- Electrical Equipment & Services

- Battery Testing Equipment Market

Battery Testing Equipment Market Size, Share, and Growth Forecast, 2026-2033

Battery Testing Equipment Market by Product Type (Stationary, Portable), Function (Cell Testing, Module Testing, Pack Testing), End-User (Automotive, Industrial, Electronics & Telecommunications, Medical, Renewable Energy, Others), and Regional Analysis for 2026-2033

Battery Testing Equipment Market Share and Trends Analysis

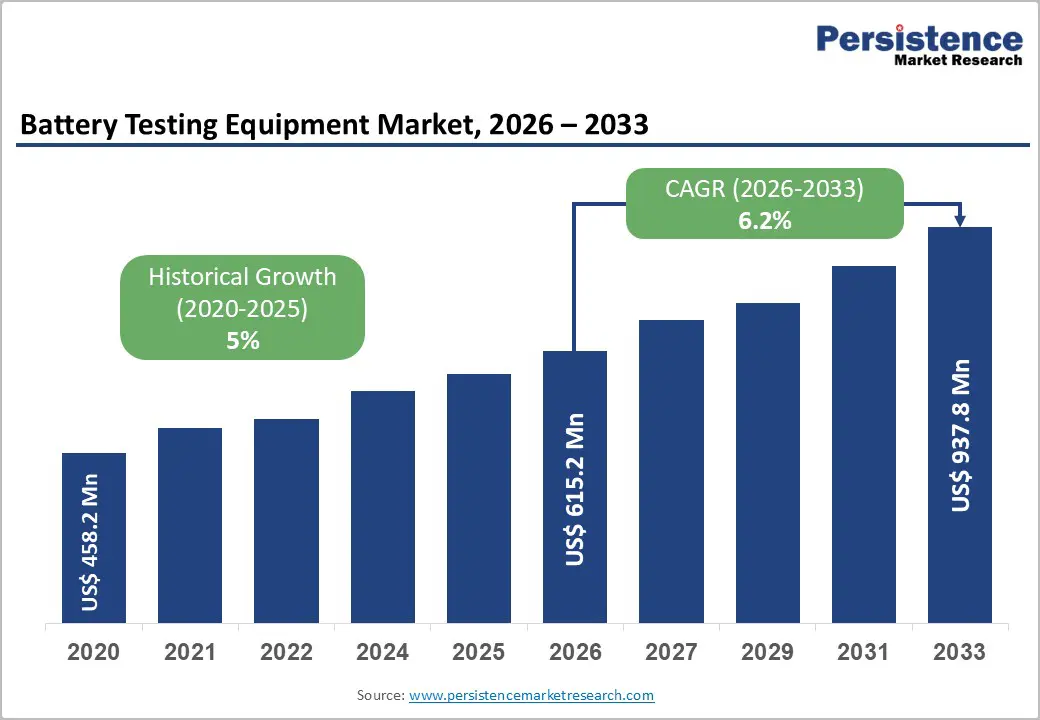

The global battery testing equipment market size is likely to be valued at US$ 615.5 million in 2026 and is projected to reach US$ 937.8 million by 2033, growing at a CAGR of 6.2% during the forecast period 2026-2033.

The growth of the market is being strongly supported by the rapid adoption of electric vehicles, which require rigorous performance, safety, and lifecycle testing to meet regulatory standards and consumer expectations. Simultaneously, the expansion of renewable energy storage systems, including solar, wind, and grid-scale battery installations, is driving demand for high-capacity and reliable stationary testing solutions. Increasingly stringent quality and safety standards, set by organizations such as the International Electrotechnical Commission (IEC) and the International Organization for Standardization (ISO), are compelling manufacturers to adopt advanced testing platforms that ensure compliance and enhance reliability. The rising production of batteries for industrial, consumer electronics, and medical applications, coupled with the global shift toward electrification and sustainability-focused regulations, is projected to significantly elevate the demand for comprehensive battery testing equipment over the forecast period.

Key Industry Highlights

- Dominant Product Types: Stationary equipment is set to command around 60% of the revenue share in 2026, while portable testing solutions are likely to grow the fastest at a 7.1% CAGR through 2033, driven by increasing demand for field diagnostics.

