- Inks, Coatings, Adhesives & Sealants (ICAS)

- Barrier Coated Paper Market

Barrier Coated Paper Market Size, Share, and Growth Forecast, 2025 - 2032

Barrier Coated Paper Market by Product Type (Water-Based Coatings, Wax Coatings, Dispersion Coatings, Others), Paper Weight (Lightweight (<60 GSM), Mid-weight (60-150 GSM), Heavyboard (>150 GSM)), Barrier Property (Grease Resistance, Moisture Resistance, Oil Resistance, Vapor Barrier), Application, and Regional Analysis for 2025 - 2032

Barrier Coated Paper Market Size and Trends Analysis

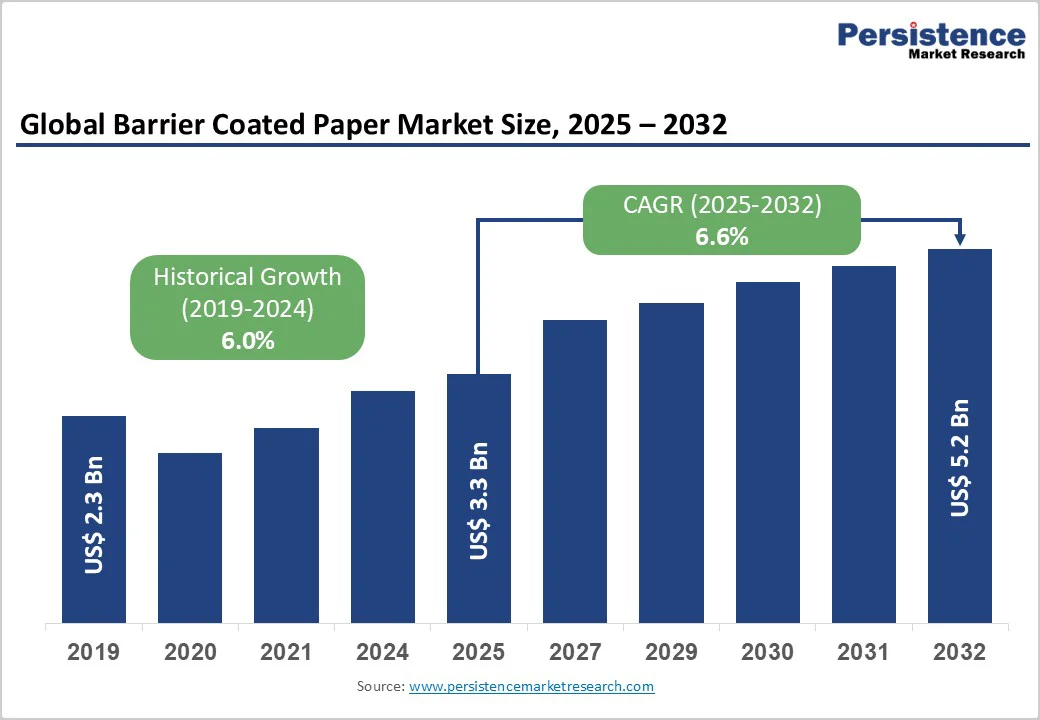

The global barrier coated paper market size is likely to value at US$ 3.3 billion in 2025 and is projected to reach US$ 5.2 billion, growing at a CAGR of 6.6% between 2025 and 2032.

This expansion reflects sustained demand for sustainable, high-performance packaging solutions driven by stringent environmental regulations, accelerating e-commerce growth, and shifting consumer preferences toward plastic alternatives.

