- Advanced Materials

- Carbon Nitride Market

Carbon Nitride Market Size, Share, and Growth Forecast, 2026 - 2033

Carbon Nitride by Product type (Graphitic Carbon Nitride, Polymeric Carbon Nitride), Morphology (Powder, Thin Films, Nano particle), End-user (Electronics, Healthcare, Coatings), Application (Photocatalysis, Others), and Regional Analysis 2026–2033

Carbon Nitride Market Size and Trends Analysis

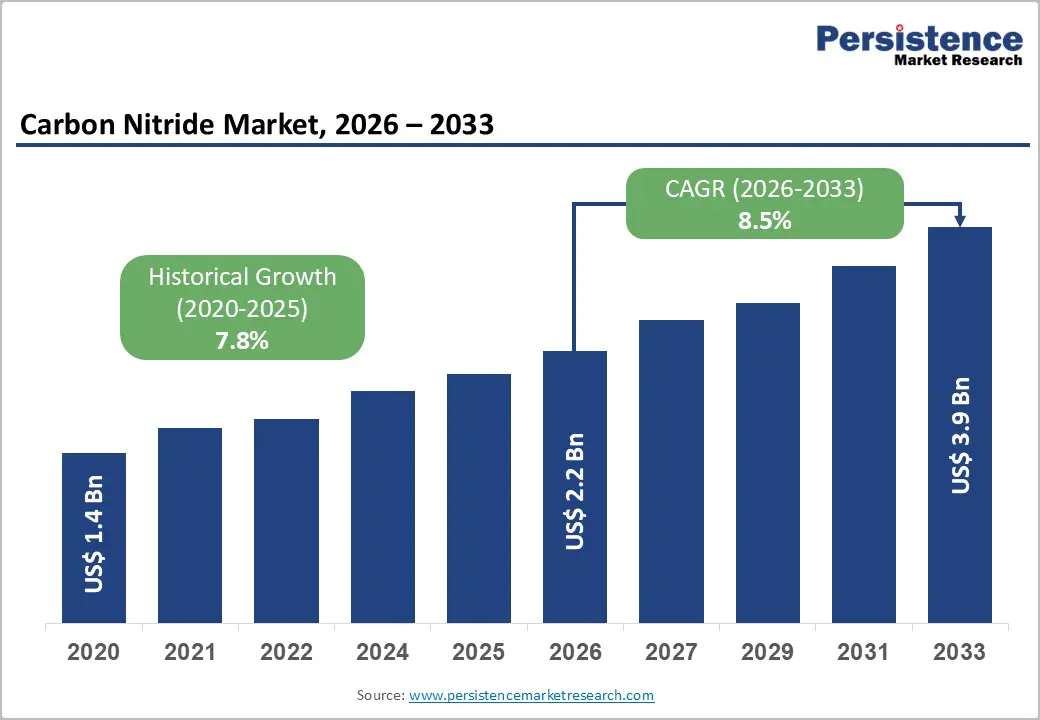

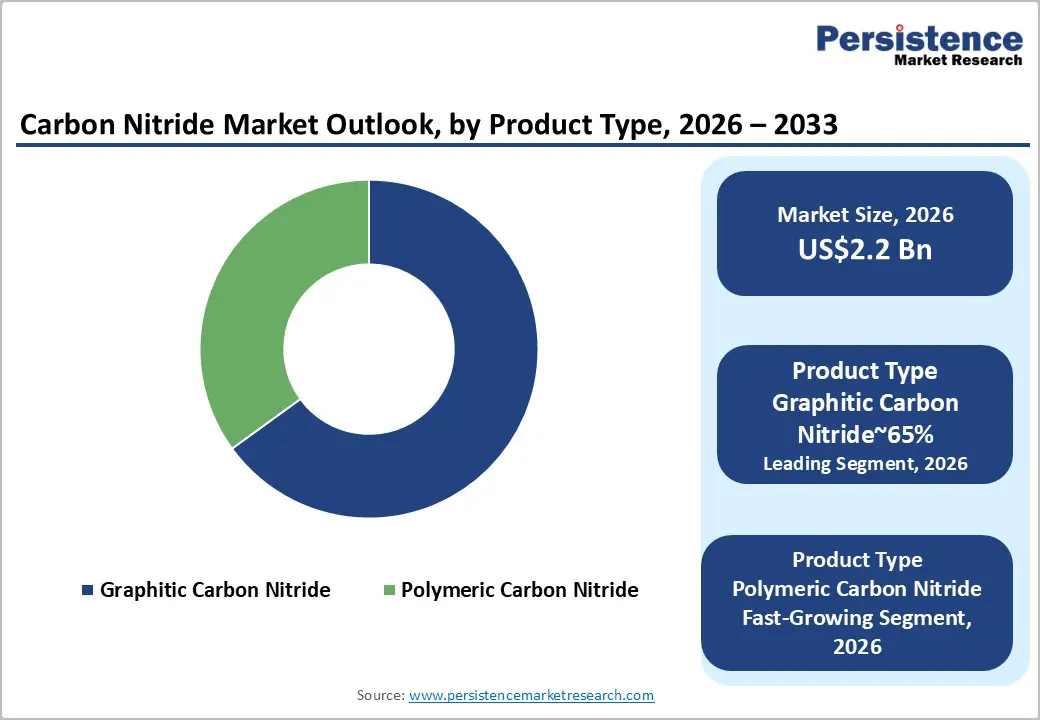

The global carbon nitride market size is likely to be valued at US$2.2 billion in 2026 and is expected to reach US$3.9 billion by 2033, growing at a CAGR of 8.5% during the forecast period between 2026 and 2033, driven by the rapid commercialization of graphitic carbon nitride (g-C3N4) in renewable energy sectors, specifically for photocatalytic water splitting and hydrogen production.

