- Healthcare Services

- Cosmetic Procedures Market

Cosmetic Procedures Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Cosmetic Procedures Market by Procedure Type (Surgical Procedures, and Non-Surgical Procedures), End-user (Hospitals, Office-based Facilities, Ambulatory Surgical Centers), and Regional Analysis, from 2026 to 2033

Cosmetic Procedures Market Share and Trends Analysis

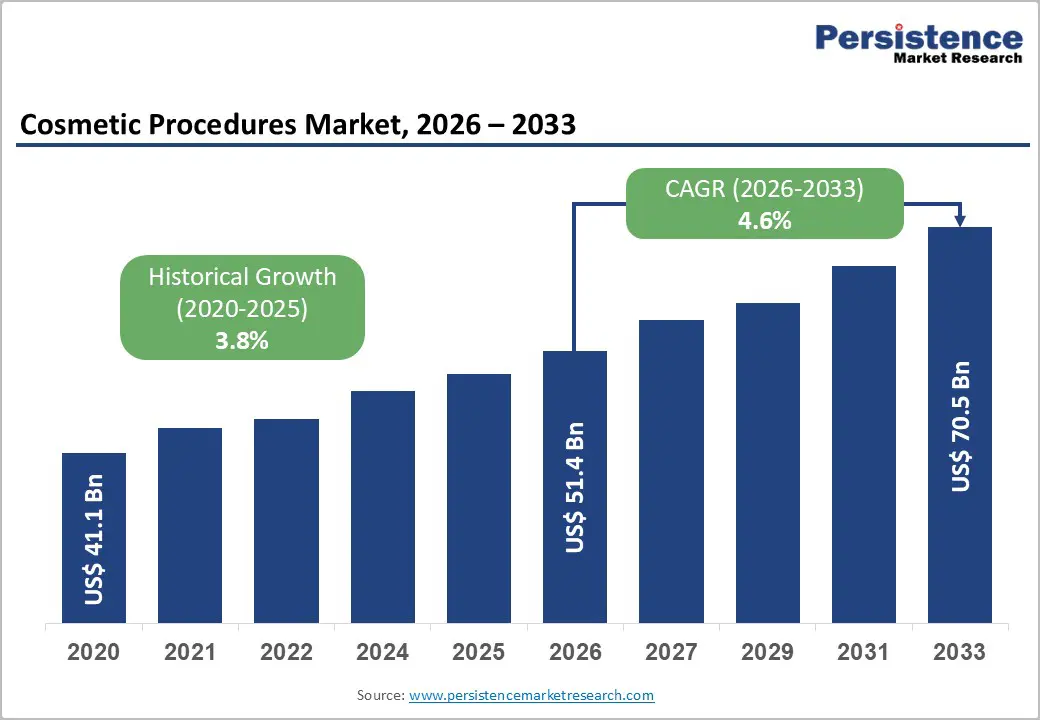

The global cosmetic procedures market size is likely to be valued at US$ 51.4 billion in 2026 and projected to reach US$ 70.5 billion by 2033 growing at a CAGR of 4.6% during the forecast period from 2026 to 2033.

The global market has experienced steady growth over the past decade, driven by increasing aesthetic awareness, rising disposable income, and wider acceptance of appearance-enhancing treatments. Both surgical and non-surgical procedures are gaining traction as consumers seek solutions that enhance physical appearance and support confidence and well-being. Technological advancements in devices, injectables, and treatment techniques have improved safety, precision, and outcomes, encouraging higher adoption across diverse age groups.

