- Processed Food

- Coffee Grounds Market

Coffee Grounds Market Size, Share, and Growth Forecast, 2026 - 2033

Coffee Grounds Market by Application (Agriculture & Horticulture, Food & Beverage, Cosmetics & Personal Care, Bioenergy & Biofuels, Materials & Industrial Products, Construction Materials, Others), Product Type (Fresh, Spent, Processed/Upcycled), Source (Households, Commercial Foodservice, Industrial Processing Facilities, Agricultural Processing Residues), and Regional Analysis for 2026 - 2033

Coffee Grounds Market Share and Trends Analysis

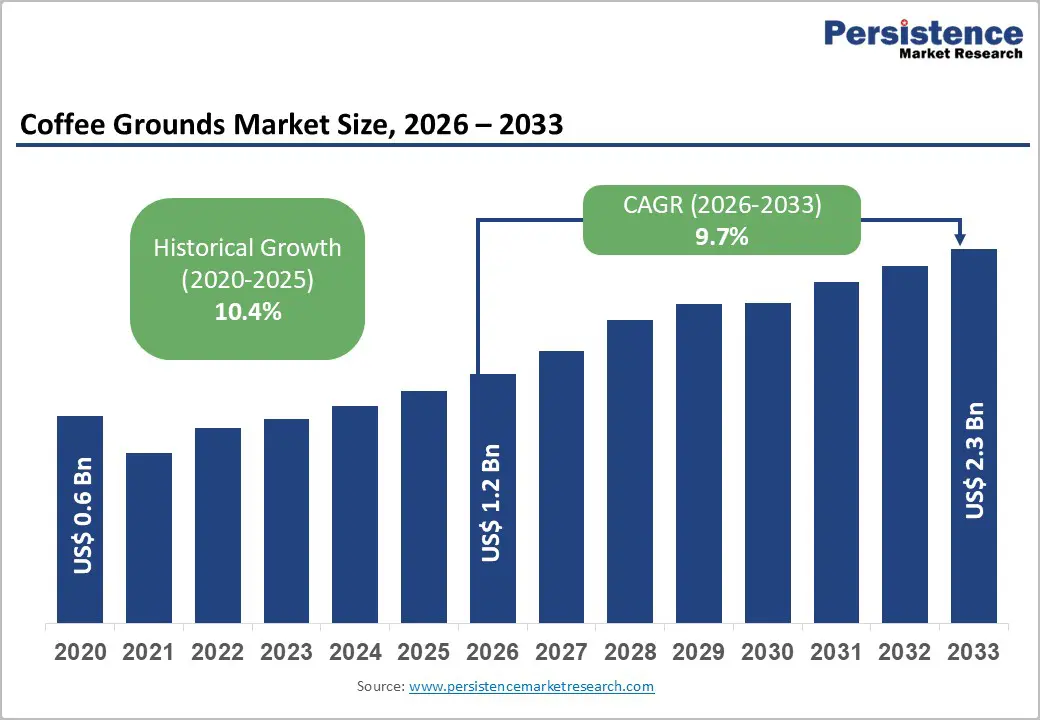

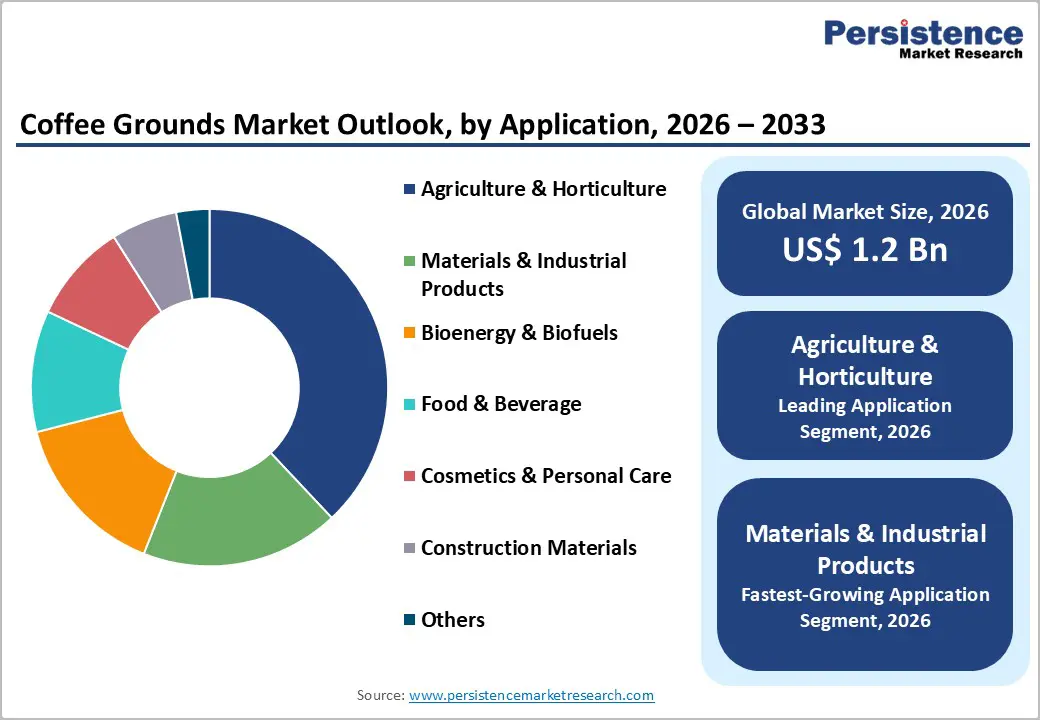

The global coffee grounds market size is likely to be valued at US$ 1.2 billion in 2026, and is projected to reach US$ 2.3 billion by 2033, growing at a CAGR of 9.7% during the forecast period 2026 - 2033.

The market is gathering traction as waste valorization economics are improving and regulatory pressure on organic waste diversion is strengthening across major consumption regions. The growth trajectory of the market reflects the transition of coffee waste from low-value applications such as composting toward higher-margin uses including industrial materials, bioenergy feedstock, and functional ingredients. Rising global coffee consumption is continuing to support this shift by increasing the availability of recoverable biomass. The International Coffee Organization (ICO) reports annual consumption exceeding 170 million 60-kilogram bags. As supply volumes expand and processing technologies advance, companies are gaining greater confidence in developing scalable business models that convert organic waste into commercially valuable products.

