- Medical Devices

- Post Mastectomy Supplies Market

Post Mastectomy Supplies Market Size, Share, and Growth Forecast 2026 – 2033

Post Mastectomy Supplies Market by Material Type (Silicone, Foam/Fabric, Other), Product Type (Breast Forms, Others), Application (Post-Mastectomy Care, Other), Distribution Channel (Retail Pharmacies/Stores, Others), End-user, and Regional Analysis 2026–2033

Post Mastectomy Supplies Market Size and Trends Analysis

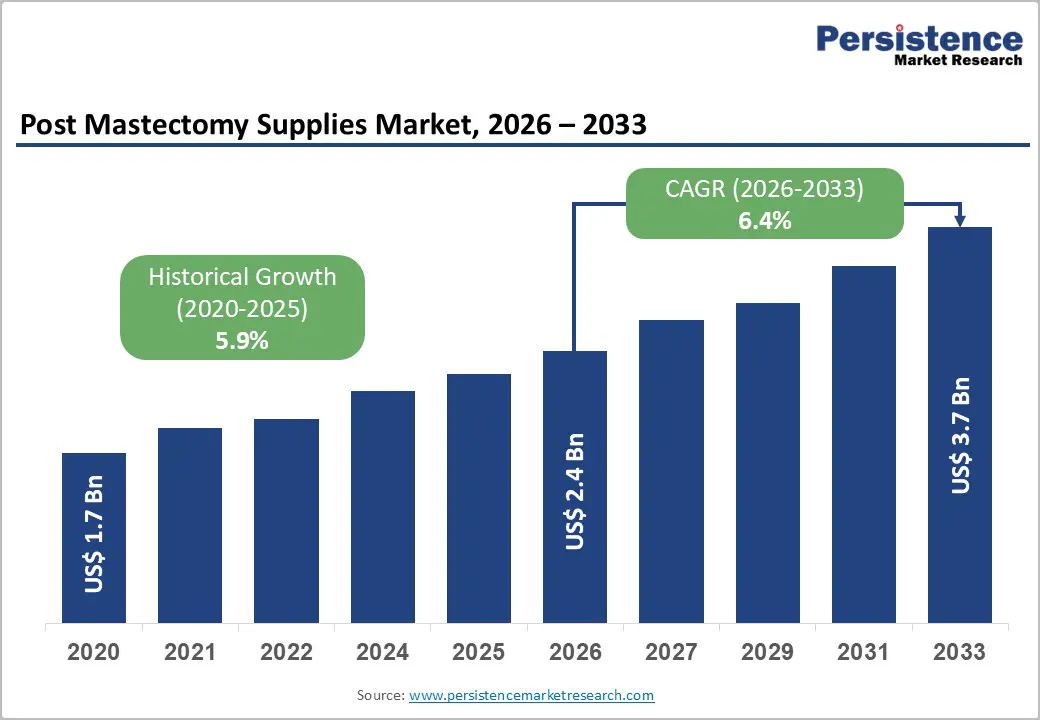

The global post mastectomy supplies market size is projected to be valued at US$ 2.4 billion in 2026 and is projected to reach US$ 3.7 billion by 2033, growing at a CAGR of 6.4% during the forecast period from 2026 to 2033, driven by the rising global incidence of breast cancer, significant advancements in 3D-printed custom prosthetics, and favorable updates to international reimbursement policies.

As healthcare systems shift toward patient-centric recovery models, the demand for high-fidelity silicone forms and specialized post-surgical apparel has become a critical component of comprehensive oncology care. Concurrently, significant technological advancements in material science, particularly silicone-based formulations with moisture-wicking and hypoallergenic properties, combined with accelerating e-commerce adoption across developed and emerging markets, are creating robust demand for specialized post-mastectomy solutions.