Key Industry Highlights

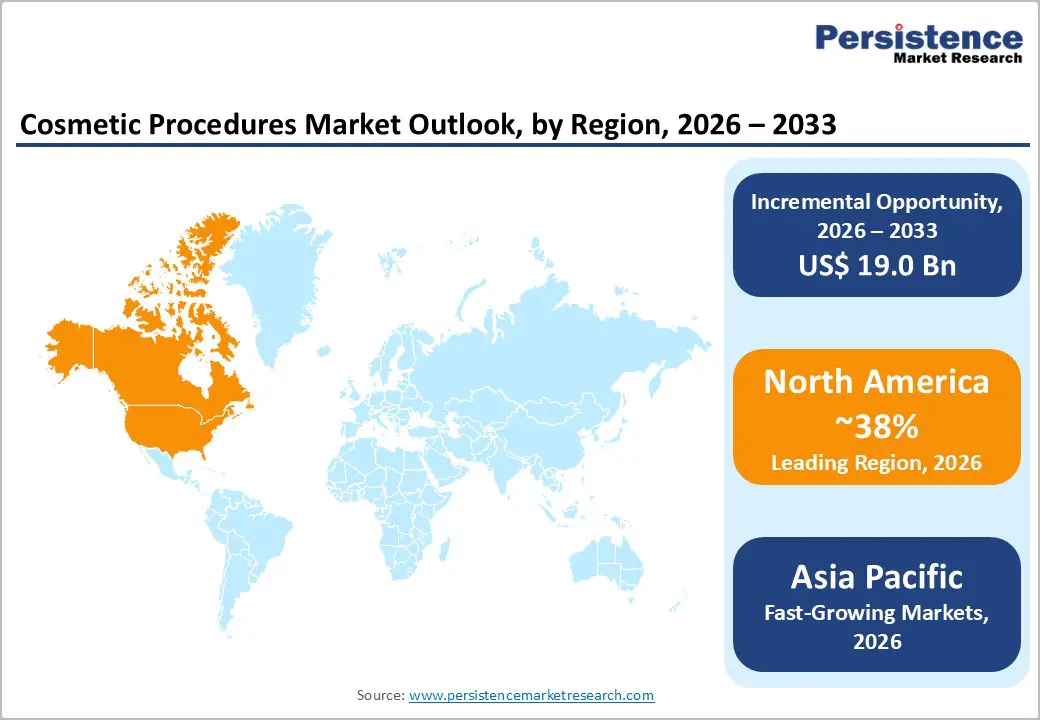

- Leading Region: North America remains the leading region in the cosmetic procedures market, supported by strong consumer spending, high adoption of minimally invasive treatments, and a robust ecosystem of board-certified specialists and advanced clinics.

- Fastest Growing Region: Asia Pacific is expected to be the fastest-growing region, driven by expanding middle-class populations, rapid urbanization, established cosmetic surgery hubs such as South Korea and India, and the rise of medical tourism for aesthetic services.