Key Industry Highlights:

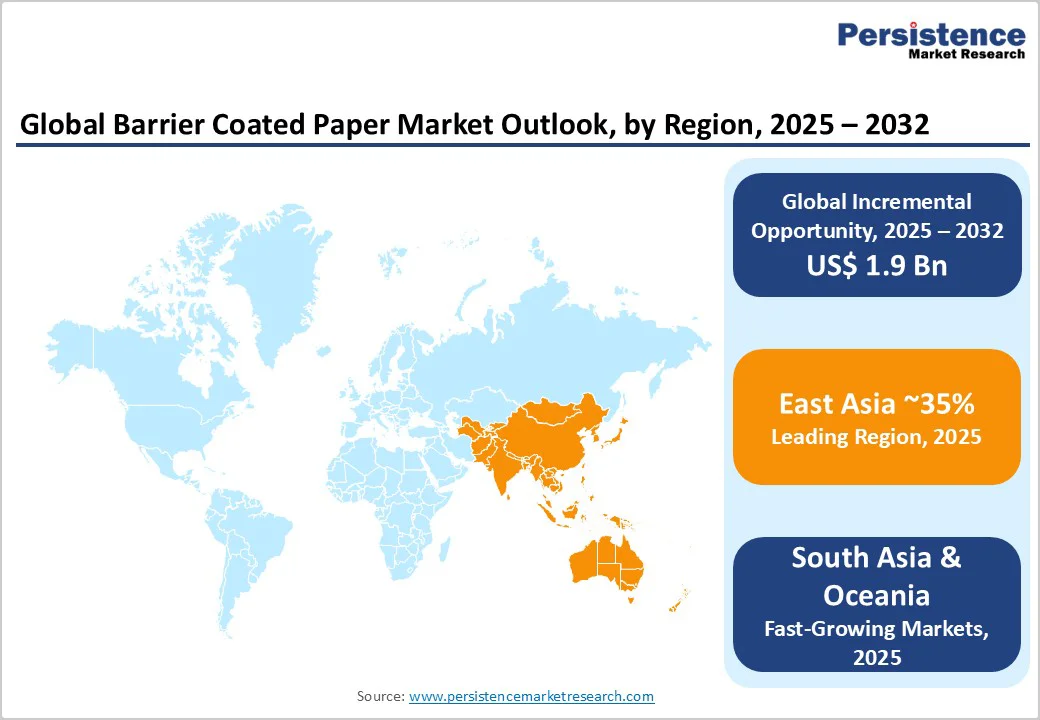

- East Asia leads the global market with an estimated 35% share in 2025, driven by large-scale manufacturing capacity in China and strong domestic demand from food, beverage, and consumer goods sectors.

- Europe ranks as the second-largest regional market (≈26%), supported by stringent EU packaging regulations (PPWR) and advanced recycling infrastructure promoting PFAS-free and compostable barrier coatings.

- Food & Beverage Packaging dominates by holding ~56% market share, supported by regulatory compliance requirements and the need for moisture, grease, and aroma barriers to ensure extended shelf life.

