- Home Care & Utilities

- Coffee Creamer Market

Coffee Creamer Market Size, Share, and Growth Forecast, 2025 - 2032

Coffee Creamer Market By Product Type (Dairy Creamers, Non-Dairy Creamers), Form (Liquid Creamers, Powdered Creamers). Flavor, Distribution Channel, End-user, and Regional Analysis for 2025 - 2032

Coffee Creamer Market Size and Trends Analysis

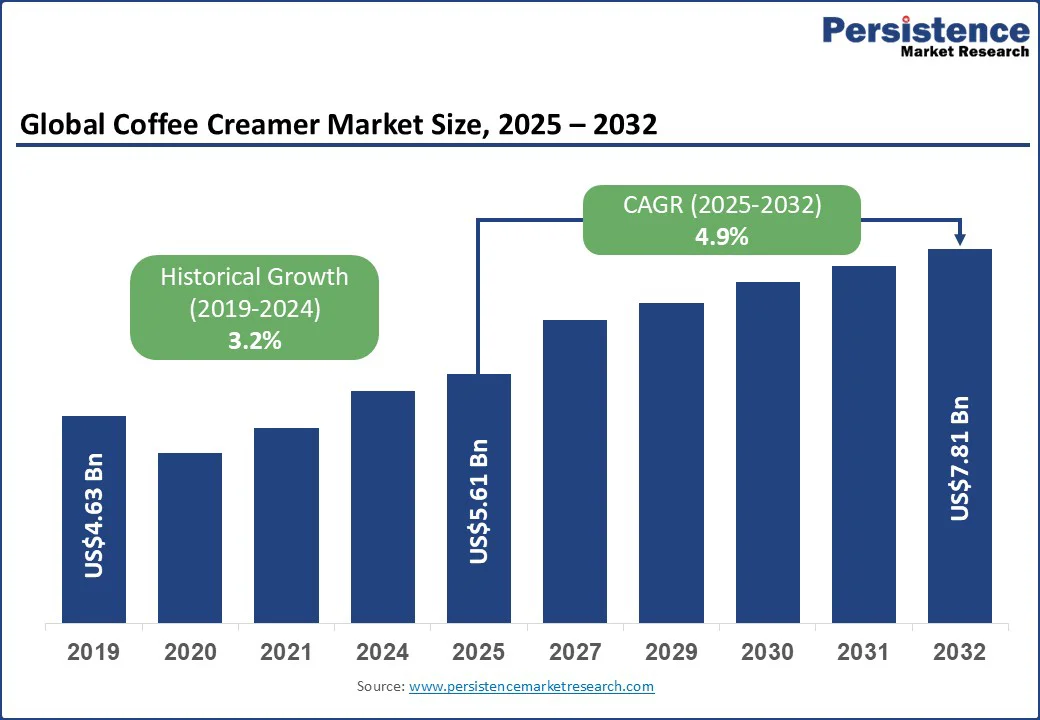

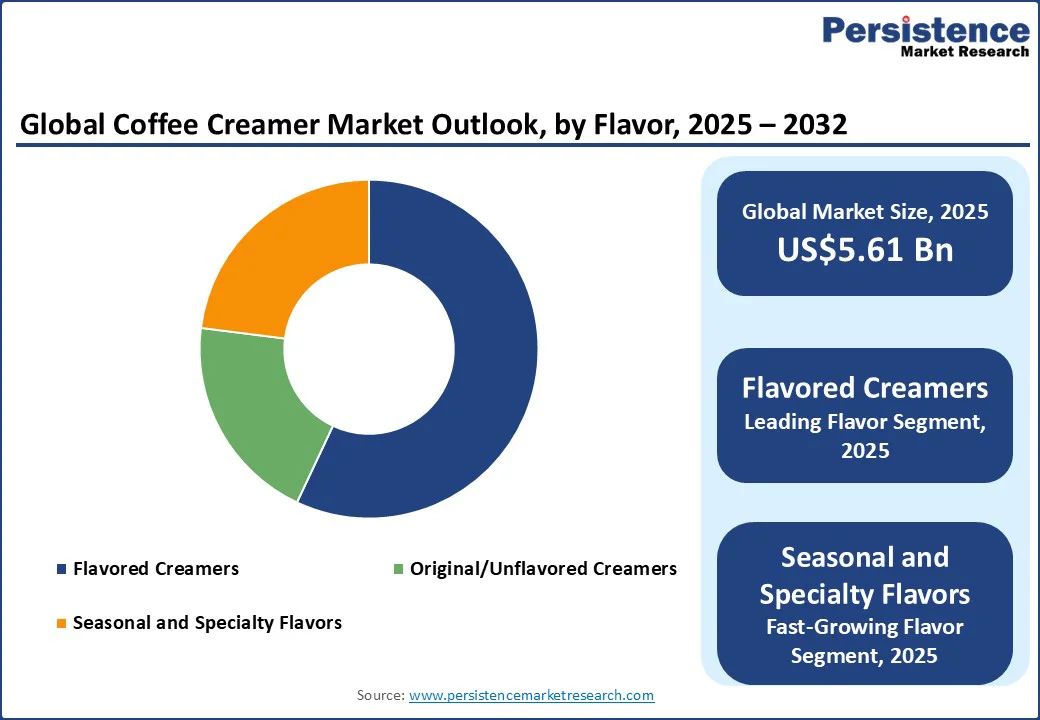

The global coffee creamer market size is likely to be valued at US$5.61 Bn in 2025 and is expected to reach US$7.81 Bn by 2032, growing at a CAGR of 4.9% during the forecast period from 2025 to 2032, due to the shift of consumer