- Hardware & Software IT Services

- Cloud Collaboration Market

Cloud Collaboration Market Size, Share, and Growth Forecast 2026 - 2033

Cloud Collaboration Market by Solution (Unified Communication & Collaboration, Document Management, File Sharing & Cloud Storage, Project & Team Management, Enterprise Social Collaboration, Others), Service, Deployment Model, Organization Size, Industry, by Regional Analysis, 2026 - 2033

Cloud Collaboration Market Size and Trend Analysis

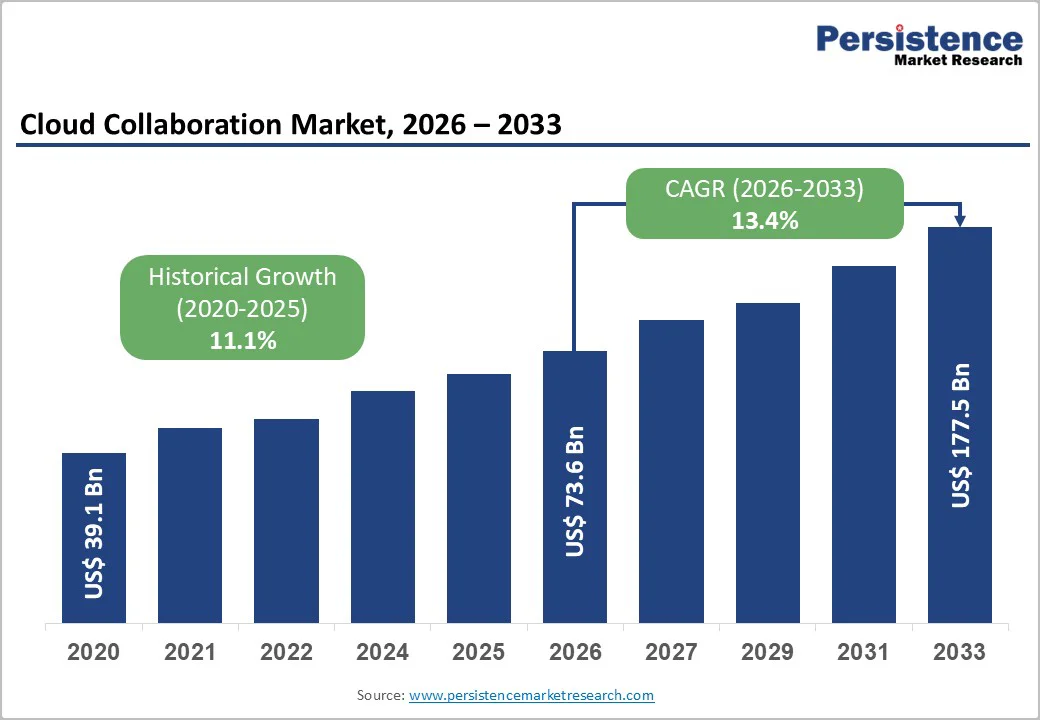

The global cloud collaboration market size is projected to reach US$ 177.5 billion by 2033, up from US$ 73.6 billion in 2026, at a CAGR of 13.4% in the forecast period from 2026 to 2033.

This growth is fueled by the widespread adoption of remote and hybrid work models, with 83% of employees preferring flexible arrangements that combine in-office and virtual collaboration. Organizations are increasingly leveraging cloud collaboration to maintain productivity across distributed teams while optimizing operational costs through digital transformation. Furthermore, advancements in artificial intelligence and machine learning are enhancing collaboration tools with features such as real-time editing, automated meeting summaries, and intelligent workflow automation, driving market expansion.

