- Smart Packaging

- Barrier Coatings for Packaging Market

Barrier Coatings for Packaging Market Size, Share, and Growth Forecast, 2026 - 2033

Barrier Coatings for Packaging Market by Coating Material (Polyethylene (PE), Polypropylene (PP), Others), Technology (Water-Based Coatings, Solvent-Based, Others), End-use Industry, and Regional Analysis for 2026 - 2033

Barrier Coatings for Packaging Market Size and Trends Analysis

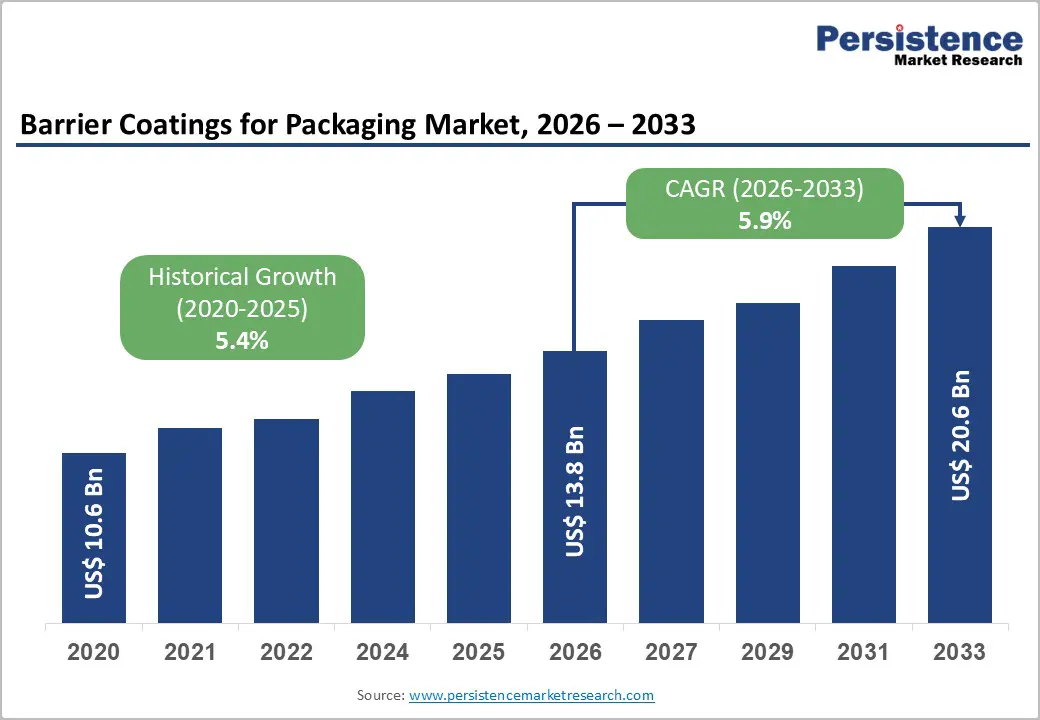

The global barrier coatings for packaging market size is likely to be valued at US$13.8 billion in 2026 and is expected to reach US$20.6 billion by 2033, growing at a CAGR of 5.9% between 2026 and 2033, driven by rising demand for extended shelf life across food & beverage and pharmaceutical applications, accelerated substitution of single-use plastics with coated paperboard and recyclable substrates, and continuous migration toward low-VOC, water-based, and bio-based barrier systems.

Asia Pacific represents the strongest demand center due to manufacturing scale and packaged-food consumption, while regulatory pressure in Europe and circular-economy commitments among global brand owners are intensifying product innovation and supplier consolidation across the value chain.

