- Specialty & Fine Chemicals

- Cosmetic Ingredients Market

Cosmetic Ingredients Market Size, Share, and Growth Forecast, 2025 - 2032

Cosmetic Ingredients Market By Ingredient Type (Surfactants & Emulsifiers, Emollients & Lipids, Others), Application (Skincare, Hair Care, Others), Source, and Regional Analysis for 2025 - 2032

Cosmetic Ingredients Market Size and Trends Analysis

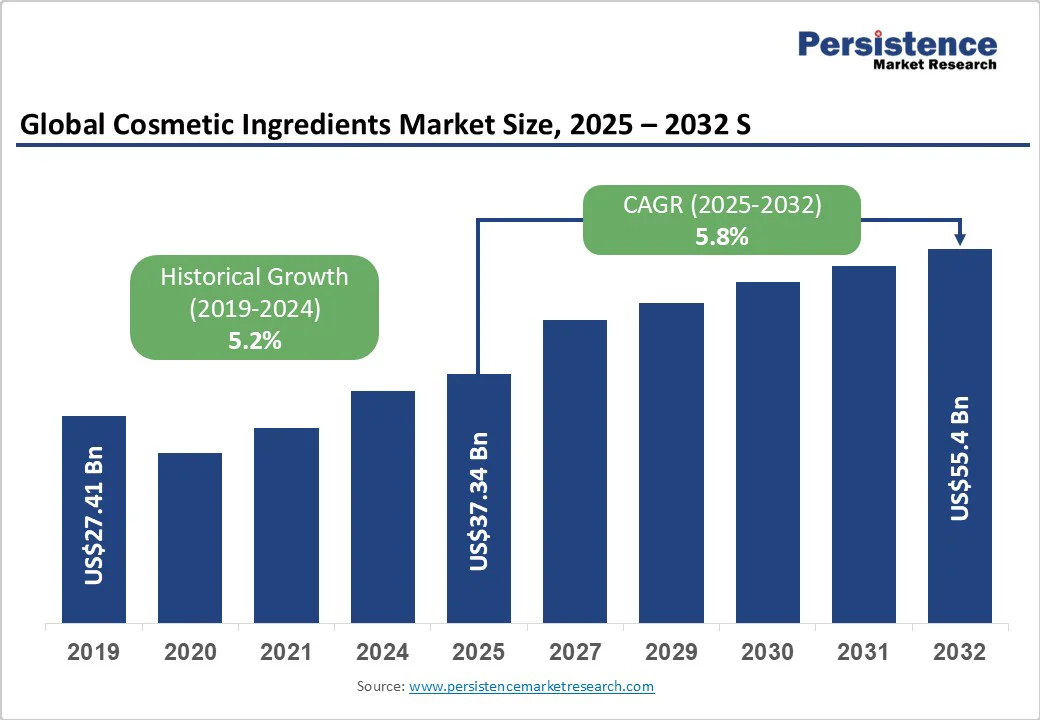

The global cosmetic ingredients market size is likely to be valued at US$37.4 Billion in 2025 and is projected to reach US$55.4 Billion by 2032, growing at a CAGR of 5.8% between 2025 and 2032, driven by the demand for specialty and active ingredients (peptides, botanicals, microbiome-friendly actives) and sustainability-driven substitution.