- Leading Function: Cell testing is expected to account for the largest share at 42% in 2026, whereas pack testing is projected to grow the fastest at a 6.8% CAGR during 2026–2033, reflecting large-scale energy storage deployment.

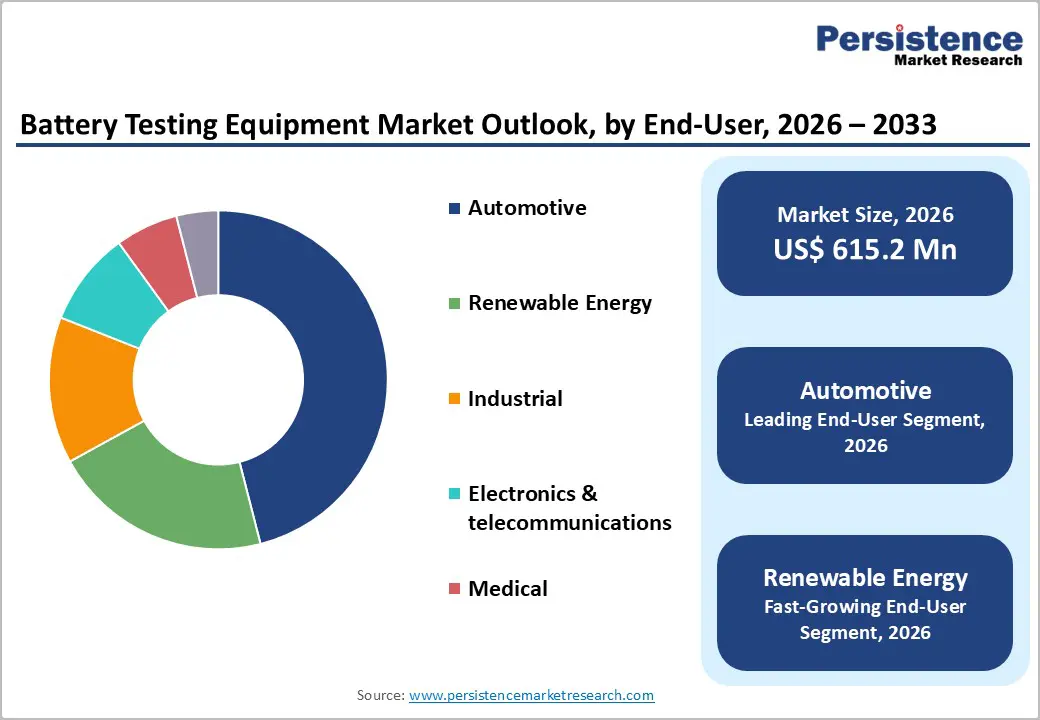

- Dominant End-Users: Automotive is set to lead with an estimated 46% revenue share in 2026, while renewable energy is likely to register the fastest growth at about 6.5% CAGR through 2033, supported by expanding energy storage system (ESS) installations.