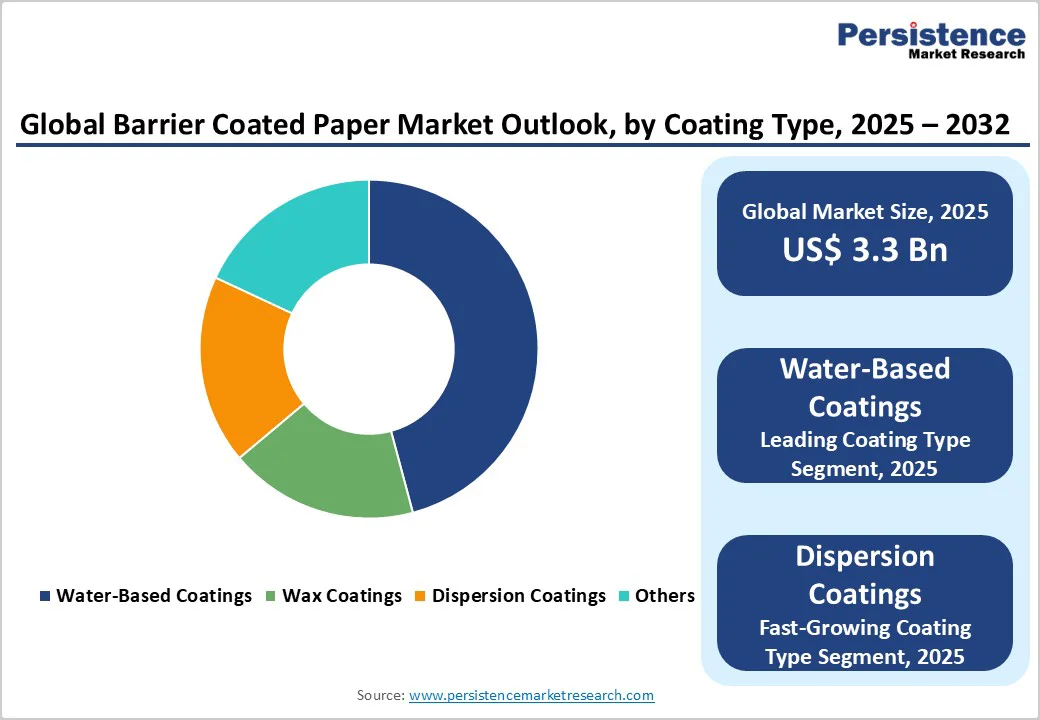

- Water-Based Coatings remain the leading coating category (~38% share) due to regulatory alignment with VOC-free, fluorine-free sustainability standards and broad application versatility.

- Mid-weight Papers (60-150 GSM) command the largest volume share (~49.5%), offering a balance of functionality and cost efficiency across diverse packaging uses.

| Key Insights | Details |

|---|---|

| Barrier Coated Paper Market Size (2025E) | US$ 3.3 Bn |

| Market Value Forecast (2032F) | US$ 5.2 Bn |

| Projected Growth (CAGR 2025 to 2032) | 6.6% |

| Historical Market Growth (CAGR 2019 to 2024) | 6.0% |

Market Dynamics

Driver - Regulatory Mandates Accelerating Plastic Phase-Out and Sustainable Packaging Adoption

The barrier coated paper market is experiencing substantial momentum from increasingly stringent global regulatory frameworks restricting single-use plastics and mandating sustainable packaging alternatives. The European Union's Packaging and Packaging Waste Regulation (PPWR), effective from August 2026, establishes comprehensive PFAS (per- and polyfluoroalkyl substances) restrictions limiting individual PFAS to 25 parts per billion and total PFAS to 250 parts per billion, driving an accelerated transition toward barrier-coated paper solutions.

The United States is witnessing state-level regulatory proliferation, with jurisdictions including New York, California, and New Mexico implementing PFAS bans on food-contact materials and consumer products. These regulatory interventions create substantial structural demand for fluorine-free barrier solutions within the Barrier Coated Paper Market, as manufacturers must re-engineer packaging specifications to maintain compliance. Industry data demonstrates that approximately 30-35% of packaging conversions globally are now explicitly driven by regulatory compliance requirements rather than market differentiation.

The confluence of EU regulatory action and North American state-level initiatives establishes a compliance imperative that systematically favours barrier-coated paper over traditional fluorochemical-treated plastics, fundamentally reshaping supply chain sourcing decisions across pharmaceutical, food service, and consumer goods manufacturers.

Quantifiable Food Waste Reduction and Extended Shelf-Life Capabilities

Scientific evidence increasingly validates the economic and environmental value proposition of barrier-coated paper in reducing post-consumer food waste. University of Georgia research demonstrates that shelf-life extension through advanced packaging can reduce consumer-level food waste by up to 40%, with specific applications documenting shelf-life extensions ranging from 50% to 300% depending on product category, bell peppers extending from 4 to 20 days, cherries from 14 to 28 days, and green beans from 7 to 19 days.

The global barrier coated paper market benefits substantially from corporate sustainability commitments and government initiatives targeting approximately 1 billion meals discarded daily worldwide.