Market acceleration is also being reinforced by policy-driven circular economy initiatives and corporate sustainability commitments across industries. Regulatory frameworks such as the European Union (EU) waste directives and landfill diversion programs, combined with national bioeconomy strategies in North America and Asia Pacific, are encouraging businesses to commercialize organic waste streams rather than dispose of them. Technological advancements in biomass processing methods such as pyrolysis, solvent extraction, and biopolymer integration are further improving conversion efficiency and expanding the range of viable end-use applications beyond agriculture. Commercial adoption is increasingly shifting toward structured industrial supply chains, with multinational foodservice companies forming partnerships with recycling firms to monetize waste streams and achieve environmental targets.

Key Industry Highlights

- Application Leadership: Agriculture and horticulture applications are estimated to account for around 38% of global revenues in 2026, driven by low processing requirements and established demand for organic soil amendments.

- Fastest-growing Application: Materials and industrial products are expected to expand the fastest at approximately 13% CAGR through 2033, supported by rising demand for bio-composites and sustainable packaging materials.

- Source Concentration: Commercial foodservice establishments are projected to contribute nearly 46% of supply in 2026, reflecting centralized waste generation from café chains and institutional brewing systems.

- Regional Dominance: North America is expected to dominate with an estimated 34% market share in 2026, supported by high coffee consumption volumes, while Asia Pacific is projected to be the fastest-growing market at about 12% CAGR, owing to expanding café culture.

- Technology Trends: Increasing investment in extraction, pyrolysis, and composite processing technologies is enabling a transition from low-value compost uses toward higher-margin industrial and functional ingredient applications.