Key Industry Highlights

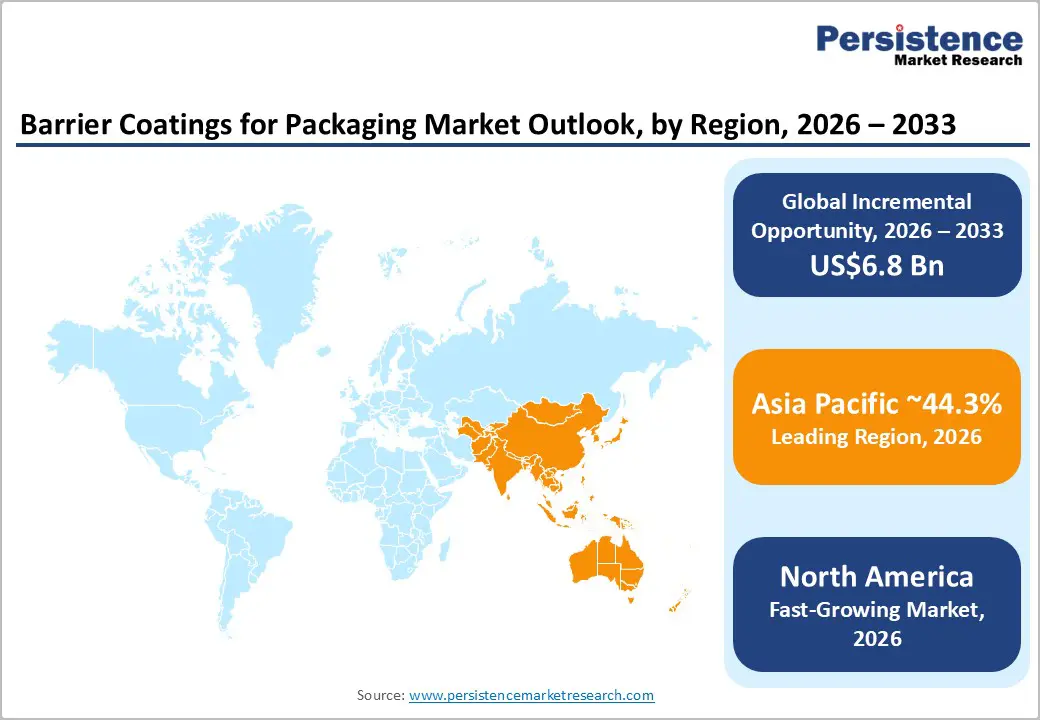

- Leading Region: Asia Pacific leads the market with approximately 44.3% of global market share, supported by large-scale manufacturing capacity, strong packaged-food consumption growth, and cost-competitive production across China, India, and Southeast Asia.

- Fastest-growing Region: North America is the fastest-growing regional market, driven by accelerating adoption of recyclable fiber-based packaging, tightening food-contact and recyclability regulations, and rising demand for pharmaceutical and medical packaging in the U.S.

- Investment Plans: Investment activity is increasingly concentrated in water-based, bio-based, and solvent-free barrier coating technologies, with capacity expansions, R&D programs, and supplier-converter collaborations aimed at replacing plastic laminates while meeting regulatory and brand sustainability requirements.

