- Food Packaging

- Dairy Packaging Machine Market

Dairy Packaging Machine Market Size, Share, and Growth Forecast, 2026 - 2033

Dairy Packaging Machine Market by Machine Type (Filling Machines, Form-Fill-Seal Machines, Others), Packaging Type (Cartons, Pouches & Sachets, Others), Automation Level, Application, and Regional Analysis for 2026 - 2033

Dairy Packaging Machine Market Size and Trends Analysis

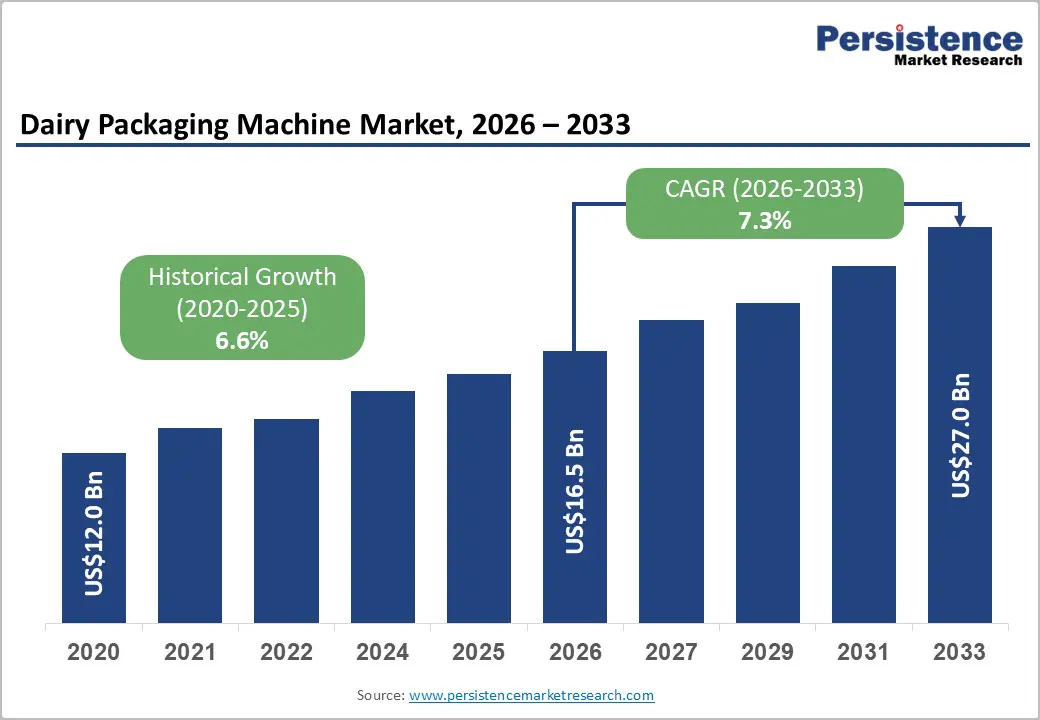

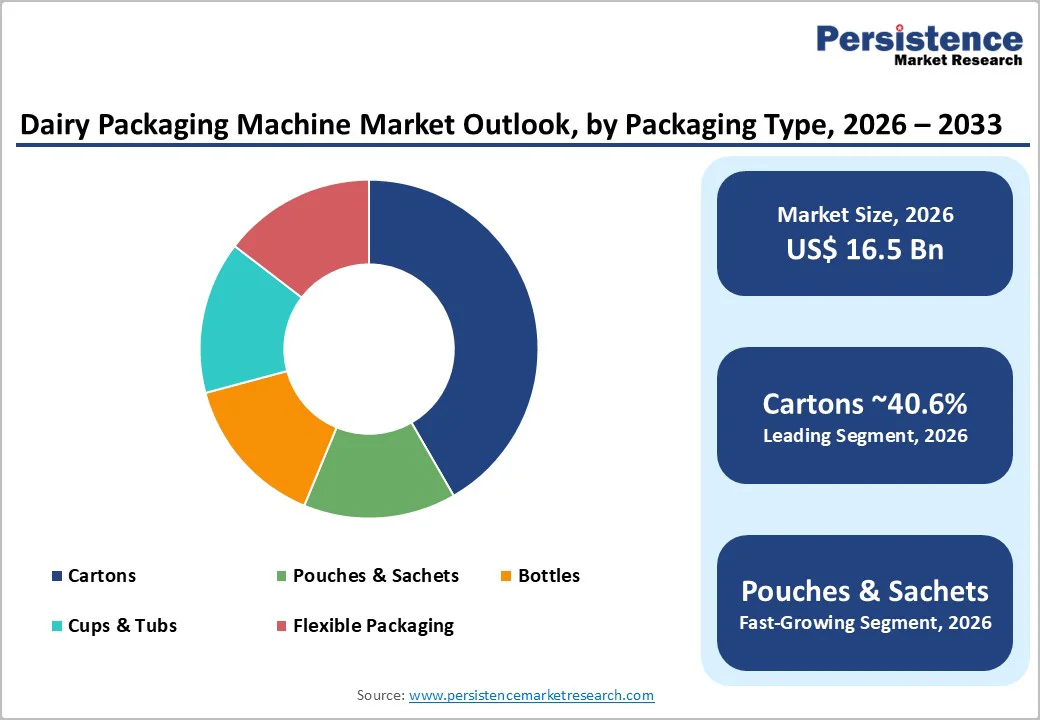

The global dairy packaging machine market size is likely to be valued at US$16.5 billion in 2026 and is expected to reach US$27.0 billion by 2033, growing at a CAGR of 7.3% between 2026 and 2033, driven by rising