- Technology

- Docker Monitoring Market

Docker Monitoring Market Size, Share, Trends, and Growth Forecast, 2026 - 2033

Docker Monitoring market by Component (Solutions, Services), Deployment Mode (Cloud based, On premises, Hybrid), Organization Size (Large Enterprises, Small & Medium Enterprises (SMEs) Industry (IT & Telecommunications, BFSI (Banking, Financial Services, Insurance), Retail & E‑Commerce, Healthcare & Life Sciences, Manufacturing, Miscellaneous) and Regional Analysis for 2026 - 2033

Docker Monitoring Market Size and Trends Analysis

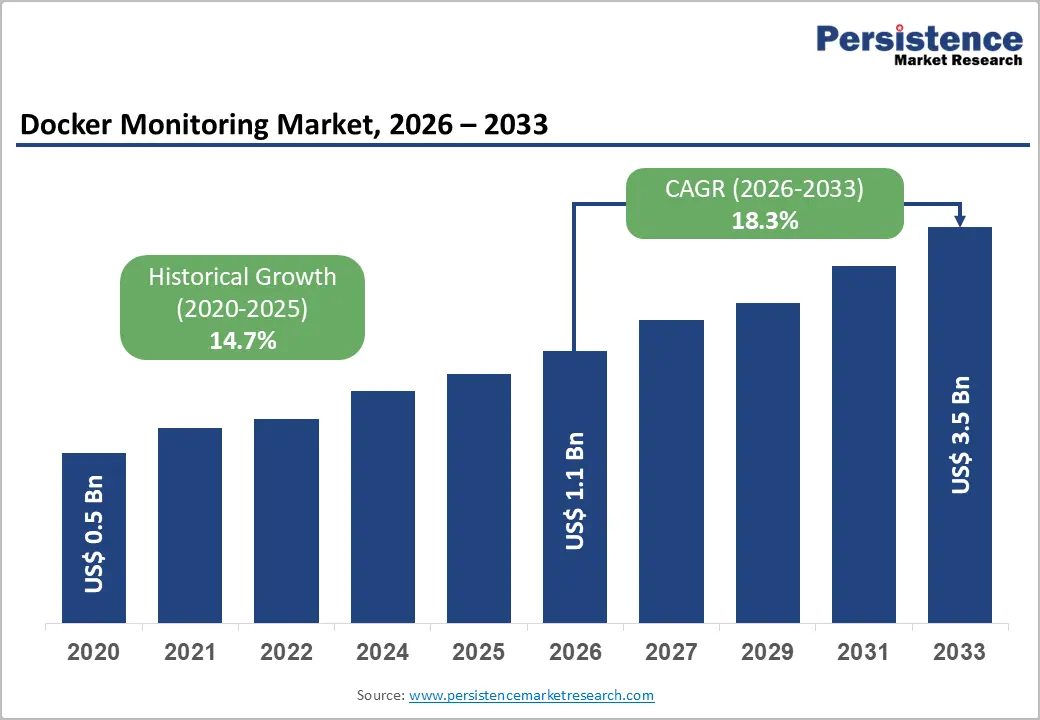

The global Docker monitoring market size is likely to be valued at US$1.1 billion in 2026 and is projected to reach US$3.5 billion by 2033, growing at a CAGR of 18.3% between 2026 and 2033.

This expansion reflects accelerating adoption of containerization, cloud-native application architectures, and enterprise demand for real-time observability across distributed systems. Containerized workloads have become standard in development and production environments, with IT organisations requiring sophisticated monitoring to track performance, security, and compliance across thousands of ephemeral containers deployed across hybrid and multi-cloud infrastructures.

