- Medical Devices

- Dental Laboratory Oven Market

Dental Laboratory Oven Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Dental Laboratory Oven Market by Product (Muffle Ovens, Vacuum Ovens, Sintering Ovens, and Others), Application (Ceramic Sintering, Wax burnout, Sterilization, Research and Development, and Others), End-user (Dental Laboratories, Dental Clinics, Hospitals, Dental Institutions, and Others), and Regional Analysis from 2026 - 2033

Dental Laboratory Oven Market Share and Trends Analysis

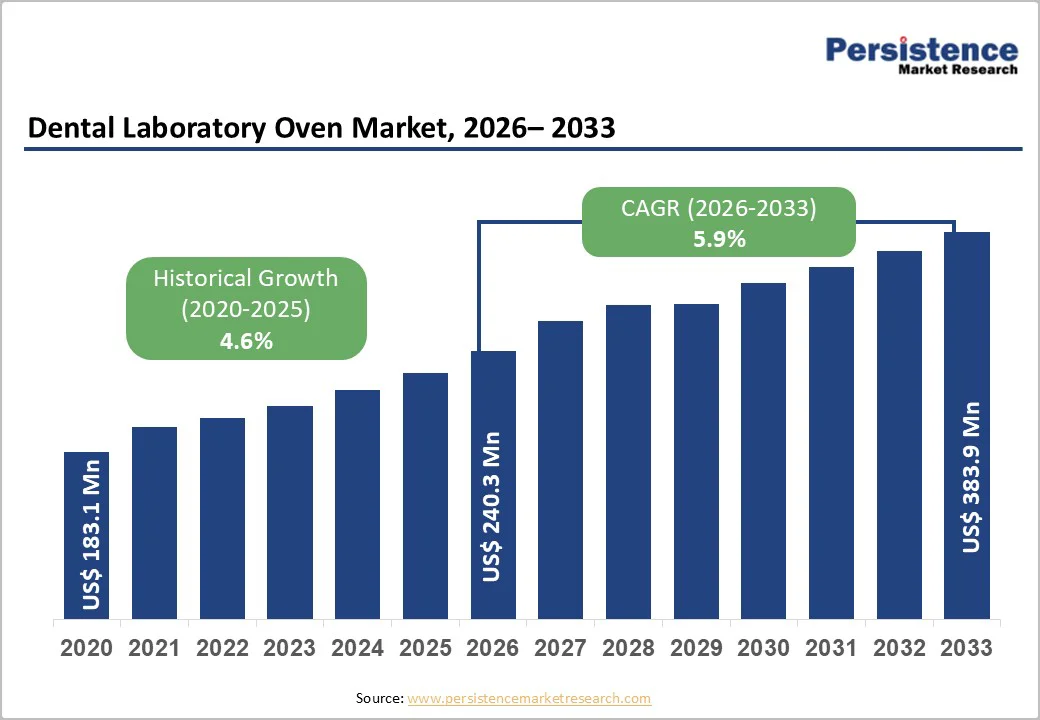

The global dental laboratory oven market size is estimated to grow from US$ 240.3 million in 2026 and projected to reach US$ 383.9 million by 2033, growing at a CAGR of 5.9% during the forecast period from 2026 to 2033. Global demand for dental laboratory ovens is rapidly increasing due to the growing adoption of digital dentistry, rising demand for zirconia and all-ceramic restorations, and the expansion of centralized and private dental laboratories.

The shift toward esthetic and minimally invasive procedures, increasing cosmetic dental awareness, and the need for precise, efficient, and high-quality dental restorations are key contributors. Technological advancements such as energy-efficient rapid-sintering ovens, smart temperature control systems, and digitally connected monitoring features are improving workflow efficiency, accuracy, and product quality. Additionally, supportive regulatory frameworks, structured dental reimbursement programs, and investments in research and development are further driving market growth.