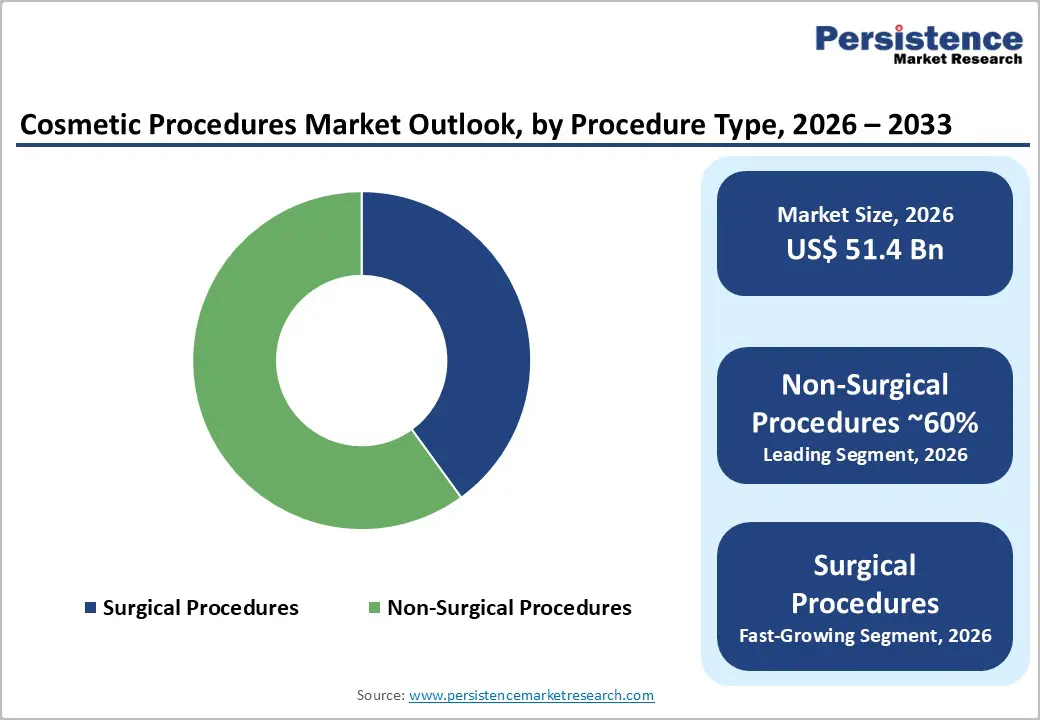

- Dominant Segment: Non-Surgical Procedures dominate with about 60% share in 2025, reflecting global preference for injectables, facial rejuvenation, and device-based treatments that offer strong results with minimal downtime.

- Fastest Growing Segment: Ambulatory Surgical Centers are expanding rapidly due to cost efficiency, shorter recovery times, and rising outpatient cosmetic procedures.

| Key Insights | Details |

|---|---|

| Cosmetic Procedures Market Size (2026E) | US$ 51.4 Bn |

| Market Value Forecast (2033F) | US$ 70.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.6% |

| Historical Market Growth (CAGR 2020 to 2024) | 3.8% |

Market Dynamics

Driver - Surge in Minimally Invasive and Non-Surgical Aesthetics

The global cosmetic procedures market is being strongly driven by the growing preference for minimally invasive and non-surgical aesthetic treatments that deliver noticeable results with minimal recovery time. Procedures such as botulinum toxin injections, dermal fillers, chemical peels, and laser-based skin resurfacing have gained widespread acceptance due to their lower risk profile and convenience compared to surgical interventions. Industry data from organizations such as ISAPS and the American Society of Plastic Surgeons indicate consistent year-on-year growth of approximately 7% in minimally invasive procedures, reflecting changing patient expectations toward safer and faster aesthetic solutions. These treatments appeal to a broad demographic, including younger consumers seeking preventive aesthetics and older individuals looking for subtle rejuvenation.

In 2023, ISAPS reported over 19 million non-surgical cosmetic procedures performed globally, surpassing surgical volumes and highlighting a clear shift in patient preference. Continuous innovation in injectable formulations, energy-based devices, and combination treatment protocols has further improved safety, precision, and duration of results. This progress has increased repeat treatment rates and expanded the addressable patient base. As accessibility improves and outcomes become more predictable, non-surgical aesthetics continue to drive higher procedure volumes, reinforcing their dominant contribution to overall cosmetic market revenues.

Restraints - Safety Risks, Complications, and Workforce Limitations

Despite strong market momentum, safety risks and workforce limitations remain key restraints in the cosmetic procedures market. While complication rates are low when treatments are performed by trained professionals, the rapid growth of non-medical providers and unregulated clinics has increased adverse events. According to professional society reviews, complications related to injectables such as dermal fillers and botulinum toxin account for over 60% of reported aesthetic adverse events, often linked to improper technique or lack of anatomical expertise. Energy-based devices also pose risks of burns, scarring, and pigment changes when misused, undermining patient trust and attracting regulatory scrutiny.

