- Telecommunications

- Cloud Telephony Service Market

Cloud Telephony Service Market Size, Share, and Growth Forecast 2026 - 2033

Cloud Telephony Service Market by Service Type (Hosted PBX, SIP Trunking, Interactive Voice Response IVR, Toll-Free Numbers, Voice Broadcasting, Click-to-Call, Call Recording & Analytics, Communication Platform as a Service (CPaaS), Unified Communications as a Service UCaaS, Virtual Numbers), Deployment Model (Public Cloud, Private Cloud, Hybrid Cloud), Organization Size (Small & Medium-Sized Enterprises SMEs, Large Enterprises), Industry, and Regional Analysis, 2026 - 2033

Cloud Telephony Service Market Size and Trend Analysis

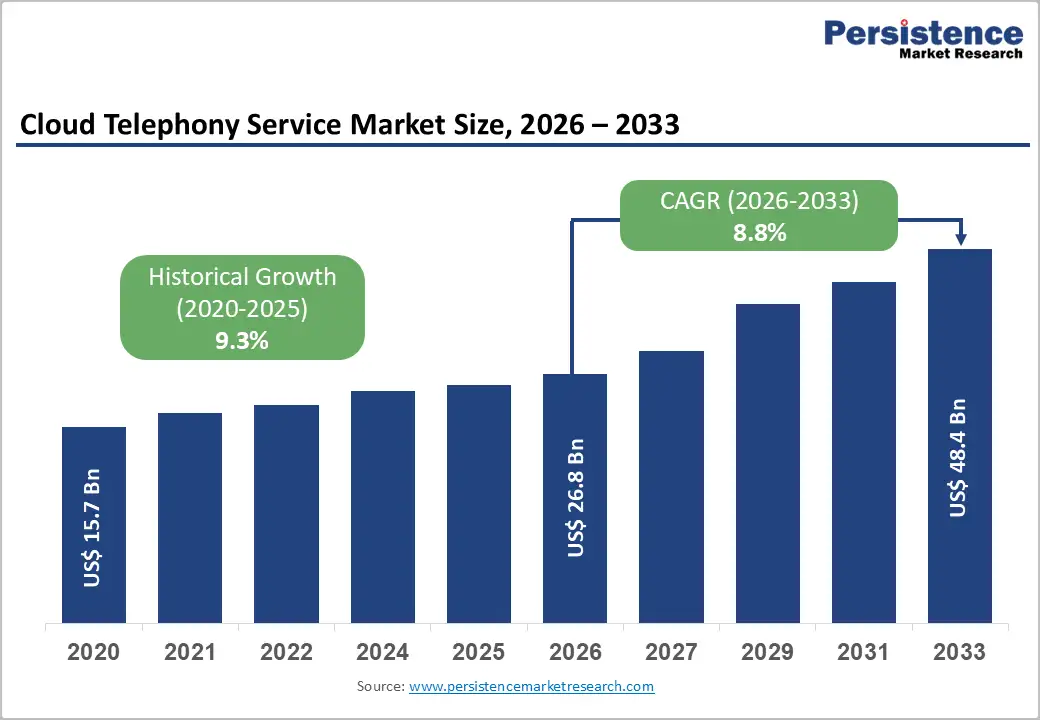

The global cloud telephony service market size is expected to reach US$ 26.8 billion in 2026 and US$ 48.4 billion by 2033, growing at a CAGR of 8.8% between 2026 and 2033.

The market is experiencing robust growth driven by widespread adoption of Unified Communications as a Service (UCaaS) platforms, accelerating digital transformation across enterprises, and persistent remote and hybrid work arrangements, creating sustained demand for flexible communication solutions. Legacy PBX transition to cloud UC adds 2.1 percentage points to market CAGR, representing the single most important accelerator as enterprises eliminate hardware refresh cycles, specialized telephony talent requirements, and complex capacity-planning overheads. AI-enhanced contact-center productivity integrated with advanced analytics enables organizations to reduce operational costs by 25% while improving customer satisfaction metrics, establishing compelling business cases supporting widespread cloud telephony adoption across diverse industry verticals globally.