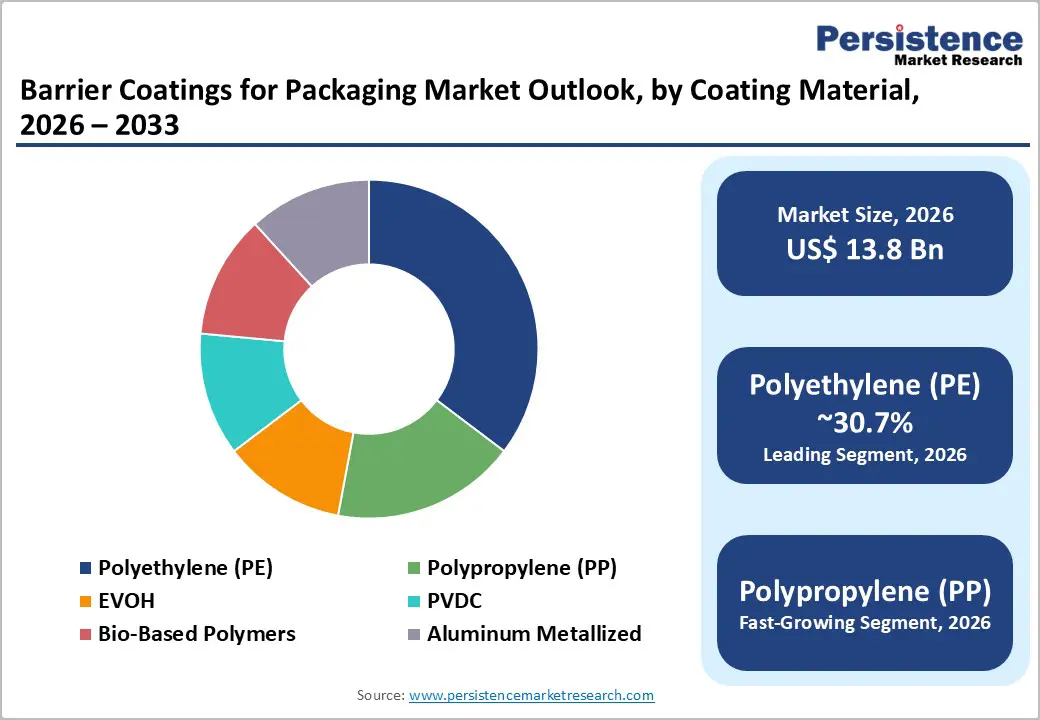

- Dominant Coating Material: Polyethylene (PE) remains the dominant coating material, accounting for over 30.7% of the market share, due to its cost efficiency, ease of processing, and strong moisture-barrier performance in high-volume food and consumer-goods packaging.

- Leading Technology: Water-based coatings lead the technology segment with over 41.2% share, supported by low VOC emissions, regulatory compliance, and strong compatibility with recyclable and fiber-based packaging formats across food, beverage, and personal-care applications.

| Key Insights | Details |

|---|---|

| Barrier Coatings for Packaging Market Size (2026E) | US$13.8 Bn |

| Market Value Forecast (2033F) | US$20.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Sustainability and Regulatory Push for Recyclable and Compostable Packaging

Regulatory frameworks aimed at reducing plastic waste and improving recyclability are fundamentally reshaping the selection of packaging materials. Extended producer responsibility policies and packaging waste regulations across multiple regions are accelerating the replacement of solvent-based extrusion laminates with recyclable paper structures supported by advanced barrier coatings.

Large food, beverage, and personal-care brands have committed to recyclable or reusable packaging targets between 2025 and 2030, creating near-term procurement demand for coatings that preserve shelf life while enabling fiber-based recycling. This transition is already visible in large-scale pilot programs led by paper mills and converters, with water-based and bio-based barrier coatings emerging as commercially viable alternatives that can be applied using existing coating infrastructure.

Growth in Packaged Food Supply Chains and Shelf-Life Requirements in Emerging Markets

Rapid urbanization, rising disposable incomes, and the expansion of refrigerated logistics across the Asia Pacific are increasing per-capita consumption of packaged food. Food & beverage remains the largest end-use segment, accounting for more than 41.2% of total demand, and continues to drive volume consumption of moisture, oxygen, and grease barrier coatings across flexible films and paperboard formats.

High-growth markets such as China, India, and Southeast Asia are investing heavily in flexible packaging capacity, directly increasing demand for polyethylene, polypropylene, EVOH, and PVDC-based barrier layers. In response, converters are prioritizing capacity additions and scalable coating technologies to meet rising throughput requirements while maintaining cost efficiency.

Barrier Analysis - High Cost and Processing Complexity of Advanced Barrier Chemistries

High-performance barrier materials such as EVOH, PVDC, and metallized coatings typically involve higher raw-material costs and require specialized coating, curing, or lamination equipment. Compared with standard polyethylene extrusion, these solutions increase conversion complexity and capital intensity, making adoption challenging for cost-sensitive FMCG applications.

In markets where recycling infrastructure remains underdeveloped, converters are often hesitant to invest in new coating lines without guaranteed visibility into demand. In many applications, switching to advanced barrier solutions can raise per-pack material costs by approximately 5-20%, depending on substrate type, coating thickness, and production scale.