Key Industry Highlights

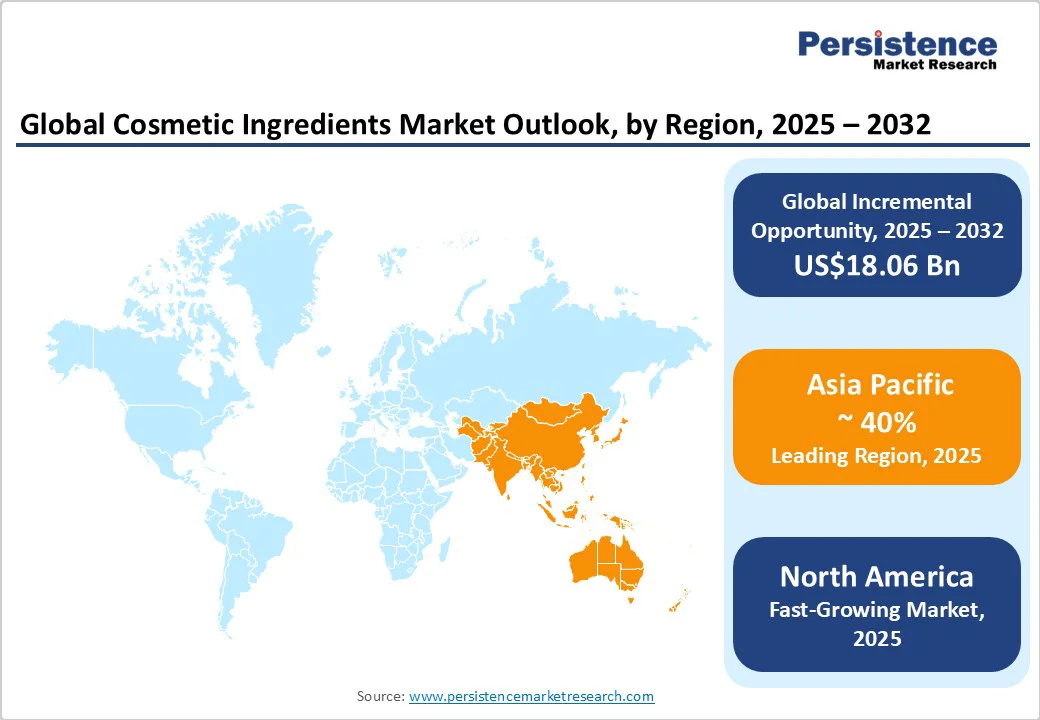

- Leading Region: Asia Pacific, accounting for approximately 40% of the global market share in 2025, driven by high consumption and large-scale manufacturing.

- Fastest-growing Region: North America; projected CAGR of 6-7% through 2032, fueled by premium skincare adoption and clinical-claim-driven ingredients.

- Investment Plans: Expansion of local manufacturing footprints, R&D partnerships, and joint ventures in APAC and Europe; aimed at accessing raw materials and accelerating innovation.

- Dominant Ingredient Type: Surfactants & Emulsifiers holding 29% of the market due to wide usage across cleansing, emulsions, and rinse-off formats.

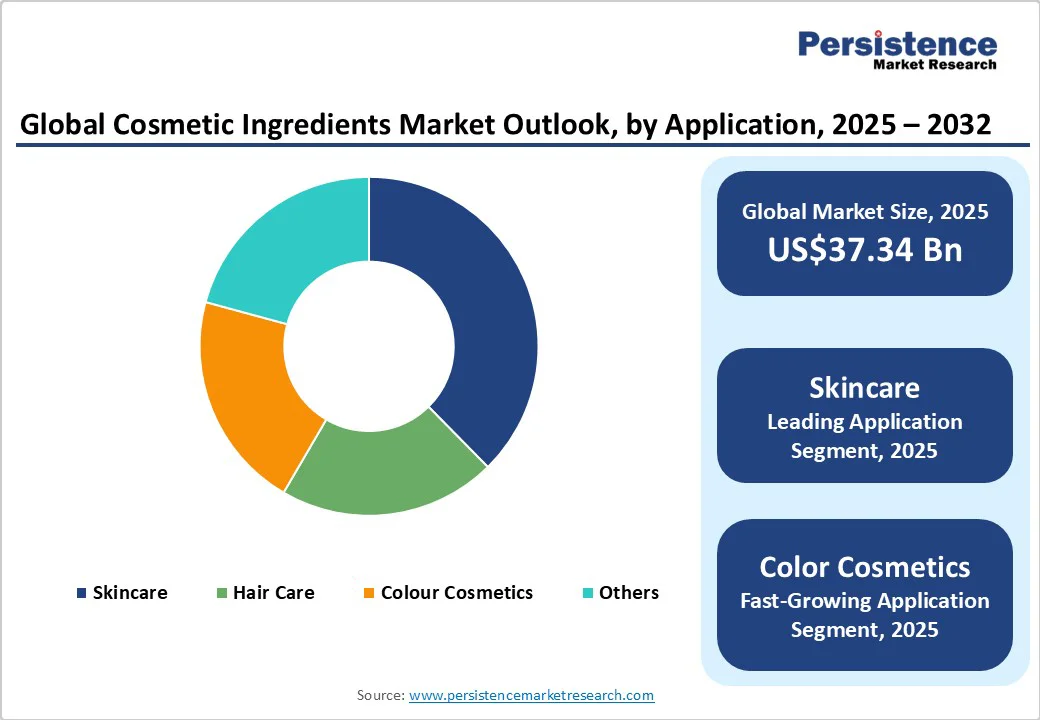

- Leading Application: Skincare, representing the largest application share at 38%, with high active ingredient penetration and premiumization trends.