Key Industry Highlights:

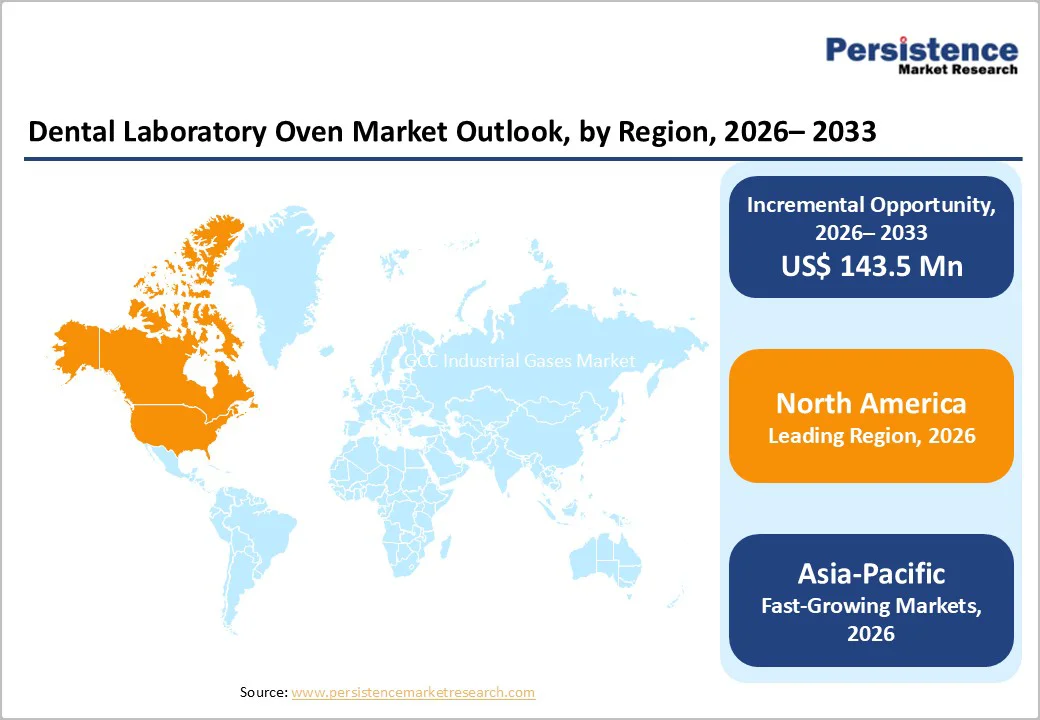

- Leading Region: North America dominates the global dental laboratory oven market with a 45.7% share, driven by high adoption of digital dentistry, advanced dental infrastructure, and strong presence of key oven manufacturers.

- Fastest-Growing Region: Asia Pacific is the fastest-growing market, supported by rising dental awareness, expanding private dental laboratories, increasing disposable incomes, and growing investments in modern dental technology.

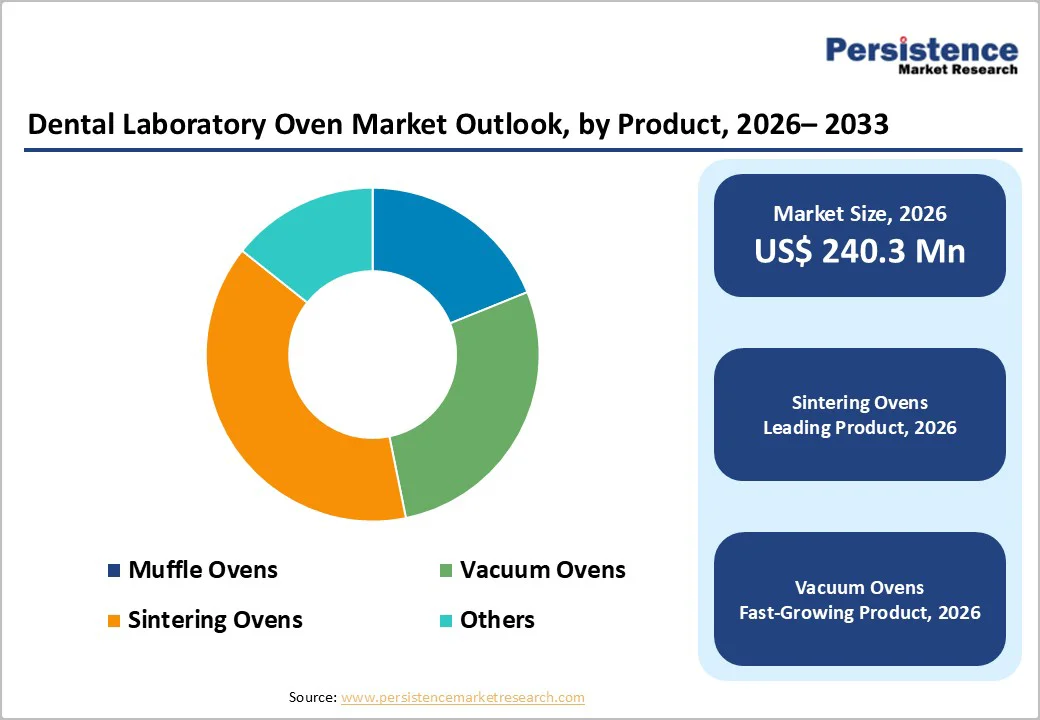

- Leading Product Segment: Sintering ovens lead the product category, owing to high precision, programmable functions, and widespread use in zirconia and ceramic restorations.