Key Industry Highlights:

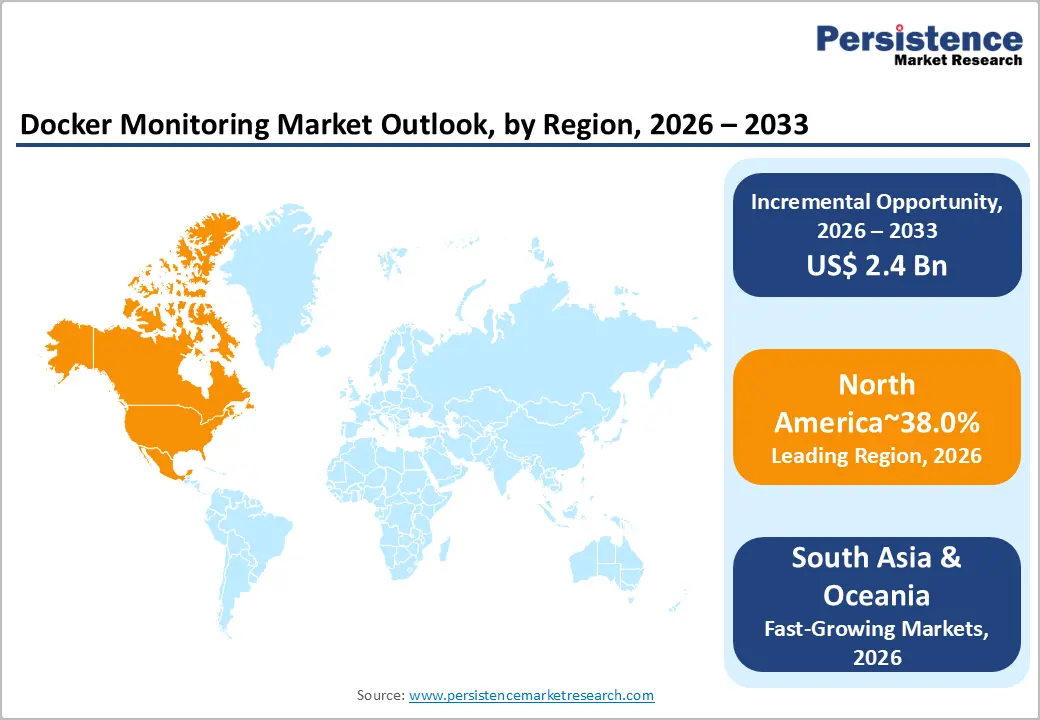

- Leading Region: North America dominates the Docker monitoring market with ~38% share in 2025, driven by advanced DevOps adoption, concentrated cloud infrastructure investment, and regulatory compliance mandates.

- Fastest-Growing Region: East Asia accounts for ~20% of the market share, fueled by massive-scale digital transformation in China and India and large-scale containerised application deployments.

- Leading Component: Solutions lead the market with ~72% share in 2026, reflecting enterprise preference for integrated platforms offering metrics, logs, traces, visualisation, and alerting in unified interfaces.

- Fastest-Growing Component: Services, including consulting, implementation, and managed operations, are expanding rapidly as organizations outsource specialised observability functions to expert vendors.