- October 2025: Researchers at the University of Sharjah, UAE, patented a technology that converts spent coffee grounds and plastic waste into porous activated carbon capable of capturing carbon dioxide from industrial emissions.

| Key Insights | Details |

|---|---|

| Coffee Grounds Market Size (2026E) | US$ 1.2 Bn |

| Market Value Forecast (2033F) | US$ 2.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 9.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 10.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Circular Economy Regulations to Accelerate Organic Waste Valorization

Governments are tightening landfill diversion regulations, widening both the availability of organic waste feedstock and the economic viability of coffee grounds recovery. The EU Waste Framework Directive requires member states to establish separate bio-waste collection systems, which is formalizing supply channels for organic residues generated by households and commercial establishments. In the U.S., the Environmental Protection Agency (EPA) is advancing landfill diversion objectives through its Sustainable Materials Management (SMM) program, which is encouraging municipalities and businesses to adopt waste recovery solutions. At the global level, the United Nations Environment Programme (UNEP) is prioritizing organic waste reduction to mitigate methane emissions, a greenhouse gas with significantly higher warming potential than carbon dioxide. These coordinated policy actions are progressively converting organic waste streams into regulated resource pools rather than unmanaged disposal burdens.

The evolving regulatory landscape is also reshaping cost structures and investment behavior across the coffee value chain. Coffee retailers and foodservice operators are reducing landfill disposal fees by participating in structured collection programs, while recyclers and processors are generating new revenue streams from recovered biomass. Companies are entering multi-year supply agreements with waste management firms, which are stabilizing feedstock availability and lowering procurement risk for downstream manufacturers. This supply certainty is supporting capital deployment into drying, extraction, and thermal processing infrastructure that would otherwise face utilization risks.

Rising Coffee Consumption to Increase Secondary Biomass Supply

Global coffee consumption is expanding steadily, particularly across Asia Pacific and rapidly urbanizing economies where changing lifestyles and income growth are increasing demand for specialty beverages. The ICO is reporting sustained consumption growth supported by urban population expansion, rising disposable income, and the proliferation of café chains in metropolitan areas. This trend is directly influencing the generation of secondary biomass because each kilogram of brewed coffee is producing approximately 0.9 to 1.2 kilograms of spent coffee grounds. As consumption volumes increase, the availability of recoverable organic material is rising proportionally, creating a predictable and scalable feedstock base for recycling and industrial utilization. China, India, Indonesia, and Vietnam are contributing significantly to incremental demand, and these countries are facing increasing waste management pressures, which is strengthening the economic rationale for organized recovery systems.

The expanding volume of spent grounds is enabling operational efficiencies across the recycling ecosystem and is improving the investment attractiveness of downstream applications. Large coffee chains and beverage manufacturers are consolidating waste collection logistics through centralized procurement and distribution networks, which is reducing supply fragmentation and improving material consistency. This structural improvement in supply reliability is lowering operational risks for processors and is supporting the development of industrial-scale conversion facilities such as bioenergy plants and biomaterial manufacturing units. Investors are increasingly allocating capital toward higher-margin applications including biofuels, carbon materials, and composite products, where predictable feedstock supply is essential for achieving acceptable returns on investment.

Collection Logistics and Moisture Management to Spike Processing Costs

Spent coffee grounds hold 60-80% moisture content, which raises transportation expenses substantially and reduces storage life. Processors therefore dry or stabilize the material before industrial applications such as fertilizers or cosmetics, yet these steps demand extra energy and heighten operational demands. Food and Agriculture Organization (FAO) benchmarks for biomass handling reveal that moisture control consumes 30-40% of total processing budgets for organic waste, pushing companies to seek cost-efficient technologies now and invest in automation by 2030.

Supply chains for coffee grounds remain scattered because thousands of small cafés produce them without centralized hubs. Regions still build aggregation networks, so providers struggle to achieve volume efficiencies that lower per-unit costs. New businesses thus face delayed returns on investment alongside elevated upfront funding needs, compelling stakeholders to partner with waste collectors today for streamlined flows that ensure profitability in the coming years.

Regulatory Classification of Waste Materials Is Creating Compliance Barriers

Authorities across various jurisdictions classify spent coffee grounds as waste instead of raw material. This categorization allows them to impose strict rules for transport, storage, and processing. As a result, businesses are forced to secure waste handling permits, environmental clearances, and safety certifications, which elevate paperwork demands and extend project launch timelines. Differences in these classifications across regions hinder international shipments, prompting firms to standardize compliance strategies now for smoother global operations by 2030.

Food and cosmetic sectors encounter extra oversight on contaminants and microbial risks, so companies conduct rigorous testing that boosts expenses and delays product launches. Startups with tight budgets find these demands especially tough to meet, given their operational and financial constraints, slowing their entry and progress in premium markets. Leaders are thus prioritizing early regulatory expertise today to accelerate innovation and capture high-value opportunities in the years ahead.