Key Industry Highlights:

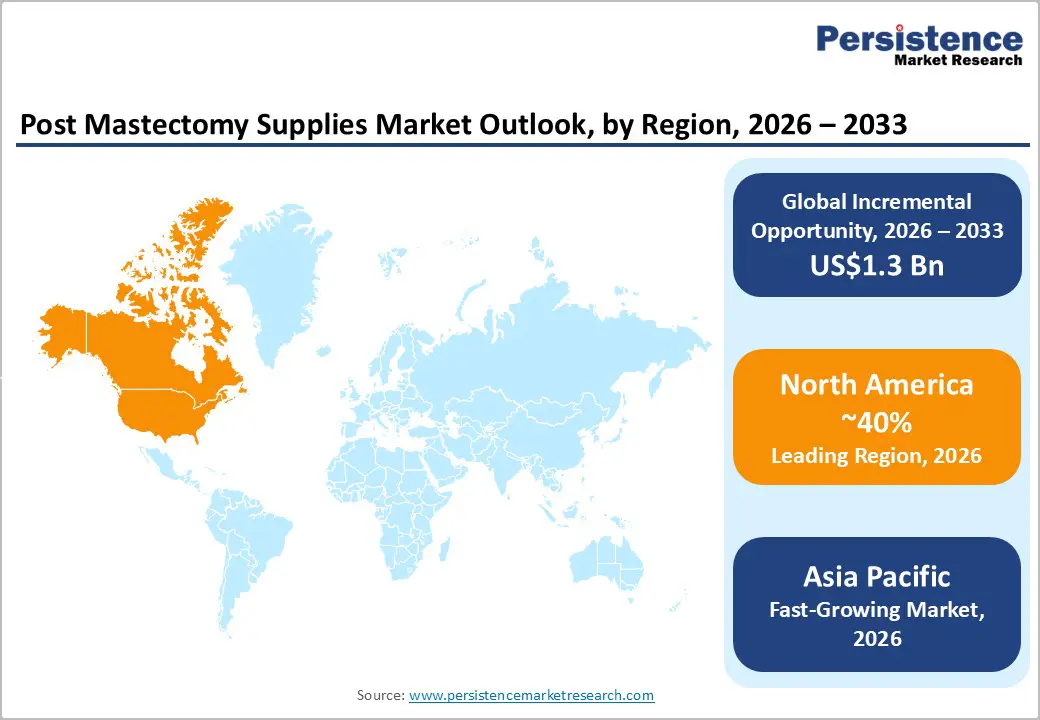

- Leading Region: North America to lead with a market share of 40%, supported by its dominant value share and strengthened reimbursement frameworks.

- Fastest-growing Region: Asia Pacific, driven by rising breast cancer awareness, improving diagnostic penetration, and rapid manufacturing scale-up in China and India.

- Leading Material: Silicone to dominate with approximately 80% share, favored for biocompatibility, body-temperature conformity, realistic feel, and widespread clinical adoption across hospitals, oncology clinics, and specialty retailers.

