- Advanced Materials

- Carbon Nanotubes Market

Carbon Nanotubes Market Size, Share, and Growth Forecast, 2026 - 2033

Carbon Nanotubes Market by Product Type (Multi-Walled CNTs (MWCNT), Single-Walled CNTs (SWCNT), Others), Application (Polymers, Energy, Others), Synthesis Method, and Regional Analysis for 2026 - 2033

Carbon Nanotubes Market Size and Trends Analysis

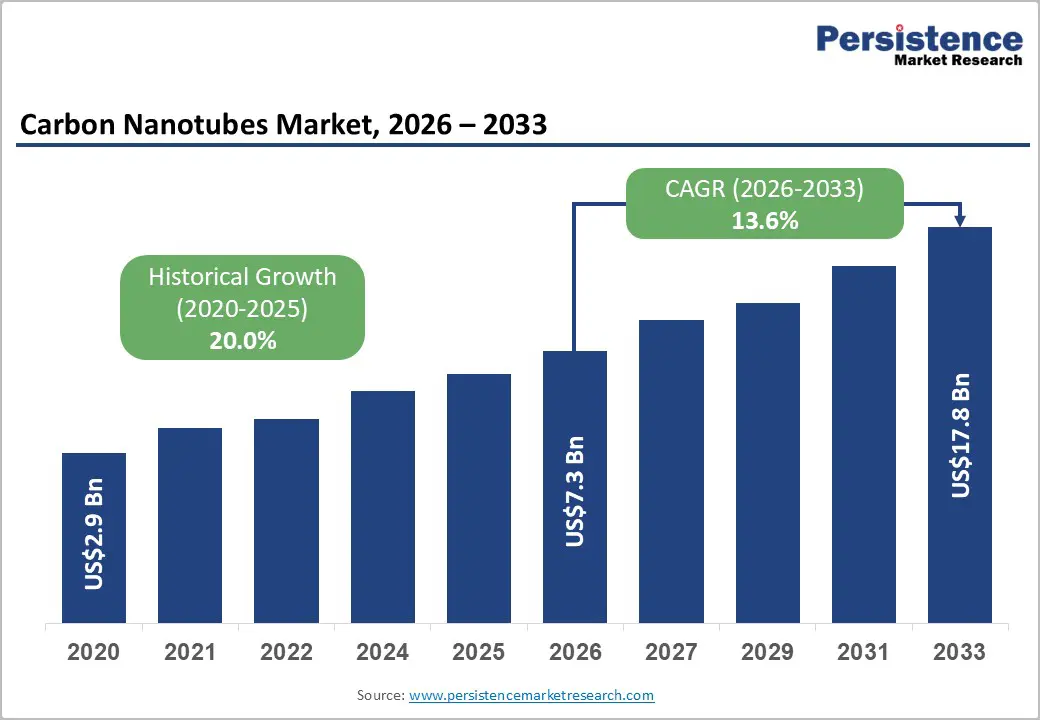

The global carbon nanotubes market size is likely to be valued at US$7.3 billion in 2026 and is expected to reach US$17.8 billion by 2033, growing at a CAGR of 13.6% during the forecast period from 2026 to 2033, driven by EV battery demand, high-conductivity additives for electronics, and lightweight reinforcement in polymers and composites.

IEA data show that global EV battery demand exceeded 750 GWh in 2023, while leading manufacturers are investing in domestic CNT and conductive-additive capacity to support batteries and grid storage. CNT demand is supported by performance needs that traditional conductive fillers do not meet as efficiently, especially in energy storage, conductive plastics, and advanced semiconductor materials.