Workforce shortages further limit safe market expansion. ISAPS data indicate that more than 70% of board-certified plastic surgeons are concentrated in North America and Europe, leaving emerging regions underserved. In low- and middle-income countries, limited access to trained specialists restricts procedure volumes and increases reliance on underqualified providers. Inconsistent regulatory enforcement and gaps in standardized training programs slow capacity expansion, making patient safety a critical constraint on sustained market growth.

Opportunity - Expansion of Non-Surgical Technologies and Injectables

The rapid expansion of non-surgical technologies and injectable treatments represents a major growth opportunity for the cosmetic procedures market. According to ISAPS, over 19 million non-surgical cosmetic procedures were performed globally in 2023, accounting for more than 55% of total aesthetic procedures. Botulinum toxin and dermal fillers alone represent the largest share, with injectables growing at an estimated 6-8% annually. Continuous improvements in filler longevity, toxin formulations, and biostimulatory injectables are enhancing outcomes while reducing complication risks.

Technological advances in energy-based devices, including lasers, radiofrequency, and ultrasound systems, are also expanding treatment indications. These platforms support combination therapies, increasing repeat visit rates and lifetime patient value. Short treatment durations, minimal downtime, and office-based delivery models make non-surgical aesthetics accessible to younger consumers and working professionals. As acceptance of preventive and maintenance aesthetics rises, non-surgical technologies are expected to remain the primary driver of future revenue growth across global markets.

Category-wise Analysis

By Procedure Type Insights

Non-surgical procedures are expected to dominate the cosmetic procedures market, accounting for nearly 60% of total market share in 2025. Global data from aesthetic societies indicate that treatments such as botulinum toxin injections, dermal fillers, and skin resurfacing significantly exceed surgical volumes. In 2023, more than 19 million non-surgical procedures were performed worldwide, compared with approximately 15.8 million surgical interventions. This preference is driven by shorter recovery periods, lower perceived risk, and greater affordability. Non-surgical options allow individuals to enhance or maintain appearance through gradual, repeated treatments rather than undergoing invasive surgery. Ongoing innovation in injectables and energy-based technologies, including laser, radiofrequency, and ultrasound systems, continues to improve results and safety. These factors position non-surgical procedures as a core revenue driver for clinics, medspas, and office-based providers focused on recurring patient engagement.

By End-user Insights

Hospitals are projected to account for about 72% of the cosmetic procedures market in 2025, reflecting their central role in delivering complex surgical and high-value aesthetic treatments. Hospital-based plastic surgery departments provide comprehensive care, including advanced diagnostics, anesthesia support, inpatient monitoring, and complication management, which is critical for procedures such as body contouring and breast surgery. Many leading aesthetic surgeons operate within accredited hospitals to comply with strict safety and regulatory standards. Hospitals are also expanding their aesthetic offerings by integrating minimally invasive services such as injectables, laser therapies, and skin rejuvenation treatments. This blended model enables hospitals to address a wide range of patient needs while maintaining quality and safety. Although office-based clinics and ambulatory surgical centers continue to grow for lower-risk procedures, hospitals remain the primary setting for high-complexity cosmetic care.

Region-wise Insights

North America Cosmetic Procedures Market Trends

North America, led by the U.S., is projected to remain the largest regional market for cosmetic procedures, supported by high per capita expenditure on aesthetic services, strong consumer awareness, and a dense network of board-certified plastic surgeons and dermatologists. The American Society of Plastic Surgeons (ASPS) 2023 Procedural Statistics report documented a 5% rise in cosmetic surgeries and a 7% increase in minimally invasive procedures compared with the prior year, underscoring sustained demand despite economic uncertainty. Popular treatments include liposuction, breast augmentation, tummy tucks, and eyelid surgery on the surgical side, and botulinum toxin type A, dermal fillers, and laser skin resurfacing among minimally invasive options.

