- Medical Devices

- Surgical Hemostat, Internal Tissue Sealants and Adhesion Barrier Market

Surgical Hemostat, Internal Tissue Sealants and Adhesion Barrier Market Size, Share, and Growth Forecast, 2025 - 2032

Surgical Hemostat, Internal Tissue Sealants and Adhesion Barrier Market by Product Type (Hemostats, Internal Tissue Sealants, and Adhesion Barriers), Application, End-User, and Regional Analysis for 2025 - 2032

Surgical Hemostat, Internal Tissue Sealants and Adhesion Barrier Market Share and Trends Analysis

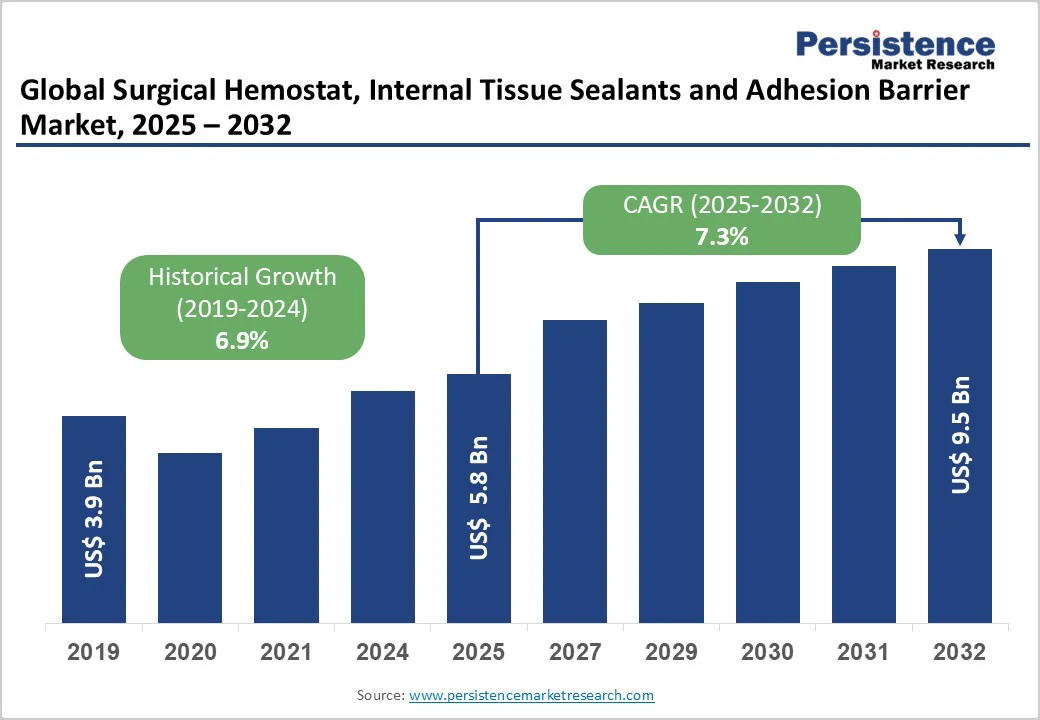

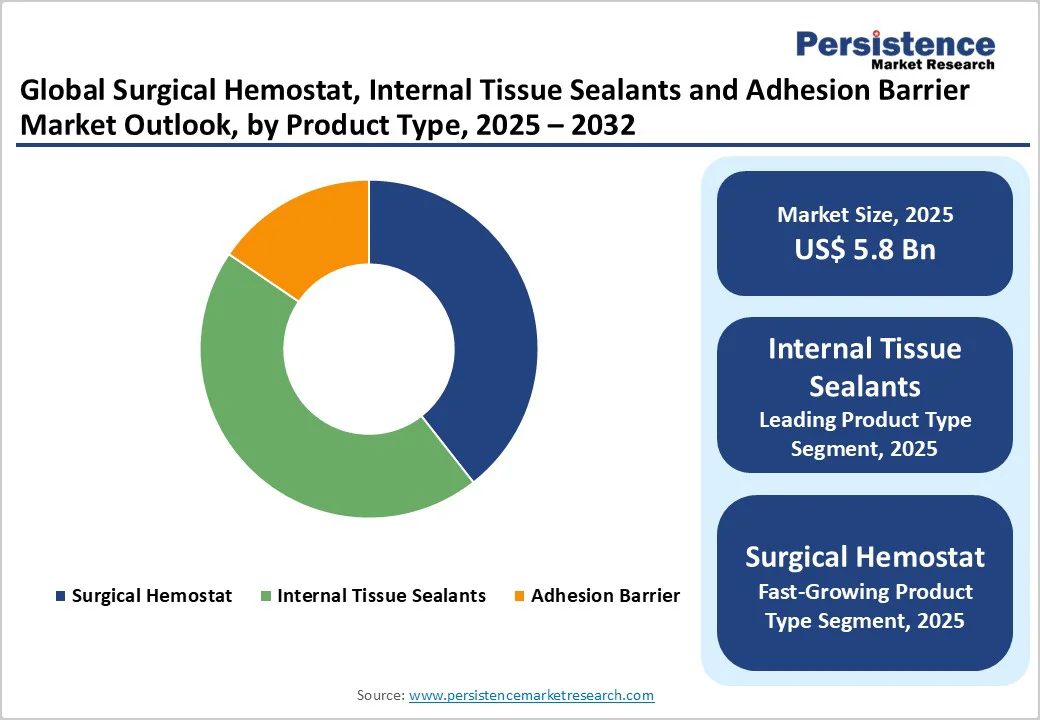

The global surgical hemostat, internal tissue sealants and adhesion barrier market size is likely to be valued at US$ 5.8 billion in 2025, and is projected