- Biotechnology

- Cell Line Development Market

Cell Line Development Market Size, Share, and Growth Forecast 2026 - 2033

Cell Line Development Market by Product (Immunotherapy Cell Lines, GPCR Cell Lines, Cell Signaling Pathway Cell Lines, Gene Knockout Cell Lines, Ion Channel Cell Lines, Cancer Cell Lines, Others), Application (Drug Discovery & Development, Basic Research, Toxicity Screening, Biopharmaceutical Production, Tissue Engineering, Forensic Testing), End-user (Biopharmaceutical Companies, Contract Research Organization, Academic & Research Institutes, Forensic Science Laboratories, Diagnostic Laboratories), and Regional Analysis, 2026 2033

Cell Line Development Market Size and Trend Analysis

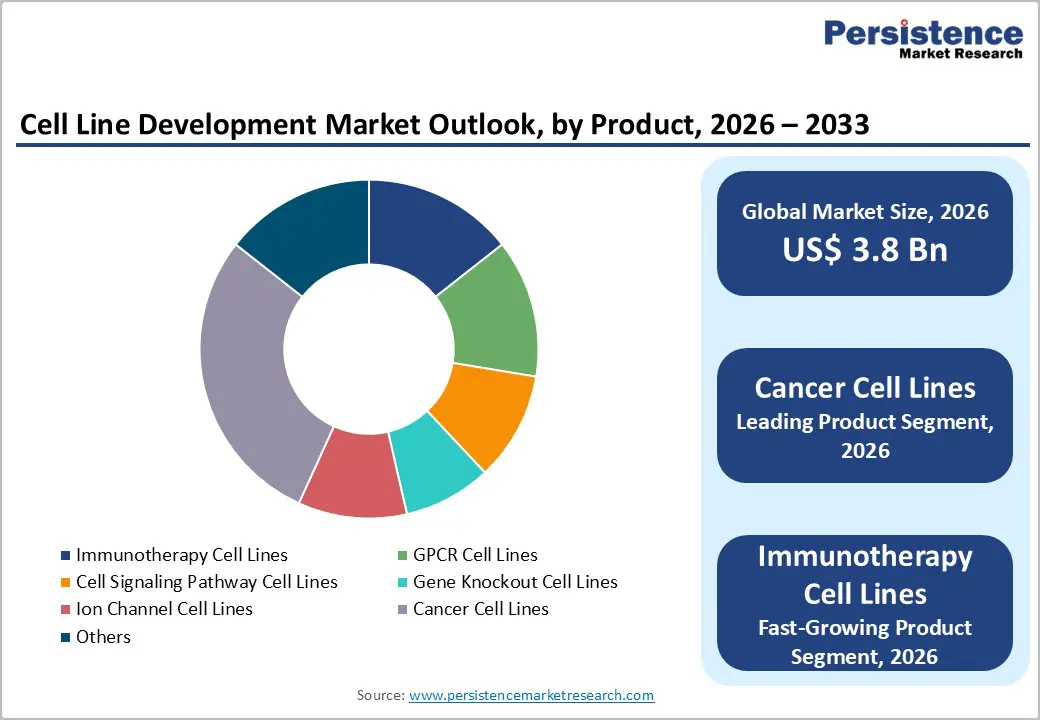

The global cell line development market size is expected to be valued at US$ 3.8 billion in 2026 and projected to reach US$ 5.8 billion by 2033, growing at a CAGR of 6.1% between 2026 and 2033.

The market is driven by the exponential rise in demand for biopharmaceuticals, monoclonal antibodies, and biosimilars, coupled with technological advancements in CRISPR-Cas9 gene editing and automated cell culture systems. According to the International Agency for Research on Cancer (IARC), cancer cases are projected to rise from 19.29 million in 2020 to 24.58 million by 2030, necessitating advanced cell line development for therapeutic discovery. The increasing prevalence of chronic diseases and the shift toward personalized medicine further accelerate market expansion as biopharmaceutical companies invest heavily in stable, high-yield cell line platforms.