Key Industry Highlights:

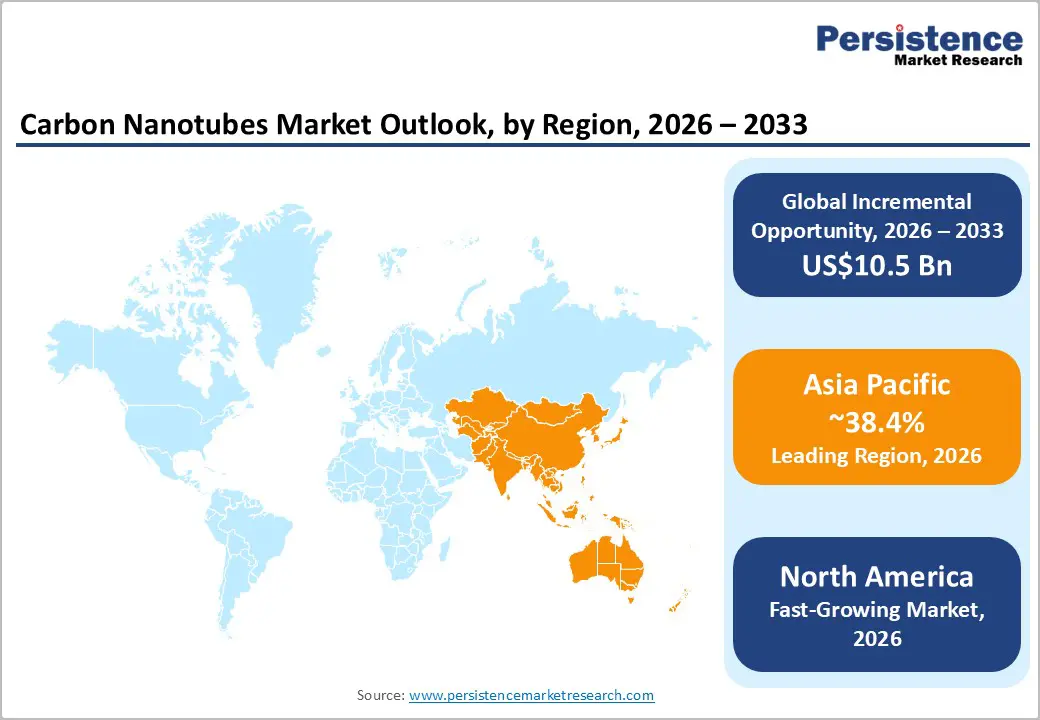

- Leading Region: Asia Pacific is projected to account for 38.4% market share in 2026, supported by strong battery manufacturing capacity, electronics production, and advanced materials processing across China, Japan, India, and ASEAN countries.

- Fastest-growing Region: North America, driven by EV battery localization, aerospace innovation, advanced electronics manufacturing, and government-supported domestic supply chain investments.