Bio-Materials and Construction Applications to Unlock High-Margin Growth

Research is increasingly confirming that biochar produced from spent coffee grounds is enhancing concrete performance while reducing the amount of cement required in construction mixtures. Cement manufacturing is contributing approximately 7.5% of global carbon dioxide (CO2) emissions, according to the International Energy Agency (IEA), and this environmental impact is creating strong incentives for alternative low-carbon additives. Coffee-derived biochar improves compressive strength and durability characteristics by enhancing microstructural bonding within cement matrices, which is making it attractive for sustainable construction applications. Construction firms and material developers are actively evaluating biomass-based fillers and supplementary cementitious materials as part of broader decarbonization strategies aligned with environmental regulations and corporate sustainability commitments. As governments are tightening carbon reporting standards and green building certification requirements, the demand for low-emission construction inputs is expected to rise across both developed and emerging markets.

The commercial potential of coffee-based construction materials is becoming significant as adoption barriers decline and performance validation improves. Companies that are establishing standardized processing methods, quality specifications, and performance certifications are positioning themselves to secure early market leadership because construction industries require consistent material reliability before large-scale adoption. Investors are increasingly allocating capital toward this segment due to its scalability, long product life cycles, and alignment with global decarbonization targets. Strategic partnerships between waste processors, construction material manufacturers, and infrastructure developers are likely to accelerate commercialization.

Functional Food Ingredients and Nutraceutical Extraction to Expand Value Capture

Spent coffee grounds contain substantial amounts of dietary fiber, antioxidants, and polyphenolic compounds, which are enabling their application in functional foods and nutraceutical formulations. These bioactive components are supporting product positioning related to digestive health, metabolic support, and antioxidant intake, making coffee grounds highly appealing for health-conscious consumers. Food manufacturers are actively incorporating coffee-derived flour and fiber additives into bakery products, snacks, and beverage formulations to meet consumer preferences for environmentally responsible and nutrient-dense ingredients. Regulatory acceptance is also improving as safety assessments and standardization efforts are progressing, which is strengthening commercialization pathways across developed markets.

This segment is offering considerably higher profit margins compared with traditional agricultural uses, as value creation is based on nutritional functionality. Processing technologies such as solvent extraction, enzymatic treatment, and controlled fermentation are improving compound recovery efficiency and product consistency, which is making large-scale production more economically viable. The combined food and nutraceutical opportunity could cross the half-billion market by 2033, powered by markets where consumers are prioritizing health-oriented and sustainable products. Companies that are investing in proprietary extraction methods, clinical validation, and regulatory compliance will likely gain competitive advantages. Strategic collaborations between ingredient suppliers, food manufacturers, and research institutions are expected to accelerate product innovation and expand market penetration over the forecast period.

Category-wise Analysis

Application Insights

Agriculture and horticulture applications are poised to command around 38% of the coffee grounds market revenue share in 2026. These applications require limited processing and are benefiting from well-established distribution channels. Coffee grounds are being utilized as soil conditioners, compost enhancers, and organic fertilizers due to their nitrogen content, micronutrients, and soil structure improvement properties. Adoption is particularly strong among commercial landscaping companies, greenhouse operators, and certified organic farming enterprises that are prioritizing sustainable soil inputs. The relatively low cost of conversion and immediate usability are supporting continued demand, especially in regions where organic waste diversion policies are encouraging agricultural reuse.

Materials and industrial products are set to be the fastest-growing segment with a projected 2026 - 2033 CAGR of 13.2%, driven by technological innovation and increasing sustainability requirements across manufacturing sectors. Coffee grounds are being incorporated into applications such as bioplastics, polymer composites, activated carbon, filtration media, and sustainable packaging materials. Manufacturers are developing standardized particle processing techniques and surface treatments that are improving compatibility with thermoplastic and resin systems, which is accelerating commercialization. Corporate commitments to reduce virgin plastic consumption and carbon emissions are encouraging adoption of biomass-derived fillers, while regulatory pressure on petrochemical materials is further strengthening the demand for renewable alternatives.

