distribution networks and brand equity, while foundries secure the upstream supply of LED chips, backplanes, and mass-transfer processes.

Competitive positioning varies by specialization – display giants pursue vertical integration and modular production models, foundries focus on high-volume cost optimization, and IP disruptors leverage proprietary processes to capture niche AR/VR and microdisplay applications. Industry behavior demonstrates active ecosystem consolidation, with partnerships like AUO-PlayNitride-Garmin sharing development risk and accelerating platform evolution. Yield optimization remains the primary battleground, supported by equipment providers such as Coherent and Kulicke & Soffa, while capital intensity and dense patent portfolios create high barriers to entry, preserving leadership advantages for established players.

Key Industry Developments:

- In February 2026, LG Display achieved the industry’s first 100% Dimming Consistency verification for its pixel-level control technology. This validation confirms OLED’s superiority over Mini-LED by ensuring perfect brightness and eliminating light bleeding in high-contrast scenarios.

- In January 2026, Samsung Electronics unveiled the world's first 130-inch Micro RGB TV (R95H) at CES 2026, featuring next-generation AI processing. The launch establishes a new "ultra-premium" category, utilizing sub-100μm LEDs to achieve 100% of the BT.2020 color gamut. Samsung's R95H signifies the transition of micro LED technology into a consumer-ready, ultra-premium market by delivering 100% BT.2020 color accuracy.

Companies Covered in Micro LED Display Market

- Samsung Electronics Co., Ltd.

- Sony Corporation

- AUO Corporation

- BOE Technology Group Co., Ltd.

- PlayNitride Inc.

- LG Display

- Epistar Corporation

- Apple Inc.

- Rohinni LLC

- VueReal Inc.

- Plessey Semiconductors

- JBD (Jade Bird Display)

- Innolux Corp.

- Aledia SA

- Raxium

- Japan Display Inc.

- Lumens Co. Ltd.

Frequently Asked Questions

The demand for micro LED displays is surging due to their high resolution, energy efficiency, durability, and suitability for various applications.

Some of the key players operating in the market are LG Electronics., Samsung Electronics Co., Ltd., Sony Corporation, and Groupe Atlantic.

Lighting Insights segment recorded the significant market share.

A compelling opportunity in the micro LED display market is the integration of micro LEDs into automotive displays, enhancing durability, brightness, and high-resolution visuals for infotainment systems, and heads-up displays.

Asia Pacific to account for the significant share in the market.