Performance Trade-Offs Between Recyclability and Barrier Efficiency

Some of the highest-performing barrier chemistries, including multi-layer PVDC systems and metallized films, negatively impact recyclability by complicating mono-material recovery streams. As a result, these solutions face increasing scrutiny from brand owners and regulators in regions with strict recycling targets. R&D teams are therefore required to balance oxygen and moisture protection against recyclability or compostability requirements. If alternative recyclable coatings fail to achieve comparable shelf-life performance, brand owners may be forced to accept higher costs or delay transitions away from traditional plastic laminates, slowing overall market conversion.

Opportunity Analysis - Water-Based and Bio-Based Coatings for Fiber-Based Packaging

Water-based and bio-based barrier coatings present a significant opportunity as converters and paper mills retrofit existing coating lines to support recyclable fiber packaging. These coatings allow paperboard to replace plastic laminates in many dry and semi-liquid food applications while maintaining the required barrier properties.

If water-based and bio-based systems capture even 10-15% of the existing polyethylene-coated fiber packaging market by 2030, the incremental revenue opportunity would reach several hundred million U.S. dollars annually. Near-term commercialization is being driven by pilot trials with global brand owners and collaborative scale-ups between coating suppliers and paper producers.

High-Performance Nanocoatings and UV-Curable Systems for Specialty Packaging

Nanocoatings and UV-curable barrier technologies offer ultra-thin, high-performance protection with reduced material usage and fast curing cycles. These characteristics are particularly valuable for pharmaceutical, medical device, and electronics packaging, where sterility, moisture control, and dimensional stability are critical.

Specialty end-use segments typically command more than twice the price per kilogram compared with food packaging coatings. Achieving 5-10% additional penetration in these premium verticals can generate disproportionate revenue growth. Strategic focus on regulatory approvals and co-development with contract packaging providers can accelerate adoption.

Category-wise Analysis

Coating Material Insights

Polyethylene is anticipated to maintain its leading position, accounting for over 30.7% revenue share, driven by its cost-effectiveness, processing simplicity, and reliable moisture-barrier performance across high-volume packaging applications. PE coatings are extensively used in extrusion-coated paperboard, liquid packaging cartons, cupstock, and flexible pouch liners, particularly for dairy products, beverages, dry foods, and frozen items. Their compatibility with high-speed converting lines and the widespread availability of global resins make PE the default choice for mass-market food and consumer-goods packaging. Long-standing operational familiarity among converters, combined with predictable performance under diverse climatic conditions, continues to reinforce PE’s dominance in both rigid and flexible packaging formats despite rising sustainability-driven material innovation.

Polypropylene coatings represent the fastest-growing material segment, supported by rising demand for improved stiffness, heat resistance, and machinability in retortable and high-temperature flexible packaging. Growth is especially pronounced in snack foods, ready meals, and microwaveable packaging, where PP delivers superior thermal stability compared with PE. Brand owners increasingly favor PP-coated structures for applications requiring higher gloss, rigidity, and sealing consistency. Ongoing R&D efforts focus on improving PP adhesion to paper substrates and enabling recyclable mono-material packaging designs. Capacity expansions in Asia, along with evolving petrochemical feedstock economics, are expected to play a decisive role in shaping PP coating availability, pricing trends, and adoption momentum over the forecast period.

Technology Insights

Water-based coatings are anticipated to retain a leading position with over 41.2% revenue share, supported by low VOC emissions, regulatory compliance, and strong alignment with recyclable and fiber-based packaging formats. These coatings commonly use acrylic dispersions, modified PVOH, and tailored polymer emulsions to provide moisture, grease, and limited-oxygen barriers without solvent emissions. Their ability to integrate seamlessly into existing coating and drying equipment makes them particularly attractive for converters transitioning from plastic laminates to coated paper solutions. Widespread adoption is evident in food cartons, paper cups, and personal-care packaging, with brand sustainability commitments and tightening environmental regulations expected to further accelerate demand.