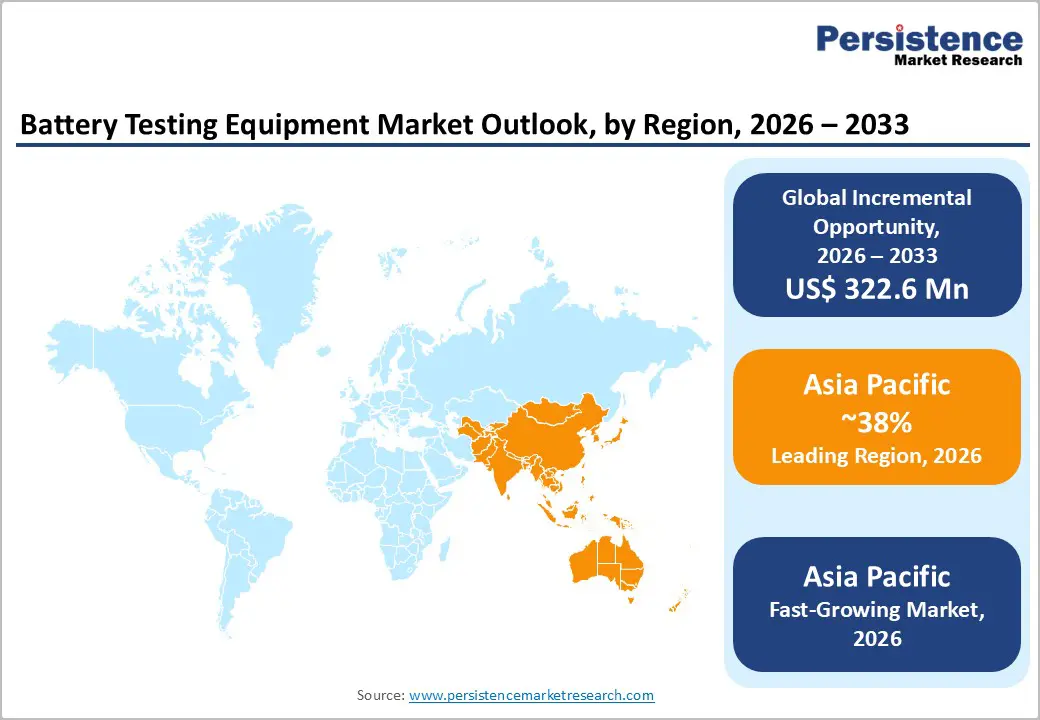

- Regional Leadership: Asia Pacific is anticipated to dominate with an estimated 38% share in 2026 and record around 7.5% CAGR through 2033, led by battery manufacturing and electric vehicle (EV) production hubs of China, Japan, and India.

- Technology Shifts: AI-enabled testing platforms, automation, and next-generation battery chemistry validation are enhancing test efficiency and predictive capabilities, supporting faster adoption across industries.

| Report Attribute | Details |

|---|---|

|

Battery Testing Equipment Market Size (2026E) |

US$ 615.2 Mn |

|

Market Value Forecast (2033F) |

US$ 937.8 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

6.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Accelerated Adoption of Electric Vehicles and Energy Storage Systems

The rapid adoption of EVs continues to fuel demand for battery testing equipment. The government incentives, emission regulations, and consumer preference for low-emission vehicles are prompting manufacturers to enhance battery validation at cell, module, and pack levels. Regulatory frameworks such as ISO 26262 and UNECE Rev. R100 reinforce the need for rigorous testing to ensure performance, durability, and safety across the battery lifecycle. Advanced battery designs, including higher energy-density chemistries, require multi-level testing to ensure operational reliability under diverse conditions.

The expansion of utility-scale energy storage systems is also driving market growth. Europe installed 27.1 GWh of large-scale ESS, a 45% year-on-year increase, while Saudi Arabia deployed nearly 3 GW of battery storage, a market previously non-existent. Asia-Pacific storage capacity is rapidly rising, led by China’s grid-scale deployments. These developments boost demand for high-capacity stationary battery testing solutions, ensuring operational safety and reliability across renewable energy and EV applications. As ESS adoption continues to accelerate, manufacturers are increasingly investing in advanced test infrastructure to support the expanding battery ecosystem.

Rising Quality and Safety Standards across Applications

Increasingly stringent battery safety and performance standards are shaping testing practices worldwide. Regulatory oversight in automotive, industrial, and energy storage sectors demands rigorous evaluation of thermal stability, cycle life, and environmental resilience. Manufacturers are upgrading to automated and high-precision testing platforms to ensure predictive diagnostics and lifecycle compliance. Stricter quality standards across EV and stationary storage applications also promote innovation in testing methodologies, supporting safer and more efficient battery solutions.

A key development supporting this driver is China’s 2026 mandatory EV battery safety standard, which requires batteries to prevent fire and explosion even after thermal runaway, including bottom-impact and high-cycle testing protocols. Such regulatory milestones, combined with widespread industry adoption of EVs and ESS, are creating sustained demand for advanced testing platforms capable of validating safety, performance, and compliance across all battery types and applications. This regulatory momentum is expected to set a global benchmark, prompting other regions to adopt similar safety and quality frameworks, further reinforcing market growth.

High Capital Investment and Technological Complexity

Advanced battery testing equipment requires significant capital expenditure, particularly for high-precision chambers, multi-channel cyclers, and environmental simulation systems. This high upfront cost can be prohibitive for small and medium-sized manufacturers, research labs, and academic institutions, slowing adoption in cost-sensitive markets, even as demand for EV and stationary storage testing continues to rise. Companies must also invest in facility upgrades and integrate specialized infrastructure to operate these systems efficiently, adding further financial pressure.