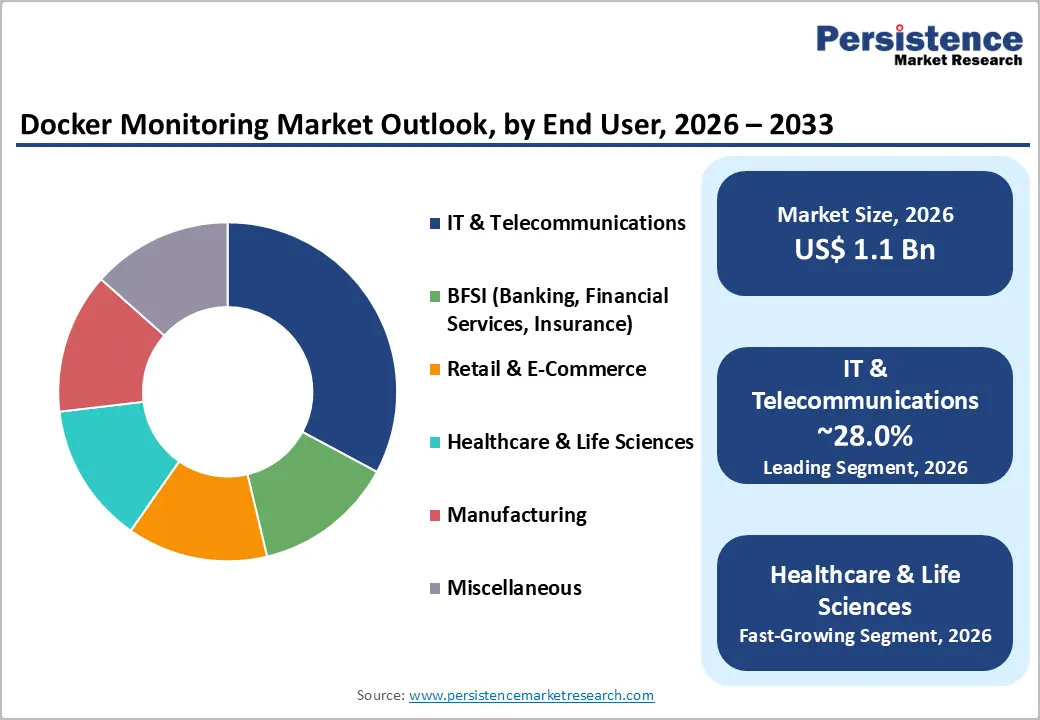

- Key Industry: IT & Telecommunications leads with ~28% share, driven by mission-critical containerised platforms supporting network management, billing systems, and large-scale digital services.

- The Healthcare & Life Sciences industry is the fastest-growing segment, requiring HIPAA-compliant monitoring, anomaly detection, and real-time observability for clinical and patient-facing systems.

| Key Insights | Details |

|---|---|

|

Docker Monitoring Market Size (2026E) |

US$ 1.1 Bn |

|

Market Value Forecast (2033F) |

US$ 3.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

18.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

14.7% |

Market Dynamics

Drivers - Containerization as Foundational Enterprise Infrastructure

Docker container adoption has transitioned from emerging technology to standard enterprise infrastructure, creating structural demand for specialised monitoring solutions. The Docker monitoring market has become essential to managing containerised application complexity on a scale.

Global internet usage reached approximately 6 billion users, which is 74% of the world's population, in 2025, up from 60% in 2020, with nearly 1.3 billion people coming online between 2020 and 2025. This digital expansion corresponds directly with the enterprise shift toward containerised microservices to support massive user bases and data volumes. Container orchestration platforms such as Kubernetes have achieved near-ubiquitous adoption among enterprises modernising infrastructure, with Datadog's analysis of over 2.4 billion containers highlighting consistent growth patterns across container usage, serverless deployments, and GPU-accelerated workloads in 2023.

The proliferation of containerised applications increases operational complexity. Each container generates multiple data streams, such as metrics, logs, traces, and security events, that must be correlated to identify issues. Organisations managing Docker environments face exponential growth in observability data volumes, necessitating automated Docker monitoring solutions capable of ingesting, correlating, and analysing telemetry at petabyte scales without incurring prohibitive costs.

Cloud-Native DevOps Transformation and Continuous Delivery Requirements

Enterprises across industries are increasingly adopting cloud-native architectures and DevOps operating models to improve agility, scalability, and speed of innovation. This structural transformation is redefining how applications are developed, deployed, and managed, placing greater emphasis on real-time visibility and operational resilience.

The Docker Monitoring Market supports the operational model where development teams deploy code changes multiple times daily within containerized environments, requiring real-time feedback on application health, performance, and resource utilisation.

In India's telecommunications sector, the subscriber base reached 1.21 billion, with a tele-density of 86.09% as of June 2025, and internet subscribers reached 979 million, supporting massive-scale digital service deployments. These backend services, increasingly containerised, depend on continuous observability to maintain service levels. Broadcom's July 2025 launch of the Bitnami Secure Images offering, which provides production-ready containerised applications with hardened security and vulnerability transparency, exemplifies the vendor's adaptation to cloud-native requirements.

Organisations implementing CI/CD pipelines require monitoring integration across development, testing, and production stages to detect regressions, performance degradations, and security issues immediately after deployment. Dynatrace's February 2025 launch of Observability for Developers, with runtime insights, advanced analytics, and a Live Debugger, demonstrates the industry shift toward embedding monitoring directly into developer workflows, accelerating shift-left observability practices. This transformation creates sustained demand for Docker-aware monitoring solutions that integrate seamlessly with container orchestration platforms and DevOps toolchains.

