- Hardware & Software IT Services

- Digital Asset Management Market

Digital Asset Management Market Size, Share, and Growth Forecast 2026 - 2033

Digital Asset Management Market by Component (Solution, Service), by Deployment (On-premise, Cloud), Application (Human Resource, Sales & Marketing, IT, Finance and Accounting), Vertical (Government & Public Sector, Healthcare, IT & Telecom, Manufacturing, Retail & eCommerce, Media and Entertainment, Travel and Hospitality, BFSI), by Regional Analysis, 2026 - 2033

Digital Asset Management Size and Trend Analysis

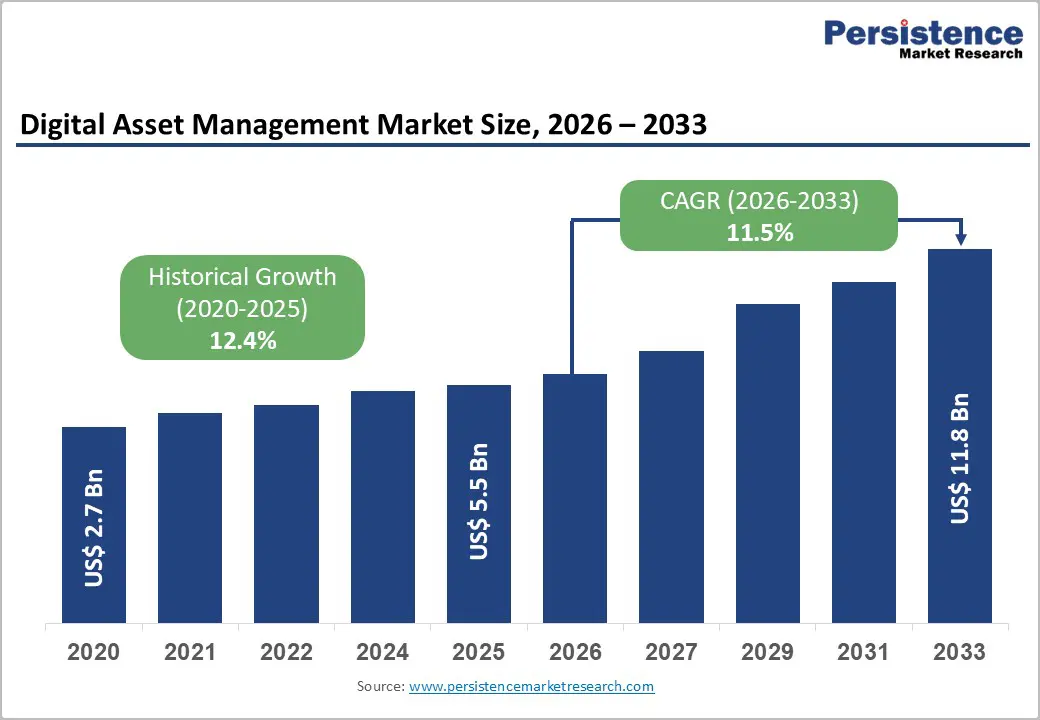

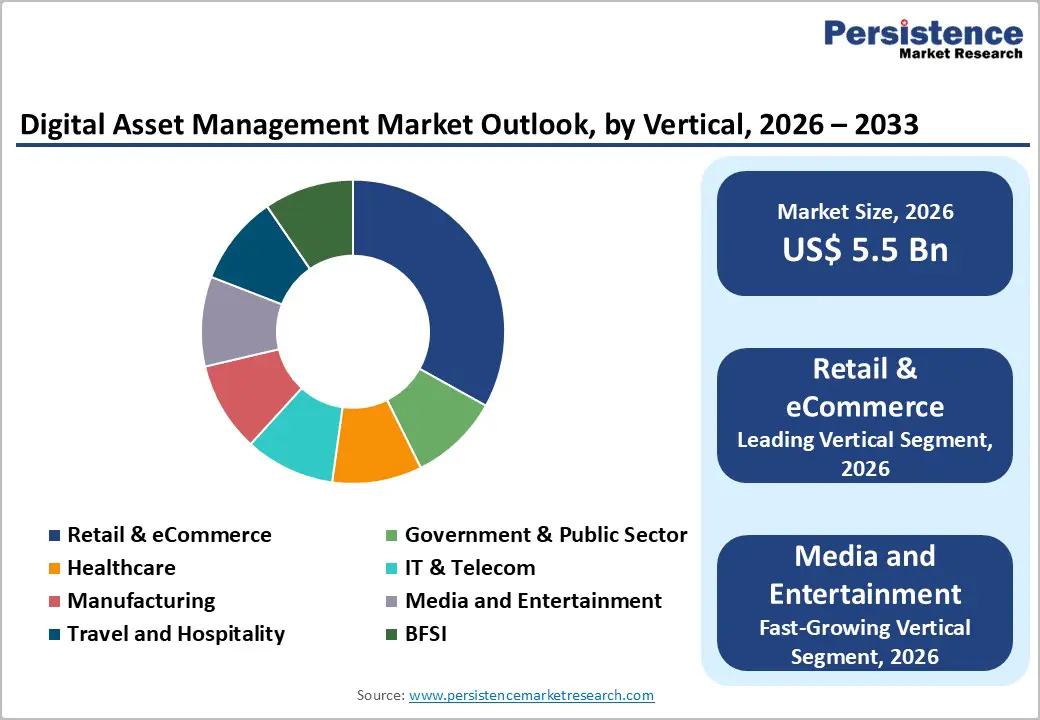

The global digital asset management market size is likely to be valued at US$ 5.5 billion in 2026 and projected to reach US$ 11.8 billion by 2033, growing at a CAGR of 11.5% between 2026 and 2033.

The sustained expansion is driven by exponential growth in digital content creation across enterprises, widespread adoption of cloud-based deployment models, and growing enterprise recognition of Digital Asset Management (DAM) solutions as critical infrastructure for brand consistency and operational efficiency. Organizations are increasingly allocating budget toward centralized content repositories to streamline workflows, reduce time-to-market for campaigns, and ensure regulatory compliance across distributed teams. This strategic shift reflects the fundamental evolution of how enterprises manage their rapidly expanding digital asset portfolios in an omnichannel marketplace.

Key Industry Highlights:

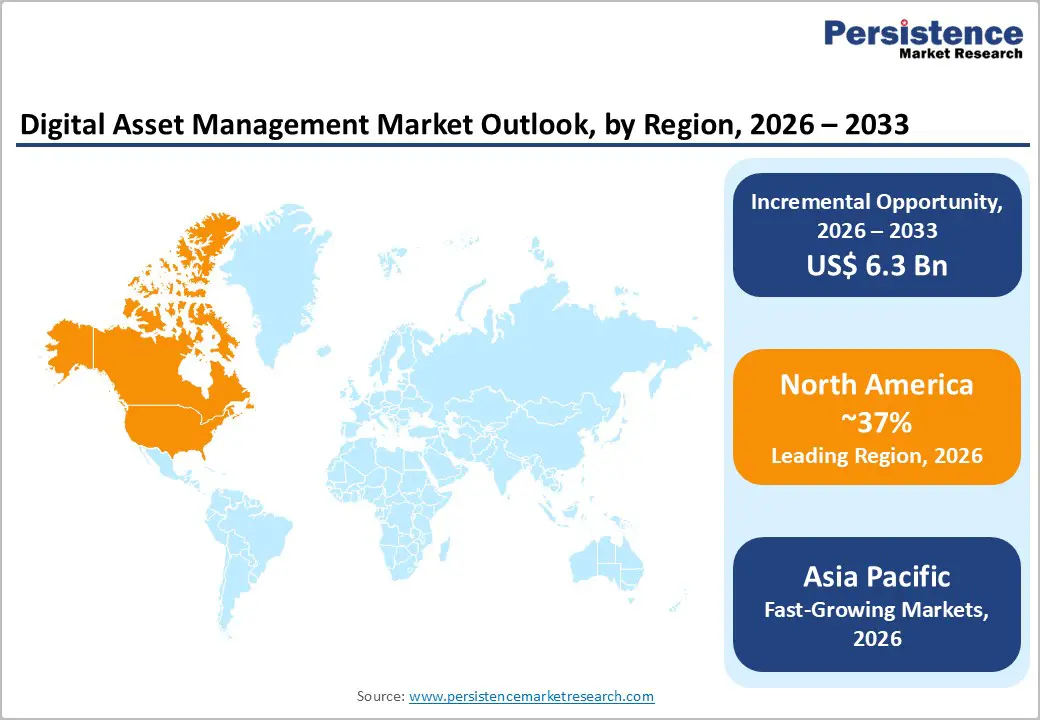

- Leading Region: North America dominates the digital asset management market with a 36% market share in 2026, driven by substantial enterprise digital transformation investments, sophisticated cloud infrastructure supporting scalable deployments, and an organizational focus on omnichannel marketing and customer experience optimization that requires centralized digital asset management capabilities.

- Fastest Growing Region: The Asia Pacific region demonstrates exceptional growth momentum with a CAGR projected between 19%, driven by explosive e-commerce expansion, rapid urbanization, government-mandated digital transformation initiatives, and massive population bases creating robust demand for scalable digital asset management solutions.

- Dominant Segment: Cloud-based deployment model commands approximately 66% of digital asset management market revenue, reflecting organizational preference for operational flexibility, cost-effectiveness, scalability, and accessibility advantages over legacy on-premise infrastructure investments in managing organizational digital assets.

- Fastest Growing Segment: Media and Entertainment vertical demonstrates the highest growth rates exceeding 18% annually, driven by explosive content consumption growth, proliferation of streaming platforms, and increasing complexity in managing multimedia assets, licensing agreements, and distribution rights across global audiences.

- Key Market Opportunity: AI integration within digital asset management systems, enabling automated metadata tagging, intelligent search capabilities, and content recommendations, is expected to drive substantial adoption among marketing, creative, and e-commerce organizations seeking competitive advantage through operational efficiency and marketing agility throughout the forecast period.

| Key Insights | Details |

|---|---|

| Digital Asset Management Size (2026E) | US$ 5.5 Bn |

| Market Value Forecast (2033F) | US$ 11.8 Bn |

| Projected Growth CAGR (2026 - 2033) | 11.5% |

| Historical Market Growth (2020 - 2025) | 12.4% |

Market Dynamics

Drivers - Explosive Growth in Digital Content Creation and Omnichannel Distribution Requirements

Organizations globally are experiencing unprecedented growth in digital content creation, with the number of digital assets expanding exponentially across marketing, sales, and creative departments. The rise of e-commerce platforms, social media marketing, and omnichannel retail strategies has dramatically increased the volume of product images, videos, marketing materials, and branded content requiring centralized management. Organizations deploying digital asset management solutions report significantly improved time-to-market for campaign launches, enhanced brand consistency across channels, and measurable increases in marketing productivity. The correlation between digital content volume and DAM adoption has become increasingly evident, with enterprises recognizing that manual asset management approaches create operational bottlenecks that impede revenue generation and customer engagement objectives.

Accelerating Cloud Adoption and Shift from On-Premise to SaaS Deployment Models

Enterprise migration from legacy on-premises digital asset management systems to modern cloud-based SaaS platforms represents a fundamental transformation in deployment preferences, driven by superior scalability, cost-effectiveness, and accessibility. Cloud-based digital asset management solutions eliminate substantial capital expenditure on on-prem hardware infrastructure, enable seamless collaboration among globally distributed teams, and provide automatic security updates and compliance enhancements without manual IT intervention. This architectural shift has democratized access to enterprise-grade digital asset management capabilities for small and medium-sized enterprises, which previously lacked the financial resources to implement comprehensive on-premises solutions, thereby significantly expanding the addressable market.