The Food and Agriculture Organisation estimates that packaging innovation capable of extending product shelf life delivers measurable environmental benefits, including reduced resource consumption, lower transportation emissions, and diminished agricultural inputs. Within the food and beverage sector, which represents approximately 56% of market share in 2025, barrier-coated paper enables manufacturers to achieve compliance with extended distribution requirements while reducing spoilage losses.

For developing markets, where climatic conditions accelerate food degradation, barrier-coated paper solutions create tangible economic opportunities by reducing daily food preparation requirements and lowering waste-related expenses.

This quantifiable value proposition demonstrating 15% cost reduction in product losses validates capital investment in barrier-coated paper infrastructure among large-scale food processors, driving consistent demand expansion within the Barrier Coated Paper Market.

Restraints - Infrastructure Gaps in Recycling Systems and End-of-Life Processing

Barrier-coated papers require specialized decoating and separation processes to integrate into conventional pulp recycling streams, and many regional recycling facilities lack certified methodology or equipment to process these materials efficiently.

North America possesses developed systems achieving 60-75% recycling rates, while large emerging markets, including India and Southeast Asia, operate below 30% effective recovery rates. Regulatory uncertainty regarding composability claims and material classification standards creates compliance ambiguity for manufacturers, particularly regarding European composting certification requirements.

Until recycling infrastructure reaches systematic deployment across consumer markets, the sustainability value proposition underpinning much of the Barrier Coated Paper Market's growth narrative remains partially unrealized, potentially constraining market expansion in geographies where environmental credentials lack corresponding infrastructure support.

Opportunity - Bio-Based and Compostable Barrier Coating Technology Innovation and Market Displacement

A significant innovation opportunity exists within the Barrier Coated Paper Market to develop and commercialize fully compostable barrier coatings derived from renewable feedstock. The eco-friendly barrier coating market is projected to grow at around a 7-9% growth rate through 2032, exceeding the broader Barrier Coated Paper Market's trajectory, signaling that sustainability-focused innovations command premium market positioning and growth acceleration.

Current water-based barrier coatings capture approximately 38% market share within coating type segmentation, yet technological development pathways remain nascent for advanced formulations incorporating plant-derived polymers, starch-based matrices, and bio-engineered barrier compounds.

Companies including BASF, Arkema, and Michelman are actively developing next-generation formulations, yet market gap analysis indicates substantial opportunity for differentiated approaches targeting specific application requirements such as grease-resistant coatings for food service, moisture-barrier solutions for pharmaceutical blister packs, and vapor-barrier systems for fresh produce.

Multi-Functional Barrier Integration and Specialised Application Development

Emerging applications within the barrier coated paper market increasingly demand multi-functional barrier properties, simultaneous protection against moisture, oxygen, grease, and aroma/flavour compounds alongside active packaging features including antimicrobial agents, freshness indicators, and intelligent tracking systems.

The barrier-coated flexible paper packaging market demonstrates that functional enhancement drives premium valuation and market segment differentiation. Within the barrier coated paper market, current mid-weight (60-150 GSM) category dominance at 49.5% market share masks a significant opportunity within lightweight (<60 GSM) applications, projected as the fastest-growing segment. Lightweight barrier-coated papers address cost optimization requirements for high-volume applications, including snack packaging, dry food wrapping, and non-contact surface barriers.

Dispersion coatings, identified as the fastest-growing segment within coating type, represent a nascent technology pathway for achieving superior barrier properties through advanced particle-based matrix structures.

The pharmaceutical sector, representing approximately 10-15% of addressable market share, offers a particular opportunity for specialized barrier solutions addressing moisture-sensitive active pharmaceutical ingredients, temperature stability requirements, and tamper-evident integration.

Category-wise Analysis

Coating Type Insights

Water-based barrier coatings maintain the dominant market position within the barrier-coated paper market, commanding approximately 38.0% market share in 2025 based on proprietary market segmentation data provided.

This leadership emerges from multiple reinforcing factors: regulatory preference through PFAS elimination mandates, superior environmental performance with negligible volatile organic compound (VOC) emissions compared to solvent-based alternatives, enhanced recyclability characteristics enabling seamless integration into existing fibre recycling infrastructure, and established manufacturing compatibility with high-speed production equipment.