The burgeoning demand for superhard materials in aerospace and the miniaturization of semiconductor components in the electronics industry act as critical catalysts for sustained value appreciation. This transition toward sustainable, metal-free catalysts represents a fundamental shift in industrial material science.

Key Industry Highlights:

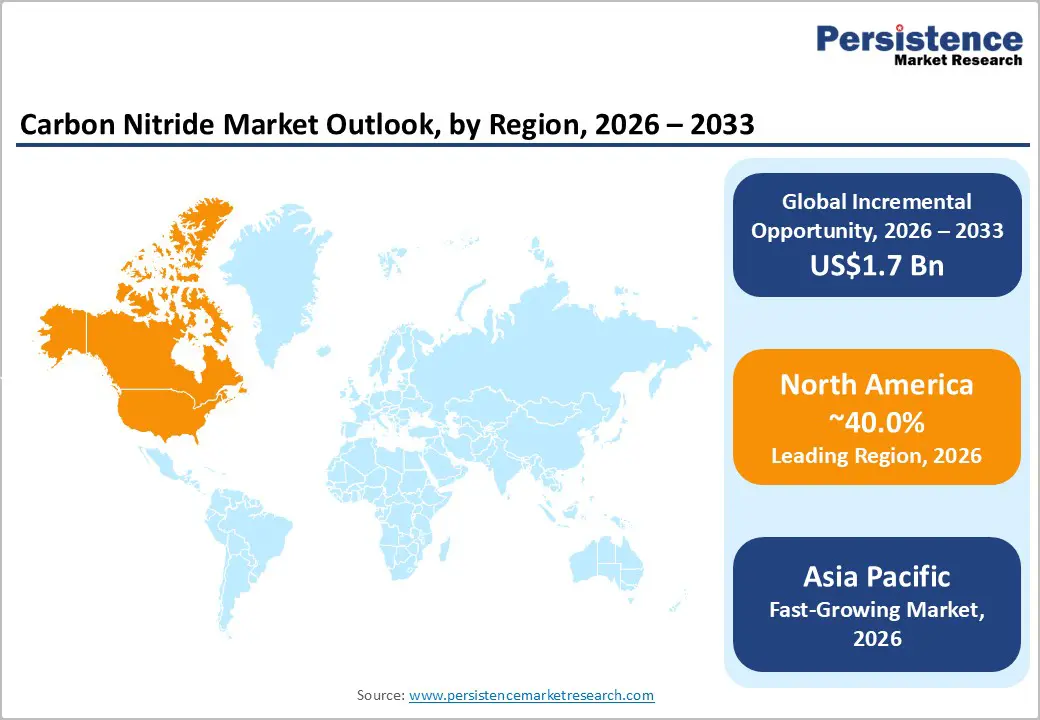

- Leading Market Region: North America is projected to remain the leading region in the carbon nitride market, accounting for approximately 40% share in 2026, underpinned by substantial investments in renewable energy, green hydrogen infrastructure, and nanotechnology-driven R&D.

- Leading Product Type: Graphitic carbon nitride (g-C3N4) is expected to lead with 60% share, favored for cost-effectiveness, thermal stability, visible-light photocatalysis, and industrial scalability across energy, environmental, and healthcare applications.

- Leading End-user: The electronics segment is projected to lead with 35% share, anchored by carbon nitride’s integration into semiconductors, LEDs, smart wearables, and high-performance power electronics.

