- Display Technologies

- Near-Eye Display Market

Near-Eye Display Market Size, Share, and Growth Forecast, 2025 - 2032

Near-Eye Display Market By Device Type (Augmented Reality (AR) Devices, Virtual Reality (VR) Devices, Others), Display Technology (Micro-OLED/OLED, Liquid Crystal on Silicon (LCOS), Others), Resolution, Application, and Regional Analysis for 2025 - 2032

Near-Eye Display Market Size and Trends Analysis

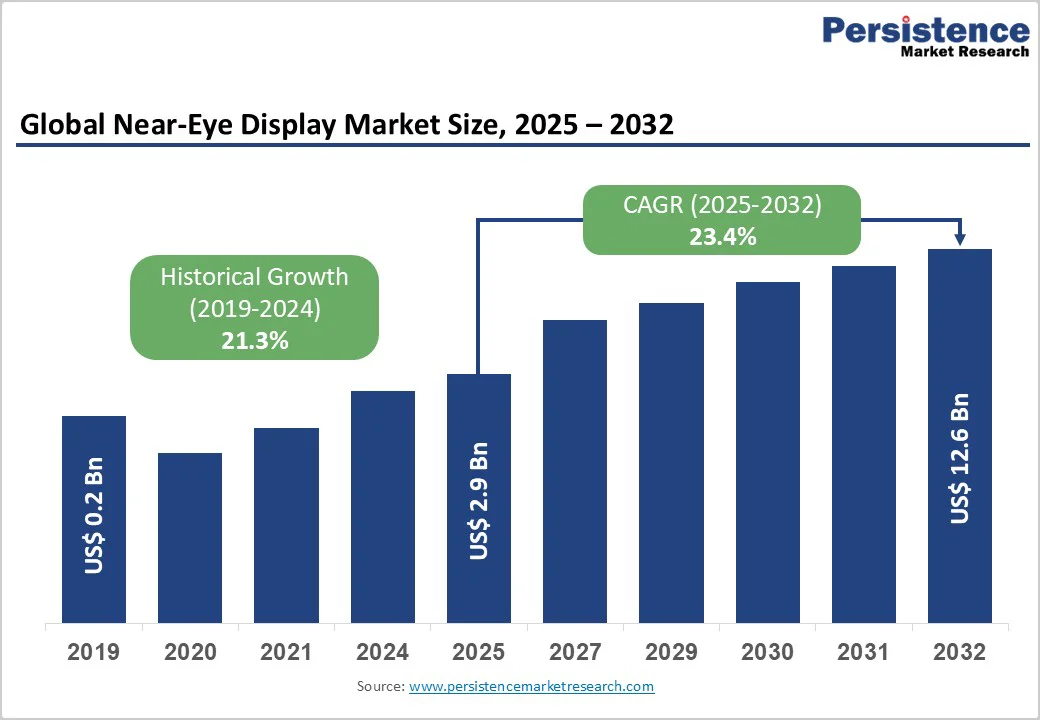

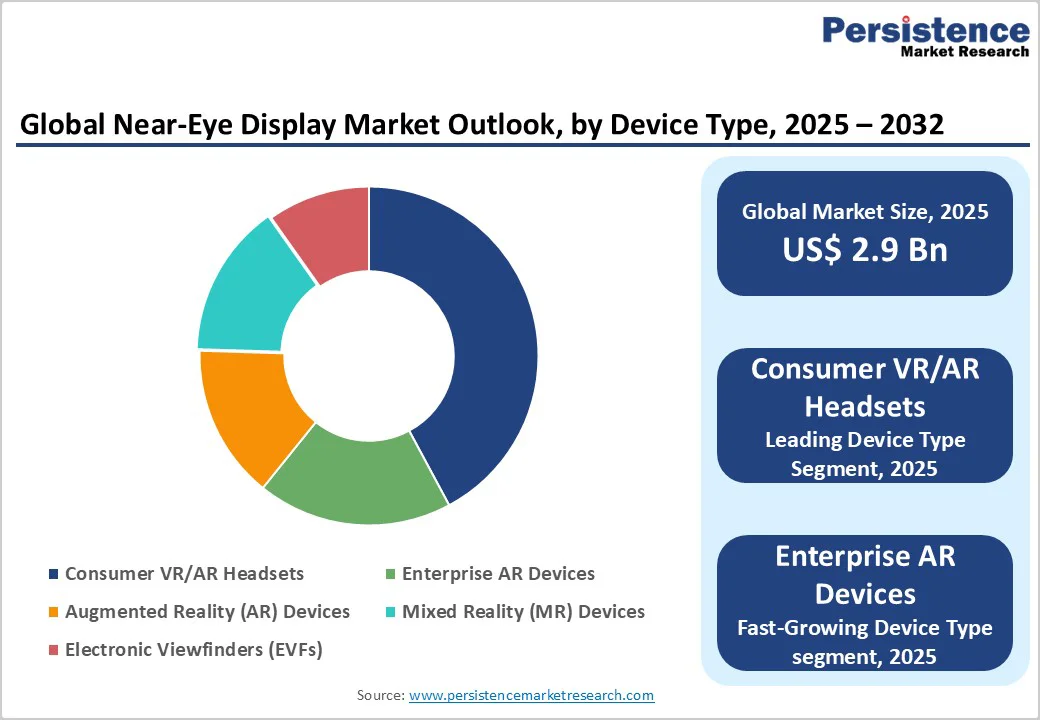

The global near-eye display market size is likely to be valued at US$2.9 Billion in 2025 and is expected to reach US$12.6 Billion by 2032, growing at a CAGR of around 23.4% during the forecast period from 2025 to 2032, driven by the accelerating adoption of AR/VR/MR headsets across consumer, enterprise, and defense sectors.