Restraints - High Implementation Complexity and Integration Challenges with Legacy Systems

Organizations encounter substantial technical complexity when implementing digital asset management solutions, particularly when integrating modern platforms with entrenched legacy systems spanning Enterprise Resource Planning (ERP), Customer Relationship Management (CRM), and content management infrastructure. The fragmentation of technology stacks within organizations with legacy systems operating on outdated data formats and architectures incompatible with modern cloud-native platforms creates formidable integration barriers that increase implementation timelines and costs. Enterprises must navigate complex API integrations, data migration protocols, metadata standardization challenges, and workflow alignment processes that can extend project timelines by months and substantially increase the total cost of ownership. These implementation complexities disproportionately impact mid-sized organizations that lack dedicated IT teams to manage sophisticated integrations, potentially suppressing adoption rates within this important market segment.

Data Security Concerns and Regulatory Compliance Requirements

Organizations maintain significant apprehension regarding data security, regulatory compliance, and privacy requirements when centralizing digital assets within cloud-based digital asset management platforms. Enterprises operating in regulated industries, including healthcare, financial services, and government, face stringent data residency requirements, encryption mandates, and audit trail obligations that complicate cloud adoption decisions. The absence of universally standardized security protocols across DAM vendors creates decision-making complexity, with organizations conducting exhaustive security assessments before selecting a platform. Additionally, growing concerns about data breaches, unauthorized access to proprietary materials, and intellectual property protection create organizational resistance to centralizing valuable assets in cloud environments, particularly for organizations managing highly sensitive content, including product designs, financial information, and strategic marketing materials.

Opportunity - AI-Powered Metadata Tagging, Automated Content Organization, and Intelligent Search Capabilities

The integration of artificial intelligence and machine learning technologies into digital asset management systems represents a transformative opportunity, enabling automation of previously manual metadata tagging, content categorization, and advanced search. Modern digital asset management platforms now incorporate AI-driven capabilities, including automated image recognition, facial recognition for video content, speech-to-text conversion, and intelligent content recommendations, which dramatically accelerate asset discovery and streamline workflows. Organizations implementing AI-enhanced Digital Asset Management solutions report measurable improvements in search accuracy, reduced time locating appropriate assets, and enhanced content reusability across campaigns. For example, enterprises deploying Bynder’s AI-powered DAM platform have achieved estimated cost savings of over €3.5 million by increasing asset reuse and eliminating unnecessary purchases of external content.

Growth in Retail and E-Commerce Verticals Requiring Advanced Product Information Management and Omnichannel Content Delivery

Explosive growth in retail e-commerce, social commerce, and direct-to-consumer (DTC) business models is generating unprecedented demand for scalable Digital Asset Management infrastructure capable of managing vast product catalogs, dynamic pricing information, and localized marketing content across multiple channels simultaneously. Retail organizations implementing Digital Asset Management systems report accelerated time-to-market for new product launches, enhanced product information consistency across online and physical channels, and improved customer engagement through personalized product experiences. For instance, Chewy’s migration of 2 million assets to Bynder’s DAM platform enabled automated workflows, avoided more than US$ 1 million in legacy system costs, and now publishes over 42,000 assets monthly to e-commerce pages. The convergence of rapid e-commerce expansion, consumer expectations for personalized shopping experiences, and regulatory requirements for product information consistency is expected to drive robust demand for sophisticated digital asset management solutions within retail and e-commerce organizations throughout the 2026 - 2033 forecast period.

Category-wise Analysis

Component Insights

Solution represents the dominant component segment within the digital asset management market, commanding approximately 65% of market value, driven by enterprise investment in comprehensive DAM platforms that include content management, workflow automation, and asset distribution capabilities. Digital asset management solutions encompass the core software platforms enabling organizations to organize, govern, and activate their digital asset portfolios, representing the fundamental value proposition that attracts organizational investment. Solution-based deployments require ongoing operational management, customization, and integration services that create recurring revenue opportunities and deep customer relationships for solution providers.