automation adoption, sustainability-driven packaging transitions, and increasing digitalization of packaging lines.

Accelerating investment in intelligent, high-throughput equipment supports forecast credibility. Growth is driven by rising processed dairy demand, automated packaging to boost efficiency, and sustainability mandates. Offsets include component supply constraints and the high capital costs of equipment upgrades.

Key Industry Highlights

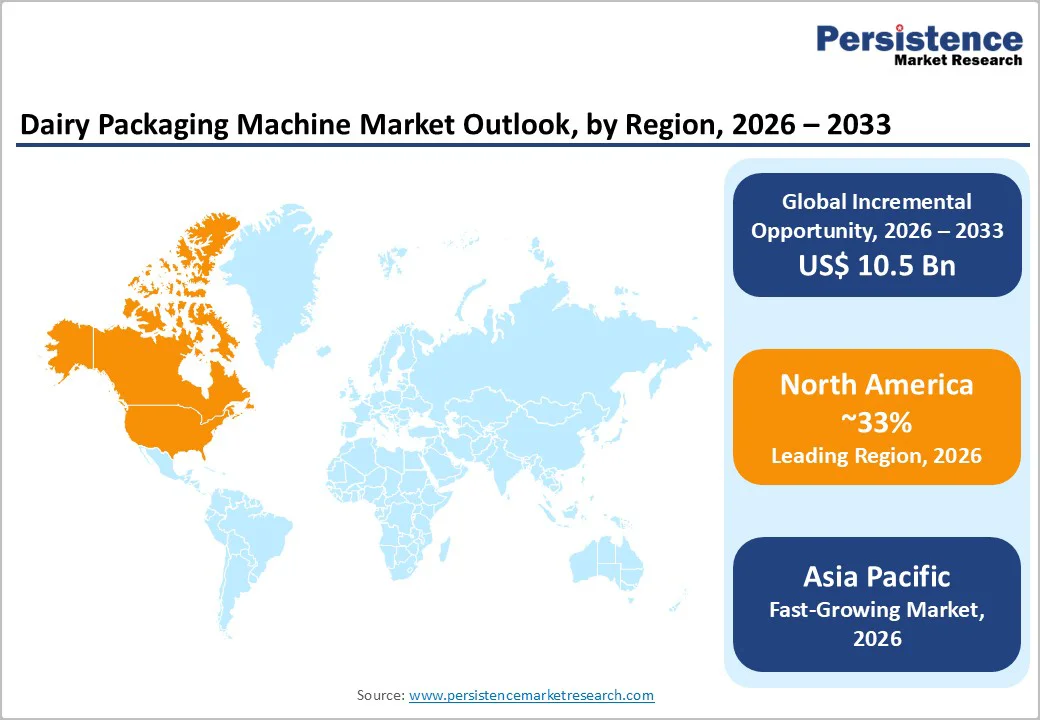

- Leading Region: North America is projected to hold 33% market share, supported by high automation density, large-scale dairy processors, and sustained investment in fully automated, digitally enabled packaging lines.