Key Industry Highlights:

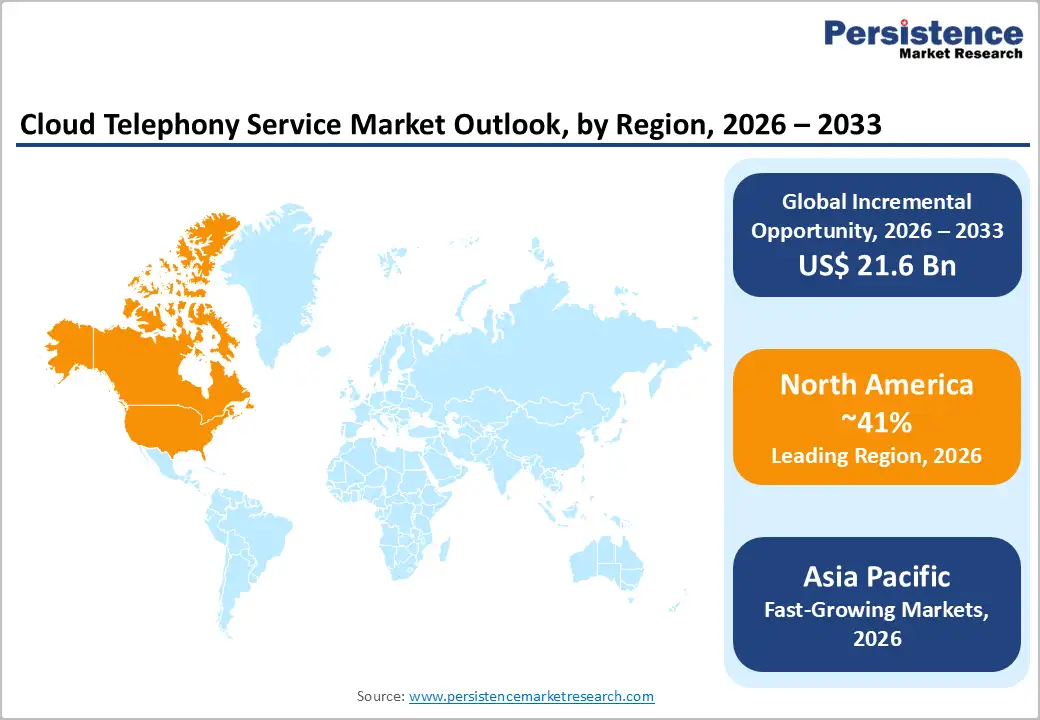

- Leading Region: North America leads the market with around 41% share, supported by robust cloud infrastructure, high enterprise IT spending, widespread broadband access, and strong adoption of flexible work models.

- Fastest Growing Region: Asia Pacific is the fastest-growing region with a CAGR of 10.9% during 2026 - 2033, driven by rapid digital transformation, smart city initiatives, and expanding outsourcing and cloud adoption.