Source Insights

Commercial foodservice establishments are anticipated to lead in 2026, accounting for an estimated 46% of the coffee grounds market share, fueled by the generation of large volumes of consistently recoverable material by cafés, restaurants, and multinational coffee chains. These businesses are implementing centralized collection systems that are improving supply reliability and reducing contamination risks associated with mixed waste streams. Structured partnerships between foodservice operators and recycling companies are creating predictable feedstock pipelines, which are supporting long-term processing contracts and infrastructure investments. Material quality from commercial brewing environments is typically higher than household waste due to standardized preparation methods and controlled handling conditions, which is increasing suitability for industrial applications such as materials manufacturing and bioenergy conversion. Given the continued expansion of café chains and institutional beverage services globally, this segment is expected to maintain its leadership position through 2033.

Industrial processing facilities are likely to register the highest growth between 2026 and 2033, attributable to the concentration of waste generation at manufacturing sites. Instant coffee production and large-scale beverage processing operations are producing substantial quantities of spent grounds in centralized locations, which is significantly improving collection efficiency and reducing transportation costs compared with distributed retail sources. As multinational beverage companies are adopting zero-waste manufacturing strategies and circular production models, they are increasingly monetizing by-products through partnerships with bioenergy producers, agricultural input manufacturers, and biomaterial companies. The availability of large, consistent volumes is also enabling processors to achieve economies of scale and invest in advanced conversion technologies, which is accelerating the supply of feedstock for higher-value applications.

Regional Insights

North America Coffee Grounds Market Trends

North America is expected to account for approximately 34% of the coffee grounds market value in 2026. Strong coffee consumption patterns across the United States and Canada are sustaining regional leadership, while advanced waste management and recycling infrastructure are enabling efficient collection and processing of spent coffee grounds. Large coffee chains, institutional foodservice operators, and office beverage systems are generating substantial volumes of recoverable material, which companies are increasingly converting into inputs for agriculture, bioenergy, and materials manufacturing. Corporate sustainability commitments are encouraging retailers to establish partnerships with recycling firms to reduce landfill disposal and achieve environmental targets. The presence of established logistics networks and processing facilities is further strengthening supply chain reliability and supporting commercialization at scale.

Regulatory frameworks across the region are promoting landfill diversion, renewable energy adoption, and greenhouse gas reduction, which are accelerating market adoption and investment activity. Government incentives and environmental programs are encouraging biomass utilization and circular resource management, particularly in the United States and Canada. Venture capital firms and institutional investors are funding startups focused on biofuel production, advanced materials, and waste conversion technologies, which is fostering innovation and competitive differentiation. Stakeholders are likely to benefit from strategic collaborations that integrate regulatory incentives with scalable processing technologies.

Europe Coffee Grounds Market Trends

Europe is slated to hold roughly 29% of the global market for coffee grounds in 2026, supported by strong regulatory alignment with circular economy principles and resource efficiency policies. The European Green Deal is prioritizing waste reduction, carbon neutrality, and sustainable material innovation, while regional bioeconomy strategies are encouraging the commercialization of organic waste valorization technologies. Germany, the Netherlands, and the U.K. maintain advanced recycling infrastructure and are investing heavily in research related to biomass conversion and bio-based materials. Regulatory frameworks are also encouraging landfill diversion and industrial symbiosis initiatives, which are improving the availability of recoverable coffee waste streams for commercial utilization.

The Europe market is projected to expand at a moderate CAGR through 2033, driven by increasing consumer demand for sustainable products and continued public-sector investment in green technologies. Adoption is expanding across industries such as cosmetics, personal care, functional food ingredients, and biomaterials, where manufacturers are integrating recycled inputs to meet environmental performance targets. Government funding programs and research grants are accelerating the development of standardized processing technologies and scalable production models, which are improving commercialization speed. As sustainability regulations continue tightening and corporate environmental commitments expand, Europe is expected to remain a major global hub for technological advancement and market growth throughout the 2026-2033 forecast period.

Asia Pacific Coffee Grounds Market Trends

The market for coffee grounds in Asia Pacific is projected to record the highest CAGR of approximately 12.4% between 2026 and 2033, on account of surging coffee consumption and massive urbanization. China, India, South Korea, and Japan are expanding organized café networks and specialty beverage markets, which is increasing the volume of spent coffee grounds generated across metropolitan areas. High population density and increasing municipal waste pressures are encouraging governments and private stakeholders to adopt recycling and resource recovery initiatives to manage organic waste more efficiently. Urban waste management programs are increasingly integrating organic waste segregation, which is improving feedstock availability for industrial reuse. In parallel, the region is benefiting from expanding middle-class populations and shifting consumer preferences toward premium beverages, which is further supporting long-term supply growth for secondary utilization markets.