- Fastest-growing Region: Asia Pacific, accounting for the largest share of incremental demand, driven by rising dairy consumption in China and India, rapid urbanization, and expanding adoption of flexible and single-serve packaging formats.

- Investment Plans: Capital investments are primarily directed toward fully automated and retrofit-ready lines, with a growing share of spending allocated to digitalization, predictive maintenance, and sustainability-compliant machinery to support recyclable and lightweight packaging formats.

- Dominant Machine Type: Filling machines are estimated to hold approximately 36.9% revenue share, reflecting their critical role in liquid and semi-liquid dairy applications such as milk, drinkable yogurt, and flavored dairy beverages.

- Leading Packaging Type: Carton packaging is anticipated to hold approximately 40.6% revenue share, driven by strong demand for long-life milk and aseptic dairy beverages, alongside favorable recyclability and logistics efficiency.

| Key Insights | Details |

|---|---|

| Dairy Packaging Machine Market Size (2026E) | US$16.5 Bn |

| Market Value Forecast (2033F) | US$27.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.6% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Automation and Industry 4.0 Adoption

Equipment automation, line integration, and data-driven operations represent the most significant modernization forces shaping dairy packaging facilities. Dairy processors are increasingly investing in fully automatic filling, cartoning, labeling, and palletizing systems to improve throughput, enhance traceability, and reduce reliance on manual labor.

Automated lines also lower contamination risk by minimizing human contact with food products. The integration of digital tools such as predictive maintenance, real-time performance monitoring, and line optimization software has become a standard investment priority.

These developments directly expand demand for advanced dairy packaging machines that can support digital connectivity and smart factory environments, making automation a repeatable and scalable growth driver for equipment suppliers.

Sustainability and Lightweighting

Sustainability commitments from dairy brands, retailers, and regulators are accelerating the shift toward recyclable, mono-material, and lightweight packaging solutions. As packaging formats evolve, dairy producers must upgrade or replace existing machinery to process new materials at a commercial scale.

Extended producer responsibility frameworks, recycling targets, and retailer sustainability scorecards are prompting rapid transitions away from complex multi-material structures. Equipment capable of handling recyclable cartons, mono-material flexible packs, and lightweight plastic formats is increasingly favored.

This structural shift is driving capital reallocation toward machinery that supports sustainability objectives while maintaining hygiene standards, shelf life, and operational efficiency.

Growth in Processed and Convenience Dairy Formats

Rising consumer demand for single-serve, extended-shelf-life, and ready-to-consume dairy products is supporting sustained investment in specialized packaging equipment. Growth in drinkable yogurts, flavored milk, portion-controlled dairy snacks, and on-the-go dairy beverages is increasing the number of packaging lines and product variants per facility.

This trend drives demand for form-fill-seal systems, aseptic filling technologies, and flexible packaging machinery. Expansion of refrigerated and ambient cold-chain infrastructure further supports this shift. As dairy portfolios diversify, manufacturers increasingly pursue brownfield expansions and equipment upgrades to maintain efficiency while meeting hygiene and quality requirements.

Barrier Analysis - High Capital Intensity and Long Payback Periods

Upgrading to fully automated and digitally enabled packaging lines requires substantial capital investment, often resulting in extended payback periods. This financial barrier is particularly challenging for mid-sized and regional dairy processors with constrained capital budgets. Rising energy costs and volatility in raw milk pricing further limit discretionary capital spending.

As a result, equipment replacement cycles may be delayed, creating uneven demand patterns. Fully integrated filling, cartoning, and palletizing systems can require investments in the low-to-mid million-dollar range, with returns dependent on utilization rates, labor savings, and product mix.