Key Industry Highlights:

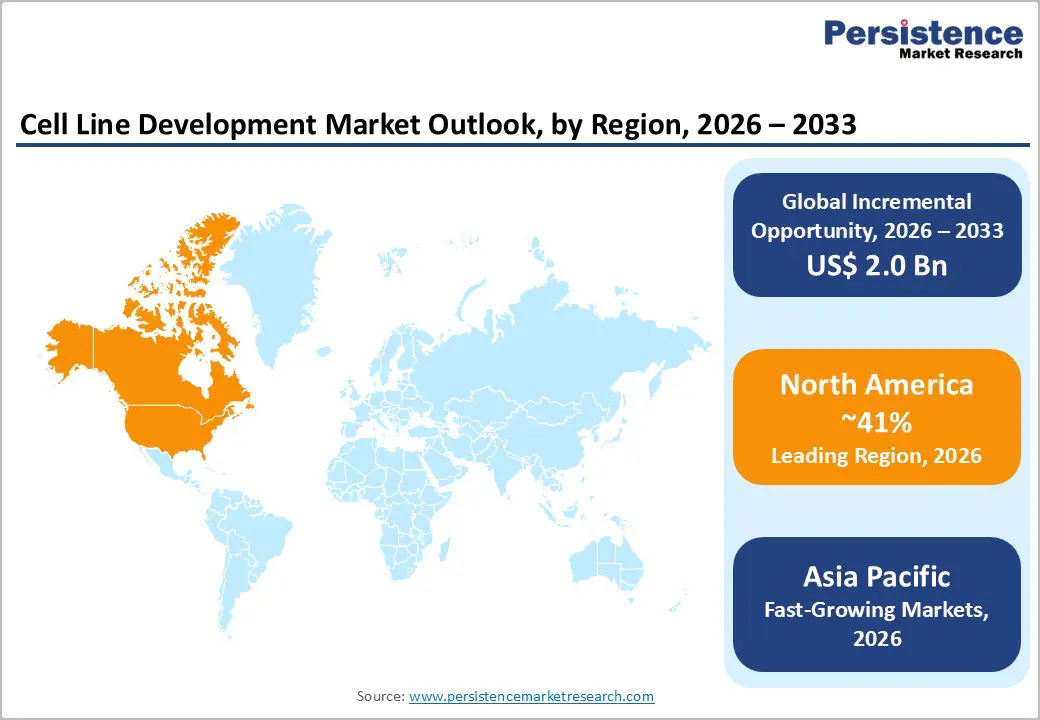

- North America leads the market: Accounted for ~41% of the global cell line development market share in 2025, supported by strong biopharmaceutical infrastructure, robust NIH funding, and a large pharmaceutical presence.

- Asia Pacific shows fastest growth: Expected to grow at a CAGR of 11.63% through 2033, driven by supportive government policies, expanding manufacturing capacity in China, India, and Japan, and rising collaborations with regional CDMOs.

- Cancer Cell Lines dominate: Held ~24% market share in 2025, fueled by expanding oncology pipelines, CRISPR-based mutation modeling, and increased use of PDX models in preclinical research.

- Immunotherapy Cell Lines grow fastest: Growth driven by rising approvals of CAR-T therapies, checkpoint inhibitors, and advanced cell therapy platforms.

- Biopharmaceutical production leads applications: Accounted for 45.9% of market value, driven by strong demand for monoclonal antibodies, biosimilars, and recombinant proteins.

| Global Market Attributes | Key Insights |

|---|---|

| Cell Line Development Market Size (2026E) | US$ 3.8 billion |

| Market Value Forecast (2033F) | US$ 5.8 billion |

| Projected Growth CAGR (2026-2033) | 6.1% |

| Historical Market Growth (2020-2025) | 3.9% |

Market Dynamics

Drivers - Rising Demand for Monoclonal Antibodies and Biologics Production

The global surge in monoclonal antibodies and recombinant protein therapeutics is a primary driver of the cell line development market. Biopharmaceutical production represents approximately 45.9% of the application segment, supported by the increasing demand for biosimilars and complex biologics. The World Health Organization (WHO) emphasizes that consistency in quality during biomanufacturing is critical in ensuring biologics and vaccines remain globally accessible safely and effectively. Lonza, one of the leading cell line development service providers, reported 23.1% CDMO revenue growth in the first half of 2025, with more than 85% of revenue now derived from cell line development and manufacturing operations. The accelerating expiration of patents for blockbuster biologics has intensified demand for biosimilar development, requiring robust cell line platforms to achieve commercial viability and regulatory compliance. This trend is expected to maintain momentum throughout the forecast period as pharmaceutical companies expand their biologics portfolios.