Regulatory oversight from bodies such as the U.S. Food and Drug Administration (FDA) ensures rigorous evaluation of implants, injectables, and energy-based devices, supporting patient safety and fostering innovation in technologies like next-generation fillers and non-invasive fat reduction. North America also benefits from well-developed training pathways, professional societies, and industry-supported education, which maintain high procedural standards and facilitate rapid adoption of new techniques. Additionally, the rise of integrated medspa models and subscription-based injectables programs broadens access, reinforcing the region’s leadership position in the global cosmetic procedures market.

Asia Pacific Cosmetic Procedures Market Trends

Asia Pacific is anticipated to be the fastest-growing region in the cosmetic procedures market, driven by large populations, rising disposable incomes, and cultural acceptance of aesthetic enhancement. China, Japan, South Korea, and India are key growth engines, with high demand for facial contouring, eyelid surgery, rhinoplasty, and skin-brightening treatments. South Korea, for example, is renowned as a global hub for cosmetic surgery, attracting international patients seeking advanced facial and body procedures, while Japan and China record strong uptake of minimally invasive treatments tailored to local beauty preferences.

Manufacturing and cost advantages across Asia Pacific support the availability of competitively priced implants, lasers, and injectables, enabling clinics to offer a wide range of services to domestic and foreign patients. Academic articles highlight that aesthetic plastic surgery in India is poised for exponential growth, fueled by expanding middle-class awareness, social media influence, and a growing base of skilled surgeons. Governments and tourism boards promoting medical travel, combined with investment in international accreditation and English-speaking staff, further solidify Asia Pacific’s position as a rapidly expanding and increasingly sophisticated hub for cosmetic procedures.

Competitive Landscape

The cosmetic procedures market is moderately fragmented, featuring a mix of global aesthetics companies, implant manufacturers, laser and energy-device providers, and pharmaceutical firms specializing in neuromodulators and fillers. Leading players such as Allergan, Plc, Mentor Worldwide LLC (Johnson & Johnson Services, Inc.), GC Aesthetics, Sientra, Inc., Polytech Health & Aesthetics GmbH, HansBiomed Co., Ltd, Galderma S.A., and Cutera, Inc. compete through differentiated product portfolios, safety data, and physician training programs. Strategic priorities include geographic expansion into high-growth emerging markets, development of next-generation implants and bioengineered tissues, and continuous innovation in minimally invasive platforms such as lasers, radiofrequency, and focused ultrasound. Many companies also support digital engagement tools and loyalty programs that help clinics build recurring treatment plans and long-term patient relationships.

Key Industry Developments:

- In July 2025, Mumbai’s government-run Cama and Albless Hospital will become Maharashtra’s first to launch a dedicated gyno-cosmetic unit, offering intimate cosmetic procedures at subsidized rates.

- In April 2023, Allergan Aesthetics collaborated with the American Society of Plastic Surgeons, The Aesthetic Society, and the American Hernia Society to strengthen its global brand presence.

Companies Covered in Cosmetic Procedures Market

- Allergan, Plc

- Mentor Worldwide LLC (Johnson & Johnson Services, Inc.)

- GC Aesthetics

- Sientra, Inc

- Polytech Health & Aesthetics GmbH

- HansBiomed Co., Ltd

- Galderma S.A.

- Alma Lasers Ltd. (Shanghai Fosun Pharmaceuticals Ltd.)

- Merz Pharma GmbH & Co. KGaA

- Cutera, Inc

- Anika Therapeutics, Inc.

- Valeant Pharmaceuticals International, Inc.

- Syneron Medical Ltd.

- Cynosure Inc. (Hologic Inc.)

- Others

Frequently Asked Questions

The global cosmetic procedures market is projected to be valued at US$ 51.4 Bn in 2026.

Growing demand for aesthetic enhancement, aging demographics, technological advancements, improved safety profiles, and rising acceptance of cosmetic treatments.

The global market is expected to witness a CAGR of 4.6% between 2026 and 2033.

Emerging market expansion, minimally invasive procedure adoption, personalized aesthetic solutions, male consumer growth, and advanced device innovations.

North America is the leading region in the global cosmetic procedures market.