Water-based coating systems deliver functional performance specifications across the complete range of barrier coated paper applications, from grease-resistant food service packaging to moisture-protective pharmaceutical applications.

These systems use aqueous polymer dispersions, frequently based on acrylic, styrene-acrylic, or polyurethane polymer matrices, that cure through coalescence and water evaporation rather than chemical cross-linking, enabling compatibility with rapid processing speeds and thermal-sensitive paper substrates.

The expanding installed base of water-based coating equipment among major paper producers, including Mondi, Sappi, Huhtamaki, and UPM Specialty Papers, has created network effects where converters standardize specifications around water-based systems, reducing switching costs and embedding market advantage.

Paper Weight Insights

Mid-weight papers within the 60-150 GSM range command the dominant market position in the barrier coated paper market, representing approximately 49.5% of market share in 2025 based on the provided segmentation data. This category's leadership emerges from fundamental application versatility, mid-weight substrates optimize functional performance across the complete spectrum of barrier-dependent packaging formats while maintaining cost efficiency relative to heavier substrates and premium functional performance compared to lightweight alternatives.

Lightweight barrier coated papers below 60 GSM represent the fastest-growing weight category within the barrier coated paper market, driven by regulatory mandates targeting packaging material minimization and economic incentives favoring weight reduction across the supply chain.

The EU Packaging and Packaging Waste Regulation establishes 50% maximum void space requirements for packaging structures, directly incentivizing converters to minimize substrate weight while maintaining functional barrier performance, creating market demand for lightweight barrier coated papers that achieve full barrier functionality at GSM levels previously considered technically inadequate.

Application Insights

Food and beverage packaging represents the dominant application segment within the barrier coated paper market, commanding approximately 56% market share in 2025 based on the provided segmentation data. This dominance emerges from fundamental functional requirements: food and beverage products demand multiparametric barrier protection against moisture ingress, oxygen penetration, grease migration, and aroma loss, precisely the performance specifications that barrier coated papers are engineered to deliver.

Personal care packaging represents the fastest-growing application segment within the barrier-coated paper market, reflecting accelerating brand-owner transition toward fibre-based sustainable packaging solutions for cosmetics, skincare products, and personal hygiene items.

Regional Insights and Trends

North America Barrier Coated Paper Market Trends

North America represents the third-largest regional market in the barrier coated paper market, commanding approximately 21% of global demand in 2025, driven by regulatory plastic elimination mandates, foodservice sector expansion, and pharmaceutical packaging transition toward sustainable materials.

The U.S. flexible packaging industry generated US$ 41.5 billion in sales in 2022, representing 21% of the country's US$ 180.3 billion packaging market, with food packaging dominating at approximately 50% of shipments, establishing substantial demand for barrier-coated paper alternatives to traditional plastic structures.

The U.S. food and beverage manufacturing sector employs approximately 1.7 million workers and is concentrated in key states, including California, Texas, and New York, creating geographic demand clusters for barrier coated paper packaging solutions.

Strategic capacity expansion initiatives by major manufacturers, including Huhtamaki (Hammond, Indiana egg carton expansion; Texas folded carton facility investment) and Mondi, demonstrate confidence in sustained North American market growth and profitability potential.

North America's market position reflects regulatory plastic elimination timelines, substantial foodservice sector demand, and pharmaceutical packaging transition trajectories, positioning the region for steady market expansion through the forecast period, supported by regulatory compliance requirements and brand owner sustainability commitments.

East Asia Barrier Coated Paper Market Trends

East Asia commands the largest regional market share in the barrier coated paper market, representing approximately 35% of global demand in 2025, reflecting the region's dominance in global manufacturing capacity, high-volume packaging conversion operations, and rapidly expanding consumer goods distribution infrastructure.

China's paper and paperboard production capacity exceeded 100 million tons in 2024, with coated paper products representing nearly 45% of total production, establishing China as the world's largest producer of barrier coated papers and primary manufacturing hub serving global supply chains.