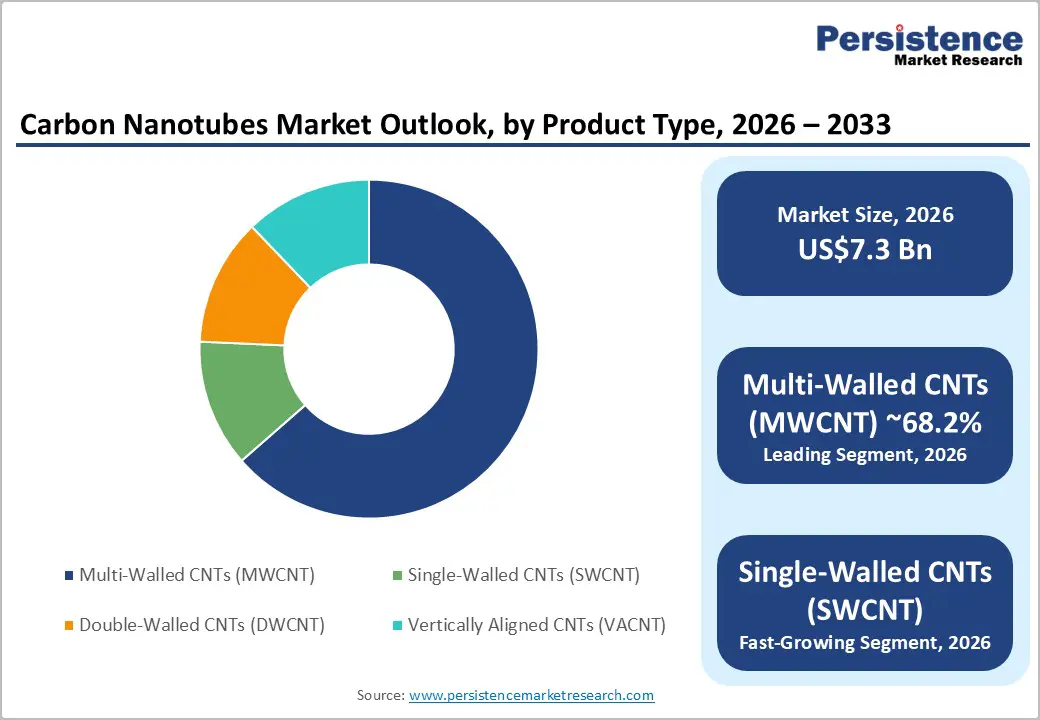

- Dominant Product Type: Multi-Walled Carbon Nanotubes (MWCNTs) are anticipated to account for approximately 68.2% of market revenue in 2026, due to their cost efficiency, scalability, and widespread use in conductive polymers, coatings, elastomers, and battery additives.

- Leading Application: Polymers are expected to hold approximately 63.7% market share in 2026, supported by growing adoption in automotive lightweighting, EMI shielding materials, industrial plastics, consumer electronics components, and advanced composite applications.

DRO Analysis

Driver - Rapid EV and Energy-Storage Buildout Is Raising Demand for CNT-Based Conductive Systems

IEA reported that EV battery demand reached more than 750 GWh in 2023, up 40% from 2022, with electric cars accounting for 95% of the increase. That matters for CNTs because battery makers use them to improve conductivity, cycle life, and rate performance in anodes, cathodes, and conductive dispersions. Cabot’s 2024 DOE-backed U.S. facility is a clear signal that OEMs and cell producers now treat CNTs as part of the domestic battery supply chain, not as an experimental input. Zeon’s 2025 agreement with SiAT and its 2026 production-line plan point to the same trend: battery performance targets are pulling CNT demand into commercial procurement.

High-Performance Materials Are Gaining Share in Electronics, Semiconductors, and Lightweight Composites

CNTs are attractive because they combine electrical conductivity, thermal management, and mechanical reinforcement in a single additive. Reports show strong CNT usage in plastics and composites, while Canatu’s 2025 Carbon Age program was launched specifically to advance CNT-enabled semiconductor technologies. That is important because the electronics value chain is increasingly prioritizing thinner, lighter, and more conductive materials for flexible devices, sensor platforms, and advanced packaging. In practice, CNTs help formulators reduce filler loading while maintaining performance, which creates a measurable design and cost advantage in electronics, automotive interiors, conductive coatings, and transparent conductive films.

Restraint - Manufacturing Cost, Product Handling, And Regulatory Compliance Remain Structural Barriers

Public market coverage continues to flag high manufacturing costs as a constraint, and the challenge is not only production yield but also consistent quality, dispersion, and safe handling. Cabot’s 2025 annual report notes that CNT-related products require extensive product testing and data, and that a subset of its multi-walled CNTs is classified under EU rules as carcinogen category 1B and specific target organ toxicant (lung) category 1 after repeated exposure. ECHA’s nanomaterial framework also requires nanoforms to be registered and characterized under REACH, which adds time, documentation, and compliance cost. For many downstream buyers, that raises qualification risk and slows switching from carbon black or other fillers.

Opportunity - SWCNT and Advanced Conductive Paste Solutions Can Capture Premium Battery and Semiconductor Demand

Single-walled CNTs are the most promising premium segment because they improve battery energy density, cycle life, and conductivity at lower loadings than conventional fillers. Zeon’s 2025 investment in SiAT shows that commercial buyers are already funding capacity expansion around SWCNT conductive paste for next-generation lithium-ion batteries. Canatu’s 2025 program also shows an adjacent opportunity in semiconductors, where CNTs can support device architectures that are reaching the limits of conventional silicon-based materials. This opens a pathway to higher-margin applications beyond bulk composites.

Regional localization of CNT supply can convert policy support into new manufacturing revenue.