| Key Insights | Details |

|---|---|

| Cosmetic Ingredients Market Size (2025E) | US$37.34 Bn |

| Market Value Forecast (2032F) | US$55.4 Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.8% |

| Historical Market Growth (CAGR 2019 to 2024) | 5.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising demand for active, multifunctional ingredients & natural/biotech substitution

Consumers are shifting from commodity ingredients to functional actives that deliver measurable skincare outcomes. The global skincare boom is driving ingredient sophistication: active ingredients accounted for a rapidly rising share of formulators’ spend in 2022-2024, and market estimates place the active-ingredients segment among the faster-growing submarkets (mid-single to high-single digit CAGR). This elevates average selling prices and opens repeat-purchase, claim-driven revenue for suppliers who can back claims with clinical/analytical data.

Brands and regulators are accelerating the removal of problematic chemistries and replacing them with bio-derived, biodegradable, or upcycled ingredients. Large ingredient companies are launching natural-based lines and biodegradable emulsifiers and acquiring biotech actives to meet demand. Sustainable ingredient premiums (performance + ecolabeling) are driving value growth even where unit volumes rise modestly.

Asia Pacific is the largest regional market for cosmetics and a major manufacturing/export hub; higher household incomes and accelerated e-commerce adoption translate into faster ingredient consumption per capita. Regional manufacturing scale (oleochemical feedstock access, lower production costs) supports both commodity and premium ingredient supply chains, fueling global demand and competitive pricing dynamics.

Regulatory Complexity and Testing Burden and Supply Chain Constraints

The EU’s Cosmetics Regulation (EC) No. 1223/2009 and tighter enforcement on contaminants (PFAS, asbestos in talc) increase pre-market safety and post-market surveillance costs for suppliers and brand formulators. In the U.S., regulatory proposals under MoCRA increase compliance costs and create product-reformulation risk. These regulatory costs disproportionately affect smaller suppliers, slow time-to-market for novel actives, and can erode margins.

Key ingredient feedstocks (plant oils, specialty fatty acids, fermentation feedstocks) are price-sensitive to agricultural cycles and energy costs. Supply interruptions (logistics, tariffs, regional crop shortfalls) can raise costs or force formulators to reformulate, compressing margins or delaying launches. Short-term capex increases for traceability/certification also act as a headwind.

Biotech-Derived Actives and Claimable Science And Sustainable Formulation Platforms

Biotechnology (fermentation, enzymatic conversion) enables novel, traceable actives with clinical evidence (microbiome modulators, peptides). These ingredients command premium pricing and recurring revenue through demonstrated efficacy.

The active ingredients submarket will be a key value driver through 2032. Suppliers that combine robust safety dossiers with clinical efficacy data and traceable analytics are well-positioned to capture significant value. Early movers can secure partnerships with prestige brands seeking differentiated claims and science-backed innovation.

Demand for biodegradable emulsifiers, upcycled by-products, and low-carbon ingredients offers addressable revenue in both mass and premium tiers. Several large suppliers launched natural/biodegradable emulsifier lines in 2024-2025, showing how new product introductions convert into immediate buyer interest, an opportunity to re-price ingredient mixes, and extend margin.

Category-wise Analysis

Ingredient Type Insights

Surfactants and emulsifiers remain the largest segment by revenue, accounting for approximately 29% of the overall market in 2025. Their widespread use across cleansing products, emulsions, lotions, creams, and rinse-off formulations ensures high volume consumption.

Large-scale adoption in personal care, hair care, and baby care products drives consistent demand. Commodity pricing compresses margins; however, the sheer scale of usage maintains revenue dominance. Surfactants also include specialty mild surfactants for sensitive skin, which are increasingly integrated into premium formulations, adding incremental value to this segment.