Despite increasing regulatory scrutiny, solvent-based and high-performance systems remain the fastest-growing niche due to their unmatched oxygen, aroma, and grease barrier capabilities. Premium snack foods, processed meat packaging, and certain pharmaceutical and medical applications continue to rely on these systems, where water-based alternatives cannot yet deliver equivalent performance. Metallized films, PVDC-based coatings, and hybrid solvent systems are particularly critical in shelf-life-sensitive applications. Suppliers are responding by developing lower-VOC formulations and hybrid technologies that reduce environmental impact while preserving functional performance, enabling sustained growth in specialized and high-margin packaging segments.

Regional Insights

North America Barrier Coatings for Packaging Market Trends - Regulation-Driven Shift toward Recyclable Fiber-Based Packaging

North America holds a significant share of the global barrier coatings for packaging market, led by the U.S., the main demand hub, driven by its expansive packaged food, beverage, and pharmaceutical industries. Growth is supported by high per-capita consumption of packaged foods, advanced converting infrastructure, and increasing use of coated paperboard and flexible packaging in ready-to-eat and e-commerce formats. Major food and beverage brands such as PepsiCo, General Mills, and Kraft Heinz have publicly committed to reducing non-recyclable plastic content, directly accelerating demand for functional barrier coatings that enable fiber-based packaging without compromising shelf life.

The regional regulatory environment strongly shapes technology adoption. Oversight from the U.S. Food and Drug Administration (FDA) on food-contact materials and rising scrutiny from the Federal Trade Commission (FTC) on recyclability and environmental claims are raising compliance thresholds. This favors suppliers with robust material traceability, migration testing, and lifecycle documentation. Coating producers such as PPG Industries and Dow are expanding water-based and solvent-free barrier portfolios to align with these requirements, while converters increasingly require third-party validation before commercialization.

Investment activity in North America is concentrated in water-based, bio-based, and fluorochemical-free grease-barrier technologies. Companies such as Mondi (via its North American operations) and WestRock are collaborating with coating suppliers to commercialize recyclable paper cups, frozen-food cartons, and quick-service restaurant packaging. In pharmaceuticals, rising demand for blister packs, sachets, and medical device packaging has sustained niche demand for high-performance barrier coatings, including solvent-based and hybrid systems. North America’s innovation-driven ecosystem and regulatory clarity continue to position it as a critical testing ground for next-generation barrier-coating solutions.

Europe Barrier Coatings for Packaging Market Trends - PPWR Compliance Accelerating Mono-Material Paper Barrier Adoption

Europe is characterized by a mature packaging industry and some of the world’s most stringent sustainability and recyclability regulations, making it a global reference market for barrier coating innovation. Germany, the U.K., France, and Spain lead regional demand, supported by advanced converting capabilities, high-quality paperboard production, and strong retailer-driven sustainability mandates. Pan-European retailers and brand owners increasingly require packaging to comply with EU Packaging and Packaging Waste Regulation (PPWR) targets, accelerating the transition toward recyclable and compostable barrier-coated materials.

Regulatory harmonization across the region is driving the adoption of standardized fiber-based barrier solutions. Companies such as Stora Enso and UPM Specialty Papers have expanded dispersion-coated and bio-based barrier paper offerings designed to replace plastic laminates in foodservice and dry-food applications. Similarly, Mondi has invested heavily in functional barrier coatings that allow mono-material paper structures, supporting recyclability within existing European waste streams. These developments are influencing converter investment decisions and shortening time-to-market for compliant solutions.

Circular-economy pilot projects play a critical role in validating new technologies at scale. For example, collaborations between coating suppliers, converters, and brand owners in France and Germany have demonstrated recyclable paper packaging for confectionery and frozen foods, segments historically dependent on plastic barriers. Investment remains selective but strategic, focusing on functional-coating innovation, capacity upgrades, and acquisitions that strengthen sustainability portfolios. Europe’s regulatory rigor and coordinated policy framework continue to make it a leading driver of globally adopted technical standards.