Beyond purchase price, the total cost of ownership (TCO) includes ongoing maintenance, calibration, software updates, and operator training. The complexity of advanced testing platforms, especially for next-generation chemistries such as solid-state and high-energy lithium-ion, demands skilled personnel, further increasing operational costs. China’s 2026 mandatory EV battery safety standard, requiring batteries to prevent fire and explosion even after thermal runaway, introduces rigorous crash, thermal, and fast-charge cycle tests, expanding testing complexity and increasing investment requirements for compliant equipment.

Lack of Standardization and Supply Chain Challenges

The absence of universally accepted testing standards across battery chemistries and applications complicates procedures and increases operational challenges. Fragmented regulatory requirements force manufacturers to maintain diverse testing protocols tailored to local compliance, slowing scalability and adding administrative burdens. Companies often need to adapt test sequences for different markets, which consumes additional time, resources, and operational bandwidth, limiting efficiency in scaling production and testing.

Battery testing systems rely on specialized components sourced through complex supply chains. U.S. federal tax credit rule changes in 2026, under the “One Big Beautiful Bill Act,” impose stricter sourcing requirements on critical battery materials, potentially slowing energy storage deployment and creating supply pressures. With fragmented protocols, these factors hinder adoption, reduce operational efficiency, and constrain the market’s ability to scale in line with growing EV and ESS demand.

Testing Solutions for Next-Generation Battery Chemistries

Emerging battery technologies such as solid-state, sodium-ion, and hybrid chemistries are creating a strong need for specialized testing systems capable of validating performance under real-world operating conditions. Manufacturers who expand their equipment portfolios to support ultra-fast charging, high energy density, and enhanced cycle life can capture early adoption advantages in a rapidly evolving market. These advanced platforms must also accommodate complex stress and degradation profiles, ensuring batteries meet demanding performance and safety requirements across multiple applications.

Regulatory and industry milestones, such as H55 completing all propulsion battery module certification tests for aviation in 2026, underline the growing emphasis on rigorous validation beyond automotive and stationary storage. This signals broader adoption needs for high-safety, high-precision testing platforms, while also creating opportunities for manufacturers to provide modular and adaptable solutions that can evolve with emerging battery chemistries. Early movers can establish long-term partnerships with original equipment manufacturers (OEMs) and high-safety industry players, positioning themselves as preferred providers of specialized testing solutions.

Portable Testing and AI-Enabled Predictive Platforms

The demand for portable and field-ready battery testing solutions is rising, particularly for on-site diagnostics, state-of-health assessments, and maintenance in energy storage systems and grid applications. These solutions allow operators to monitor battery performance in real time, extend lifecycle, and reduce unplanned downtime, creating new revenue opportunities beyond conventional laboratory testing. Portable systems also enable distributed teams and service networks to perform accurate, rapid testing without relying on central labs, improving operational efficiency and customer satisfaction.

Germany’s 2026 grid-forming BESS procurement demonstrates how large-scale storage is being integrated into energy system planning, highlighting a growing need for advanced testing systems that ensure performance, safety, and operational reliability for utility-scale installations. Combining portability with AI-driven predictive analytics enhances these capabilities, providing actionable insights for maintenance, lifecycle management, and test optimization. This trend positions companies offering intelligent and field-ready testing solutions to capture expanding opportunities across utility, industrial, and renewable energy sectors.

Category-wise Analysis

Function Insights

Cell testing is likely to lead the market with an estimated 42% of the battery testing equipment market revenue share in 2026, driven by early-stage performance evaluation, safety verification, and quality assurance. It is critical for next-generation lithium-ion, solid-state, and hybrid chemistries to detect defects, optimize energy density, and enhance cycle life before module or pack integration. Rigorous protocols include charge/discharge cycles, thermal resilience, and environmental stress testing. Investment in advanced test chambers, multi-channel cyclers, and automated data acquisition is accelerating. UL Solutions opened an advanced battery testing lab in Aachen, highlighting industry focus on high-precision validation. Surging EV production and regulatory standards will sustain strong demand for cell-level testing.