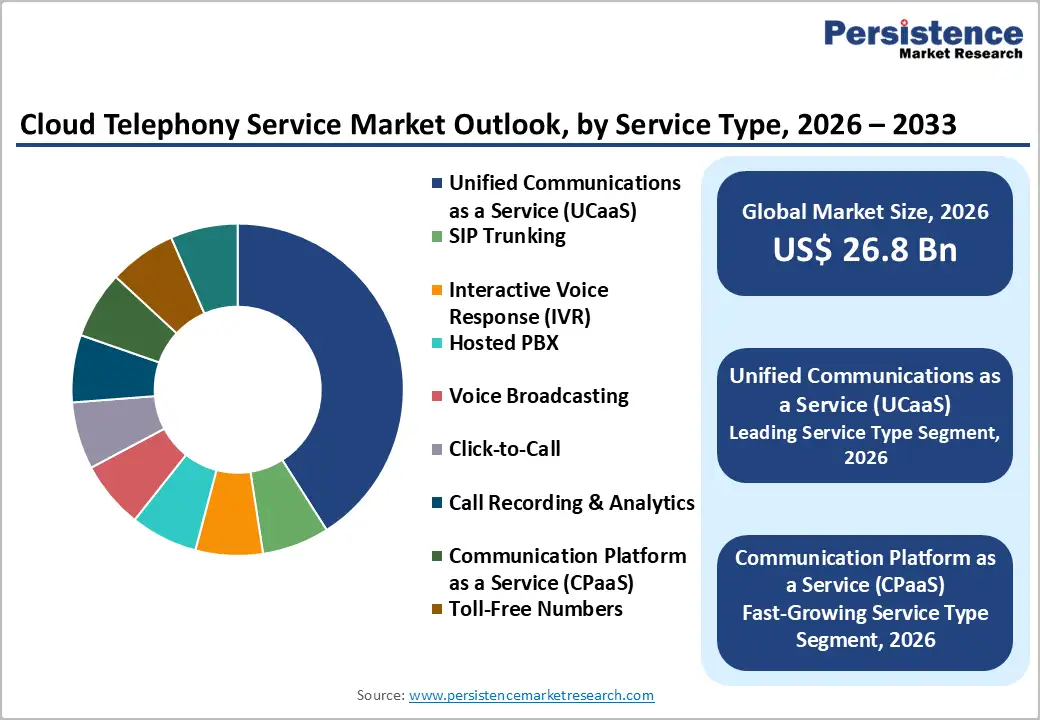

- Dominant Segment: Unified Communications as a Service (UCaaS) dominates the market with about 41.6% share, reflecting strong demand for integrated platforms replacing traditional communication systems.

- Fastest Growing Segment: Communications Platform as a Service (CPaaS) is the fastest-growing segment, expanding at a CAGR of 25.4% due to rising adoption of programmable APIs for omnichannel engagement.

- Key Market Opportunity: AI-powered call analytics and autonomous contact center automation present the largest opportunity by significantly improving efficiency, resolution rates, and real-time performance insights.

| Key Insights | Details |

|---|---|

| Market Size (2026E) | US$ 26.8 Billion |

| Market Value Forecast (2033F) | US$ 48.4 Billion |

| Projected Growth CAGR (2026 - 2033) | 8.8% |

| Historical Market Growth (2020 - 2025) | 9.3% |

Market Dynamics

Drivers - Persistent Remote and Hybrid Work Culture Adoption

Remote and hybrid work represent a fundamental and durable shift in organizational structures, creating sustained demand for cloud-based communication solutions enabling seamless team collaboration regardless of physical location. Post-pandemic normalization has solidified flexible work arrangements as a permanent organizational feature, with 74% of IT leaders prioritizing cloud communication as the #1 IoT use case for smart cities, reflecting unprecedented organizational commitment to cloud-based infrastructure. Unified communications as a service (UCaaS) platforms eliminate geographic constraints on team collaboration, enabling distributed workforces to communicate and collaborate with the same effectiveness as colocated teams.

Microsoft Teams dominates knowledge worker segments, with embedded voice capabilities that reduce the total cost of ownership by 30% compared to traditional PBX systems. Cisco Webex Calling accelerates adoption within industries where telephony is mission-critical, including healthcare, manufacturing, and logistics. Cloud telephony solutions that support fixed-mobile convergence enable employees to transition seamlessly between office and mobile environments while maintaining a unified call history and device integration, supporting both organizational flexibility and employee satisfaction objectives simultaneously.

Enterprise Transition from On-Premises PBX to Cloud UC Architectures

Enterprise migration toward cloud-based unified communications represents the most significant market accelerator, as aging on-premises PBX equipment approaches end-of-support cycles, creating natural replacement opportunities for cloud solutions. Five-year capital equipment depreciation schedules align neatly with cloud migration initiatives, encouraging wholesale platform replacement projects, eliminating specialized IT staff requirements and expensive ongoing maintenance contracts. Consolidated licensing bundles integrating voice, messaging, and video under predictable subscription models attract CFO and financial controller decision-making participation, establishing cost-governance transparency and budget predictability advantages compared to traditional capital-intensive PBX infrastructure.

Total cost of ownership improvements exceeding 30% achieved through the elimination of hardware costs, simplified network management, and reduced IT staffing requirements provide a compelling financial justification for executive-level cloud telephony adoption decisions. Public-cloud OPEX and elastic scalability enable SMEs to access enterprise-grade communication capabilities through pay-as-you-go pricing, eliminating the costs of over-provisioned capacity during periods of reduced utilization. Multinationals benefit from geographic expansion, treating it as a licensing matter rather than an infrastructure development imperative, thereby supporting international growth initiatives with minimal incremental technology investment.