Supply-Chain and Component Constraints

Dairy packaging machines rely on specialized components such as servo motors, control systems, sensors, and precision sealing mechanisms. Disruptions in component supply chains can lead to extended lead times, higher procurement costs, and production delays for equipment manufacturers.

These constraints increase working capital requirements and complicate delivery schedules. When component shortages coincide with periods of strong demand, equipment suppliers may experience backlog-driven revenue deferrals, limiting near-term market realization despite strong order intake.

Opportunity Analysis - Retrofit and Brownfield Modernization

A significant portion of dairy packaging infrastructure consists of legacy equipment with limited automation and digital capabilities. Retrofitting existing lines with automation modules, vision inspection, in-line weighing, and digital monitoring presents a substantial opportunity.

In mature markets, retrofit spending can represent a meaningful share of annual new-equipment investment. Retrofit solutions offer faster payback and lower upfront cost compared to full line replacements, making them attractive to mid-sized processors. This opportunity favors equipment suppliers with modular designs and strong service capabilities.

Emerging Markets and Localized Manufacturing

Rapid growth in dairy consumption across Asia Pacific and parts of Latin America is driving capacity expansion and greenfield investments. Demand is strongest for mid-speed machinery adapted to local packaging formats such as pouches, cups, and sachets.

Even a modest shift in global dairy volume growth toward these regions translates into significant incremental demand for packaging equipment. Establishing localized assembly operations and regional partnerships reduces delivery times and costs, creating competitive advantages for global suppliers expanding into high-growth markets.

Services, Spare Parts, and Digital Subscriptions

Beyond equipment sales, recurring revenue streams from spare parts, maintenance services, and digital monitoring platforms offer attractive margin expansion opportunities. Remote diagnostics, predictive maintenance, and performance analytics reduce downtime and total cost of ownership for dairy processors.

Over the first several years of operation, service-based revenues can generate steady, annuity-like cash flows. Equipment manufacturers that bundle hardware with digital services and long-term support contracts are well-positioned to enhance customer retention and lifetime value.

Category-wise Analysis

Machine Type Insights

Filling machines are estimated to account for approximately 36.9% of total demand in the dairy packaging machine market, reflecting their indispensable role in liquid and semi-liquid dairy processing. Dairy products require precise dosing, hygienic handling, and, in many cases, aseptic conditions to ensure food safety and shelf stability.

Equipment types include rotary piston fillers for viscous products such as yogurt and cream, volumetric fillers for standardized milk portions, gravity fillers for low-viscosity liquids, and aseptic filling systems for long-life dairy beverages.

High consumption volumes of liquid milk, drinkable yogurts, creamers, and flavored dairy drinks ensure consistent utilization of these systems across processing facilities. Replacement cycles and capacity expansions remain heavily concentrated in this segment, reinforcing its position as the primary source of revenue.

Large-scale dairy processors regularly upgrade filling equipment to improve line speeds, reduce product loss, and comply with evolving hygiene and traceability requirements.

For example, aseptic filling lines are widely deployed in the production of ultra-high-temperature milk and ambient yogurt drinks, where extended shelf life and regulatory compliance are critical. The need to support multiple product viscosities and packaging formats further sustains long-term investment in filling technologies.

Form-fill-seal machines are likely to be the fastest-growing machine type, driven by the rapid adoption of flexible packaging across dairy applications. Vertical form-fill-seal systems are extensively used for pouches and sachets containing milk, yogurt drinks, flavored dairy beverages, and creamers. These machines combine forming, filling, and sealing into a single continuous operation, enabling high-speed output while reducing floor space and labor requirements.

Growth is particularly strong in emerging markets, where single-serve dairy sachets are widely distributed through urban retail and local distribution networks.

At the same time, processors in developed markets are increasingly adopting form-fill-seal systems for resealable spouted pouches used in flavored milk and protein-enriched dairy drinks. The ability of these machines to handle lightweight films, recyclable mono-material structures, and high-speed production makes them well-suited to both cost-efficiency and sustainability-driven packaging strategies.