- Key Industry Developments: Carbon Nitride Nanocomposites Validated for Multi-Modal Cancer Therapy. New research clinical summaries highlight the use of g-C3N4 as a biocompatible photosensitizer for combining photodynamic therapy (PDT) with gene and gas therapy in oncology.

| Key Insights | Details |

|---|---|

|

Carbon Nitride Market Size (2026E) |

US$2.2 Bn |

|

Market Value Forecast (2033F) |

US$3.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Acceleration of Green Hydrogen Production

The accelerating global shift toward cleaner energy systems is positioning graphitic carbon nitride as a critical enabler within green hydrogen production. Decarbonization mandates are intensifying demand for metal-free photocatalysts that reduce reliance on costly or scarce materials. Compared with conventional photocatalysts that depend on ultraviolet activation, graphitic carbon nitride can operate under visible light, improving practicality for large-scale hydrogen generation.

This functional advantage, combined with strong thermal stability and chemical resistance, reinforces its suitability for industrial photoreactors. The broader expansion of the hydrogen economy continues to strengthen market momentum for carbon nitride materials. Energy transition roadmaps increasingly emphasize scalable, low-emission hydrogen pathways, creating sustained pull for photocatalytic technologies that balance performance with cost efficiency.

Graphitic carbon nitride is gaining preference due to its ability to deliver hydrogen reactions without precious metal additives, aligning with long-term cost control objectives. Ongoing research activity and pilot-scale validation are translating into early commercial uptake, particularly where infrastructure developers prioritize durability, regulatory alignment, and operational simplicity.

Dispersibility and Interface Issue

Persistent dispersibility and interface limitations continue to constrain broader industrial adoption of carbon nitride materials. Bulk carbon nitride exhibits poor solubility in common solvents, complicating its use in composites, coatings, and liquid-phase manufacturing workflows. In photocatalytic systems, inefficient charge separation further weakens performance, as rapid electron recombination reduces usable reaction output.

Addressing these issues often requires advanced material modification steps, increasing processing complexity and cost. As a result, commercial deployment lags behind laboratory potential, reinforcing a structural gap between material promise and scalable integration across energy and chemical value chains.

In January 2025, engineered vacancy-defective carbon nitride nanowire clusters overcame long-standing dispersibility and charge recombination bottlenecks. This development underscores the severity of the restraint, highlighting that fundamental synthesis limitations must be resolved before wider adoption can occur. The need for highly controlled structural engineering reinforces capital intensity and technical barriers, particularly for manufacturers lacking advanced materials processing capabilities.

Expansion into Circular Economy and Waste-to-Energy Projects

Carbon nitride is positioned to play a meaningful role in circular economy and waste-to-energy frameworks, particularly through photocatalytic carbon dioxide conversion. Its ability to transform captured emissions into usable fuels aligns closely with tightening carbon-neutral mandates across industrial sectors. As policy support increasingly favors carbon capture and utilization pathways, carbon nitride offers a practical material route that connects emissions management with energy recovery.

This creates a secondary demand channel beyond hydrogen, allowing industrial operators to integrate decarbonization objectives directly into existing production systems while improving regulatory compliance and long-term sustainability positioning.

Beyond energy applications, water treatment represents a commercially accessible opportunity for carbon nitride deployment. Its photocatalytic properties enable effective breakdown of organic contaminants and pharmaceutical residues in wastewater streams. Growing regulatory pressure on effluent quality is accelerating interest in advanced treatment materials, particularly membrane-based solutions. This segment favors scale and reliability over extreme material purity, allowing carbon nitride suppliers to establish volume-driven revenue streams while higher-complexity applications continue to evolve.

Category–wise Analysis

Product Type Insights

Graphitic carbon nitride is expected to dominate the product type segment, accounting for a market share of approximately 60% in 2026, driven by its cost-effectiveness, high thermal stability, and robust performance as a metal-free photocatalyst, making it the preferred choice for renewable energy, environmental remediation, and emerging healthcare applications. Its industrial adoption is reinforced by advances in nanocomposites and heterojunctions with metal oxides to enhance charge separation, scalable thermal condensation synthesis using abundant precursors such as urea and melamine, and expansion into biosensors and drug delivery systems.

The material’s low production cost, ideal 2.7 eV band gap for visible-light photocatalysis, and biocompatibility support versatile use across water treatment, CO2 conversion, and flexible electronics. Recent trends include morphological engineering into 2D nanosheets and 0D quantum dots, hybrid material development, and alignment with sustainability initiatives, while regulatory compliance with environmental protection, safety standards, and green energy incentives further drives adoption. Leading suppliers are consolidating graphite carbon nitride’s position as the stable, scalable, and high-performance choice for industrial photocatalysis.