Restraint - VoIP Security Compliance and Data Protection Concerns

Cloud telephony services handle sensitive business communications and customer interactions requiring stringent cybersecurity safeguards and regulatory compliance alignment with GDPR, HIPAA, PCI-DSS, and industry-specific standards, creating substantial implementation complexity. Regulatory compliance requirements for call recording, data retention, encryption standards, and access control establish specialized technical and operational requirements exceeding capabilities of basic cloud communication solutions.

Hyperscale egress fees charged by major cloud providers for data transfer between cloud and on-premises infrastructure create unexpected cost escalation and unpredictable total cost of ownership, particularly for organizations with mission-critical on-premises systems that require hybrid deployment architectures. Inconsistent broadband quality in emerging markets limits the viability of cloud telephony in regions with unreliable internet connectivity, constraining market expansion opportunities in developing economies despite economic incentives and technological advantages.

Technology Fragmentation and Vendor Lock-in Concerns

The heterogeneous cloud telephony vendor ecosystem creates interoperability challenges and data migration complexity when organizations transition between providers, establishing switching costs that reduce competitive dynamics and customer flexibility. Enterprise adoption of multi-vendor strategies, balancing Microsoft Teams Phone with Cisco Webex Calling, creates organizational complexity but prevents single-vendor dependency and establishes redundancy protections. Legacy system integration challenges arise when cloud telephony platforms need to synchronize with established CRM systems, business analytics platforms, and enterprise communication infrastructure, necessitating specialized integration services and extended implementation timelines.

Opportunity - AI-Powered Call Analytics and Autonomous Contact Center Automation

Artificial intelligence integration into cloud telephony platforms enables real-time call analytics, sentiment analysis, automated transcription, and intelligent call routing, supporting operational efficiency improvements exceeding 35-40% while reducing agent workload and improving customer satisfaction. AI-driven call summaries and voicemail transcription capabilities eliminate manual review requirements, enabling supervisors to access performance intelligence and quality assurance insights within minutes of call completion rather than hours or days required for traditional manual review processes.

Automated call routing, powered by machine learning algorithms, directs inbound inquiries to the optimal agents based on historical performance, skill matching, and customer preference analysis, improving first-call resolution rates by 25-30%. Intelligent virtual assistants and IVR systems powered by natural language processing reduce agent-handled call volume by 20-25%, enabling organizations to maintain service quality while reducing operational costs. Predictive analytics, identifying call abandonment patterns and peak demand periods, enable workforce scheduling optimization and service level improvement. The CCaaS (Contact Center as a Service) market, growing at 11.1% annually, reflects exceptional adoption of AI-enhanced contact center platforms supporting customer service transformation.

Rapid Adoption of Communications Platform as a Service (CPaaS) and Developer Ecosystem Expansion

CPaaS (Communications Platform as a Service) is the fastest-growing segment, with a 25.4% CAGR, as developers integrate voice, SMS, video, and authentication directly into customer-facing applications, enabling omnichannel engagement and personalized communication experiences. Retail organizations embed click-to-call widgets at checkout, enabling seamless customer support and reducing cart abandonment rates. Logistics applications implement two-way SMS notifications and voice alerts, automating driver communications and delivery confirmations, reducing administrative overhead.

Financial technology and fintech applications leverage CPaaS for two-factor authentication, KYC verification, and fraud prevention, driving exceptional adoption in emerging market fintech ecosystems. A programmability narrative that directly feeds into digital transformation budgets positions CPaaS as a strategic pillar of the broader cloud telephony market, supporting sustained expansion across software development and digital innovation initiatives. Healthcare applications implementing telehealth platforms and patient engagement systems leverage CPaaS capabilities supporting integrated voice, video, and messaging, supporting patient-provider communication.

Category-wise Analysis

Service Type Insights

Unified Communications as a Service (UCaaS) is the dominant service segment, accounting for approximately 41.6% of the cloud telephony service market in 2025. Its leadership reflects a strong enterprise preference for consolidated platforms that unify voice, video, messaging, and collaboration within a single cloud environment. UCaaS solutions reduce reliance on legacy desk phones and fragmented conferencing tools, simplifying IT management and lowering operational complexity.