Pack testing is projected to be the fastest-growing function, projected at 6.8% CAGR through 2033, due to the complexity of integrated EV and stationary storage packs. Testing ensures thermal stability, safety, and performance under real-world conditions, managing interconnected cell behavior and high-current dynamics. Rapid EV adoption, large-scale ESS deployment, and stricter safety regulations amplify demand. ANDRITZ Schuler launched a 1.5 GW formation line in 2026 with 50,000+ real-time monitoring channels, illustrating high-throughput pack testing needs. Modular, scalable systems with intelligent BMS integration are now essential. Pack testing growth offers substantial opportunities for advanced testing equipment providers.

End-User Insights

The automotive sector is expected to dominate with an estimated 46% of the battery testing equipment market share in 2026, driven by accelerating EV production and stringent battery reliability standards. Manufacturers invest in high-throughput, precise testing solutions to ensure lifecycle performance, thermal management, and regulatory compliance across cells, modules, and packs. Protocols such as UNECE R100 and ISO 26262 reinforce the need for rigorous validation. In 2026, Germany projected an increase of around 10% in EV production, intensifying demand for advanced automotive battery testing equipment. The complexity of EV packs and continuous innovation in chemistries further strengthen the already dominant role of the automotive sector. This sector remains the primary driver of cell, module, and pack testing equipment demand.

The renewable energy sectors are anticipated to be the fastest-growing end users, projected at a 6.5% CAGR through 2033, fueled by large-scale ESS deployment, electrification of manufacturing, and automated processes. These segments require scalable battery testing solutions for high-capacity packs, long-term performance validation, and operational safety. The EU installed 27.1 GWh of new battery storage, mostly stationary systems, highlighting the growing need for robust testing infrastructure. Portable and software-driven platforms enable real-time diagnostics and predictive maintenance. Rising regulatory standards and ESS expansion accelerate adoption of advanced testing equipment. These sectors present substantial growth opportunities for manufacturers of innovative testing solutions.

Regional Insights

North America Battery Testing Equipment Market Trends

North America is poised to hold a significant share of battery testing equipment demand, driven by strong EV adoption, ESS deployments, and advanced manufacturing clusters across the U.S. and Canada. Expansion of battery validation services, such as the 2025 expansion of SGS’s Suwanee, Georgia lab to support LEV and ESS testing, reflects growing local testing capacity for cell, module, and pack levels, reinforcing confidence in product reliability and regulatory compliance. Manufacturers are integrating high-throughput test platforms with automated monitoring and performance analytics to meet tightening safety and quality benchmarks. Regulatory incentives and production mandates continue to encourage hardware deployment in automotive and grid applications. Technical conferences and battery shows in Michigan are fostering knowledge exchange and technology innovation.

The region’s testing ecosystem continues to evolve, with TÜV SÜD’s Auburn Hills EV battery safety lab marking two years of operation, providing OEMs and suppliers with advanced abuse, vibration, and environmental testing. These labs support validation across diverse battery architectures and performance conditions, enhancing compliance and safety assurance. OEMs are investing in local testing infrastructure to reduce development timelines and align with North American standards. Field-ready testing and diagnostic platforms are gaining traction as ESS and EV service networks expand. Overall, North America is positioning itself as a major market and an innovation hub for advanced battery testing technologies, supporting both current demand and future growth.

Europe Battery Testing Equipment Market Trends

Europe represents a mature and steadily expanding market for battery testing equipment, supported by harmonized regulatory frameworks and decarbonization policies. The inauguration of UL Solutions’ Advanced Battery Testing Laboratory in Aachen, Germany significantly increases regional capacity for rigorous battery evaluation, including safety, lifecycle, and performance testing for EVs and large-scale energy storage systems. This facility strengthens Europe’s ability to support OEMs and ESS developers with certified testing services across all stages of development. In parallel, events such as The Battery Show Europe 2025 in Stuttgart highlight new testing technologies and collaborative efforts among test equipment providers and battery manufacturers, driving knowledge sharing and innovation adoption.

The unprecedented scale of EV and ESS deployments further underscore the need for comprehensive validation platforms. The European government continues to reinforce battery safety and performance mandates, promoting the establishment of advanced testing centers and harmonized cross-border protocols. Shared standards help reduce duplicate testing efforts and enable manufacturers to streamline certification across jurisdictions. Growing renewable energy generation and industrial battery usage are increasing demand for field-ready and software-integrated testing solutions. Public and private investment in certification labs supports deeper adoption of next-generation battery validation platforms across automotive, industrial, and energy segments.