Key Industry Highlights:

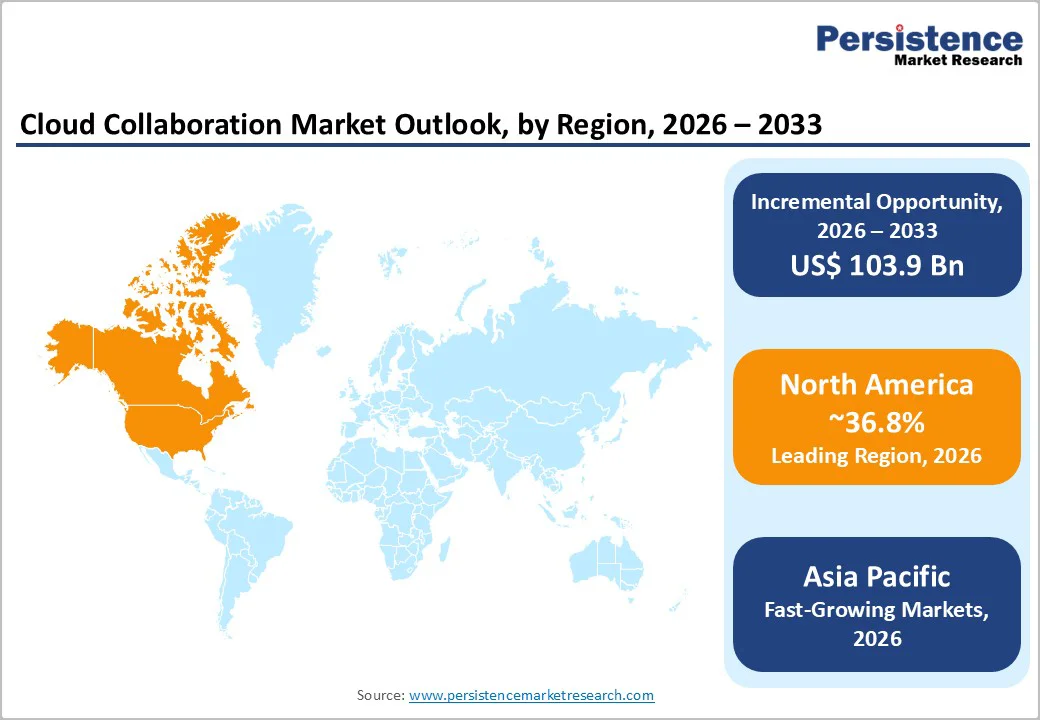

- Leading Region: North America leads with 36.8% of global revenues due to mature IT infrastructure, high remote work adoption, and advanced digital transformation initiatives.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region with a projected CAGR of 14.2%, driven by digital transformation in China and India, favorable demographics, and cloud-first government policies.