to reach US$ 9.5 billion by 2032, growing at a CAGR of 7.3% during the forecast period 2025-2032. Increasing geriatric population across the globe, coupled with a soaring demand for cardiovascular, orthopedic, digestive, and other surgical procedures, is expected to fuel the consumption of surgical hemostats, internal tissue sealants and adhesion barriers market. Ageing population, strong healthcare infrastructure, and well-established reimbursements are driving market growth.

Key Industry Highlights:

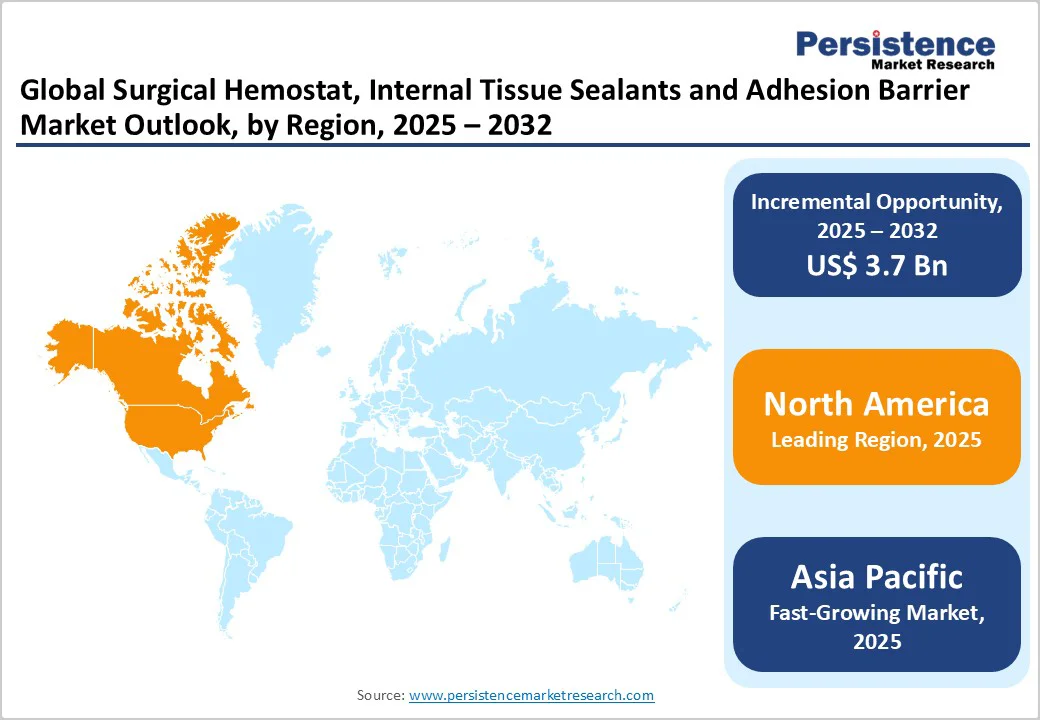

- Leading Region: North America, supported by advanced healthcare infrastructure, high surgical volumes, well-established medical device companies, and strong adoption of innovative surgical technologies.