Technological Advancements in Gene Editing and Automation

Innovations in CRISPR-Cas9, zinc finger nucleases (ZFN), and artificial intelligence (AI)-driven clone selection are revolutionizing cell line development efficiency. CRISPR technology has transformed the ability to develop customized cell lines with enhanced stability and productivity, reducing development timelines by up to 50% , according to recent industry reports. AI-driven optimization applications combined with automated bioreactor systems enable faster identification of high-producing clones and improve predictability in cell line characteristics. The OECD reports that strong federal funding and well-established biomanufacturing infrastructure accelerate the development of stable, high-yield cell lines. Companies like Thermo Fisher Scientific Inc. continue to invest in advanced automation platforms that integrate real-time quality monitoring and digital manufacturing systems. These technological breakthroughs reduce development costs and timelines, allowing companies to bring novel therapeutics to market faster while maintaining regulatory compliance.

Restraints - Complex Regulatory Requirements and GMP Compliance Challenges

Cell line development for therapeutic applications faces stringent regulatory hurdles that increase development costs and extend timelines. The FDA and European Medicines Agency (EMA) mandate comprehensive documentation including clonality reports, extensive genetic stability studies, adventitious agent testing, and Good Manufacturing Practice (GMP) compliance. Developers must prove that production cell lines originate from a single progenitor cell, requiring sophisticated imaging systems and detailed documentation. Quality control variability, contamination risks, and scalability restrictions remain persistent challenges that require continuous investment in specialized equipment and trained personnel. The complexity of regulatory submissions and the need for pre-clinical safety assessments significantly burden smaller biopharmaceutical companies, potentially limiting market participation and innovation velocity in developing regions.

Genetic Instability and Low Productivity Issues

Genetic instability represents a critical hurdle in cell line development, as cells can undergo genetic changes over multiple passages, leading to reduced protein expression and loss of critical quality attributes. Low productivity arising from suboptimal gene integration sites, insufficient gene copy numbers, and unfavorable chromatin environments requires extensive screening to identify commercially viable expression levels. These challenges necessitate sophisticated characterization and long-term stability data generation, consuming considerable time and resources. Companies must balance the need for rapid cell line development with the imperative to ensure product consistency and quality attributes, creating a fundamental constraint on market acceleration.

Opportunity - Expansion of Cancer Cell Lines for Immunotherapy Development

The cancer cell line segment is capturing significant market attention, holding approximately 24% market share in 2025 and emerging as the fastest-growing category with immunotherapy cell lines demonstrating accelerated adoption. The International Journal of Cancer reports that cancer immunotherapy treatments, particularly CAR-T cell therapies and checkpoint inhibitors, are achieving regulatory approvals at unprecedented rates. Horizon Discovery, a leading provider of engineered cancer cell lines, was recently recognized by CiteAb as the Cell Line Supplier to Watch in Cancer Research for 2024, reflecting the surging demand for validated cancer cell line platforms. The development of patient-derived xenograft models and three-dimensional cell culture systems enables more accurate disease modeling and drug response prediction. Biopharmaceutical companies are increasingly partnering with specialized cell line developers to access comprehensive cancer cell line libraries for high-throughput drug screening. This segment is expected to generate substantial revenue as oncology pipelines expand and combination therapy approaches require diverse cellular models for efficacy validation.

Adoption of Allogeneic "Off-the-Shelf" Cell Therapies and Universal Donor Cell Lines

The emerging market for allogeneic, universal donor cell line platforms represents a transformative opportunity for cell line development companies. Unlike autologous therapies requiring patient-specific processing, allogeneic approaches enable standardized manufacturing at scale, significantly reducing production costs and timelines. Industry analysis indicates that universal donor cell lines—highly characterized, regulatory-compliant platforms pre-adapted for multiple products—can reduce development timelines by 50% or more compared to traditional approaches.