Asia Pacific Battery Testing Equipment Market Trends

Asia Pacific is projected to be the leading and fastest-growing regional market for battery testing equipment, with an estimated 38% share in 2026, driven by China’s dominant battery manufacturing base, rapid EV production, and large ESS deployments. The Battery Show Asia 2026 in Hong Kong highlights regional focus on testing and validation, bringing battery developers, test equipment providers, and integrators together for technology exchange. Demand for high-precision test platforms is rising as manufacturers scale production and certify products for regional and export markets. Government incentives and industrial partnerships strengthen testing infrastructure planning. Regional forums foster collaboration and accelerate adoption of advanced testing solutions across automotive and energy sectors.

Governments and industry bodies actively support localized research and testing initiatives. For instance, India’s Department of Science & Technology co-hosted the Battery Summit 2025, advancing innovation, diagnostics infrastructure, and battery lifecycle evaluation platforms. Japan and South Korea continue to enhance EV and ESS testing through government-industry collaboration, while India emphasizes battery diagnostics and safety. Cost-competitive supply chains and large-scale production attract investment in cell, module, and pack validation systems. Growth in gigafactory capacity and export-oriented production ensures robust, sustained demand. These initiatives position Asia Pacific at the forefront of battery testing technology development.

Competitive Landscape

The global battery testing equipment market structure is moderately consolidated, with leading vendors such as Keysight Technologies, Chroma ATE, AVL, MACCOR, and NI (National Instruments) controlling a significant portion of market revenue. These established players leverage extensive relationships with OEMs, battery manufacturers, and research institutions while investing heavily in R&D to maintain leadership in high-throughput testing, AI-enabled predictive diagnostics, and automated validation systems. Integrated hardware-software platforms and multi-level test capabilities (cell, module, and pack) further strengthen their competitive position.

Regional and niche competitors, including HIOKI, ARBIN Instruments, and PEC, focus on specialized segments such as portable testers, renewable energy storage applications, or laboratory-scale validation. Barriers such as high capital costs, complex multi-level testing requirements, and regulatory compliance challenge new entrants, but software-driven solutions, predictive analytics, and cloud integration enable innovative players to participate. Market consolidation is expected to grow gradually as leading vendors acquire smaller specialists to expand geographically and technologically, while partnerships with software firms continue to enhance testing automation and data management capabilities.

Key Industry Developments

- In January 2026, Polaris Battery Labs independently tested Enovix’s AI1 battery, confirming 12% higher energy density compared to leading competitors. This milestone highlights the importance of impartial testing and benchmark reporting in demonstrating battery performance and supporting adoption of advanced technologies.

- In December 2025, Geely Auto launched a major safety testing facility to support 27 test types, including battery safety and powertrain evaluations. This investment underscores the growing demand for comprehensive validation infrastructure to ensure performance, reliability, and regulatory compliance in EV and hybrid vehicles.

- In December 2025, Seres Automobile partnered with Tsinghua University to establish the Battery Innovation Technology Joint Research Centre, targeting next-generation EV battery research and validation. The center enables advanced testing of emerging chemistries and accelerates innovation in high-performance, safe, and efficient battery systems.

Companies Covered in Battery Testing Equipment Market

- Arbin Instruments

- Chroma ATE

- Keysight Technologies

- Hioki

- Maccor Systems

- Digatron Power Electronics

- NH Research

- Neware Technology

- Enerdis

- Bitrode

- National Instruments

- Vötsch Industrietechnik

Frequently Asked Questions

The global battery testing equipment market is projected to reach US$ 615.5 million in 2026.

Strong adoption of electric vehicles, expansion of renewable energy storage systems, and increasingly stringent battery performance and safety standards are key drivers of market growth.

The market is poised to witness a CAGR of 6.2% from 2026 to 2033.

Emerging opportunities include testing solutions for next-generation battery chemistries, portable and field-ready testing platforms, and AI-enabled predictive diagnostics and software integration.

Keysight Technologies, Chroma ATE, AVL, MACCOR, HIOKI, ARBIN Instruments, PEC are some of the leading market players.