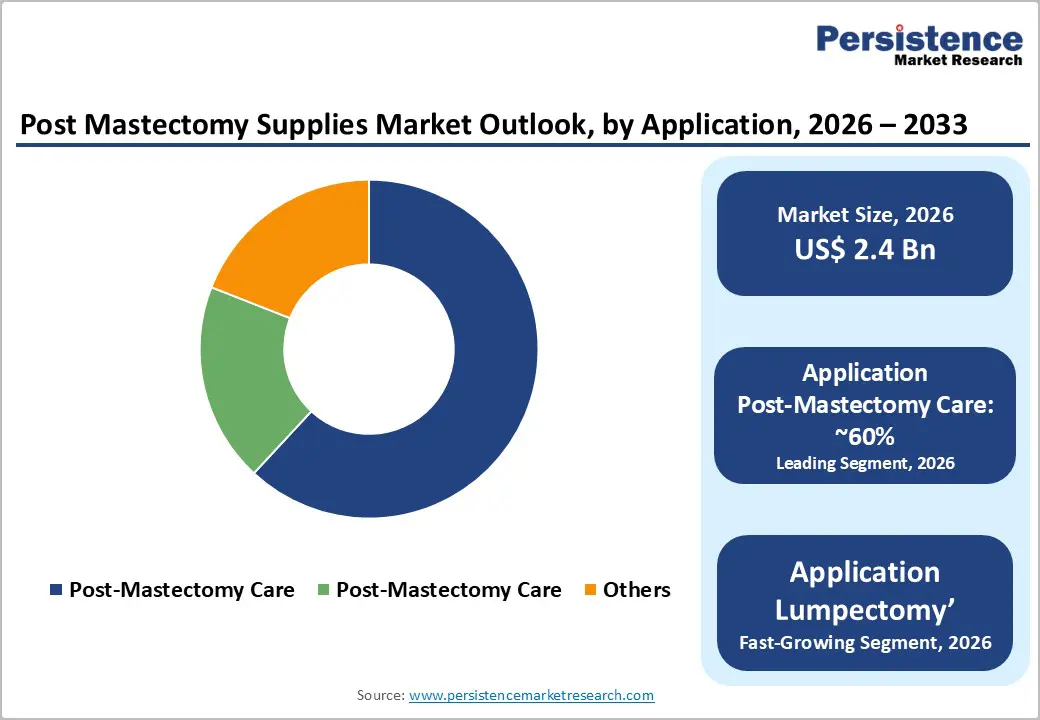

- Leading Application: Post-mastectomy to account for ~60% share, supported by high surgical volumes, reimbursement mandates, and integration into survivorship and clinical care pathways.

| Key Insights | Details |

|---|---|

| Post Mastectomy Supplies Market Size (2026E) | US$ 2.4 Bn |

| Market Value Forecast (2033F) | US$ 3.7 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Escalating Breast Cancer Incidence and Survivorship Rates

The post-mastectomy supplies market is structurally driven by the rising global breast cancer burden and expanding survivorship base. Incidence growth across developed markets, reinforced by early detection programs and aging demographics, is increasing mastectomy and lumpectomy volumes. Parallel improvements in survival outcomes have extended post-operative care timelines, converting episodic demand into long-duration replacement cycles. In the U.S. alone, a large and growing survivor population sustains repeat demand for prosthetics, alternative formats, and lifestyle-integrated solutions. This dynamic reinforces predictable volume expansion and underpins medium-term market visibility, aligning demand growth with procedural intensity rather than discretionary consumption.

The WHO's International Agency for Research on Cancer (IARC) projects 3.2 million new breast cancer cases annually by 2050, a 38% increase, with deaths rising to 1.1 million yearly, disproportionately affecting lower HDI countries due to factors such as obesity, alcohol, and air pollution. This epidemiological shift is intensifying demand in emerging markets as screening penetration improves and treatment access expands. However, uneven reimbursement frameworks and affordability constraints continue to shape adoption velocity, positioning regulatory alignment and cost-efficient supply models as critical market differentiators.

Social Stigma and Psychological Barriers in Emerging Markets

Market adoption in emerging economies remains constrained by persistent social stigma and psychological resistance surrounding post-mastectomy body image. In several Asia Pacific and Latin American markets, cultural taboos continue to suppress proactive use of external prostheses, despite rising surgical volumes. Limited patient education around the clinical benefits of weighted breast forms, including lymphedema prevention and postural correction, reduces perceived medical necessity. As a result, demand skews toward informal or improvised solutions, compressing addressable volumes within formal distribution channels.

These behavioral barriers are reinforced by fragmented retail infrastructure and uneven access to trained fitment professionals, weakening conversion even where awareness exists. The constraint is most pronounced in the Breast Forms and Other Apparel segments, where clinical validation alone has not translated into sustained uptake. Without coordinated education initiatives, reimbursement alignment, and healthcare-led advocacy, penetration rates in high-growth territories are likely to lag epidemiological expansion, moderating near-term realization of regional demand potential.