Restraint - Complexity and Cost of Observability at Scale

The Docker Monitoring Market faces significant constraints due to the complexity and cost of implementing observability across large, dynamic container environments. Container telemetry volumes typically exceed traditional infrastructure monitoring by 3-5x due to ephemeral container lifecycles, sidecar logging, and detailed trace generation.

Organisations encounter substantial costs for data ingestion, storage, and analysis when deploying comprehensive monitoring across hundreds or thousands of containerised workloads, particularly when utilising consumption-based SaaS pricing models. Skills gaps represent an additional constraint to deploying effective Docker monitoring, which requires expertise spanning container technologies, Kubernetes, distributed systems instrumentation, and observability architecture that many mid-market organisations lack, delaying implementations and reducing perceived ROI on monitoring investments.

Opportunity - AI-Powered Intelligent Observability for Container Environments

Enterprises are increasingly operating large-scale, distributed container environments where manual monitoring and rule-based alerting are no longer sufficient. As containerized workloads grow in scale, complexity, and criticality, there is a strong need for intelligent systems that can interpret vast volumes of telemetry data and convert it into actionable insights in real time.

AI-driven observability platforms can automatically establish behavioural baselines, identify subtle deviations, and correlate signals across distributed systems without manual rule configuration. Dynatrace's March 2024 introduction of Cosign-signed immutable container images for its observability stack demonstrates the vendor's focus on securing container monitoring infrastructure while maintaining auditability. Machine learning models trained on historical container telemetry can predict resource constraints, identify cascading failures, and recommend preventive actions, thereby reducing mean-time-to-resolution and enabling lean operations teams to manage larger deployments. Large language models (LLMs) enable conversational natural language queries against observability data, allowing operators to ask questions like "Why did API latency spike in the production east region?" without constructing complex queries, democratizing observability beyond specialised practitioners. This capability addresses critical pain points in container-native environments where dynamic scaling, service mesh complexity, and multi-cloud deployments create observability challenges that exceed traditional alerting capabilities.

As organizations deploy increasingly sophisticated containerized applications, including real-time bidding platforms, financial transaction processors, and healthcare systems, the ability to rapidly identify and resolve issues becomes directly correlated with revenue and regulatory compliance. The Docker Monitoring Market can capture substantial incremental demand by delivering AI-enabled intelligence that reduces investigation time from hours to minutes and prevents customer-impacting incidents.

Regulatory Compliance and Security Monitoring in Healthcare and BFSI

Healthcare and Life Sciences represent the fastest-growing end-user segment for Docker Monitoring, driven by digital health initiatives, telemedicine deployment, and stringent HIPAA compliance requirements. The Docker Monitoring Market can address unmet needs for continuous audit logging, real-time anomaly detection, and compliance reporting within healthcare IT environments, as they increasingly deploy containerized clinical systems.

China's banking and insurance sectors, with total assets of RMB 467.3 trillion (banking) and RMB 39.2 trillion (insurance) in Q2 2025, demonstrate a scale of financial infrastructure that requires robust monitoring for operational risk, fraud detection, and regulatory compliance. Containerized payment systems, fraud detection platforms, and customer data pipelines in BFSI environments must maintain 99.99%+ uptime while demonstrating compliance with regulatory mandates from central banks and financial regulators.

The Docker Monitoring Market can deliver value through integrated security monitoring, compliance audit trails, and incident response automation, satisfying both operational and regulatory requirements. Healthcare institutions deploying containerised EHR systems, patient portals, and analytics platforms require monitoring that correlates application performance with patient safety outcomes, creating distinctive observability requirements that vendors can address with industry-specific Docker monitoring solutions.