preferences toward convenient, dairy-free, and plant-based alternatives that enhance the coffee-drinking experience.

Key Industry Highlights

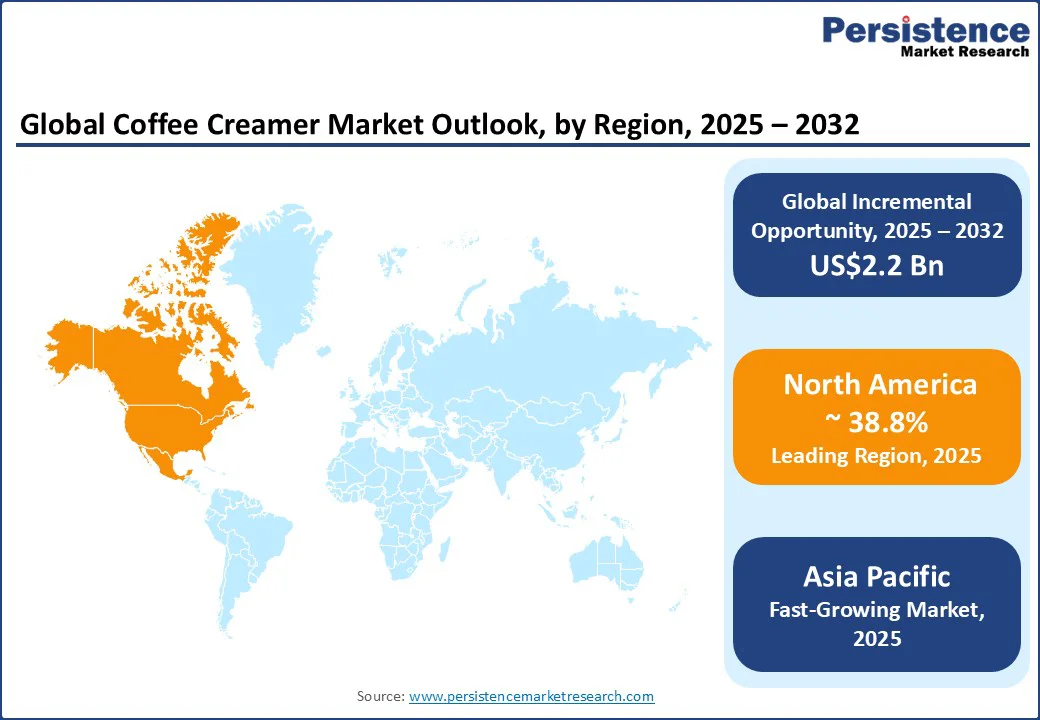

- Leading Region: North America, anticipated to hold around 38% of the global market share in 2025, driven by the strong presence of established brands such as Nestlé, Danone, and Chobani, coupled with rising consumer demand for plant-based and flavored creamers.

- Fastest-growing Region: Asia Pacific, projected to expand at a CAGR of over 7.5% (2025–2032), fueled by urbanization, café culture in markets like China and South Korea, and rising adoption of dairy-alternative creamers.