Packaging Type Insights

Cartons are anticipated to hold approximately 40.6% of the dairy packaging market by value, maintaining their position as the leading packaging type, particularly for liquid milk and long-life dairy beverages.

Their ability to support aseptic processing, extended shelf life, and efficient storage and transportation makes cartons a preferred format for large-scale dairy processors. Carton packaging is widely used for ultra-high-temperature milk, flavored milk, creamers, and nutritional dairy drinks distributed through ambient and refrigerated supply chains.

Aseptic carton systems require specialized and capital-intensive equipment, including sterile filling chambers, chemical sterilization units, and precision sealing technologies.

These technical requirements create high entry barriers and concentrate demand among established equipment suppliers. Cartons continue to benefit from sustainability-driven brand strategies, as fiber-based packaging aligns with recycling objectives and circular economy initiatives. Regulatory frameworks supporting recyclable packaging materials further reinforce ongoing investment in carton-compatible machinery.

Pouches and sachets are likely to be the fastest-growing packaging format, supported by material efficiency, lightweight logistics, and growing consumer demand for convenience.

These formats use significantly less material per unit compared to rigid packaging, lowering transportation costs and reducing overall packaging waste. Single-serve sachets and stand-up pouches are increasingly used for milk, yogurt drinks, flavored dairy products, and dairy-based nutritional beverages.

Flexible packaging already accounts for a substantial share across multiple dairy categories, sustaining demand for high-speed pouching and sealing equipment. Growth is further reinforced by e-commerce and quick-commerce distribution models, where lightweight and durable packaging improves delivery efficiency.

Urban consumption patterns and on-the-go lifestyles continue to accelerate adoption, prompting dairy processors to invest in pouch-filling lines capable of handling recyclable films, resealable closures, and premium pouch designs.

Regional Market Insights

North America Dairy Packaging Machine Market Trends - Automation-Intensive, Service-Led Equipment Demand

North America is expected to dominate the market with roughly a 33% share, supported by the advanced automation adoption by the U.S., the presence of large dairy processors, and stringent food safety and traceability regulations. Major dairy groups and contract packers in the U.S. continue to invest in high-speed, fully automated filling, cartoning, and palletizing lines to improve throughput and operational consistency.

Brands producing extended-shelf-life milk, flavored dairy beverages, and single-serve yogurt formats increasingly rely on aseptic and digitally integrated packaging lines to support nationwide distribution.

Sustainability initiatives, including recyclable packaging commitments by leading retailers and foodservice chains, influence packaging format decisions and reinforce demand for adaptable machinery capable of running cartons, lightweight bottles, and mono-material pouches.

Canada contributes through specialty, organic, and value-added dairy segments, where processors focus on flexible, lower-volume production with high hygiene and quality standards. Across the region, original equipment manufacturers increasingly emphasize service-led business models, offering predictive maintenance, remote monitoring, and lifecycle support contracts.

This shift reflects the maturity of the market, where long-term equipment reliability and uptime are prioritized alongside capital investment, reinforcing North America’s position as a high-value and service-intensive region for dairy packaging machinery.

Europe Dairy Packaging Machine Market Trends - Regulation-Driven Sustainability and Precision Engineering

Europe represents a technologically advanced and regulation-driven market, shaped by stringent environmental policies and a strong domestic machinery manufacturing base.

Germany serves as the core production and innovation hub for dairy packaging equipment, supported by a dense network of engineering firms and automation specialists. End-user demand is led by countries such as the U.K., France, and Spain, where large dairy processors and cooperative groups invest in modernized filling, labeling, and case-packing lines.

Harmonized packaging waste and recycling regulations across the region accelerate the transition toward recyclable and mono-material packaging, driving upgrades to machinery that can handle new material structures without compromising line speed or hygiene.

Premium dairy categories, including cultured products, specialty cheeses, and value-added milk beverages, further support demand for specialized equipment designed for gentle handling and precise portioning.