Category-wise Analysis

Component Type Insights

Solutions represent the dominant component segment of the Docker Monitoring Market, commanding approximately 72.0% in 2026, encompassing integrated platforms that provide metrics collection, log aggregation, distributed tracing, visualisation, and alerting capabilities within unified user interfaces. These solutions address enterprise preference for consolidated tooling that reduces operational complexity and vendor management overhead. The solutions' dominance reflects recognition that effective observability requires correlated analysis across multiple signal types. Attempting to manage separate point solutions for metrics, logs, and traces creates blind spots and delays root-cause identification. Docker-aware solutions that automatically discover containers, collect telemetry without instrumentation overhead, and provide Kubernetes-native integration have achieved significant traction among mid-market and enterprise organisations seeking to simplify monitoring architectures.

Services encompassing consulting, professional implementation, training, and managed monitoring operations represent the fastest-advancing component within the Docker Monitoring Market. Many organisations lack internal expertise to design comprehensive observability for containerised environments and therefore engage service providers for architecture design, platform deployment, integration, and 24/7 operational management. Services segment growth reflects a broader organizational trend toward outsourcing specialised functions, enabling focus on core business capabilities while transferring operational complexity to expert vendors.

Industry Insights

IT and Telecommunications is the leading end-user segment, accounting for approximately 28.0% in 2025. Telecom operators and IT service providers manage mission-critical systems, network management platforms, billing systems, content delivery networks, and customer-facing applications increasingly deployed on containers for scalability and operational efficiency.

India's telecom gross revenue increased from US$39.22 billion in FY24 to US$43.42 billion in FY25, with wireless services accounting for over 96% of subscriptions, supported by affordability and 5G expansion. These telecommunications platforms generate massive transaction volumes requiring real-time observability to maintain service levels and detect anomalies. The docker monitoring Market captures substantial IT & Telecommunications spending due to operational criticality of monitoring solutions and the sector's advanced technology adoption patterns.

Healthcare & life sciences emerge as the fastest-growing end-user segment within the Docker monitoring market, driven by digital health transformation, electronic health record modernisation, and emerging regulatory compliance requirements. Healthcare organizations containerize clinical applications, patient portals, and analytics systems to improve scalability and enable rapid deployment of new capabilities while maintaining strict uptime requirements for patient-facing systems. Monitoring solutions tailored to healthcare requirements, enabling HIPAA-compliant audit trails, continuous availability verification, and anomaly detection that correlates with patient safety, address the distinctive needs of the healthcare sector.

Regional Insights and Trends

North America Docker Monitoring Market Trends

North America commands approximately 38% of the global market, anchored by concentrated cloud infrastructure investment, advanced DevOps adoption, and robust enterprise IT spending. The region remains the global centre for container and Kubernetes innovation, with major cloud providers (AWS, Microsoft Azure, Google Cloud) headquartered in North America and driving platform-level observability features. The U.S. Department of Veterans Affairs' February 2024 adoption of Dynatrace container monitoring for VA Platform One exemplifies North American government modernisation initiatives driving monitoring demand. Regulatory environments, including HIPAA, SOX, PCI-DSS, and sector-specific cyber-resilience mandates, compel organizations to deploy comprehensive monitoring, logging, and audit mechanisms for containerised workloads.

Investment trends favour AI-driven observability and security-integrated monitoring, reflecting North American enterprise focus on automated incident response, predictive analytics, and continuous compliance verification. Competitive dynamics feature leading global vendors (Dynatrace, Datadog, New Relic, Splunk) competing alongside cloud-provider-native tools and open-source alternatives, creating a diverse ecosystem supporting North American customer choice and vendor competition.

East Asia Docker Monitoring Market Trends

East Asia represents approximately 20% share in the global market, driven by massive-scale digital transformation in China and India. China reached 1.108 billion internet users by December 2024, with mobile internet users at 1.105 billion (99.7% of netizens), creating an enormous backend application scale requiring containerized microservices and sophisticated monitoring. Digital service platforms serving social networking, instant messaging, online video, and e-commerce for over one billion Chinese users each depend on containerized infrastructure monitored for performance, reliability, and security.