- Fastest-growing Regional Market: Asia Pacific, driven by rising healthcare spending, growing awareness of minimally invasive surgeries, expansion of hospital infrastructure, and increasing government support for medical device manufacturing.

- Dominant End-User: Hospitals, to the high number of complex surgical procedures, availability of skilled professionals, and greater utilization of advanced hemostatic and sealing products.

- Fastest-growing End-User: Ambulatory Surgical Centers (ASCs) are witnessing the highest growth, fueled by the shift toward outpatient procedures, lower treatment costs, and faster patient recovery times.

- Investment Plans: Major players focus on product innovation, strategic partnerships, and regional expansions to enhance their surgical portfolios and strengthen market presence globally.

|

Key Insights |

Details |

|

Surgical Hemostat, Internal Tissue Sealants and Adhesion Barrier Market Size (2025E) |

US$ 5.8 Bn |

|

Market Value Forecast (2032F) |

US$ 9.5 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Escalating Surgical Procedure Volumes and Aging Demographics

The escalating volume of surgical procedures globally, driven by an aging population and rising prevalence of chronic diseases, represents a primary growth driver for the surgical hemostat, internal tissue sealants and adhesion barrier market. The World Health Organization (WHO) reports that chronic diseases including cardiovascular diseases, cancer, respiratory conditions, and diabetes account for 71% of all global deaths, with 17.9 million, 9.3 million, 4.1 million, and 1.5 million deaths, respectively, creating a substantial urgency for surgical interventions. Research published in the Journal of the American Medical Association indicates that approximately 70% of cardiothoracic surgeries involve patients aged 65 years or older, demonstrating the impact of aging demographics on surgical volumes.

Additionally, trauma cases requiring emergency surgical intervention affect approximately 4.4 million lives annually according to the WHO, with hemostatic products playing critical roles in controlling massive hemorrhage and improving patient survival outcomes. The convergence of aging populations, chronic disease prevalence, and trauma incidence creates sustained demand for advanced hemostatic solutions across diverse surgical specialties and clinical settings globally.

Stringent Regulatory Requirements and Extended Development Timelines

The surgical hemostat, tissue sealants, and adhesion barrier market encounters substantial challenges from rigorous regulatory frameworks requiring extensive clinical trials, comprehensive safety demonstrations, and thorough efficacy validations before market authorization. For example, the U.S. Food and Drug Administration (FDA) mandates comprehensive preclinical and clinical data demonstrating product safety, biocompatibility, sterility, and performance across diverse surgical applications before authorization.

These requirements extend product development timelines by 5-7 years, substantially increase research and development costs, and create significant market entry barriers particularly for smaller companies lacking extensive regulatory expertise and financial resources. Post-market surveillance requirements and potential product recall due to safety concerns create ongoing compliance obligations, potentially limiting innovation speed and reducing manufacturer willingness to invest in novel hemostatic technologies.

Development of Dual-Function Combination Products

The development of combination products delivering multiple functions simultaneously represents significant growth opportunity, addressing evolving surgical needs while improving operational efficiency. Innovative combination products serving as hemostats, tissue sealants, and adhesion barriers simultaneously reduce the number of products required during surgical procedures, simplifying surgical workflows and reducing operative time. Baxter's Seprafilm Adhesion Barrier, for instance, composed of sodium hyaluronate and carboxymethylcellulose prevents post-surgical adhesions while functioning as a tissue barrier, representing dual-function innovation.