Technology-Enabled Personalization and Adjacent Care Expansion

The convergence of digital health, advanced textiles, and direct-to-consumer models is creating a structurally attractive opportunity within post-mastectomy care. Smart mastectomy bras incorporating temperature regulation and moisture management are addressing post-radiation sensitivity and long-duration wear requirements, supporting premiumization. In parallel, smartphone-enabled 3D scanning and virtual fitting services are reshaping distribution economics by improving sizing accuracy, expanding rural access, and reinforcing privacy-led adoption. These digital-first models are structurally positioned to compress return rates, strengthen e-commerce margins, and reduce dependency on specialized physical retail infrastructure.

Beyond core prosthetics, product diversification into lumpectomy-specific solutions, lymphedema management, and integrated wellness applications is expanding the addressable market. Breast-conserving procedures and post-surgical lymphedema remain underpenetrated despite clear clinical need, while integrated posture, rehabilitation, and survivorship-focused solutions are capturing incremental healthcare and lifestyle spending. This shift favors manufacturers with design breadth, clinical alignment, and access to oncology and rehabilitation distribution ecosystems.

Category–wise Analysis

Material Insights

Silicone is projected to dominate the breast prosthetics market, accounting for approximately 80% share in 2026, underpinned by its entrenched clinical role, regulatory acceptance, and installed base across post-mastectomy rehabilitation pathways, specialty medical boutiques, and oncology-linked care settings. Adoption remains anchored by biocompatibility, thermodynamic conformity to body temperature, and tissue-like drape that restores natural weight distribution, with providers prioritizing postural balance, long-term wearability, and aesthetic realism in daily-use prostheses. Ongoing platform evolution, including super-lightweight silicone chemistries, phase-change thermal regulation, 3D scanning–enabled customization, and direct-to-consumer fitting workflows, continues to reinforce replacement cycles and utilization intensity. Vendors such as Amoena, Anita, and Adapt-to-Me are expanding product ecosystems with adhesive “contact” forms and inclusive personalization to lock in long-term user loyalty. This combination of mature regulatory infrastructure, ecosystem lock-in, and predictable replacement demand sustains silicon’s dominance within structured clinical and retail deployment models.

Foam/Fabrics is likely to be the fastest-growing segment within the breast prosthetics market, driven by unmet comfort needs, post-radiation skin sensitivity, and weight limitations associated with bilateral procedures across immediate post-op recovery, sleep, leisure wear, and active lifestyle use cases. Growth is being catalyzed by smart antimicrobial fabrics, open-cell memory foams, seamless 3D knitting, and bio-based materials that materially improve breathability, skin tolerance, and day-one usability. Accelerating adoption is supported by outpatient surgery pathways, clinician guidance for lymphatic health, and reimbursement code expansion for soft interface garments, lowering friction for first-time adopters. Companies, including Knitted Knockouts, Amoena, and Anita, are scaling leisure-first product lines and clinic partnerships to capture early-cycle demand and embed switching costs. As clinical validation, reimbursement clarity, and workforce familiarity improve, this segment is expected to outpace overall market growth over the forecast period.

Application Insights

Post-mastectomy is anticipated to dominate the breast prosthetics market, accounting for approximately 60% share in 2026, underpinned by sustained surgical volumes, reimbursement mandates, and an entrenched installed base across oncology clinics, hospital discharge pathways, specialty boutiques, and home recovery workflows. Adoption remains anchored by non-invasive body image restoration, rapid post-surgical continuity of care, and clinical reliability, with providers prioritizing standardized fitting protocols, predictable replacement cycles, and integration into survivorship programs in high-volume care settings. Ongoing platform evolution, including 3D scanning and in-office printing, digital fitting tools, and clinic-embedded access models, continues to reinforce replacement frequency and utilization intensity. Vendors such as Anita International and American Breast Care are expanding portfolios with customizable forms, lifestyle-specific designs, and omnichannel distribution to lock in longitudinal patient pathways. This combination of mature reimbursement infrastructure, ecosystem lock-in, and predictable demand sustains post-mastectomy leadership within structured clinical deployment models.