Asia Pacific Barrier Coatings for Packaging Market Trends - Scale-Driven Growth Supported by Cost-Efficient Sustainable Coatings

Asia Pacific is expected to lead the market with approximately 44.3% share in 2026, driven by population scale, rapid urbanization, manufacturing expansion, and rising packaged-food consumption. China represents the largest single market, supported by its extensive flexible packaging and paperboard manufacturing base, while India and Southeast Asia exhibit the fastest growth, fueled by rising middle-class consumption and the penetration of organized retail. Multinational brands such as Nestlé, Unilever, and Mondelez are scaling sustainable packaging initiatives across the region, directly increasing demand for barrier coatings that balance performance with cost efficiency.

The region benefits from cost-competitive manufacturing, access to abundant raw materials, and large-scale capacity additions in extrusion coating, dispersion coating, and flexible packaging. Chinese and ASEAN-based converters are increasingly integrating water-based and hybrid barrier coatings to meet sustainability requirements for export markets, particularly for shipments to Europe and North America. Domestic regulatory frameworks, while uneven, are also tightening around food safety and material compliance, especially in China and Japan.

Brand-led sustainability commitments are a major driver of adoption. For example, ITC Limited in India has expanded coated paperboard packaging for food and personal-care brands, leveraging water-based barrier technologies to improve recyclability. In Southeast Asia, joint ventures between local converters and global coating suppliers are accelerating technology transfer and localization of advanced barrier formulations, reducing reliance on imports. Asia Pacific’s combination of scale, manufacturing agility, and rising sustainability expectations also positions it as the most influential growth engine shaping global demand and cost dynamics for barrier coatings.

Competitive Landscape

The global barrier coatings for packaging market is moderately concentrated among large chemical groups and specialized coating suppliers, supported by a broad base of regional and niche formulators. Leading players dominate high-value specialty coatings, while smaller firms address application-specific niches. Competitive advantage is driven by regulatory compliance capabilities, global supply reliability, and co-development partnerships with converters and brand owners.

Recent strategic activity includes partnerships to commercialize fully bio-based barrier coatings in the Asia Pacific, development of certified compostable coated papers, process innovations enabling barrier coatings on flexible paper at an industrial scale, and acquisitions aimed at expanding functional-coating and circular-economy capabilities.

Key strategies include accelerated innovation in recyclable and low-VOC coatings, vertical collaboration with paper mills and converters, selective acquisitions to secure functional-coating intellectual property, and targeted capacity expansion in high-growth Asia Pacific markets.

Key Industry Developments

- In June 2025, PPG Industries introduced an advanced UV-curable barrier coating specifically for pharmaceutical packaging, providing enhanced moisture and oxygen protection while meeting global regulatory standards.

- In March 2025, Lecta unveiled Linerset FP, a high-performance barrier base paper tailored for flexible packaging applications, enhancing performance for bags, pouches, and wraps in food and industrial markets.

Companies Covered in Barrier Coatings for Packaging Market

- Dow Inc.

- BASF SE

- Henkel AG & Co. KGaA

- Arkema

- Kuraray Co., Ltd.

- Solenis LLC

- Siegwerk Druckfarben AG

- Michelman, Inc.

- H.B. Fuller Company

- Avery Dennison Corporation

- Solvay S.A.

- Evonik Industries AG

- Clariant AG

- Wacker Chemie AG

- Eastman Chemical Company

- PPG Industries, Inc.

- Sika AG

- Omnova Solutions

Frequently Asked Questions

The global barrier coatings for packaging market is estimated to be valued at US$13.8 billion in 2026.

By 2033, the barrier coatings for packaging market is expected to reach US$20.6 billion, supported by rising adoption of recyclable and high-performance barrier solutions.

Key trends include the rapid shift toward water-based and bio-based coatings, substitution of plastic laminates with coated paper and recyclable substrates, increasing demand for extended shelf life in food and pharmaceutical packaging, and growing supplier, converter collaborations to meet regulatory and brand sustainability targets.

Polyethylene (PE) is the leading coating material segment, accounting for over 30.7% share, driven by its cost efficiency, strong moisture-barrier properties, and widespread use in food and consumer-goods packaging.

The barrier coatings for packaging market is projected to grow at a CAGR of 5.9% between 2026 and 2033.

Major players include Dow Inc., BASF SE, Henkel AG & Co. KGaA, Kuraray Co., Ltd., and Solenis LLC.