The U.S. and Europe are both trying to localize critical-material supply chains, and CNTs fit that agenda because they sit inside battery, grid, and advanced-materials ecosystems. Cabot’s DOE-supported project in Michigan targets battery-grade CNTs and conductive dispersions for domestic supply, while OCSiAl’s 2025 Luxembourg hub is framed as a US$300 million deep-tech investment with more than 300 new jobs. In Asia, China-based capacity expansion for SWCNT dispersions shows the same localization trend at scale. For investors, the opportunity is not just volume growth; it is also the creation of region-specific supply chains where compliance, logistics, and customer qualification matter as much as chemistry.

Category-wise Analysis

Product Type Insights

Multi-Walled Carbon Nanotubes (MWCNTs) are anticipated to account for approximately 68.2% of market share, making them the leading product segment. Their dominance is attributed to lower production costs, higher scalability, and broad commercial adoption across conductive polymers, coatings, elastomers, and lithium-ion battery components. MWCNTs provide an effective balance between electrical conductivity, mechanical reinforcement, and processability, making them suitable for high-volume industrial applications.

Automotive manufacturers increasingly incorporate MWCNT-enhanced polymer compounds in lightweight vehicle components to improve durability and electromagnetic interference (EMI) shielding. In the electronics sector, MWCNTs are widely used in conductive plastics for connectors, housings, and antistatic packaging materials. Their established manufacturing ecosystem, supported by major suppliers such as LG Chem, Cabot Corporation, and Nanocyl, further strengthens their market position.

Single-Walled Carbon Nanotubes (SWCNTs) are anticipated to be the fastest-growing product segment. Unlike MWCNTs, SWCNTs offer exceptional electrical conductivity, superior electron mobility, and higher aspect ratios, enabling advanced performance in next-generation technologies. Their growing use in high-energy-density lithium-ion batteries is a major growth catalyst, as battery manufacturers seek materials that enhance conductivity while reducing additive loading.

For example, Zeon Corporation has expanded investments in SWCNT-based conductive materials for electric vehicle batteries, while OCSiAl continues to increase global production capacity for TUBALL™ SWCNT products used in energy storage systems. Beyond batteries, SWCNTs are gaining traction in semiconductor devices, transparent conductive films, flexible displays, and advanced sensors. Companies such as Canatu are leveraging SWCNT technology to develop semiconductor and electronics applications that require ultra-thin conductive networks.

Application Insights

Polymers are anticipated to account for 63.7% of market revenue in 2026. The segment's leadership stems from the extensive use of CNTs as reinforcement and conductivity-enhancing additives in thermoplastics, thermosets, and elastomer compounds. Carbon nanotubes improve tensile strength, thermal stability, impact resistance, and electrical conductivity, enabling manufacturers to develop lightweight, multifunctional materials for automotive, aerospace, electronics, and industrial applications.

In the automotive sector, CNT-reinforced polymers are increasingly replacing heavier metal components to support vehicle lightweighting initiatives and improve fuel efficiency. Electronics manufacturers also utilize CNT-enhanced polymers for EMI shielding in smartphones, laptops, and communication equipment. Packaging applications represent another growing area, particularly for antistatic materials used in semiconductor transportation and storage.

The energy segment is anticipated to be the fastest-growing application area throughout the forecast period, driven by accelerating investments in electric vehicles, renewable energy infrastructure, and advanced energy-storage technologies. Carbon nanotubes play a critical role in improving electrode conductivity, charge-discharge efficiency, and cycle life in lithium-ion batteries, solid-state batteries, and supercapacitors.

The rapid expansion of the global EV market continues to create substantial demand for CNT-based conductive additives, particularly SWCNT formulations that enhance battery performance at lower loading levels. For instance, Cabot Corporation introduced its LITX® conductive additive platform to address growing energy-storage requirements, while Zeon Corporation has expanded SWCNT production capacity specifically for next-generation EV battery applications.

Regional Insights

North America Carbon Nanotubes Market Trends

North America is anticipated to remain the fastest-growing developed regional market for carbon nanotubes (CNTs) during the forecast period. Growth is primarily supported by accelerating investments in electric vehicle (EV) battery manufacturing, aerospace innovation, advanced electronics, and high-performance polymer composites. Government-backed initiatives aimed at strengthening domestic battery supply chains and reducing dependence on imported critical materials are creating favorable conditions for CNT adoption.