Lumpectomy is projected to be the fastest-growing segment within the breast prosthetics market, driven by earlier detection, rising breast-conserving surgery volumes, and unmet needs around symmetry restoration across outpatient recovery, radiation follow-up, and everyday wear use cases. Growth is being catalyzed by ultra-thin partial shells, micro-shapers, adjustable-volume designs, and adhesive contact forms that materially improve comfort, concealment, and personalization for asymmetry management. Accelerating adoption is supported by oncoplastic care pathways, insurer reclassification of shapers as medically necessary devices, and specialty retail expansion, lowering access barriers for first-time users. Companies, including Amoena and Nearly Me, are scaling lumpectomy-specific product lines and clinic partnerships to capture early-cycle demand and embed switching costs. As clinical validation, reimbursement clarity, and provider familiarity improve, this segment is expected to outpace overall market growth over the forecast period.

Regional Insights

North America Post-mastectomy Supplies Market Trends

North America is expected to lead, accounting for approximately 40% of global value in 2026, underpinned by a mature regulatory and reimbursement environment and a highly developed healthcare infrastructure. The U.S. drives regional dominance with a dense oncology network, widespread insurance coverage, and established protocols for post-operative care, while Canada contributes through publicly funded health programs despite a smaller patient population. Rising breast cancer incidence and high survivorship create a continuously expanding patient base requiring replacement prosthetics, supportive apparel, and recovery aids. The region benefits from advanced distribution networks, accredited fitting centers, and strong integration of e-commerce channels and digital health solutions, which together facilitate efficient access to premium and lifestyle-aligned products. Insurance frameworks support broad adoption and consistent revenue generation across hospital, retail, and digital channels.

Regulatory oversight is well-established, providing structured pathways for product approval and standardized coverage, which reduces compliance complexity and supports market entry for innovative solutions. The competitive landscape shows moderate concentration, with market leadership determined by distribution strength, customization capabilities, and integration of digital services. Strategic investment activity is focused on digital health infrastructure, virtual fitting technologies, and operational efficiency rather than new brand launches, reflecting the importance of scale and innovation in maintaining competitive advantage. North America’s combination of regulatory stability, technology adoption, and high patient engagement positions it as the benchmark region for market growth and innovation.

Europe Post Mastectomy Supplies Market Trends

Europe represents a significant post-mastectomy supplies market, driven by mature healthcare systems, comprehensive insurance coverage, and well-established clinical infrastructure. Germany serves as the primary hub for clinical innovation and premium prosthetic adoption, supported by extensive public reimbursement mechanisms. The United Kingdom and France contribute through specialized retail channels and strong lifestyle-aligned product positioning, enabling high-margin growth despite budgetary constraints in public healthcare systems. Southern European countries display slower uptake due to lower per-capita healthcare spending and less comprehensive coverage for discretionary post-operative products. Harmonized regulatory oversight under the EU Medical Device Regulation ensures consistent safety and quality standards, reducing compliance complexity across member states while enabling faster market access for innovative prosthetic and apparel solutions.

The European competitive landscape is moderately concentrated, with German manufacturers maintaining leadership through integrated distribution, clinical relationships, and product customization capabilities. UK and French players capture meaningful regional shares through boutique and lifestyle-oriented positioning. Investment activity emphasizes platform consolidation, digital health integration, and sustainability initiatives, reflecting policy and market alignment with long-term innovation objectives. Market dynamics are shaped by regulatory harmonization, high survivorship rates, and infrastructure maturity, positioning Europe as a benchmark for premium product adoption and controlled growth relative to other global regions.