Manufacturing cost advantages in China, India, and Southeast Asia have concentrated global barrier coated paper production capacity in the East Asian region, creating network effects that reinforce regional market leadership and facilitate supply chain integration across food, beverage, and consumer goods segments.

Indian packaging sector expansion, valued at US$ 86 billion in 2024 with annual growth rates of 22-25%, demonstrates accelerating domestic demand for barrier coated papers in food processing, e-commerce logistics, and retail packaging applications, with 861 operational paper mills providing substantial local production infrastructure.

East Asia's regional market position reflects both manufacturing ecosystem advantages and domestic consumption growth trajectories, positioning the region for sustained market dominance through the forecast period.

Europe Barrier Coated Paper Market Trends

Europe represents the second-largest regional market in the barrier coated paper market, commanding approximately 26% of global demand in 2025, driven by stringent regulatory frameworks establishing binding plastic reduction mandates and the world's most advanced recycling infrastructure supporting specialised barrier coating materials.

The EU Packaging and Packaging Waste Regulation (PPWR) establishes the regulatory foundation for European market expansion, with enforcement timelines creating systematic procurement pressure for barrier coated papers across food, beverage, and consumer goods packaging segments.

Competitive Landscape

The global barrier coated paper market is moderately consolidated, with a few large multinational companies dominating global production and innovation.

Key players such as Mondi Group, Stora Enso Oyj, Sappi Limited, Ahlstrom-Munksjö Oyj, and International Paper hold significant market presence through extensive product portfolios and strong distribution networks. These companies focus on sustainable coating technologies, including water-based and dispersion coatings, to meet the rising demand for eco-friendly packaging solutions.

The market exhibits oligopolistic traits, where continuous R&D, technological integration, and sustainable product innovation act as major competitive differentiators. Regional players and converters contribute to localised supply but operate at smaller scales compared to these global leaders.

Key Industry Developments

- In February 2025, delfort introduced ThinBarrier 302, a high-performance barrier coated paper for heat-sealing and cold-sealing flexible food packaging applications. The product offers combined oxygen, water vapour, and grease resistance comparable to plastic films while being lightweight and recyclable, marking a significant advancement in sustainable, PFAS-free barrier paper technology.

- In September 2021, Toppan announced the development of GL-X-P, a new barrier coated paper offering high water vapor resistance, excellent flex durability, and full heat sealability for food, cosmetic, and toiletry packaging. The innovation enables plastic-free, recyclable packaging with up to 35% lower CO2 emissions, marking a major step in sustainable paper-based barrier solutions under Toppan’s GL BARRIER portfolio.

Companies Covered in Barrier Coated Paper Market

- International Paper

- Mondi Group

- Stora Enso Oyj

- Sappi Limited

- Ahlstrom-Munksjö Oyj

- Cascades Inc.

- Gascogne Group

- Schweitzer-Mauduit International

- Domtar Corporation

- Twin Rivers Paper Company

Frequently Asked Questions

The global barrier coated paper market is projected to be valued at US$ 3.3 Bn in 2025.

The Water-Based Coatings segment is expected to account for approximately 38% of the global Barrier Coated Paper Market by coating type in 2025.

The barrier coated paper market is expected to witness a CAGR of 6.6% from 2025 to 2032.

The barrier coated paper market growth is driven by stringent global regulations phasing out single-use plastics and PFAS, coupled with rising demand for sustainable, shelf-life-extending packaging solutions that reduce food waste and ensure regulatory compliance.

Key market opportunities in the barrier coated paper market lie in the development of bio-based and fully compostable coating technologies, along with multi-functional barrier solutions that combine moisture, grease, and vapor protection for high-value applications across food, pharmaceutical, and personal care packaging segments.

The leading global players in the Barrier Coated Paper market include International Paper, Mondi Group, Stora Enso Oyj, Sappi Limited, and Ahlstrom-Munksjö Oyj.