U.S. Carbon Nanotubes Market Trends

The U.S. represents the largest CNT market in North America. Demand is increasingly driven by battery-grade CNTs used in lithium-ion batteries, conductive additives, and advanced composite materials. Federal investments through clean-energy and advanced manufacturing programs have encouraged domestic production of battery materials and conductive nanomaterials.

The country also benefits from strong aerospace and defense sectors, where CNT-enhanced composites are utilized for lightweight structural applications. Recent developments such as Cabot Corporation's DOE-supported expansion of CNT manufacturing capacity demonstrate the transition from laboratory-scale innovation to commercial-scale production.

Canada Carbon Nanotubes Market Trends

Canada is emerging as an important market for CNT-enabled energy storage, clean technology, and advanced manufacturing applications. The country's focus on sustainable industrial development, battery supply chain investments, and critical minerals processing supports growing demand for advanced conductive materials.

Canadian research institutions and industrial partners are actively exploring CNT applications in renewable energy systems, conductive coatings, and next-generation composite materials. Although smaller than the U.S. market, Canada is expected to benefit from increasing regional integration of North American battery and electronics supply chains.

Europe Carbon Nanotubes Market Trends

Europe is expected to account for approximately 20% of the market share in 2026 and remains a strategically important region due to its advanced manufacturing base, strong regulatory framework, and growing focus on battery technology and sustainable materials. Demand is concentrated in high-value applications including electric mobility, aerospace, specialty chemicals, industrial electronics, and semiconductor manufacturing. While regulatory compliance requirements increase market entry barriers, they also encourage the adoption of high-quality CNT products with proven safety and performance characteristics.

Germany Carbon Nanotubes Market Trends

Germany is the largest CNT market in Europe. The country's leadership stems from its extensive automotive manufacturing ecosystem, advanced battery development initiatives, and strong industrial materials sector. German automotive manufacturers increasingly utilize CNT-reinforced polymers and conductive materials to support lightweight vehicle designs and EV battery performance improvements. The country's emphasis on industrial innovation continues to drive demand for advanced nanomaterials.

U.K. Carbon Nanotubes Market Trends

The U.K. represents one of Europe's leading innovation centers for CNT research and commercialization. Growth is supported by investments in semiconductor technologies, aerospace engineering, and advanced materials research. Universities, technology startups, and industrial manufacturers are collaborating to develop CNT applications for flexible electronics, sensors, and next-generation energy storage systems.

France Carbon Nanotubes Market Trends

France benefits from a strong specialty chemicals sector and increasing investments in battery manufacturing and clean-energy technologies. The country's emphasis on industrial sustainability and advanced materials development has accelerated adoption of CNTs in conductive coatings, polymer composites, and energy-storage applications. Strategic support for domestic battery supply chains is expected to further strengthen demand.

Benelux Region Carbon Nanotubes Market Trends

The Benelux countries, particularly Luxembourg and Belgium, play an important role in the European CNT ecosystem. Luxembourg has gained prominence through OCSiAl's planned US$300 million nanotube manufacturing hub, while Belgium remains home to key CNT technology developers and specialty materials companies. These investments reinforce the region's position as a center for advanced nanomaterial commercialization.

Asia Pacific Carbon Nanotubes Market Trends

Asia Pacific is anticipated to remain the largest regional market for carbon nanotubes, accounting for approximately 38.4% of market revenue in 2026. The region's leadership is driven by its extensive electronics manufacturing base, dominant battery production capacity, expanding automotive industry, and rapidly growing renewable energy sector. Asia Pacific also benefits from lower manufacturing costs, established supply chains, and significant investments in advanced materials production.

China Carbon Nanotubes Market Trends

China is expected to account for approximately 34% of the Asia Pacific market in 2026, making it the largest national CNT market globally. The country dominates lithium-ion battery production, consumer electronics manufacturing, and electric vehicle supply chains. CNT demand is expanding rapidly due to the increasing use of conductive additives in EV batteries and energy-storage systems.