- Investment Plans: Major investments are channeled toward plant-based creamers, functional formulations (including collagen, MCT, and probiotics), and sustainable packaging innovations. For example, Nestlé invested US$675 million in a U.S. production facility in 2024, while Oatly expanded its oat-based creamer line in North America in the same year.

- Dominant Category: Flavored Creamers are projected to hold the largest share, at around 56.5% in 2025, owing to their widespread use in both households and food-service settings, which offers consumers versatility and variety.

- Leading Distribution Channel: Supermarkets/Hypermarkets are expected to account for nearly 43% of sales in 2025, reflecting their broad assortment and strong presence in both developed and developing economies.

| Key Insights | Details |

|---|---|

|

Coffee Creamer Market Size (2025E) |

US$5.61 Bn |

|

Market Value Forecast (2032F) |

US$7.81 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

4.9% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Portable Formats and Functional Formulations Reshape Creamer Consumption

The rising popularity of single-serve coffee creamer pods is transforming consumption patterns across food-service chains, airline catering, and hospitality segments. These formats provide hygiene assurance, portion control, and portability, making them particularly attractive in hotel mini-bars and quick-service outlets. With billions of units sold annually, compact pods and sachets meet the on-the-go consumer demand, prompting manufacturers to redesign packaging solutions tailored for travel and convenience-driven markets.

Advances in functional coffee creamers are also driving strong growth momentum, as consumers increasingly seek products that combine indulgence with health benefits. Formulations enriched with protein, MCT oil, probiotics, or adaptogens are gaining traction, while plant-based options such as oat, almond, and coconut creamers continue to expand rapidly. These innovations appeal to health-conscious, keto, and dairy-free consumers, positioning coffee creamer as both a flavor enhancer and a nutritional supplement that can be integrated into daily routines.

Sensory Gaps and Supply Chain Volatility Limit Market Expansion

Concerns around taste perception in sugar-free and non-dairy creamers continue to slow wider adoption in mainstream markets. Many reformulated products, including those using hydrogenated oils, artificial sweeteners, or plant-based substitutes, struggle to deliver the creamy texture and rich flavor profile associated with traditional dairy creamers. This gap in sensory experience often leads to lower repeat purchases, with retailers in key regions even reducing shelf space for certain variants. The result is a persistent challenge for brands aiming to balance health positioning with consumer expectations for indulgence.

Volatility in the raw material supply chain for almond, oat, and coconut bases is another constraint shaping growth strategies. Fluctuating input prices, combined with rising packaging costs and logistics inefficiencies, have tightened margins for small and mid-size manufacturers. These pressures directly impact the scalability of niche offerings, such as protein-fortified or single-serve creamers, which rely on consistent ingredient sourcing. Without stability in raw materials and packaging availability, many innovative product formats face slower commercialization despite growing consumer interest.

Flavor Innovation and DTC Personalization Fuel Premium Growth

Seasonal and flavor-driven innovations are creating significant growth potential in the coffee creamer market, particularly within the plant-based segment. Limited-edition launches such as pumpkin spice almond creamers or maple-flavored oat blends have shown remarkable traction, with sales spikes exceeding 1,400% during peak seasonal windows. These products appeal to both nostalgia and novelty, enabling brands to command premium shelf positioning while differentiating themselves in a crowded category. By aligning flavor innovation with festive or cultural occasions, companies can capture incremental demand and build stronger brand equity.

Direct-to-consumer models are also unlocking new avenues for personalization and recurring sales. The emergence of custom-blend coffee creamers, which allow consumers to select their preferred base, sweetness level, and functional ingredients, has gained momentum through online platforms and subscription clubs. This approach not only enhances customer loyalty but also provides brands with valuable data on evolving taste preferences. The ability to deliver tailored experiences positions e-commerce and subscription channels as powerful engines for sustained revenue growth in the creamer category.

Category-wise Analysis

Flavor Insights

Flavored creamers are expected to maintain the leading position in the global coffee creamer market, accounting for over 56.5% of total category revenue by 2025. They elevate the coffee experience through customizable flavor profiles such as vanilla, hazelnut, and caramel. Vanilla alone accounts for more than 30% of the flavored segment, driven by its broad cultural familiarity and versatility.