Asia Pacific Post Mastectomy Supplies Market Trends

Asia Pacific is likely to be the fastest-growing regional market, supported by a combination of rising breast cancer incidence, expanding private healthcare infrastructure, and large patient populations across China, India, and Japan. China constitutes the largest market within the region, with increasing incidence rates and growing middle-class access to care driving adoption. India presents significant long-term growth potential due to its young and vibrant population and improving cancer detection programs. Japan demonstrates mature market characteristics, supported by universal healthcare coverage and strong product awareness. ASEAN economies such as Thailand, Vietnam, and Indonesia contribute to emerging opportunities as healthcare access improves and regional manufacturing capabilities expand. The overall market benefits from cost-competitive local production of silicone and foam prosthetics, enabling both value-tier segments and export-oriented supply chains.

Infrastructure expansion and digital adoption are key drivers in Asia Pacific. E-commerce platforms have enabled privacy-sensitive purchasing for post-mastectomy products, overcoming limitations of traditional retail. Government healthcare initiatives in China and India provide subsidized access to post-operative care, while manufacturing localization allows global brands to optimize supply chains and reduce production costs. Collectively, these factors position Asia Pacific as the fastest-growing region globally with sustained long-term market potential relative to more mature North American and European markets.

Competitive Landscape

The global post mastectomy supplies market is moderately consolidated, with top players such as Amoena, Anita, and American Breast Care controlling around 60% of total revenue. Leading firms focus on technological differentiation in breathability, weight reduction, and anatomical accuracy, while acquiring smaller boutiques to expand geographic reach.

Mid-tier and DTC brands capture 20–30% of the market through product innovation, lifestyle positioning, and digital engagement. Regional and specialty players hold 15–25%, serving niche applications and maintaining professional relationships with hospitals and orthopedic retailers. Competition centers on brand loyalty, customization, and reimbursement frameworks rather than price, supporting healthy margins and ongoing innovation.

Key Industry Developments:

- In January 2025, Halder transferred Amoena to a German family office with financing from Apera Asset Management to support global expansion. This move secured the capital needed for Amoena's next phase of digital and international growth.

- In October 2024, researchers published a study in Advanced Science on a smart 3D-printed prosthesis that sensed cancer relapse. This innovation transformed the external prosthesis from a passive aesthetic device into an active diagnostic tool, potentially creating a new "Smart Prosthetics" sub-category.

- In January 2024, the Lymphedema Treatment Act officially went into effect, mandating Medicare Part B coverage for compression garments. This landmark legislation enabled millions of breast cancer survivors to access medical-grade compression bras and sleeves with high reimbursement, stabilizing the "Other Apparel" segment's recurring revenue.

Companies Covered in Post Mastectomy Supplies Market

- Amoena Medizin-Orthopedic Technik GmbH

- Anita Dr. Helbig GmbH

- Jodee Post-Mastectomy Fashions

- Nearly Me (Essence Group)

- Trulife

- Nicola Jane

- American Breast Care (ABC)

- Symmetra (Grace & Able)

- Marena

- Can-Care Pte Ltd

- Coloplast (Comfort-U)

- Tytex

- AnaOno

- Intertrade AG

- Royce Lingerie

- Lantana Health

Frequently Asked Questions

The global post mastectomy supplies market is projected to be valued at US$2.4 billion in 2026 and is expected to reach US$3.7 billion by 2033, reflecting steady expansion across oncology recovery care.

Demand is increasing due to the rising global incidence of breast cancer, improved survival rates, favorable reimbursement frameworks, and growing adoption of patient-centric recovery and aesthetic rehabilitation solutions.

The post mastectomy supplies market is expected to grow at a CAGR of 6.4% between 2026 and 2033, supported by material innovation and expanding insurance coverage.

The fastest growth opportunities are emerging in Asia Pacific, driven by rising breast cancer awareness, expanding diagnostic penetration, cost-efficient manufacturing, and increasing access to post-surgical care products.

Key players in the post mastectomy supplies market include Amoena, Anita Dr. Helbig, Jodee Post-Mastectomy Fashions, Nearly Me, Trulife, Nicola Jane, American Breast Care, Marena, Can-Care, Coloplast, Tytex, AnaOno, Royce Lingerie, and Intertrade AG.