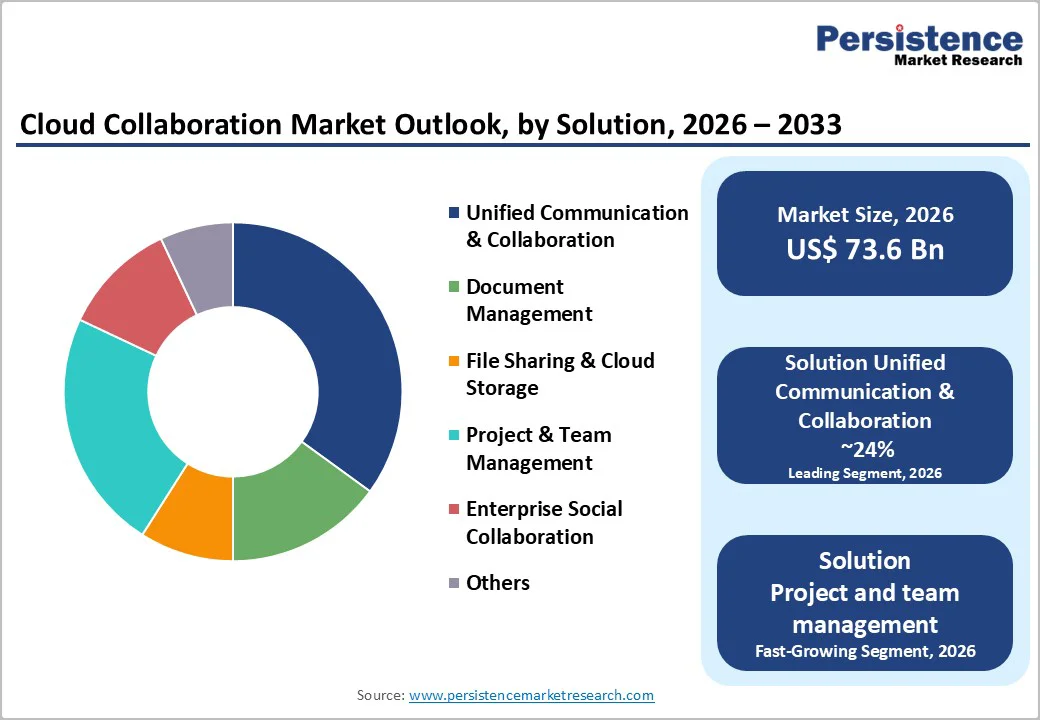

- Dominant Solution Segment: Unified Communication & Collaboration solutions hold approximately 42% of solution revenues, reflecting preference for integrated platforms with AI capabilities and enterprise-grade security.

- Fastest-Growing Organization Segment: SMEs are the fastest-growing segment with a CAGR exceeding 18%, supported by affordable pricing, managed services, and digital transformation pressures.

- Primary Market Opportunity: Healthcare and Life Sciences vertical offers significant growth potential due to increasing telehealth adoption, HIPAA-compliant platforms, and digital transformation across distributed facilities.

| Key Insights | Details |

|---|---|

| Cloud Collaboration Market Size (2026E) | US$ 73.6 billion |

| Market Value Forecast (2033F) | US$ 177.5 billion |

| Projected Growth CAGR (2026 - 2033) | 13.4% |

| Historical Market Growth (2020 - 2025) | 11.1% |

Market Dynamics

Drivers - Widespread Adoption of Remote and Hybrid Work Models Driving Cloud Collaboration Market Growth

The global transition to remote and hybrid work continues to be the foremost driver of cloud collaboration adoption. In 2025, over 32.6 million Americans work remotely, while 83% of workers worldwide prefer hybrid arrangements. This shift has made cloud collaboration platforms essential for seamless communication across distributed teams, ensuring operational continuity, enhancing employee engagement, and providing a competitive advantage, particularly in BFSI, healthcare, manufacturing, and technology sectors.

Flexible work models are directly influencing productivity and employee retention, as 46% of global workers indicate they would leave roles if required to return to full-time office work. Organizations are increasingly investing in cloud collaboration tools as critical infrastructure, enabling real-time coordination across multiple locations and time zones, while sustaining workforce satisfaction and long-term organizational performance.

Integration of Artificial Intelligence and Machine Learning as a Key Driver for Cloud Collaboration Adoption

AI and machine learning capabilities are transforming cloud collaboration platforms, creating strong incentives for enterprises to adopt advanced solutions. Tools like Microsoft Teams with Copilot and Google Workspace with Gemini AI enhance productivity through real-time meeting summaries, automated task generation, multilingual transcription, emotion recognition, and intelligent workflow management, enabling teams to work more efficiently and effectively across locations.

The demand for AI-powered collaboration features including predictive analytics, automated scheduling, intelligent content summarization, and real-time translation is growing as organizations aim to optimize team workflows. Research indicates AI integration can reduce communication costs by up to 30%, providing tangible financial benefits while encouraging both large enterprises and mid-market companies to upgrade to cloud-based collaboration platforms with cutting-edge intelligence capabilities.

Restraints - Data Security, Privacy, and Regulatory Compliance Challenges Limiting Cloud Collaboration Adoption

Despite growing adoption of cloud collaboration platforms, concerns over data security, privacy, and regulatory compliance remain major restraints. Enterprises managing sensitive data must navigate complex regulations such as GDPR, HIPAA, and CCPA, limiting cloud migration for certain use cases. Less than 10% of organizations encrypt most of their cloud data, while cybersecurity threats like ransomware, data leakage, and unauthorized access continue to impede full-scale adoption.

Multi-cloud environments and shared responsibility models create additional uncertainty regarding accountability. Compliance breaches carry severe financial and reputational consequences, particularly in highly regulated sectors. Although privacy-preserving frameworks and customized policies are emerging to address these risks, organizations continue to face significant barriers in fully leveraging cloud collaboration tools while ensuring robust data protection.