In April 2025, Cellistic, a Belgium-based pioneer in induced pluripotent stem cell (iPSC)-based therapies, launched the Echo-NK platform, a scalable solution for manufacturing off-the-shelf allogeneic NK cell therapies targeting blood cancers and solid tumors. This model allows biopharma companies to leverage pre-qualified cell banks with established GMP documentation, genetic safety profiles, and critical quality attributes. As regulatory pathways mature and manufacturing capabilities advance, the allogeneic cell therapy market is projected to capture an increasing share from autologous platforms, creating substantial opportunities for cell line development service providers specializing in donor cell engineering and characterization.

Category-wise Analysis

Product Insights

The Cancer Cell Lines segment represents the dominant product category with approximately 24% market share in 2025, driven by the accelerating pace of oncology drug development and the critical role of cancer models in preclinical screening. Cancer cell lines, including both established lines and newly engineered variants, enable researchers to study tumor behavior, test therapeutic efficacy, and identify resistance mechanisms. The integration of CRISPR-Cas9 technology has enabled the development of highly specific cancer cell line variants targeting genetic mutations such as KRAS G12C, EGFR mutations, and HER2 amplifications. These engineered models provide more relevant disease representations compared to traditional cancer cell lines, supporting the development of precision oncology therapeutics.

The growing adoption of patient-derived xenograft (PDX) models derived from cancer cell lines further validates their importance in personalized medicine development. Pharmaceutical companies recognize that robust cancer cell line platforms reduce drug development failures and accelerate time-to-market, justifying premium pricing for specialized cell line products.

Application Insights

Biopharmaceutical Production emerges as the leading application segment, capturing approximately 45.9% of market value, reflecting the critical importance of stable cell lines in manufacturing monoclonal antibodies, recombinant proteins, and vaccines. Chinese hamster ovary (CHO) cells and human embryonic kidney (HEK293) cells remain the industry standard for biopharmaceutical manufacturing due to their compatibility with human tissues, reduced infection risk, and capacity for post-translational modification.

The escalating demand for biosimilars, driven by the patent expiration of blockbuster biologics, intensifies requirements for high-fidelity cell line characterization and scaled manufacturing platforms. Contract Development and Manufacturing Organizations (CDMOs) increasingly invest in proprietary cell line platforms to differentiate services and accelerate client pipelines. Advanced technologies, including perfusion bioreactors, continuous manufacturing systems, and real-time process analytical technology, enhance productivity and consistency. The biopharmaceutical production application is projected to maintain dominance throughout the forecast period as global demand for biologics, vaccines, and cell-based therapies continues its rapid expansion.

End-user Insights

Biopharmaceutical Companies represent the largest end-user segment, leveraging cell line development services to accelerate therapeutic discovery and ensure manufacturing compliance. These organizations prioritize partnerships with specialized contract research organizations (CROs) and contract development and manufacturing organizations (CDMOs) to access advanced cell line engineering capabilities and reduce internal development burdens. Contract Research Organizations have emerged as critical partners, offering specialized expertise in cell line development, clone selection, and process optimization.

The growing trend of biologics outsourcing reflects strategic decisions by pharmaceutical companies to focus on core competencies while leveraging specialized service providers' technical expertise. Academic & Research Institutes continue contributing to cell line development innovation through collaborative projects with industry partners, generating foundational knowledge that supports commercial development. This multi-stakeholder ecosystem creates diverse growth opportunities across the cell line development value chain.

Regional Insights

North America Cell Line Development Market Trends and Insights

North America dominates the cell line development market with approximately 41% market share in 2025, leveraging its advanced pharmaceutical manufacturing ecosystem, robust regulatory framework, and significant research investments. The United States hosts over 50% of global biopharmaceutical headquarters and maintains leadership in clinical trial initiation and regulatory approvals. The region benefits from substantial National Institutes of Health (NIH) funding for cell and gene therapy research, supporting both academic discoveries and commercial translation.