Advances in micro-OLED and waveguide optics have produced lighter, brighter, and more energy-efficient headsets. Rising consumer demand and mature supply chains are driving multi-year market growth.

Key Industry Highlights

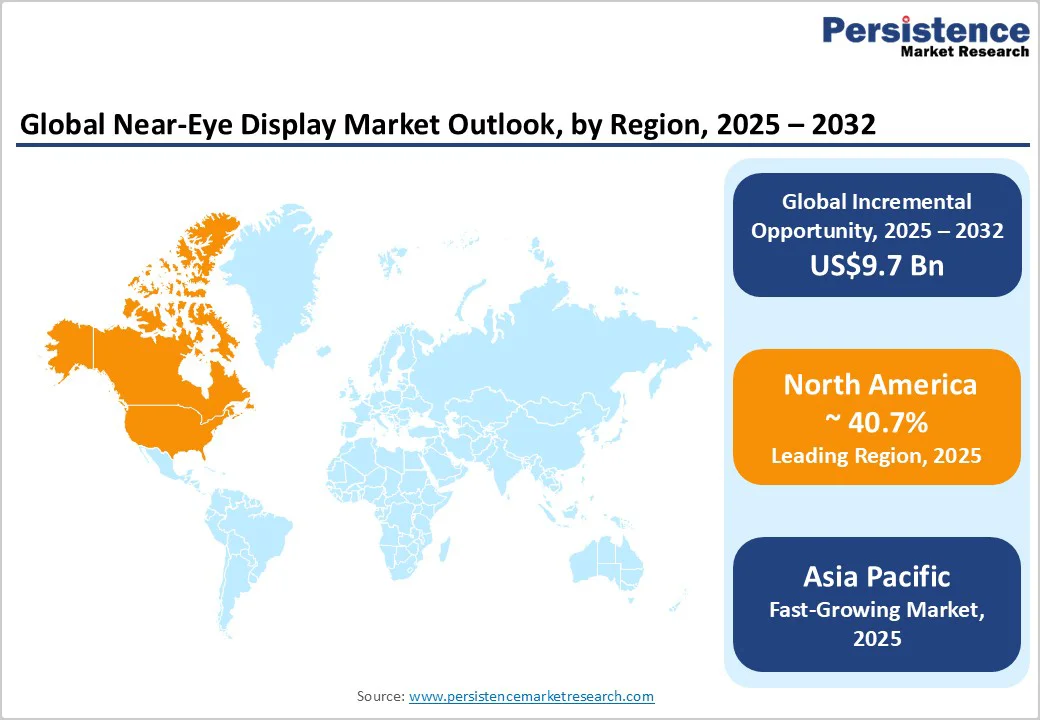

- Leading Region: North America accounts for 40.7% of the global market revenue in 2025, driven by strong consumer adoption of premium mixed-reality headsets and robust enterprise digitalization initiatives.

- Fastest-Growing Region: Asia Pacific is supported by large-scale micro-OLED and MicroLED manufacturing capacity and surging demand across gaming, education, and industrial applications.

- Investment Plans: Between 2024 and 2026, major display manufacturers announced capacity expansions exceeding US$1.5 Billion to boost micro-display production and lower component costs through vertical integration.