Research indicates that post-surgical adhesions affect 60-90% of abdominal surgery patients, causing chronic pain, bowel obstruction, and infertility in some cases, with treatment costs exceeding US$ 1 billion annually in the U.S. alone. Manufacturers developing advanced combination products addressing multiple surgical needs simultaneously create compelling value propositions, improving clinical outcomes while reducing total procedure costs. This product development strategy positions manufacturers favorably for market share gains while addressing diverse surgeon preferences and patient safety objectives across multiple surgical specialties.

Category-wise Analysis

Product Type Insights

The internal tissue sealants segment is likely to dominate with approximately 45% of the surgical hemostats, internal tissue sealants, and adhesion barriers market revenue share in 2025, driven by extensive applications across cardiovascular surgery requiring anastomotic sealing, neurological procedures demanding dura mater sealing, orthopedic interventions involving bone surface sealing, and general surgical applications requiring tissue repair and bleeding control. Fibrin-based sealants, including Baxter's TISSEEL Fibrin Sealant, composed of human fibrinogen and thrombin, provide proven clinical safety and efficacy over decades of use, helping surgeons address bleeding at surgical sites inaccessible to conventional hemostatic methods, including sutures and cautery.

These products demonstrate effectiveness across diverse surgical specialties, controlling bleeding in heparinized patients, managing effects of antiplatelet medications, and achieving hemostasis on friable or difficult tissues. Advanced tissue sealants combining mechanical properties with biological activity deliver faster hemostasis, particularly in difficult bleeding situations where conventional methods prove inadequate. Continuous innovation, including sprayable formulations, improved laparoscopic application systems, and dual-function products serving as sealants and adhesion barriers simultaneously, reinforce this segment's market leadership position globally.

End-user Insights

The hospitals segment is set to dominate the surgical hemostat market with approximately 65% market share, attributed to high surgical procedure volumes performed in hospital settings, availability of comprehensive surgical infrastructure, including specialized operating rooms and advanced medical equipment, and presence of multidisciplinary surgical teams capable of performing complex procedures. Hospitals maintain strong procurement capabilities enabling access to premium surgical products, comprehensive formulary management systems, and established relationships with leading medical device manufacturers ensuring consistent product supply.

Hospitals also benefit from insurance reimbursement frameworks covering advanced hemostatic and sealing products for approved procedures, reducing financial barriers to adoption of premium technologies. These facilities accommodate diverse surgical specialties including cardiovascular, neurological, orthopedic, urological, and general surgeries, each requiring specialized hemostatic solutions tailored to specific tissue types and bleeding challenges. Hospitals' investment in surgical excellence programs, quality improvement initiatives focusing on complication reduction, and adoption of evidence-based surgical protocols incorporating advanced hemostatic products reinforce this segment's market leadership position.

Regional Insights

North America Surgical Hemostat, Internal Tissue Sealants, and Adhesion Barrier Market Trends

North America, particularly the U.S., leads the global surgical hemostat market, backed by an advanced healthcare infrastructure, high surgical procedure volumes, and a sophisticated regulatory framework through the FDA, ensuring product safety and efficacy. The region accounts for approximately 45% of the global market share, supported by widespread chronic disease prevalence, including cardiovascular disorders, obesity, arthritis, and cancer, requiring surgical interventions. Major medical device companies, including Baxter International Inc., Ethicon Inc. (a Johnson & Johnson MedTech company), and Integra Lifesciences Corporation, are headquartered in the region, fostering a robust innovation ecosystem.

The U.S. market benefits from a strong research and development infrastructure with companies investing substantially in next-generation hemostatic technologies. For example, Baxter recently launched Hemopatch Sealing Hemostat with room temperature storage capability in April 2025, eliminating refrigeration requirements and enhancing operating room accessibility. The region's sophisticated reimbursement systems, stringent clinical evidence requirements driving product quality, and widespread adoption of minimally invasive surgical techniques support continued market growth and technological advancement across all surgical specialties.

Asia Pacific Surgical Hemostat, Internal Tissue Sealants and Adhesion Barrier Market Trends

Asia Pacific is poised to emerge as the fastest-growing surgical hemostat market, experiencing sustained expansion driven by rapid healthcare infrastructure modernization, increasing surgical volumes, rising chronic disease prevalence, and expanding medical tourism attracting international patients. China, Japan, and India lead regional growth, supported by large populations, increasing healthcare expenditure, and government initiatives promoting healthcare access and quality improvement. Japan, in particular, demonstrates sophisticated adoption of advanced surgical technologies including robotic surgery systems and minimally invasive techniques requiring specialized hemostatic products. The country's aging population with substantial elderly demographics requiring orthopedic, cardiovascular, and cancer-related surgeries drives consistent demand.