Technical Integration Complexity and Vendor Lock-In Risks Hindering Cloud Collaboration Implementation

Integrating cloud collaboration solutions into existing IT ecosystems presents substantial technical and financial challenges, particularly in enterprises with legacy systems and interdependent applications. While 77% of telecom executives find cloud migration effective, 48% of cloud investments remain unused, highlighting integration difficulties. Organizations require specialized IT expertise to connect collaboration platforms with ERP, CRM, and industry-specific systems efficiently.

Concerns about vendor lock-in and multi-cloud dependencies further slow adoption, as enterprises seek flexibility and negotiation leverage. Technical debt, high transformation costs, and lack of standardization or interoperability across providers continue to impede cloud collaboration deployment, especially in emerging markets with limited IT resources and constrained budgets.

Opportunity - Accelerated Digital Transformation in Healthcare and Life Sciences Driving Cloud Collaboration Adoption

The Healthcare and Life Sciences sector is emerging as one of the fastest-growing segments in the cloud collaboration market, fueled by digital transformation and regulatory compliance requirements. Cloud collaboration platforms enable secure sharing of medical data, real-time consultations across geographic locations, and integration with electronic health record systems, enhancing clinical decision-making and patient outcomes. Telehealth infrastructure and HIPAA-compliant solutions continue to drive sustained adoption.

Major healthcare providers and pharmaceutical companies are investing in unified communication platforms that integrate messaging, voice, video, and document sharing within secure environments. The sector’s growth is further reinforced by adoption of cloud analytics for treatment optimization and patient engagement, creating complementary demand for integrated collaboration and analytics tools that support data-driven clinical decision-making.

Expansion of Small and Medium Enterprises Creating High-Growth Opportunities in Cloud Collaboration

Small and medium enterprises (SMEs) represent a significant growth opportunity, driven by improved affordability, reduced adoption barriers, and competitive pressures to digitalize operations. About 50% of SMEs are leveraging cloud to expand business, while 52% prioritize public cloud solutions for scalability and cost-effectiveness. Vendors increasingly offer tiered pricing, flexible licensing, and simplified implementation, reducing complexity for resource-constrained organizations.

SMEs are investing in cloud skills development, with managed service providers supporting consultation, integration, and ongoing platform management. Around 39% seek trusted partners for cloud expansion, and 37% prioritize cost-effective solutions. Cloud collaboration is becoming a strategic tool for SMEs to enhance customer engagement, enable flexible work, and compete effectively with larger enterprises.

Category-wise Analysis

Solution Insights

Unified Communication & Collaboration (UCC) solutions lead the market, capturing approximately 42% of total solution revenue in 2026, reflecting strong enterprise preference for integrated platforms combining voice, video, messaging, and document collaboration. Microsoft Teams, Google Workspace, and Cisco Webex drive adoption with AI-powered capabilities, robust security, and seamless integration with existing business applications. Enterprises prioritize platforms that reduce IT complexity, improve user adoption, and deliver consolidated communication tools, reinforcing UCC solutions as the cornerstone of organizational technology stacks.

Project and team management, as well as niche collaboration tools, are emerging as the fastest-growing solution segments, driven by increasing demand for specialized platforms that support flexible workflows, real-time collaboration, and cross-functional team coordination. Vendors are enhancing these solutions with AI, automation, and cloud-native integrations, addressing diverse enterprise needs beyond traditional communication functions.

Service Insights

Support and Maintenance Services dominate the cloud collaboration services market, accounting for approximately 38% of service revenues in 2026, highlighting the critical importance of reliability and operational continuity. Enterprises increasingly invest in managed services, proactive monitoring, and 24/7 technical support to maintain optimal platform performance across distributed teams and geographies. The growing complexity of deployments, continuous feature updates, and need for ongoing training further reinforce the leadership of support and maintenance services in service revenue contribution.

Integration, consulting, and optimization services are the fastest-growing service segments, driven by increasing adoption of AI-enabled collaboration tools and hybrid deployment models. Organizations are seeking services that reduce implementation complexity, maximize technology investments, and enhance operational efficiency, creating significant growth opportunities for service providers and managed solution partners.