Actives, including peptides, botanical extracts, vitamins, antioxidants, and microbiome modulators, are the fastest-growing ingredient category. Growth is fueled by product premiumization, efficacy-driven claims, and the rising consumer preference for scientifically validated skincare solutions.

R&D investment and clinical validation support higher ASPs and recurring revenue streams. Emerging niches such as microbiome-friendly ingredients, multifunctional peptides, and delivery-system innovations are creating new application avenues across both mass-market and prestige brands.

Application Insights

Skincare accounts for the largest segment with a market share of 38% in 2025, due to high per-capita expenditure and sustained premiumization trends. Anti-aging, brightening, and hydration-focused products dominate the category, driving demand for functional ingredients such as peptides, hyaluronic acid, ceramides, and antioxidants.

Skincare formulations integrate multiple actives with carrier systems, which increase ingredient density and per-kg value. Growth is further reinforced by increasing male skincare adoption, premium e-commerce channels, and personalization trends, making skincare a consistently high-value application segment.

The convergence of color cosmetics and skincare is accelerating ingredient adoption in foundations, BB/CC creams, cushions, and lip products enriched with peptides, antioxidants, and hydrating actives. This hybrid trend has expanded the scope for functional ingredients, increasing both volume and ASPs per SKU. The segment is particularly strong in Asia Pacific and North America, where younger consumers prioritize multifunctional makeup.

Source Insights

Synthetic ingredients, including many surfactants, preservatives, and stabilizers, account for 61% of the market in 2025 due to cost-effectiveness, consistency, and scalability. Large formulators rely on synthetics for standardization across mass-market products, ensuring supply stability and formulation reliability. Synthetic polymers, silicones, and emulsifiers support multifunctional claims such as water-resistance, viscosity control, and texture enhancement in diverse applications.

Natural and biotech-derived ingredients are experiencing the fastest growth, driven by consumer preference for “clean beauty,” ecolabeling, and stricter regulatory requirements on chemical usage. Botanical extracts, plant oils, and fermentation-derived actives are increasingly used across premium skincare, color cosmetics, and hair care. Growth rates for natural/bioactives often exceed the market average in leading regions. Companies investing in certified supply chains and documentation benefit from both preferential brand partnerships and pricing premiums.

Regional Insights

North America Cosmetic Ingredients Market Trends - Science-Led Innovation and Premium Ingredient Demand

North America is a high-value market for cosmetic ingredients, with the U.S. contributing approximately 85% of the total revenue share. The market is driven by strong consumer preferences for scientifically backed skincare, high brand recognition, and significant disposable incomes.

These factors support growing demand for premium actives, multifunctional ingredients, and advanced delivery systems. While the regulatory environment, including oversight by the FDA and compliance with the Modernization of Cosmetics Regulation Act (MoCRA), adds to operational costs, it also reinforces consumer confidence in product safety and efficacy.

Growth is fueled by substantial investments in research and development from both established players and emerging innovators. There is increasing adoption of clinically substantiated claims and multifunctional formulations, as consumers seek convenience without compromising on performance. E-commerce, direct-to-consumer (DTC) models, and private-label expansion are also accelerating ingredient turnover and encouraging rapid product innovation.

Investment activity in the region reflects a strong push toward innovation, including the acquisition of science-driven startups, expansion of formulation and testing capabilities, and collaborative partnerships aimed at fast-tracking development cycles. There is also growing emphasis on sustainable sourcing and biotechnology-based ingredients, aligned with evolving consumer values.

Europe Cosmetic Ingredients Market Trends - Regulation-Driven Quality and Sustainable Ingredient Focus

Europe remains a value-driven market shaped by both high consumer expectations and one of the most stringent regulatory environments globally. Regulation (EC) No. 1223/2009 plays a pivotal role by restricting the use of certain chemicals and mandating full transparency in product safety. The region’s core markets, Germany, France, the U.K., and Spain, are characterized by strong demand for skincare and prestige cosmetics, with deep ingredient penetration across product categories.