Several Asia Pacific economies are implementing biomass energy programs and waste reduction strategies to address environmental challenges and energy security concerns, which is encouraging investment in organic waste conversion technologies. The region’s established manufacturing infrastructure is enabling cost-effective production of coffee-based materials such as composites, biofuels, and filtration media, which is improving global competitiveness. Industrial clusters are facilitating partnerships between recyclers, material manufacturers, and energy companies, accelerating commercialization timelines, cementing the position of Asia Pacific as a major production and innovation center over the forecast period.

Competitive Landscape

The global coffee grounds market structure is moderately fragmented, with participation from specialized recycling firms, biomaterial startups, food ingredient innovators, and large waste management companies. Competitive positioning is primarily depending on access to consistent feedstock, efficiency of processing technologies, and the ability to develop commercially viable downstream products across multiple industries. Partnerships with coffee chains, beverage manufacturers, and institutional foodservice providers are becoming critical for securing reliable supply streams and ensuring material quality. Companies are also differentiating themselves through proprietary conversion methods that improve yield, reduce costs, or enhance performance characteristics in applications such as advanced materials and nutraceutical ingredients.

Investment activity is increasingly concentrating on scalable processing platforms that are capable of supplying diverse end-use sectors, including agriculture, energy, construction, and consumer products. Firms that are implementing vertically integrated operating models, which include collection, processing, and product manufacturing within a unified value chain, are gaining measurable competitive advantages through cost control and supply security. With industrial adoption expanding and sustainability requirements intensifying across sectors, companies that are combining technological expertise with strong supply partnerships are expected to strengthen their market positions and achieve higher long-term profitability.

Key Industry Developments

- In February 2026, researchers from RMIT University in Australia developed concrete using biochar derived from waste coffee grounds that can be up to 30% stronger while replacing about 15% of sand, reducing both resource extraction and emissions. The approach also helps divert organic waste from landfills and may lower the construction sector’s carbon footprint.

- In September 2025, 7-Eleven expanded its “Grounds to Green” initiative by partnering with Foodlink Foundation and New Life Farm to convert used coffee grounds into fertilizer that grows vegetables later used in new private-label juices, creating a farm-to-table circular model. The program also integrates social impact by supporting vocational rehabilitation while demonstrating scalable coffee waste upcycling across retail supply chains.

- In April 2025, Greek startup Coffeeco Upcycle raised € 715,000 in seed funding to scale its proprietary technology that converts spent coffee grounds into antioxidant-rich skincare ingredients and experimental bioplastics, with plans to expand across Europe and the United States. The company processes more than 10 tons of coffee waste monthly and is building a vertically integrated supply chain, highlighting growing investor confidence in high-value coffee waste commercialization.

Companies Covered in Coffee Grounds Market

- Nestlé S.A.

- Veolia Environnement S.A.

- SUEZ S.A.

- Bio-bean Limited

- Starbucks Corporation

- Reground Pty Ltd

- Coffee Recycling Company Limited

- Ground Control Limited

- Caribou Coffee Company, Inc.

- Farmer Brothers Company

- Lavazza Group (Luigi Lavazza S.p.A.)

- UCC Holdings Co., Ltd.

- Blue Tokai Coffee Roasters Private Limited

- Kaffa Roastery Ltd.

- Wake The Tree Pty Ltd

Frequently Asked Questions

The global coffee grounds market is projected to reach US$ 1.2 billion in 2026.

Surging coffee consumption worldwide, improving feasibility of waste valorization operations, and the expanding utilization of coffee waste higher-value applications are driving the market.

The market is poised to witness a CAGR of 9.7% from 2026 to 2033.

Regulatory pressure on organic waste diversion and production of biochar from coffee grounds for enhancing concrete performance to reduce carbon emissions from cement in construction activities are key market opportunities.

Nestlé S.A., Veolia Environnement S.A., SUEZ S.A., and Bio-bean Limited are some of the key players in the market.