Deployment Insights

Cloud-based deployment is the dominant segment, commanding approximately 66% of digital asset management market revenue and continuing to expand at accelerated growth rates as organizations prioritize operational flexibility, cost-effectiveness, and scalability over on-premises infrastructure models. Cloud deployment provides superior access for geographically distributed teams, eliminates substantial capital expenditures, and enables organizations to scale infrastructure dynamically as content volume increases. The architectural advantages of cloud-native digital asset management platforms, including automated security updates, built-in redundancy, global content delivery capabilities, and seamless integration with adjacent cloud services, have driven massive adoption of cloud deployment models across enterprise segments. On-premise deployment, while declining as a percentage of total market share, continues to serve specific use cases, including organizations with strict data residency requirements, government agencies with security mandates, and enterprises managing highly sensitive intellectual property.

Application Insights

Sales & marketing emerges as the leading application segment, commanding the largest organizational investment as marketing teams require sophisticated digital asset management capabilities to manage brand assets, campaign materials, product photography, and promotional content across omnichannel distribution channels. Marketing organizations deploying digital asset management solutions report substantially improved campaign execution speed, enhanced brand consistency across regions and campaigns, and measurable improvements in marketing team productivity. The Sales & Marketing application segment benefits from clear return-on-investment metrics, as organizations can quantitatively measure improvements in campaign time-to-market, reductions in asset creation costs through increased reuse, and improved content performance through analytics capabilities embedded in modern digital asset management platforms.

Vertical Insights

Retail & eCommerce represents the dominant end-use vertical, commanding approximately 35% of the digital asset management market share, driven by explosive growth in online retail, intensified competition requiring differentiation through superior product information and visual content, and regulatory requirements mandating accurate product descriptions across multiple markets. Retail organizations manage vast product catalogs encompassing thousands or millions of individual product variations, seasonal collections, and regional customizations, requiring sophisticated asset organization, workflow automation, and distribution capabilities. However, media and entertainment is the fastest-growing vertical, expanding at growth rates exceeding 18% annually, driven by explosive growth in content consumption, the proliferation of streaming platforms, and the increasing complexity of managing multimedia assets, licensing agreements, and distribution rights. Organizations within the media and entertainment vertical that deploy digital asset management solutions report improved content monetization through enhanced asset organization, accelerated content production workflows, and reduced licensing administration complexity enabled by centralized rights management.

Regional Insights

North America Digital Asset Management Trends

North America maintains the largest 36% market share globally in 2025, anchored by robust enterprise digital transformation investments, sophisticated cloud infrastructure ecosystem, and organizational focus on marketing automation and customer experience optimization. The region benefits from substantial investment by leading digital asset management solution providers, including Adobe, Bynder, Canto, and Cognizant, which have established comprehensive service-delivery ecosystems to support enterprise deployments.

United States organizations are allocating substantial budgets to cloud infrastructure modernization, with hyperscale cloud providers including Amazon Web Services, Microsoft Azure, and Google Cloud investing over US$30 billion annually in North American data center expansion to support enterprise application deployments. The region’s regulatory framework, including data protection requirements and compliance obligations within healthcare, financial services, and government sectors, is driving the adoption of digital asset management solutions capable of maintaining comprehensive audit trails and enforcing granular access controls.

Europe Digital Asset Management Trends

Europe demonstrates accelerating digital asset management adoption driven by stringent data protection regulations, evolving marketing requirements emphasizing personalization and omnichannel experiences, and organizational focus on operational efficiency within cost-constrained business environments. The General Data Protection Regulation (GDPR) and related data localization requirements have created strong incentives for organizations to implement Digital Asset Management systems capable of maintaining compliant data-handling practices, enforcing user access controls, and maintaining comprehensive audit documentation to support regulatory compliance efforts.

German enterprises leading in industrial manufacturing are investing in digital asset management solutions to support Industry 4.0 transformation initiatives, managing technical documentation, product specifications, and quality control assets in centralized repositories, enabling rapid product iterations and quality assurance processes. United Kingdom and French organizations are increasingly adopting cloud-based digital asset management platforms to support omnichannel retail strategies, enhance customer engagement through personalized marketing content, and streamline brand asset management across geographically distributed marketing teams.