- Dominant Device Type: Consumer AR/VR Headsets represent approximately 43.5% of total market revenue, fueled by immersive entertainment, gaming, and spatial computing trends.

- Leading Display Technology: Micro-OLED Display Technology holds the largest technology share at nearly 55.6%, favored for its high brightness, pixel density, and compactness in premium headsets.

| Key Insights | Details |

|---|---|

| Near-Eye Display Market Size (2025E) | US$2.9 Bn |

| Market Value Forecast (2032F) | US$12.6 Bn |

| Projected Growth (CAGR 2025 to 2032) | 23.4% |

| Historical Market Growth (CAGR 2019 to 2024) | 21.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Micro-OLED Adoption and Display Miniaturization

Micro-OLED, or OLED-on-Silicon, has become the dominant technology for near-eye applications due to its superior resolution, brightness, and power efficiency. High-volume platform launches in 2024 - 2025 accelerated supplier investments in micro-OLED capacity.

These displays achieve very high pixel density while maintaining compact form factors, addressing the ergonomic limitations of earlier generations. As yields improve and wafer costs fall, per-unit display prices are declining, expanding affordability for mainstream devices. The resulting economies of scale support both lower-cost consumer products and higher-performance professional systems, strengthening the industry’s overall growth trajectory.

Platform Launches and Ecosystem Pull

Recent product launches by leading technology firms marked a turning point for the near-eye display sector. Flagship headset introductions in 2024 demonstrated the viability of spatial computing and immersive content experiences, creating significant downstream demand for high-resolution displays, waveguides, and supporting components.

The success of these platforms stimulated broader content creation, enhancing ecosystem value and encouraging additional hardware adoption. OEMs are now forming long-term supply agreements and expanding production capacity to ensure continuity, which in turn provides suppliers with predictable demand visibility and stable capital-investment conditions.

Enterprise and Defense Demand

Beyond consumer entertainment, demand is expanding rapidly within enterprise, defense, and medical environments. Organizations are deploying near-eye systems for simulation, remote assistance, maintenance, and surgical visualization.

Defense programs, in particular, are investing in ruggedized optics and high-brightness displays to enhance situational awareness. This segment provides steady, high-margin revenue streams and extends product lifecycles through specialized certification and support requirements. The resulting diversification of end-use sectors stabilizes overall market performance and mitigates reliance on cyclical consumer spending.

Barrier Analysis - Component Cost and Manufacturing Scale

Despite technological progress, near-eye display production remains cost-intensive. High-precision bonding of micro-displays, driver ICs, and waveguides requires advanced fabrication processes with limited yield at scale. Component costs can represent more than a quarter of a headset’s total bill of materials, constraining price reductions in the consumer market.

Significant capital investment is needed to expand capacity and achieve cost parity with mature display formats. The payback period for these facilities is often long, which can delay market penetration among price-sensitive segments.

Regulatory and Optical Safety Challenges

Products designed for near-eye use must comply with stringent optical-safety and exposure standards. Devices intended for clinical or defense purposes also require separate certification procedures, adding time and expense to commercialization.

European medical regulations, U.S. safety testing standards, and local certification frameworks increase the pre-market workload for vendors. These factors lengthen approval cycles, raising barriers to entry for smaller manufacturers and delaying new product introductions.

Opportunity Analysis - Low-Cost Microdisplay Lines and Vertical Integration

The next major opportunity lies in reducing micro-display production costs through dedicated fabrication lines and vertically integrated supply chains. As manufacturing capacity expands, economies of scale are expected to reduce unit prices by as much as half, enabling wider adoption among mid-range consumer headsets.

This shift could expand the total addressable market by several billion dollars over the next decade. Integration of display, optics, and driver technologies within a single production ecosystem also allows suppliers to capture greater value and improve quality control.

Convergence with AI and Mixed-Reality Software Ecosystems

Embedding artificial intelligence in near-eye systems enables advanced features such as eye-tracking, foveated rendering, and real-time contextual overlays. These functions reduce processing load, extend battery life, and create more natural user experiences.

The growing availability of AI-driven software platforms is transforming near-eye hardware from standalone devices into intelligent computing environments. This convergence supports new monetization models through enterprise software subscriptions, cloud-linked spatial content, and professional training applications.

Category-wise Analysis

Device Type Insights

Consumer VR/AR headsets accounted for the largest share of the market, driven by strong demand for immersive gaming, media consumption, and personal computing experiences. The segment represented approximately 43.5% of the total revenue, supported by continuous product refresh cycles and a growing software ecosystem.