European dairy brands also prioritize energy efficiency and reduced water consumption, influencing purchasing decisions toward machines with lower operating footprints and advanced digital controls. Digitalization, including inline inspection and data-driven line optimization, has become a standard requirement rather than a differentiator, positioning Europe as a reference market for compliance-driven and sustainability-focused equipment innovation.

Asia Pacific Dairy Packaging Machine Market Trends - Rapid Capacity Expansion and Cost-Efficient Modernization

Asia Pacific is the fastest-growing regional market for dairy packaging machines, supported by rising dairy consumption, rapid urbanization, and ongoing retail modernization. China and India lead demand growth, with large dairy brands expanding capacity to meet increasing consumption of packaged milk, yogurt drinks, and nutritional dairy beverages.

In China, investment is concentrated in high-speed aseptic filling and pouching lines for drinkable dairy products, reflecting strong demand for shelf-stable and convenient formats. India shows robust uptake of mid-speed filling and form-fill-seal equipment, particularly for milk sachets and yogurt cups distributed through expanding organized retail and cold-chain networks.

Southeast Asian markets demonstrate strong adoption of single-serve and flexible packaging formats, reinforcing demand for compact, cost-efficient machinery. Local manufacturing advantages, combined with government incentives for domestic production, encourage global equipment suppliers to establish regional assembly and service hubs.

These localized strategies reduce lead times and improve affordability, accelerating the conversion of small and mid-sized processors from manual or semi-automatic operations to modern packaging lines. As a result, Asia Pacific accounts for a disproportionate share of incremental global equipment demand and remains the primary engine of volume growth over the forecast period.

Competitive Landscape

The global dairy packaging machine market is moderately concentrated at the high end, with global leaders dominating aseptic and high-speed liquid applications. At the same time, a fragmented ecosystem of regional and specialized suppliers serves flexible packaging and semi-automatic segments. Competitive advantage is driven by R&D scale, global service networks, and validated hygiene and sustainability performance.

Recent strategic activity highlights the industry’s focus on digital platforms, portfolio expansion, and sustainability-driven innovation. Equipment manufacturers are launching factory-level software solutions, pursuing acquisitions to broaden technological capabilities, and investing in regional training and service infrastructure. These initiatives reinforce the transition from equipment-only models toward integrated systems and lifecycle partnerships.

Leading players emphasize modular product platforms, digital service monetization, geographic expansion through local assembly, and differentiated pricing strategies. Energy efficiency, hygiene validation, and operational flexibility remain key competitive differentiators.

Key Industry Developments

- In August 2025, Syntegon introduced enhancements to pouch and thermoforming packaging systems, while Sidel presented its Aseptic Combi Predis™ solution at ProPak Asia, combining blow-fill-seal capability for PET and pouch applications in dairy and beverage markets.

- In April 2025, Tetra Pak launched a new high-speed aseptic filling module designed for PET bottles that reduces CIP energy consumption by approximately 30% and simplifies integration with existing packaging lines, signaling product innovation aimed at boosting operational efficiency globally.

Companies Covered in Dairy Packaging Machine Market

- Tetra Pak

- Krones AG

- Sidel

- Syntegon Technology

- GEA Group

- IMA Group

- KHS Group

- SIG Combibloc

- Barry-Wehmiller/ProMach

- Coesia S.p.A.

- Ishida Co., Ltd.

- MULTIVAC

- Nordson/Douglas Machine

- ULMA Packaging

- Sealed Air

Frequently Asked Questions

The global dairy packaging machine market is estimated to be valued at US$16.5 billion in 2026.

Key trends include increasing adoption of fully automated packaging lines, growing demand for aseptic and flexible packaging formats, rising integration of digital monitoring and predictive maintenance, and a shift toward machinery capable of handling recyclable and lightweight packaging materials.

Filling machines represent the leading segment, accounting for approximately 36.9% of total market share, due to their critical role in packaging liquid and semi-liquid dairy products such as milk, yogurt drinks, and creamers.

The market is expected to grow at a CAGR of 7.3% between 2026 and 2033.

Major players with strong and diversified portfolios include Tetra Pak, Krones AG, Sidel, GEA Group, and Syntegon Technology.