Consumer preferences in Europe increasingly lean toward natural, clinically validated, and sustainably sourced ingredients. High-end brands continue to set the pace, fostering a demand for advanced actives that deliver proven results. The regulatory landscape supports these trends by promoting quality assurance and long-term consumer trust.

To align with regulatory requirements and consumer preferences, many organizations are directing R&D resources into European hubs. These efforts often focus on developing green chemistry platforms, sustainable ingredient lines, and novel actives derived from biotechnology or plant-based sources. Collaborations with research institutions and innovation-driven enterprises are also growing, supporting a steady pipeline of compliant and market-relevant product solutions.

Asia Pacific Cosmetic Ingredients Market Trends - High Consumption Backed by Local Trends and Rapid Innovation

Asia Pacific leads the global market in cosmetic ingredient consumption, accounting for nearly 40% of the global market share. Market growth is driven by rapid urbanization, increasing disposable incomes, and the rise of middle- and upper-income consumers. Local beauty movements such as K-beauty in Korea, J-beauty in Japan, and C-beauty in China are influencing global trends and contributing to rising ingredient demand, especially in skincare, hair care, and multifunctional cosmetics.

The region benefits from cost-efficient manufacturing, access to abundant raw materials, and strong digital infrastructure, which together support the rapid launch and scaling of new products. Clean-label, natural, and functional ingredients are gaining traction across both mass-market and premium segments, as consumer awareness of product composition continues to grow.

Investment efforts are increasingly directed at strengthening local R&D capabilities, establishing regional innovation hubs, and advancing ingredient technologies such as fermentation-based actives and botanical extractions. These activities aim to accelerate responsiveness to fast-changing consumer preferences while leveraging regional expertise in traditional and holistic beauty approaches.

Competitive Landscape

The global cosmetic ingredients market combines consolidation among top-tier players with fragmentation in specialized niches. Leading chemical companies dominate through scale, global supply chains, and regulatory expertise, enabling efficient ingredient launches and strong brand associations. Their R&D and procurement strengths support consistent innovation and cost advantages.

In contrast, niche players, including biotech start-ups and botanical extractors, focus on premium, performance-driven ingredients such as microbiome-friendly actives and multifunctional peptides. Their agility allows rapid adaptation to consumer trends and regulatory shifts, catering to high-end brands with tailored, clinically validated solutions.

Strategic growth is driven by acquisitions, co-development with biotech firms, and geographic expansion, particularly in Asia Pacific, via joint ventures and local manufacturing. Sustainability is a key focus, with increasing investments in bio-based, biodegradable, and low-carbon ingredients to meet clean-label demand and regulatory standards.

Key Industry Developments

- In October 2024, BASF launched Emulgade Verde, a line of naturally based emulsifiers designed to support biodegradable, mild formulations. These emulsifiers enable brands to make “green” product claims while also contributing to energy-efficient manufacturing processes.

- In July 2023, Evonik acquired Novachem, which strengthens Evonik’s sustainable actives portfolio and Latin America access and secures biotech actives and speeds time-to-market.

Companies Covered in Cosmetic Ingredients Market

- BASF SE

- Evonik Industries

- Croda International plc

- Givaudan/IFF

- Symrise AG

- Lonza Group

- Dow/DuPont

- Solvay SA

- Clariant AG

- DSM (Royal DSM)

- Ashland Inc.

- Kao Corporation

- Eastman Chemical Company

- Chr. Hansen Holding A/S

- Lubrizol Corporation

- Inolex Chemical Company

- Merck KGaA

- Seppic SA

- Kerry Group

- Active Concepts

Frequently Asked Questions

The cosmetic ingredients market size was valued at US$37.34 Bn in 2025.

The cosmetic ingredients market is projected to reach US$55.4 Bn by 2032.

Key trends include the rising demand for bioactives and multifunctional ingredients, the growth of natural and bio-derived ingredients, premium skincare formulations, and sustainability-driven ingredient replacement.

By ingredient type, Surfactants & Emulsifiers are the leading segment, accounting for approximately 29% of the market. By application, Skincare dominates with a 38% market share.

The cosmetic ingredients market is expected to grow at a CAGR of 5.8% between 2025 and 2032.

Key players include BASF SE, Evonik Industries, Croda International plc, Givaudan/IFF, and Symrise AG.