Rapid scalability allows organizations to onboard users in minutes, supporting distributed and hybrid workforces. Standardized user experiences, centralized security controls, and seamless integration with productivity and business applications further strengthen adoption. Growing acceptance among large enterprises and regulated sectors highlights UCaaS as the foundation of modern enterprise communication strategies.

Deployment Model Insights

Public cloud deployment dominates the cloud telephony service market with around 68.1% share in 2025, driven by its cost efficiency, flexibility, and ease of implementation. Organizations increasingly favor multi-tenant cloud infrastructure to eliminate capital expenditure on hardware and reduce ongoing maintenance requirements. Public cloud platforms offer rapid scalability, high availability, and automatic updates, enabling enterprises to respond quickly to changing communication needs. Centralized management and global accessibility support geographically dispersed workforces without additional infrastructure investment. Security enhancements, redundancy, and compliance certifications offered by major cloud providers have improved enterprise confidence. As digital transformation accelerates, public cloud deployment remains the preferred model for scalable, resilient, and agile communication services.

Organization Size Insights

Small and medium-sized enterprises represent the fastest-growing organization segment, recording a projected CAGR of 11.2% during 2026 - 2033 and contributing over half of total market growth. Cloud telephony enables SMEs to replace costly on-premise systems with subscription-based services, eliminating hardware investments and specialized IT staffing. Access to advanced features such as IVR, call analytics, and omnichannel communication enhances customer engagement and competitive positioning. Simplified deployment and intuitive management interfaces align well with limited technical resources. Built-in security features support compliance without additional overhead, while elastic scalability allows SMEs to expand communication capacity seamlessly as business needs evolve.

Industry Insights

The IT and telecom sector represents the largest end-user segment, accounting for approximately 24.3% of cloud telephony service revenue. Adoption is driven by the need to standardize internal communications, support distributed teams, and enable scalable customer-facing services. Cloud telephony aligns closely with digital-native operating models, allowing rapid provisioning, API-driven customization, and integration with software platforms. Service providers also leverage cloud telephony to resell voice capacity and value-added services, expanding revenue streams. High call volumes, advanced analytics requirements, and continuous innovation cycles reinforce demand. As technology companies prioritize agility and global reach, cloud telephony remains central to their communication infrastructure.

Regional Insights

North America Cloud Telephony Service Market Trends and Insights

North America maintains significant market dominance with approximately 41% regional share in 2025, driven by strong enterprise IT budgets, advanced cloud infrastructure, and rapid adoption of flexible work arrangements. The United States leads global adoption through extensive broadband infrastructure, a competitive cloud provider landscape, and regulatory frameworks supporting digital transformation initiatives. Enterprise migration from legacy PBX systems to cloud UC platforms continues to accelerate as equipment depreciation cycles align with cloud migration roadmaps.

RingCentral, Twilio, Vonage, and 8x8 Inc. maintain strong North American competitive positions through established enterprise relationships and regional support infrastructure. Financial services and professional services sectors lead regional adoption through capital availability and digital transformation budgets. The healthcare industry transition toward cloud-based communication, supporting telehealth initiatives and patient engagement, drives specialized UCaaS adoption throughout the region.

Europe Cloud Telephony Service Market Trends and Insights

Europe represents a mature market characterized by stringent data protection regulations, GDPR compliance requirements, and an emphasis on sustainability and environmental responsibility. Germany, the United Kingdom, and France lead regional adoption through strong industrial bases and investment in digital transformation initiatives. EU regulatory harmonization facilitates cross-border deployment of cloud telephony, reducing fragmentation and establishing standardized compliance frameworks.

Compliance-focused UCaaS solutions that incorporate data residency guarantees, encryption standards, and audit trails address European regulatory requirements and help compliant vendors differentiate. Hybrid deployment preferences in Europe reflect regulatory sensitivity to data sovereignty and national border data retention requirements. Green data-center mandates drive adoption of sustainable cloud infrastructure aligned with EU environmental commitments.