- Fastest-Growing Product Segment: Vacuum ovens represent the fastest-growing segment, driven by affordability, energy efficiency, and integration in modern dental labs.

- Leading Application Segment: Ceramic sintering dominates usage segmentation, attributed to compatibility with multiple dental materials, cost efficiency, and robust adoption across laboratories and academic institutions.

- Fastest-Growing Application Segment: Research and Development (R&D) is the fastest-growing category due to increasing focus on advanced dental materials, lab innovation, and precision restoration techniques.

| Key Insights | Details |

|---|---|

|

Dental Laboratory Oven Market Size (2026E) |

US$ 240.3 Mn |

|

Market Value Forecast (2033F) |

US$ 383.9 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

5.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.6% |

Market Dynamics

Driver - Growing Adoption of Zirconia-Based Aesthetic Restorations

The shift toward zirconia crowns, bridges, and implant restorations is significantly increasing the need for advanced dental laboratory ovens capable of high-temperature, controlled sintering. Zirconia offers superior strength, biocompatibility, and fracture resistance compared to porcelain-fused-to-metal (PFM) materials, driving demand across both premium and routine restorative workflows. As more labs transition to digital CAD/CAM manufacturing, cycle accuracy, temperature uniformity, and repeatability have become essential purchasing factors for oven installations and upgrades.

Moreover, patient expectations for natural-looking, aesthetic, and durable prosthetics are rising with increasing awareness, cosmetic dentistry demand, and dental tourism. This is pushing laboratories to invest in high-precision sintering ovens that deliver consistent translucency, shade accuracy, microstructural stability, and polishability. Dental chains and outsourcing centers focusing on aesthetic outcomes are prioritizing ovens with advanced digital control, validated programs for multilayer zirconia, and integration with digital workflows are driving the market growth.

Restraints - Cost Barriers and Emerging Competitive Alternatives

High upfront investment for premium sintering and vacuum ovens, combined with ongoing maintenance costs, continues to limit adoption, particularly for small and mid-sized dental laboratories. Capital expenditure for advanced multi-chamber or rapid-sintering units can be substantial, and additional expenses such as calibration, spare parts, heating elements, and downtime-related service interruptions increase total ownership cost. These financial constraints often delay replacement cycles and push labs to extend the use of outdated systems rather than upgrading to newer, high-efficiency models.

Furthermore, the increasing penetration of 3D-printing workflows and outsourced sintering services is intensifying competitive pressure on internal oven installations. Dental processors offering centralized sintering services and high-volume providers enable laboratories to avoid both equipment purchases and maintenance responsibilities, especially when production demand is variable. As metal and ceramic 3D-printing technologies advance and become more cost-optimized, more labs may shift to outsourcing or additive manufacturing workflows, reducing reliance on traditional oven-based sintering.

Opportunity - Advancement Toward Digitally Integrated and Energy-Efficient Smart Ovens

The integration of dental laboratory ovens with computer-aided design (CAD) and computer-aided manufacturing (CAM) systems and automated sintering workflows is creating opportunities in the market. As digital dentistry expands, laboratories increasingly seek automated temperature control, preset sintering programs matching specific zirconia and ceramic materials, and connectivity with milling and design systems. Automated loading cycles, real-time performance monitoring, and reduced operator dependency improve consistency, minimize human error, and enable higher throughput. These digitally enabled ovens also support data logging for traceability and quality assurance, making them attractive for large labs, DSOs, and outsourced production centers.

Rising energy costs and sustainability requirements are accelerating demand for energy-efficient, connected smart ovens. New-generation systems featuring optimized heating elements, low-power standby modes, predictive maintenance, and remote diagnostics help laboratories reduce operating expenses and unplanned downtime. IoT-enabled models allow remote cycle programming, performance analytics, and early failure detection—significantly improving uptime and lifecycle value. These features present a strong revenue opportunity for manufacturers focused on intelligent, resource-efficient furnace technology aligned with modern digital lab environments.