The success of premium mixed-reality devices has spurred further innovation in display brightness, resolution, and ergonomic design. Shorter replacement cycles among early adopters sustain high unit volumes, creating scale advantages for leading OEMs.

AR devices designed for enterprise operations are expanding at the fastest rate, supported by measurable improvements in productivity and safety. Industries such as logistics, field maintenance, and manufacturing are using AR systems for hands-free workflows and real-time information overlays.

These deployments often involve bulk orders and long-term contracts, creating predictable revenue for suppliers. Strong return-on-investment metrics and the integration of AR into digital-twin environments are expected to sustain above-average CAGR for this segment through 2032.

Display Technology Insights

Micro-OLED technology leads the near-eye display market due to its high resolution, contrast, and compactness, with a market share of 55.6%. It enables vivid imagery while consuming minimal power, making it ideal for both consumer and professional headsets.

Continuous improvements in pixel density and brightness are extending its dominance across multiple device classes. Key suppliers have scaled production to meet growing orders, with design roadmaps targeting improved lifetime and efficiency. As a result, micro-OLED remains the preferred display architecture for premium mixed-reality devices.

MicroLED and laser beam-scanning (LBS) technologies represent the most disruptive growth opportunity. MicroLED offers exceptional brightness, durability, and efficiency, ideal for outdoor and industrial AR environments. Pilot production lines are already demonstrating performance advantages over OLED, though yield improvements are still required for mass adoption.

LBS displays, meanwhile, provide a lightweight alternative capable of generating large perceived images from compact optical engines. Both technologies are projected to expand rapidly as production techniques mature, potentially redefining the performance ceiling for near-eye systems.

Application Insights

The consumer electronics segment remains the largest end-use category, accounting for more than 40% of the global market revenue in 2024. Growth is driven by entertainment, gaming, and personal computing applications, where immersive displays have become central to user engagement.

Frequent product refresh cycles and continuous software updates encourage repeat purchases. High-profile launches in 2024 broadened consumer awareness, elevating display specifications such as resolution and field of view to new standards.

Enterprise and industrial deployments are expanding faster than consumer use in percentage terms, driven by tangible gains in operational efficiency. Applications include warehouse management, assembly training, and remote technical support.

Enterprises typically purchase in bulk and require enhanced durability and service packages, increasing average selling prices. These deployments also create recurring revenue streams from software licensing and data-management services, making this vertical a strategic growth area for both hardware manufacturers and integrators.

Regional Insights

North America Near-Eye Display Market Trends - Innovation Ecosystem and Enterprise Digital Transformation Leadership

North America accounted for nearly 40.7% of global market revenue, making it the largest regional market. The U.S. dominates regional adoption, supported by a strong innovation ecosystem, early consumer uptake, and advanced enterprise digitization programs.

Canada contributes specialized suppliers in optics and industrial integration. Early product launches and extensive marketing networks have built strong brand recognition for mixed-reality devices. Widespread investments in digital transformation across logistics, manufacturing, and defense continue to drive enterprise adoption.

Regulatory structures in North America are differentiated by use case: consumer devices follow standard electronics guidelines, while medical or defense systems undergo specific certification processes. This combination of flexible consumer rules and stringent professional standards allows for both rapid retail rollouts and safe specialized use.

The competitive environment is characterized by the presence of leading OEMs, content developers, and component suppliers. Although most microdisplay production occurs in Asia, North America houses a dense network of design, software, and system integration firms. Investment activity remains strong, with companies expanding microdisplay capacity and forming strategic alliances to secure critical component supply.

Recent product releases have stimulated a wave of follow-on investment, as suppliers move to match growing demand from new headset platforms. The region’s combination of venture capital availability, technology leadership, and large addressable market will continue to sustain its dominant position.

Europe Near-Eye Display Market Trends - Industrial and Healthcare Integration Driving Regulated Growth

Europe is a key growth region, with Germany, the U.K., France, and Spain being the primary markets. Germany leads in industrial simulation and automotive applications; the U.K. hosts a robust ecosystem of extended-reality software studios; and France and Spain are expanding their presence in healthcare and tourism-based immersive experiences.

Growth is primarily supported by industrial digitization initiatives and the adoption of AR/VR systems in manufacturing, maintenance, and training. The healthcare sector is emerging as another strong demand driver, using near-eye displays for surgical planning and medical education.

The regulatory framework in Europe, while harmonized under CE standards, imposes additional obligations for devices classified as medical equipment. Companies targeting healthcare applications must incorporate compliance planning early in product development to minimize delays. Non-medical consumer products, however, continue to follow standard electronics safety requirements.