Deployment Model Insights

Public Cloud remains the leading deployment model, commanding approximately 59.4% of total deployment revenues in 2026 due to its scalability, affordability, and ease of implementation. Platforms from Microsoft, Google, and Amazon offer automatic updates, global infrastructure access, and elimination of capital expenditure requirements. Private Cloud deployments, accounting for around 55% of security-focused implementations, address sensitive data handling and compliance needs, strengthening adoption in highly regulated industries.

Hybrid Cloud represents the fastest-growing deployment model, as enterprises balance flexibility, security, and performance across on-premises and multi-cloud environments. Hybrid solutions allow organizations to optimize cost efficiency, maintain compliance, and scale operations effectively, positioning them as a key growth driver in future market expansion.

Organization Size Insights

Large Enterprises dominate the cloud collaboration market, accounting for approximately 65% of total market revenues in 2026, driven by substantial IT budgets, complex structures, and the need for enterprise-grade security and compliance. These organizations leverage advanced governance controls, deep ERP integrations, analytics, and customizable workflows, supporting premium adoption of cloud collaboration platforms.

Small & Medium Enterprises (SMEs) are the fastest-growing segment, driven by declining adoption barriers, affordable solutions, and competitive pressures to digitalize operations. Vendors are targeting SMEs with simplified user interfaces, pay-per-seat models, and flexible deployment options, enabling rapid adoption across resource-constrained businesses.

Industry Insights

BFSI (Banking, Financial Services, and Insurance) leads industry adoption, capturing approximately 28% of vertical-specific revenues in 2026, fueled by regulatory compliance requirements, secure communication needs, and digital banking innovation. Cloud collaboration platforms streamline operations, improve customer service, reduce costs, and enable mobile banking, fintech partnerships, and open banking architectures. Healthcare and Life Sciences follow with 22% share, driven by telehealth, clinical collaboration, and HIPAA-compliant communication needs.

Government and Public Sector verticals are the fastest-growing, driven by digital-first strategies, cloud-first policies, and modernization initiatives. Governments are adopting cloud collaboration platforms to improve service delivery, operational efficiency, and cross-agency coordination, creating sustained growth opportunities in public sector deployments.

Regional Insights

North America Cloud Collaboration Market Trends

North America leads the global cloud collaboration market, accounting for approximately 36.8% of global revenues in 2026. The region benefits from mature IT infrastructure, widespread adoption of remote and hybrid work models, and the presence of global technology leaders including Microsoft, Google, Amazon, and Zoom. Enterprises across BFSI, Healthcare, Manufacturing, and Technology sectors are driving demand for feature-rich collaboration platforms, while advanced IT governance, security practices, and AI integration further support adoption. The United States serves as the innovation hub, continuously introducing AI-powered features, automation, and secure communication tools that set benchmarks for enterprise collaboration globally.

The region’s growth is sustained by ongoing digital transformation and enterprise investments in hybrid and multi-cloud deployment models. North American organizations are increasingly prioritizing secure, integrated platforms that enable seamless collaboration across distributed teams. Continuous adoption of cloud collaboration solutions to enhance productivity, maintain compliance, and support operational efficiency positions North America as the benchmark for global cloud collaboration trends through 2033.

Europe Cloud Collaboration Market Trends

Europe accounts for approximately 32% of global cloud collaboration revenues in 2026, with the United Kingdom and Germany as leading markets. Adoption is driven by strong digital infrastructure, regulatory harmonization, and advanced technology ecosystems. Germany’s industrial and manufacturing sectors are leveraging cloud collaboration for Industry 4.0 initiatives, supply chain management, and remote operations. Enterprises across Europe prioritize GDPR-compliant and privacy-enhanced solutions, creating demand for localized data centers and secure collaboration platforms. The presence of global cloud service providers ensures access to advanced AI, workflow automation, and integrated communication tools.