India presents exceptional growth potential with expanding private hospital networks, medical education infrastructure producing skilled surgeons, and increasing insurance penetration enabling patient access to quality surgical care. Besides this, manufacturing advantages include cost-effective production capabilities, skilled workforce availability, and improved regulatory frameworks following international standards support regional market development. Healthcare investments in emerging ASEAN nations can also create opportunities for market participants establishing regional operations and providing technical training supporting surgeon education.

Competitive Landscape

The global surgical hemostat, internal tissue sealants, and adhesion barrier market structure exhibits moderate consolidation with major multinational medical device companies, including Baxter, Ethicon Inc., B. Braun Melsungen AG, Integra Lifesciences Corporation, and Pfizer Inc. dominating market shares through extensive product portfolios, established distribution networks, and continuous innovation capabilities. Market leaders compete through product differentiation, focusing on faster hemostatic action, improved biocompatibility, enhanced ease of use, particularly in minimally invasive procedures, and comprehensive surgical specialty coverage.

Key differentiators include regulatory compliance expertise, clinical evidence generation through rigorous trials, technical support services educating surgical teams, and strategic partnerships with hospitals and ambulatory surgical centers. Emerging trends include the development of combination products delivering multiple functions, expansion into emerging markets through tailored product offerings, and focus on sustainability through biodegradable formulations.

Key Industry Developments:

- In October 2025, Japan’s Olympus Corporation launched the ENDOEYE 3D HD vision system alongside a new surgical energy device designed for hemostatic cutting and vessel sealing. The ENDOEYE 3D system offers surgeons enhanced visualization with high-definition, three-dimensional imaging aimed at improving minimally invasive procedures. The accompanying device employs advanced bipolar energy for precise cutting and effective vessel sealing, reducing surgical times and blood loss.

- In September 2025, Baxter introduced the HEMOPATCH sealing hemostat in New Zealand, a surgical patch designed to control bleeding and support tissue sealing during surgeries. This product facilitates rapid hemostasis, reducing operative time and improving patient outcomes. The HEMOPATCH is easy to apply and is suitable for use in cardiovascular, general, and thoracic surgeries. Its launch supports Baxter’s commitment to expanding innovative surgical solutions globally, enhancing procedural efficiency and safety.

- In September 2025, The U.S. FDA approved Womed Leaf®, the first medical device for treating moderate to severe intrauterine adhesions (Asherman syndrome), a major cause of female infertility. This resorbable adhesion barrier, inserted after hysteroscopic surgery, prevents uterine walls from bonding during healing, significantly reducing adhesion severity and recurrence. The device is drug-free, made from a proprietary polymer, and its approval marks a major advancement in treating Asherman syndrome, offering hope for improved fertility outcomes.

Companies Covered in Surgical Hemostat, Internal Tissue Sealants and Adhesion Barrier Market

- Baxter

- Ethicon, Inc.

- B. Braun Melsungen AG

- Sanofi

- C. R. Bard, Inc.

- Integra Lifesciences Corporation

- Cryolife Inc.

- Tissuemed Ltd

- Cohera Medical, Inc.

- Pfizer Inc.

Frequently Asked Questions

The global surgical hemostat, internal tissue sealants and adhesion barrier market is projected to reach at US$ 5.8 billion in 2025.

Rising number of surgical procedures worldwide, technological innovations, aging population, strong demand for minimally invasive surgeries, and emphasis on patient safety are driving the market.

The market is poised to witness a CAGR of 7.3% between 2025 and 2032.

Healthcare infrastructure growth in emerging economies, development of bio-based surgical products, advanced sealant innovations, regenerative medicine integration, and expanding applications across diverse surgical fields are key market opportunities.

Baxter, Ethicon, Inc., B. Braun Melsungen AG, and Sanofi are some of the major players operating in the market.