Europe Docker Monitoring Market Trends

Europe represents approximately 22% share, characterized by mature digital infrastructure, stringent regulatory frameworks, and advanced DevOps adoption in Northern European nations. According to Eurostat, 94% of EU individuals used the internet within three months in 2025, with household internet access at 99% in the Netherlands and Luxembourg, indicating a comprehensive digital infrastructure supporting containerization adoption.

The EU information and communication services sector generated approximately €667 billion in value added in 2022, representing 6.6% of total EU business economy value added. Computer programming and consultancy accounted for 59.8% of employment and 51.1% of value added. This substantial ICT sector drives container adoption and the deployment of monitoring platforms across software development firms, system integrators, and digital services companies. European regulatory regimes, including the GDPR, the Digital Services Act, the NIS2 Directive, and upcoming cyber-resilience rules, create compliance requirements that necessitate comprehensive monitoring, threat detection, and audit capabilities for containerized workloads.

Germany, as the largest contributor, accounts for a 22.8% of EU sectoral value added and 22.6% of employment in ICT, followed by France, with the five largest EU economies generating nearly two-thirds of total EU value added in information and communication services. Investment trends in Europe emphasize compliance-centric monitoring, data residency requirements, and vendor-neutral observability solutions enabling multi-cloud and hybrid deployments.

Competitive Landscape

The global docker monitoring market is characterized by a highly competitive and moderately consolidated landscape, dominated by major players such as Datadog, Dynatrace, AppDynamics, Splunk, Broadcom, and New Relic, who together capture a significant share of enterprise deployments. These leaders leverage advanced AI-driven analytics, seamless DevOps integration, and multi-cloud monitoring capabilities to maintain strong differentiation. Beneath this top tier, a diverse set of mid-sized and emerging vendors, including Sysdig, Sumo Logic, Instana, and Prometheus, compete on specialised features, open-source solutions, and cost-effective offerings, keeping the market dynamic.

Continuous innovation, strategic partnerships with cloud providers, and acquisitions shape competitive positioning, while SMEs and cloud-native startups increasingly adopt agile monitoring tools. The market’s structure reflects an oligopolistic dominance at the top combined with a fragmented, innovative base, making it both challenging and lucrative for new entrants and established firms alike.

Key Industry Developments:

- In October 2023, Sysdig & Docker announced a partnership integrating Sysdig runtime insights into Docker Scout, enhancing visibility into running container workloads. The integration enables developers to correlate build-time image analysis with real-time runtime data, reduce monitoring noise, prioritise active risks, and enhance Docker container monitoring and security throughout the cloud-native application lifecycle.

- In June 2024, Oracle enhanced Docker Monitoring capabilities through the OCI Management Agent, enabling native observability of Docker Engine environments. The update allows automated Prometheus-based metric collection from Docker containers across on-premises, OCI, and third-party cloud environments, improving real-time visibility, performance monitoring, and operational control of containerised applications.

Companies Covered in Docker Monitoring Market

- Dynatrace, Inc.

- AppDynamics LLC

- New Relic, Inc.

- Broadcom Inc.

- Microsoft Corporation

- Datadog, Inc.

- Sysdig, Inc.

- Splunk Inc.

- BMC Software, Inc.

- International Business Machines Corporation

- Riverbed Technology, Inc.

- Oracle Corporation

- ScienceLogic, Inc.

- SolarWinds Corporation

- Micro Focus International plc

Frequently Asked Questions

The global docker monitoring market is projected to be valued at US$ 1.1 Bn in 2026.

The industry is expected to account for approximately 28% of the global docker monitoring market by component type in 2026.

The market is expected to witness a CAGR of 18.3% from 2026 to 2033.

Docker Monitoring market growth is driven by widespread enterprise adoption of containerized infrastructure, increasing operational complexity of microservices, cloud-native DevOps transformation, and the need for real-time observability across CI/CD pipelines and large-scale container deployments.

Key market opportunities in the docker monitoring market lie in AI-powered intelligent observability for large-scale container environments and industry-specific solutions addressing regulatory compliance and security monitoring in healthcare and BFSI sectors.

Key players in the docker monitoring market include Dynatrace, Inc., AppDynamics LLC, New Relic, Inc., Datadog, Inc., Splunk Inc., and Microsoft Corporation.