Polymeric Carbon Nitride (PCN) is likely to be the fastest-growing product type, fueled by its structural tunability, higher energy conversion efficiency, and metal-free composition. Industrial adoption is accelerating through copolymerization strategies, exfoliated polymeric nanosheets, and integration into artificial leaf prototypes for green hydrogen and solar fuel production. PCN’s tunable bandgap, 3D-ordered mesoporous frameworks, and dye-sensitization techniques enhance light absorption, charge transport, and catalytic efficiency, making it ideal for photocatalytic water splitting, CO2 utilization, and degradation of persistent organic pollutants such as PFAS.

Additional growth drivers include biomedical applications such as photodynamic therapy, regulatory alignment under REACH and PFAS guidelines, and clear safety protocols for industrial handling. Leading players such as American Elements, Nanochemazone, Sigma-Aldrich, and Carbon Nitride Tech are capitalizing on high-purity polymeric forms, flexible membranes, and specialized precursors, positioning PCN as a high-value, rapidly expanding segment that complements the established g-C3N4 market while enabling next-generation energy, environmental, and electronic applications.

End-user Insights

The electronics segment is expected to command approximately 35% of the market share, due to its unique role as a metal-free semiconductor and its integration into next-generation high-tech devices. Its adoption is reinforced by scalable 300-mm wafer production, advanced packaging for high-performance power electronics, and optoelectronic applications such as LEDs, leveraging graphitic carbon nitride visible-light absorption.

Key drivers include demand from smart wearables, 5G infrastructure, and energy-efficiency mandates, while trends such as heterojunction engineering, 3D crystalline phases, and AI-driven manufacturing enhance performance, consistency, and purity. The material’s metal-free nature, tunable bandgap, flexible form factors, and low-cost precursors make it ideal for high-voltage, miniaturized, and sustainable electronic components.

The healthcare segment is expected to be the fastest-growing end-user vertical, driven by carbon nitride’s superior biocompatibility, non-toxic profile, and stable fluorescence, making it suitable for sensitive medical applications. Industrial adoption is increasing in photothermal cancer therapy, point-of-care diagnostics, fluorescence imaging, and targeted drug delivery, particularly in emerging markets.

Growth factors include the ageing population, chronic disease prevalence, and demand for continuous health monitoring and diabetes management. Emerging trends encompass tissue engineering, antibacterial coatings, and synergistic phototherapies. Regulatory alignment through ISO quality standards, sustainable metal-free production, and compliance with emission targets support adoption. Beyond flagship imaging applications, carbon nitride is also gaining relevance in coatings, point-of-care diagnostics, and therapeutic support technologies, underscoring its expanding importance across the healthcare value chain.

Regional Insights

North America Carbon Nitride Market Trends

North America is expected to be the leading region, accounting for 40% of the total market share in 2026, underpinned by substantial investments in renewable energy and green hydrogen infrastructure. The U.S. drives regional dominance through nanotechnology innovation and biomedical research, supported by federal funding programs and strategic energy initiatives. Strong regulatory frameworks enable accelerated prototyping and industrial validation of advanced materials, reinforcing adoption across high-value sectors.

This combination of policy support, technological maturity, and industrial readiness positions North America as the primary hub for high-purity carbon nitride applications, particularly in energy and healthcare domains. The region’s infrastructure and end-use ecosystems further sustain leadership by linking research outputs to commercial deployment. Pharmaceutical and clean energy companies benefit from established supply chains, pilot-scale production facilities, and integrated R&D networks.

These structural advantages allow North America to maintain a relative advantage in regulatory compliance, technology adoption, and market scalability, ensuring sustained leadership as global demand for carbon nitride expands across high-performance and specialized applications.

Europe Carbon Nitride Market Trends

Europe represents a significant growth hub, supported by strong regulatory harmonization and sustainability mandates under the EU Green Deal. Germany, France, and the U.K. lead in integrating carbon nitride into wastewater treatment and automotive innovation, leveraging industrial partnerships and advanced chemical manufacturing capabilities. The region’s emphasis on metal-free, environmentally compliant catalysts aligns with strict environmental protocols, promoting stable adoption while minimizing exposure to toxic alternatives.