Asia Pacific Cloud Telephony Service Market Trends and Insights

Asia Pacific emerges as the fastest-growing regional market with a CAGR of 10.9% during 2026 - 2033, capturing approximately 35% of the global cloud telephony service market by 2025 and expanding rapidly. China dominates regional adoption through massive digital transformation initiatives, smart city projects, and rapid expansion of internet infrastructure, supporting cloud service deployment. India’s growing outsourcing and business process management industry drives exceptional cloud telephony adoption as enterprises expand contact center operations, leveraging cloud-native platforms.

Japan maintains technological leadership through advanced communication infrastructure and enterprise IT maturity, with Cisco Webex and Microsoft Teams achieving strong adoption among large enterprises. ASEAN manufacturing expansion in Vietnam, Thailand, and Indonesia creates emerging market opportunities, as localized operations require communication infrastructure and support for distributed workforces. Cost-sensitive market segments favor CPaaS solutions, enabling direct application integration and reduced complexity compared to enterprise UCaaS platforms.

Competitive Landscape

The cloud telephony service market exhibits a moderately consolidated structure, dominated by a small group of global providers supported by numerous regional and niche players. Competition is driven by platform breadth, scalability, and the ability to integrate voice services with broader collaboration, CRM, and contact center ecosystems. Leading providers leverage large installed user bases, cloud-native architectures, and strong channel partnerships to accelerate customer acquisition and retention.

Business strategies increasingly emphasize bundled offerings, seamless migration from legacy systems, and flexible pricing models to address enterprises of varying sizes. Strategic acquisitions remain common, allowing providers to enhance AI capabilities, vertical-specific solutions, and omnichannel communication features. Regional players compete by offering cost-efficient services, localized compliance, and tailored solutions for emerging markets. Enterprises are also adopting multi-vendor strategies to reduce dependency risks, combining complementary platforms to balance functionality, resilience, and cost efficiency, further shaping competitive dynamics.

Key Market Developments:

- In May 2024, Tata Communications and Cisco launched Webex Calling in India, integrating Cisco’s cloud platform with Tata’s GlobalRapide to deliver enterprise-grade, scalable PSTN services, AI-powered collaboration tools, compliance, and seamless access to the Webex Suite, supporting hybrid work without hardware investments.

- In September 2024, Vodacom launched an affordable R249 cloud-based smartphone in South Africa with 48MB RAM, cloud apps like YouTube and TikTok, targeting underserved users to bridge the digital divide, cut device costs, and ease 2G/3G to 4G migration through Vodafone partnership.

- In October 2024, Zoom Video Communications launched Zoom Phone in India as the first licensed cloud-based phone solution, featuring AI tools like post-call summaries, local numbers, global coverage in 50 countries, and integrations to replace traditional PBX for hybrid workforces.

- In January 2025, Onecom launched Wave, a next-generation cloud phone system built on AWS in the UK post-Gradwell acquisition, featuring VoIP calling, multi-device access, voicemail transcription, and intuitive controls for simpler, cost-effective telephony with in-house innovation and nationwide engineering support.

- In August 2025, Xtelify by Bharti Airtel launched sovereign Airtel Cloud and an AI-powered software platform to accelerate business digital transformations, offering cost optimisation, telco-grade reliability, and global partnerships for enhanced customer experience and efficiency.

Companies Covered in Cloud Telephony Service Market

- Twilio

- RingCentral

- Vonage

- 8x8 Inc.

- Cisco Webex Calling

- Microsoft Corporation

- Nextiva

- Grasshopper

- Dialpad

- Mitel

- Zoom Phone

- Alcatel-Lucent Enterprise

- Avaya

- Genesys

- Bandwidth

Frequently Asked Questions

The global cloud telephony service market is expected to reach approximately US$ 26.8 billion in 2026.

Key drivers include remote and hybrid work adoption, migration from legacy PBX systems, AI-enabled call analytics, and scalable pay-as-you-go communication models.

North America is expected to lead the market with about 41% share during the forecast period.

The largest opportunity lies in AI-powered call analytics and autonomous contact center automation improving efficiency and customer experience.

Major players include Microsoft, Cisco, Twilio, RingCentral, Vonage, and 8x8.