Flavored creamers also serve as a key entry point for premiumization in the category. Consumers are increasingly willing to pay a premium for products that replicate café-style beverages at home, particularly when combined with functional attributes such as low sugar, plant-based formulations, or added nutrients. The segment continues to benefit from digital influence, as social media and DIY coffee trends fuel experimentation and visibility. User-generated content, featuring recipes like whipped coffee or flavored iced lattes, acts as organic marketing, reinforcing flavored creamers as essential to the modern, experience-driven coffee routine.

Seasonal and specialty flavors are emerging as the fastest-growing sub-segment. Limited-time products such as pumpkin spice creamers experience dramatic seasonal sales spikes, with orders increasing rapidly during the autumn period. These products thrive on scarcity, nostalgia, and social media buzz, enabling brands to charge premium prices while capturing heightened consumer attention. Companies such as Califia Farms and Planet Oats have capitalized on this trend by introducing plant-based seasonal flavors that resonate strongly with younger, health-conscious buyers.

Distribution Channel Insights

Supermarkets and hypermarkets remain the leading distribution channel for coffee creamers, contributing around 43% of the overall market share. Their dominance comes from the extensive range of products offered under one roof, competitive pricing, and strong in-store visibility. Large chains, such as Walmart and Aldi, ensure widespread accessibility, making them the preferred choice for households that purchase creamers as part of their weekly shopping routine. The combination of bulk discounts, loyalty programs, and trusted retail environments has firmly established this channel as the backbone of coffee creamer distribution.

Online retail and subscription platforms, however, are expanding at the fastest pace, with growth projected at nearly an 8% CAGR in the coming years. This surge is being fueled by the convenience of home delivery, the rising popularity of personalized blends, and the appeal of recurring subscription models. Direct-to-consumer brands are leveraging digital platforms to offer customizable creamers with options for sweetness levels, plant-based bases, and functional ingredients. The ability to deliver tailored experiences and secure recurring revenue streams positions online channels as the most dynamic growth area within the distribution landscape.

Regional Insights

North America Coffee Creamer Market Trends - Strong Retail Penetration and Rising Demand for Indulgent Innovations

North America continues to dominate the global coffee creamer market, holding nearly 38.8% of the market. The region’s leadership is rooted in a well-established coffee culture, high per-capita coffee consumption, and an advanced retail landscape that ensures widespread product availability. Consumers here are seeking flavor diversity and also want creamers that deliver functional benefits, such as protein enrichment, low sugar, or plant-based alternatives.

In the U.S., large-scale investments and innovative product launches underscore the market's strength. Nestlé’s US$675 Mn production facility in Glendale, Arizona, dedicated to Coffee-mate and Starbucks At Home creamers, is a clear indicator of the sustained demand. Starbucks offers protein-rich cold foam creamers, signaling the convergence of nutrition and indulgence in coffee innovation. These product launches align with the preferences of younger consumers, particularly millennials and Gen Z, who are seeking coffee experiences that are both premium and health-conscious.

In Canada, consumer demand for premium and plant-based creamers mirrors U.S. trends, though the product variety is comparatively limited. The popularity of Chobani’s Cookie Dough Creamer, despite not being available in Canadian retail channels, shows the influence of U.S. launches on Canadian preferences.

Asia Pacific Coffee Creamer Market Trends - Rapid Urbanization and Localized Flavor Innovation

Asia Pacific is the fastest-growing regional market, forecast to expand at a CAGR exceeding 8.5% through 2032. Growth in the Asia Pacific is being driven by rapid urbanization, increasing disposable incomes, and younger demographics eager to adopt global coffee trends. The region’s café culture is booming, with specialty coffee chains and independent cafés proliferating in major urban centers. This has created fertile ground for the adoption of coffee creamers, particularly in formats that offer convenience and align with local flavor preferences.

In China, coffee consumption is growing rapidly as middle-class consumers increasingly adopt café lifestyles and ready-to-drink formats. Domestic and international brands are introducing innovative flavored creamers such as taro and matcha, which resonate strongly with local palates. Social media plays a pivotal role in driving adoption.

For instance, Kopikko leveraged TikTok and Instagram campaigns to boost its market share by nearly 19% within a year, showing how digital-first strategies can rapidly elevate a brand’s position.

In India, the market is evolving in a distinctive direction. While tea remains the dominant hot beverage, coffee consumption is growing steadily, particularly among urban professionals and younger consumers. Creamers are also increasingly being used in instant chai mixes, blending modern convenience with traditional consumption habits. Brands such as Sunrise Premix have achieved wide distribution in key states, highlighting the opportunity for creamers to extend beyond coffee into adjacent beverage categories. The expansion of café chains such as Starbucks and Café Coffee Day is further familiarizing consumers with premium coffee experiences, accelerating the demand for flavored and liquid creamers.