Category-wise Analysis

By Product Insights

The sintering ovens segment is projected to dominate the global dental laboratory oven market in 2026, accounting for a revenue share of 38.9%. The segment’s strong performance is primarily driven by the increasing adoption of zirconia-based crowns and bridges, fueled by rising demand for high-strength, aesthetic dental restorations and rapid digitalization through CAD/CAM workflows. Sintering ovens enable precise temperature control and uniform microstructure development, which are critical for achieving optimal translucency, shade stability, and long-term durability.

Additionally, the expansion of centralized dental laboratories and outsourcing centers is accelerating high-volume sintering capacity requirements, particularly as dental tourism and cosmetic dentistry procedures expand in emerging markets. The growing shift from porcelain-fused-to-metal restorations to all-ceramic alternatives is further increasing the dependency on advanced sintering equipment.

By Application Insights

The ceramic sintering segment is projected to dominate the global dental laboratory oven market in 2026, accounting for a revenue share of 56.8%. This is driven by the surging adoption of zirconia and advanced ceramic materials for dental restorations, supported by rising patient demand for highly aesthetic, metal-free prosthetics with superior strength and longevity. As cosmetic dentistry and minimally invasive restorative procedures continue to grow worldwide, laboratories are increasingly prioritizing materials that deliver natural translucency and reliable clinical performance, positioning ceramic sintering as a critical processing stage. The shift toward digital restorative workflows and CAD/CAM production has increased the need for reliable high-temperature sintering processes, enabling consistent shade accuracy, enhanced translucency, and faster production cycles to meet competitive turnaround expectations.

Additionally, the expansion of centralized dental laboratories and outsourcing centers is accelerating investments in high-capacity sintering infrastructure to manage rising restoration volumes. Technological innovations such as rapid-cycle sintering, multi-chamber furnace systems, and automated programmable firing profiles further strengthen adoption by enabling greater productivity, reduced energy consumption, and higher reproducibility.

By End-user Insights

The dental laboratories segment is projected to dominate the global dental laboratory oven market in 2026, accounting for a revenue share 54.2%. This is driven by the increasing volume of dental restoration procedures, including crowns, bridges, implants, and aesthetic prosthetics, which require precise thermal processing and high-capacity production capabilities. Dental laboratories handle complex multi-unit cases and large daily workloads, making advanced sintering, burnout, and vacuum ovens essential components of their infrastructure.

The growing adoption of CAD/CAM–enabled digital dentistry, along with the rising shift from porcelain-fused-to-metal restorations to zirconia and all-ceramic solutions, is supporting strong equipment demand among professional labs. Centralized dental production centers, outsourcing units, and large-scale laboratory networks are significantly investing in automated, energy-efficient oven systems to improve turnaround times, achieve consistent quality, and accommodate growing cosmetic dentistry volumes.

Regional Insights

North America Dental Laboratory Oven Market Trends

North America is expected to dominate globally with a value share of 45.7% in the 2026, with the U.S. leading the region due to its highly developed dental care infrastructure, strong presence of advanced dental laboratories, and rapid adoption of CAD/CAM and digital dentistry technologies. High demand for aesthetic and implant-supported restorations, combined with substantial reimbursement coverage and patient spending on cosmetic dental procedures, further strengthens market growth. Additionally, the presence of major oven manufacturers, well-established distribution networks, and continuous technology upgrades supports strong equipment procurement and replacement cycles across large laboratory chains and specialized dental service providers. The growing shift toward in-house lab capabilities within dental clinics and DSOs is also contributing to rising equipment investments. Furthermore, increased training availability and ongoing innovation in rapid-cycle sintering technologies continue to boost market growth in the region.

Europe Dental Laboratory Oven Market Trends

Europe is expected to achieve a steady growth, driven by the rising adoption of digital dentistry, increasing demand for zirconia and all-ceramic restorations, and the strong expansion of centralized dental laboratories across key countries such as Germany, UK, France, and Italy. Supportive regulatory frameworks, structured dental reimbursement programs, and growing awareness of advanced cosmetic dental procedures are boosting equipment investments. Additionally, the region benefits from the presence of leading oven manufacturers and ongoing technological advancements in rapid sintering and energy-efficient furnace systems, which are encouraging replacement and upgrade cycles across laboratories and educational institutions. Growing collaborations between dental universities and private labs are fostering skill development and research in advanced dental materials. Furthermore, the increasing focus on minimally invasive procedures and esthetic dentistry is driving the demand for high-precision dental ovens across the region.