These structural and policy factors reinforce Europe’s position as a high-value, innovation-driven market within the global carbon nitride ecosystem. Regulatory oversight through frameworks such as REACH (Registration, Evaluation, Authorization and Restriction of chemicals) ensures that production and application of nanomaterials meet stringent safety and environmental standards, further shaping adoption patterns.

High-tech chemical and engineering partnerships enable the region to translate research into commercial-scale deployment, particularly in hydrogen energy, sustainable catalysis, and clean water infrastructure. Europe’s combination of policy alignment, infrastructure maturity, and demand for low-emission technologies positions it as a strategically important market with moderate growth potential relative to faster-expanding regions in Asia Pacific.

Asia Pacific Carbon Nitride Market Trends

Asia Pacific is likely to be the fastest-growing region, driven by rapid industrialization, nanotechnology advancements, and expanding clean energy infrastructure. China leads in production volume, leveraging a vast manufacturing base and government initiatives such as “Made in China 2025,” while Japan focuses on high-end electronic applications and India serves as a cost-effective hub for chemical manufacturing.

Regional growth is further supported by favorable industrial policies, low labor costs, and a substantial domestic demand for consumer electronics, renewable energy systems, and hydrogen infrastructure, reinforcing Asia Pacific’s strategic importance in the global carbon nitride value chain.

The region’s manufacturing ecosystem underpins both scale and technological advancement, dominating the supply chain for raw materials and battery-related components. China’s investments in photovoltaic and hydrogen projects, coupled with Japan’s leadership in solid-state battery technologies, create a volume-driven market for industrial-grade carbon nitride. South Korea and India contribute complementary capabilities, enhancing regional competitiveness in electronics, energy, and materials processing. This combination of policy support, infrastructure maturity, and industrial integration positions Asia Pacific as the primary growth engine for the sector.

Competitive Landscape

The global carbon nitride market is moderately fragmented, shaped by a combination of specialized nanomaterial suppliers and diversified chemical conglomerates. Key players such as American Elements, Merck KGaA through Sigma-Aldrich, and Reade International hold strong influence in the high-purity segment, where reliability, certification, and advanced material specifications define competitive power. The market operates under a dual structure, with a relatively consolidated upper tier serving electronics and pharmaceutical applications, while a fragmented base of regional Asian manufacturers focuses on bulk industrial-grade powders.

Competition centers on material purity, particle size control, and the ability to deliver functionalized and doped variants tailored to advanced applications. Regionally, North America and Europe lead in demand for certified high-performance materials, while Asia Pacific drives volume growth through cost-competitive production. Ongoing emphasis on material innovation and application-specific customization signals gradual premium-segment consolidation.

Key Industry Developments:

- In November 2025, researchers advanced nitrogen-deficient graphitic carbon nitride to enhance selective catalysis capabilities, improving performance in targeted reactions and driving more efficient and specialized industrial uses.

- In March 2025, researchers deployed Dual-Mechanism MoS @g-CN nanocomposites for multi-pollutant water treatment. The team introduced a new multifunctional nanomaterial that combined molybdenum disulfide and carbon nitride, which simultaneously adsorbed and photocatalytically removed drug molecules and azo dyes.

- In April 2024, researchers synthesized breakthrough ultrahard carbon nitrides that rivaled diamond. Their work confirmed that CN compounds exhibited hardness levels of 78–87 GPa, establishing them as a viable industrial alternative to synthetic diamonds for cutting tools and aerospace coatings.

Companies Covered in Carbon Nitride Market

- Merck KGaA

- ACS Material

- Reade International Corp.

- Nanjing XFNANO Materials

- Sigma Aldrich

- Green Science Alliance

- Carbodeon Ltd.

- Mknano (M K Impex Corp)

- American Elements

- US Research Nanomaterials

- SkySpring Nanomaterials

- Reinste Nano Ventures

- Alfa Aesar

- Bayer AG

- EPRUI Biotech Co., Ltd.

Frequently Asked Questions

The global carbon nitride market is valued at US$2.2 billion in 2026 and is projected to reach US$3.9 billion by 2033.

Carbon nitride is gaining importance due to its metal-free photocatalytic properties, growing use in green hydrogen production, and rising demand for superhard and miniaturized materials in electronics and aerospace applications.

The carbon nitride market is expected to grow at a CAGR of 8.5% between 2026 and 2033, supported by renewable energy commercialization and advanced material science innovation.

The most promising opportunities are emerging in biomedical applications such as drug delivery and imaging, along with photocatalytic water treatment and sustainable energy systems.

Key players include American Elements, Merck KGaA through Sigma-Aldrich, Reade International, Alfa Aesar, SkySpring Nanomaterials, Carbodeon, and Bayer AG.