Europe Coffee Creamer Market Trends - Plant-Based Growth, and Premium At-Home Coffee Experiences

Europe has a steady demand supported by a strong coffee heritage and a growing preference for health-conscious choices. Unlike the Asia Pacific, where novelty and café expansion are fueling growth, Europe’s market is shaped by sustainability, clean-label demand, and the adoption of plant-based products. Consumers here are less inclined toward overtly indulgent flavors and more focused on formulations that align with ethical sourcing, low sugar, and natural ingredients.

Germany has emerged as a hub for clean-label and vegan creamers. The country’s mature coffee culture, combined with rising interest in lactose-free and plant-based diets, has made it one of the strongest adopters of oat, soy, and almond-based products. Local brands and global players are actively investing in clean-label innovation to cater to this demand, positioning Germany as a key market for non-dairy creamers.

The U.K. presents a slightly different dynamic, where café culture and consumer curiosity for specialty products are driving innovation. The launch of Trader Joe’s Cold Foam Vanilla Creamer, designed to replicate a barista-style topping at home, quickly gained popularity and created buzz on social platforms. With rising demand for vegan and low-sugar options, the U.K. market is likely to see continued innovation in both plant-based and indulgent segments.

Competitive Landscape

The global coffee creamer market is highly competitive, with established multinationals and emerging niche players actively shaping the landscape. Leading companies such as Nestlé (Coffee-mate, Starbucks At Home), Danone (International Delight, Silk), and FrieslandCampina dominate the market with extensive product portfolios and strong distribution networks. These players are investing heavily in innovation, introducing plant-based, functional, and seasonal flavors to capture shifting consumer preferences. Large-scale investments, such as Nestlé’s new US$675 Mn production facility in the U.S., highlight the scale of competition and the push to secure long-term supply capabilities.

At the same time, smaller and specialty brands such as Chobani, Califia Farms, and Nutpods are carving out market share by focusing on clean-label, vegan, and allergen-free formulations that appeal to health-conscious consumers. Startups leveraging direct-to-consumer channels and subscription models are also gaining traction by offering customized and premium creamers, often targeting niche communities online. This blend of global giants and agile innovators has created a competitive environment where product differentiation, flavor innovation, and sustainability-driven positioning are becoming critical success factors.

Key Industry Highlights

- In April 2025, International Delight launched a ready-to-drink iced coffee inspired by Cinnabon’s cinnamon roll, featuring cinnamon and cream cheese frosting flavors. Available in 15-ounce cans at grocery and convenience stores, the launch includes an Instagram sweepstakes with Cinnabon-themed alarm clocks that chill the coffee and release a cinnamon scent.

- In February 2024, Oatly expanded its North American portfolio with flavored oatmilk creamers, available in Sweet & Creamy, Vanilla, Caramel, and Mocha variants.

Companies Covered in Coffee Creamer Market

- Nestlé S.A.

- Danone S.A.

- FrieslandCampina N.V.

- Oatly Group AB

- Chobani, LLC

- Califia Farms, LLC

- Nutpods (Green Grass Foods, Inc.)

- MUD\WTR

- Laird Superfood, Inc.

- Kerry Group plc

- Super Coffee (Kitu Life Inc.)

- Z Natural Foods, LLC

- Balchem Corporation

- WhiteWave Foods

- Prymat Group

- Hiland Dairy Foods

- Organic Valley (CROPP Cooperative)

- Nestlé Health Science

- Elmhurst 1925

- So Delicious Dairy Free

Frequently Asked Questions

The coffee creamer market size is estimated at US$5.61 Bn in 2025.

By 2032, the coffee creamer market is projected to reach US$7.81 Bn.

Key trends include the rise of plant-based and non-dairy creamers, increasing consumer preference for functional formulations such as collagen- and MCT-enriched blends, and growing adoption of flavored and seasonal variants.

The flavor creamer segment leads the market with a 56.5% share in 2025.

The market is projected to grow at a CAGR of 4.9% from 2025 to 2032.

Some of the leading players include Nestlé S.A., Danone S.A, FrieslandCampina N.V., Oatly Group AB, and Chobani, LLC.