Europe’s competitive advantage lies in optics engineering, precision manufacturing, and industrial integration. Numerous mid-sized firms supply components and modules to global OEMs. Partnerships between optics and software specialists are accelerating, and European research programs are supporting local pilot production lines.

Investment opportunities are expanding in certified medical-grade systems and industrial pilot conversions, aided by public-private funding initiatives.

Asia Pacific Near-Eye Display Market Trends - Manufacturing Dominance and Rapid Technology Scaling

Asia Pacific serves as the principal manufacturing hub for near-eye displays and is expected to post the fastest regional growth rate. China dominates the production of panels and optics, while Japan provides leadership in microdisplay and precision optics R&D.

South Korea and Taiwan contribute significant expertise in backplane and driver IC technologies, ensuring a complete supply chain ecosystem. Regional growth is being driven by rapid capacity expansion in micro-OLED fabrication and early pilot lines for MicroLED production. Local suppliers benefit from cost advantages and shorter lead times, while domestic demand for AR/VR systems is expanding across gaming, education, and industrial applications.

Regulatory frameworks differ by country but generally favor consumer electronics development. Some export restrictions and component-sourcing policies may introduce complexity, though most regional markets remain open to cross-border collaboration. Asia Pacific’s competitive landscape includes both major multinational OEMs and emerging local brands targeting affordable devices.

Significant capital is flowing into new fabrication facilities and materials research aimed at improving yield and brightness. The region’s combination of cost efficiency, technology depth, and consumer scale positions it as the fastest-growing contributor to global market revenues.

Competitive Landscape

The global near-eye display industry is moderately concentrated among display module suppliers, while the broader headset ecosystem remains fragmented. A handful of key players dominate premium micro-OLED supply, while numerous smaller firms specialize in waveguides, optics, and driver electronics. The market rewards vertically integrated manufacturers capable of delivering both display and optical modules.

North America and Asia Pacific together account for the majority of production and innovation activity, although European firms maintain strong positions in specialty optics. Market leaders are pursuing vertical integration of display, optics, and module production to strengthen supply reliability and reduce costs.

Other dominant strategies include software bundling, AI-enabled functionality, and long-term supply partnerships. Differentiation focuses on brightness, field of view, power efficiency, and seamless software ecosystems, while cost leadership is achieved through scaled manufacturing and strategic sourcing.

Key Industry Developments

- In May 2025, Google LLC announced a partnership with Warby Parker and Gentle Monster to develop smart glasses that integrate in-lens displays and augmented reality (AR) features under the Android XR platform, backed by a commitment of up to US $150 million to product development and commercialization.

- In September 2025, Meta Platforms, Inc. unveiled its new “Meta Ray-Ban Display” smart glasses at its annual Connect event, featuring a full-colour waveguide display embedded in the lens and a gesture-control neural wrist-band, priced at US $799 and set to launch on 30th September.

Companies Covered in Near-Eye Display Market

- Sony Group Corporation

- Seiko Epson Corporation

- BOE Technology Group Co., Ltd.

- Apple Inc.

- Himax Technologies, Inc.

- Kopin Corporation

- eMagin Corporation

- MICROOLED SA

- Vuzix Corporation

- LG Display Co., Ltd.

- SeeYA Technology Co., Ltd.

- Yunnan OLiGHTEK Opto-Electronic Technology Co., Ltd.

- HOLOEYE Photonics AG

- Syndiant

- WiseChip Semiconductor, Inc.

- Samsung Display Co., Ltd.

- Innolux Corporation

- Sharp Corporation

- Magic Leap, Inc.

- Northrop Grumman Corporation

Frequently Asked Questions

The global near-eye display market size in 2025 is estimated at US$2.9 Billion, reflecting growing adoption of AR/VR devices and immersive display technologies across consumer and enterprise sectors.

By 2032, the market is projected to reach a value of US$12.6 Billion.

Key trends include integration of micro-OLED and MicroLED technologies, the rise of spatial computing and metaverse ecosystems, and growing investments in lightweight, high-resolution AR/VR headsets for consumer, industrial, and defense applications.

The consumer AR/VR headset segment leads the market, accounting for approximately 43.5% of total revenue, supported by strong demand in gaming, entertainment, and immersive media experiences.

The near-eye display market is expected to grow at a CAGR of 23.4% between 2025 and 2032.

Major players include Sony Corporation, Himax Technologies, Inc., Kopin Corporation, eMagin Corporation, and BOE Technology Group Co., Ltd.