Asia Pacific Digital Asset Management Trends

Asia Pacific is the fastest-growing regional market for digital asset management, driven by explosive e-commerce expansion, rapid urbanization, and government-mandated digital transformation initiatives prioritizing organizational digitalization and investment in cloud infrastructure. China’s digital economy leadership and massive investment in technology infrastructure have created robust demand for sophisticated Digital Asset Management solutions supporting e-commerce operations, social commerce, and content-rich marketing strategies. China’s Alibaba, JD.com, and emerging platforms are investing heavily in Digital Asset Management infrastructure to manage massive product catalogs, support personalized recommendation engines, and enable rapid product launches supporting competitive positioning within intensely competitive e-commerce markets.

India’s rapidly expanding e-commerce sector, supported by Flipkart, Amazon India, and emerging domestic platforms, is creating substantial demand for scalable digital asset management solutions that manage product information, support omnichannel retail strategies, and enable regional content localization across diverse consumer markets. The Asia Pacific digital asset management market is projected to expand at a CAGR of approximately 19% during the 2026 - 2033 forecast period, significantly exceeding global growth rates, driven by massive population bases, accelerating internet penetration, and government initiatives promoting digital infrastructure investment and entrepreneurship.

Competitive Landscape

The digital asset management market features a moderately consolidated structure, with competition shaped by the interplay of large enterprise software providers, specialized DAM vendors, and cloud-centric platforms. The landscape is defined less by individual brands and more by strategic positioning around platform breadth, integration depth, and service maturity. Dominant players leverage extensive ecosystems, strong enterprise relationships, and end-to-end content workflows to retain leadership, while mid-tier and emerging vendors differentiate through vertical specialization, flexible deployment models, and cost-competitive offerings tailored to niche requirements.

Business strategies across the market emphasize portfolio expansion through acquisitions, integration of DAM with adjacent systems such as content management and product information management, and accelerated investment in AI-driven automation for tagging, workflow orchestration, and content activation. Competitive advantage increasingly depends on the sophistication of workflow automation, scalability for high-volume asset environments, interoperability with existing enterprise stacks, and the strength of implementation and support services that ensure sustained customer value.

Key Market Developments:

- October 2024: Adobe introduced AEM Assets Prime and Ultimate as new cloud-service editions, with Ultimate providing an API-first architecture, advanced automation features, and enhanced scalability for complex enterprise content workflows.

- November 2024: Bynder’s AI-powered DAM platform, including image similarity and search by image features, enables customers to locate visually similar assets and reuse them, with a case study reporting estimated €3.5?M savings.

- October 2025: IBM launches IBM Digital Asset Haven, built with Dfns, enabling financial institutions, governments and corporations to securely manage digital assets across blockchains with custody, governance, and compliance support.

Companies Covered in Digital Asset Management Market

- Adobe Systems Incorporated

- Bynder BV

- Canto, Inc.

- Adam Software NV

- Cognizant Technology Solutions Corporation

- EMC Limited

- Hewlett-Packard Development Company LP

- IBM Corporation

- Open Text Corporation

- Oracle Corporation

- North Plains Systems

- WebDAM

- BrandMaker

- Brandfolder

- Acquia Inc.

- Cloudinary Ltd.

- Celum

- ADLINK Technology Inc.

- Zenlayer Inc.

- Fujitsu Limited

Frequently Asked Questions

The market is projected to reach US$ 11.8 billion by 2033, growing at a CAGR of 11.5% from US$ 5.5 billion in 2026.

Growth is driven by increased digital content creation, cloud adoption, AI-enabled automation, regulatory compliance needs, and organizational focus on operational efficiency.

Cloud-based deployment leads with 66% market share due to flexibility, scalability, cost-effectiveness, and ease of collaboration.

North America holds the largest market share, while Asia Pacific shows the highest growth at 19% CAGR.

AI and machine learning integration offers opportunities for automated tagging, intelligent search, workflow automation, and improved asset reuse.

Key players include Adobe, Bynder, Canto, IBM, Oracle, and other leading DAM solution providers competing through platforms, services, and AI investments.