The U.S. regulatory environment, managed by the Food and Drug Administration (FDA), has implemented specialized guidance documents for cell line development and manufacturing, including Chemistry, Manufacturing, and Controls (CMC) expectations and Good Manufacturing Practice (GMP) standards. The region's highly skilled workforce in molecular biology, bioprocess engineering, and regulatory affairs supports rapid cell line development cycles. According to the American Cancer Society, the U.S. is projected to diagnose 2,041,910 new cancer cases in 2025, driving substantial investment in oncology cell lines and therapeutic development platforms.

Strategic partnerships between major pharmaceutical companies like Pfizer, Merck Group, and Bristol Myers Squibb with specialized cell line developers accelerate innovation cycles. North America's infrastructure dominance and innovation ecosystem are expected to sustain regional leadership throughout the forecast period.

Asia Pacific Cell Line Development Market Trends and Insights

Asia Pacific emerges as the fastest-growing region for cell line development, with a projected CAGR of 11.63% through 2033, driven by expanding biopharmaceutical manufacturing capacity, favorable regulatory initiatives, and substantial research and development investments. China, Japan, and India lead regional growth, with China alone representing over 20% of the Asia Pacific cell line development market.

Competitive Landscape

The cell line development market is characterized by moderate to high competition, driven by rising demand for biologics, monoclonal antibodies, and cell- and gene-based therapies. Market participants compete on speed of development, genetic stability, productivity, and regulatory-compliant platforms. Increasing outsourcing by biopharmaceutical companies has intensified competition among service providers offering customized and scalable cell line solutions.

Key Developments:

- In January 2026, Aragen announced the launch of CHOMax™, a new cell line development and early manufacturing platform designed to support an integrated pathway from DNA to IND-enabling clinical supply in approximately 10 months for suitable standard IgG monoclonal antibodies. The platform offered an accelerated, royalty-free approach, providing biotech and pharmaceutical partners with a clearly structured development pathway that included support for both drug substance and drug product.

Companies Covered in Cell Line Development Market

- BPS Bioscience, Inc.

- Thermo Fisher Scientific Inc.

- ATCC (American Type Culture Collection)

- Sigma-Aldrich (Merck Group Company)

- Lonza

- STEMCELL Technologies

- BioIVT LLC

- Novus Biologicals

- Rockland Immunochemicals

- GenScript

- BiologicsCorp

- Horizon Discovery

- Synthego

Frequently Asked Questions

The global cell line development market is projected to reach US$ 3.8 billion in 2026, growing at a CAGR of 6.1% through 2033. This growth trajectory reflects increasing demand for biopharmaceuticals, monoclonal antibodies, and biosimilars supported by technological advancements in CRISPR-Cas9 gene editing and automated cell culture systems.

The primary demand drivers include the exponential rise in cancer incidence (projected 24.58 million cases globally by 2030 from 19.29 million in 2020), accelerating adoption of precision medicine, expansion of biopharmaceutical and biosimilar pipelines, and technological breakthroughs in AI-driven clone selection and CRISPR-based genetic engineering that reduce development timelines and enhance cell line productivity.

North America leads the cell line development market with approximately 41% market share in 2025, driven by advanced biopharmaceutical infrastructure, substantial NIH funding, strong pharmaceutical company presence, and mature regulatory frameworks supporting accelerated cell line engineering and therapeutic development initiatives.

Immunotherapy Cell Lines represent the fastest-growing product category, supported by regulatory approvals of CAR-T cell therapies, checkpoint inhibitors, and allogeneic NK cell therapies. These segments require sophisticated cell line engineering capabilities and specialized manufacturing platforms for both research and commercial therapeutic development.

Key opportunities include developing universal donor cell lines that reduce development timelines by 50% or more, expanding allogeneic cell therapy platforms for "off-the-shelf" manufacturing, leveraging AI and automation for improved clone selection, and capturing growth in Asia Pacific markets where biopharmaceutical manufacturing is expanding rapidly with government supportive policies and favorable cost structures.