Investments in large-scale CNT production facilities and dispersion technologies continue to strengthen China's leadership position. OCSiAl's plan to significantly expand TUBALL™ BATT dispersion capacity in China reflects the country's growing importance in advanced battery materials.

Japan Carbon Nanotubes Market Trends

Japan is expected to represent approximately 19.3% of the regional market in 2026 and remains a global leader in CNT technology innovation. High-value applications in batteries, semiconductors, electronics, and advanced materials characterize the country. Japanese companies such as Zeon Corporation continue to invest heavily in Single-Walled Carbon Nanotube (SWCNT) production and battery-related technologies. The country's focus on quality, precision manufacturing, and advanced research supports continued growth in premium CNT applications.

India Carbon Nanotubes Market Trends

India is expected to account for approximately 6% of the Asia Pacific market in 2026 and is emerging as one of the region's fastest-growing CNT consumers. Growth is supported by government initiatives promoting domestic electronics manufacturing, EV adoption, renewable energy deployment, and advanced materials production.

Increasing investments in battery manufacturing and industrial modernization are expected to drive demand for CNT-based conductive materials, polymer composites, and energy-storage applications over the forecast period.

Competitive Landscape

The global carbon nanotubes market is concentrated but still competitive. Public market coverage names a core group of leaders, LG Chem, Nanocyl, Arkema, Cabot, OCSiAl, Resonac, and others, while also noting that companies compete through partnerships, collaborations, capacity additions, and new product development. Exact share splits are not consistently disclosed, which makes precise global concentration ratios difficult to verify, but the visible pattern is clear: a small group controls the most strategic production capability, and several regional specialists serve niche applications. Cost intensity and regulatory burden raise the barrier to entry, which helps incumbents defend position.

The dominant strategies are capacity expansion, battery-focused product development, and regional localization. Leaders are pairing R&D with manufacturing investments so they can meet customer qualification requirements and protect margins. The clearest differentiators are dispersion quality, battery performance, regulatory readiness, and the ability to supply at scale without compromising consistency. Partnerships with battery makers, semicon firms, and governments are becoming standard rather than optional.

Key Industry Developments:

- In July 2025, Cabot Corporation announced the launch of its new LITX® 95F conductive carbon engineered for lithium-ion energy storage systems (ESS), designed to improve conductivity, extend battery cycle life, and support the growing demand for grid-scale and commercial energy storage applications.

- In November 2025, Cabot Corporation's LITX® 95F conductive carbon was recognized among the "Top 10 Exhibits of 2025" at the China International Import Expo (CIIE), highlighting the company's growing presence in advanced battery materials and energy-storage technologies.

Companies Covered in Carbon Nanotubes Market

- LG Chem Ltd.

- Cabot Corporation

- OCSiAl

- Arkema S.A.

- Nanocyl S.A.

- Zeon Corporation

- Resonac Holdings Corporation

- Jiangsu Cnano Technology Co., Ltd.

- Kumho Petrochemical Co., Ltd.

- CHASM Advanced Materials, Inc.

- Thomas Swan & Co. Ltd.

- NoPo Nanotechnologies India Pvt. Ltd.

- Carbon Solutions, Inc.

- Hanwha Solutions Corporation

- Hyperion Catalysis International, Inc.

- Canatu Plc

Frequently Asked Questions

The global carbon nanotubes market is estimated to be valued at US$7.3 billion in 2026.

The carbon nanotubes market is projected to reach US$17.8 billion by 2033.

Key trends include rising utilization of CNTs in lithium-ion batteries, growing commercialization of Single-Walled Carbon Nanotubes (SWCNTs), increasing investments in domestic battery supply chains, expansion of CNT applications in semiconductors and flexible electronics, and capacity expansions by leading manufacturers.

Multi-Walled Carbon Nanotubes (MWCNTs) lead the market, accounting for an anticipated 68.2% share, due to their cost-effectiveness, scalability, and extensive use in conductive plastics, coatings, elastomers, and battery additives.

The carbon nanotubes market is anticipated to expand at a CAGR of 13.6% between 2026 and 2033.

Major companies include LG Chem, Cabot Corporation, OCSiAl, Arkema SA, and Zeon Corporation.