Europe’s market growth is supported by mature adoption patterns, digital workplace modernization, and strategic investments in cloud transformation. Organizations are increasingly implementing hybrid deployments to balance compliance and flexibility. Regulatory-driven premium solutions and focus on secure, scalable platforms continue to drive adoption across BFSI, Healthcare, and public sector organizations. While growth is slightly slower than North America and Asia Pacific, Europe’s consistent investment in cloud collaboration ensures long-term market stability and steady expansion through 2033.

Asia Pacific Cloud Collaboration Market Trends

Asia Pacific is emerging as the fastest-growing cloud collaboration region, with a projected CAGR of 14.2% through 2033. China leads the region with rapid adoption driven by digital transformation across industries, expansion of e-commerce and fintech platforms, and government cloud-first policies. India is the second-largest market, supported by IT and BPO sector growth, enterprise digitalization across BFSI, Healthcare, and Manufacturing, and a tech-savvy workforce. Increasing digital initiatives in Southeast Asia further contribute to regional expansion, while large enterprises and SMEs are adopting cloud platforms for operational efficiency, remote collaboration, and workflow automation.

The region’s growth is fueled by scalable and cost-effective cloud solutions enabling coordination across distributed teams. Asia Pacific organizations are embracing hybrid deployment models, AI-powered collaboration tools, and secure platforms to meet evolving business needs. Supportive government policies, rising digital literacy, and growing investment in technology infrastructure position Asia Pacific as the key high-growth market, creating significant opportunities for global cloud collaboration vendors through 2033.

Competitive Landscape

The global cloud collaboration market demonstrates a moderately concentrated structure, with top-tier leaders collectively capturing around 40% of total revenues. These dominant players leverage integrated productivity ecosystems, AI-powered features, and platform enhancements to maintain strong market positions. Competitive intensity remains high, with secondary players generating significant revenue through specialized capabilities, vertical-specific solutions, and strong customer relationships across targeted industry segments.

Market strategies are increasingly focused on AI integration, ecosystem development, and acquisition-driven consolidation to achieve differentiation. Emerging vendors are rapidly capturing the small and medium enterprise segment by offering affordable, user-friendly solutions with accelerated feature development, driving market dynamism and sustained growth.

Key Market Developments:

- In November 2025, Microsoft Corporation announced comprehensive Teams platform enhancements including native Copilot chat integration, new combined chat and channels experience, voice isolation for meetings, and intelligent speaker recognition capabilities. The updates represent a sustained commitment to AI-powered collaboration features and improved user experience.

- In September 2025, Zoom Video Communications, Inc. announced strategic partnership with Cisco enabling Zoom functionality on Cisco hardware through Zoom for Cisco Rooms, alongside expansion of Zoom AI Companion with Salesforce Service Cloud Voice integration and custom AI capabilities through AI Studio.

- In April 2025, Google LLC announced significant Google Workspace enhancements including audio capabilities for document creation, AI-powered writing refinement tools, Veo 2 image generation integration in Vids, and advanced Sheets analytics leveraging Gemini AI models.

Companies Covered in Cloud Collaboration Market

- Microsoft Corporation

- Google LLC

- Amazon Web Services Inc.

- Cisco Systems Inc.

- Zoom Video Communications Inc.

- Slack Technologies LLC

- Atlassian Corporation Plc

- Dropbox Inc.

- Box Inc.

- Adobe Inc.

- International Business Machines Corporation

- VMware Inc.

- Asana Inc.

- Monday.com Ltd.

- Zoho Corporation Pvt. Ltd.

Frequently Asked Questions

The global cloud collaboration market is expected to reach US$ 73.6 billion in 2026, growing from US$ 39.1 billion in 2020.

Growth is driven by widespread hybrid work adoption, AI and machine learning integration, and organizational digital transformation initiatives.

Unified Communication & Collaboration solutions lead with approximately 42% of total solution revenues, reflecting preference for integrated, AI-enabled, secure platforms.

North America leads with 36.8% of global revenues driven by mature IT infrastructure and technology leader concentration.

Growth is concentrated in Healthcare and Life Sciences, SME segments, and emerging Asia Pacific markets with cloud-first policies.

Leading market players include Microsoft Corporation, Google LLC, Amazon Web Services, Inc., Cisco Systems, Inc., Zoom Video Communications, Inc., and Slack Technologies, LLC.