Asia Pacific Dental Laboratory Oven Market Trends

The Asia Pacific market is expected to register a relatively higher CAGR of around 7.8% between 2026 and 2033, fueled by rapid urbanization, rising disposable incomes, and increasing awareness of oral healthcare across countries such as China, India, Japan, and South Korea. Strong adoption of digital dentistry solutions, growing demand for zirconia and all-ceramic restorations, and the expansion of private and chain dental clinics are driving investments in advanced dental ovens.

Furthermore, government initiatives to improve dental infrastructure, favorable reimbursement programs, and rising patient preference for cosmetic and minimally invasive procedures are supporting market growth. The region is also witnessing increasing collaborations between local manufacturers and global technology providers, facilitating the introduction of energy-efficient, rapid sintering, and high-precision oven systems. Additionally, skill development programs and research partnerships with dental universities are encouraging the adoption of advanced technologies across laboratories and educational institutions.

Competitive Landscape

The global dental laboratory oven market is highly competitive, with major players such as Aixin Medical Equipment Co., Ltd, Amann Girrbach AG, B&D Dental Corporation, DEKEMA Dental-Keramiköfen GmbH, Dentalfarm, and Forum Energy Technologies, Inc. leveraging broad product portfolios, technologically advanced oven systems, and strong international distribution networks. Companies are prioritizing innovation in compact, energy-efficient, and digitally enhanced ovens designed to support ceramic sintering, zirconia processing, and advanced restorative procedures.

Market participants are actively investing in next-generation rapid-sintering furnaces, intelligent temperature-control systems, and integrated digital monitoring to improve precision, efficiency, and laboratory workflow. Strategic initiatives include mergers and acquisitions to expand manufacturing capabilities, partnerships with dental universities and research institutions for material-device optimization, and geographic expansion across high-growth emerging markets such as China, India, and Southeast Asia.

Key Industry Developments:

- In September 2025, VBCC High Temperature Instruments Pvt. Ltd. launched its first range of high-end dental furnaces for laboratories in India. Equipped with state-of-the-art technology, these furnaces ensure precise sintering essential for producing dentures, crowns, and bridges.

- In September 2025, Dentsply Sirona announced the upcoming launch of an expanded AI-powered CEREC workflow, along with new milling units, CEREC Primemill Lite and CEREC Go designed to make Single Visit Dentistry more accessible. The innovations will be showcased through previews and hands-on demonstrations at multiple events starting in September. Complementing this launch are the multidimensional CEREC Cercon 4D™ zirconia CAD/CAM and Abutment blocks, offering enhanced precision, efficiency, and versatility for dental laboratories and clinics.

- In November 2024, VITA announced the addition of the VITA VACUMAT® 6100 M to its line of established dental furnaces. The new VITA VACUMAT 6100 M is a fully automatic, microprocessor-controlled firing unit, designed to efficiently meet all dental ceramic firing requirements, ensuring precision, consistency, and high-quality restorations in laboratory workflows.

Companies Covered in Dental Laboratory Oven Market

- Aixin Medical Equipment Co., Ltd

- Amann Girrbach AG

- B&D Dental Corporation

- DEKEMA Dental-Keramiköfen GmbH

- Dentalfarm

- Forum Energy Technologies, Inc.

- Ivoclar Vivadent

- MIHM-VOGT GmbH & Co. KG.

- Carbolite Gero Ltd.

- ShenPaz Dental LTD

- Zubler Gerätebau GmbH

- Others

Frequently Asked Questions

The global dental laboratory oven market size is projected to be valued at US$ 240.3 Mn in 2026.

Growing demand for advanced cosmetic dental procedures, digital dentistry adoption, and technological advancements in energy-efficient and rapid-sintering ovens are driving the global dental laboratory oven market.

The global dental laboratory oven market is poised to witness a CAGR of 5.9% between 2026 and 2033.

Rising adoption of digital dentistry, increasing demand for zirconia/all-ceramic restorations, and expansion of modern dental laboratories in emerging markets creating opportunities in the market.

Aixin Medical Equipment Co., Ltd, Amann Girrbach AG, B&D Dental Corporation, DEKEMA Dental-Keramiköfen GmbH, Dentalfarm, and Forum Energy Technologies, Inc. are some of the key players in the dental laboratory oven market.