- Biotechnology

- Blood Brain Barrier Technology Market

Blood Brain Barrier Technology Market Size, Share, and Growth Forecast, 2026 - 2033

Blood Brain Barrier Technology Market by Product Type (Nanocarriers, Transporters, Others), Technology (Invasive Technologies, Non-Invasive Technologies), Application (Neurological Disorders, Oncological Disorders, Others), and Regional Analysis 2026 - 2033

Blood Brain Barrier Technology Market Size and Trends Analysis

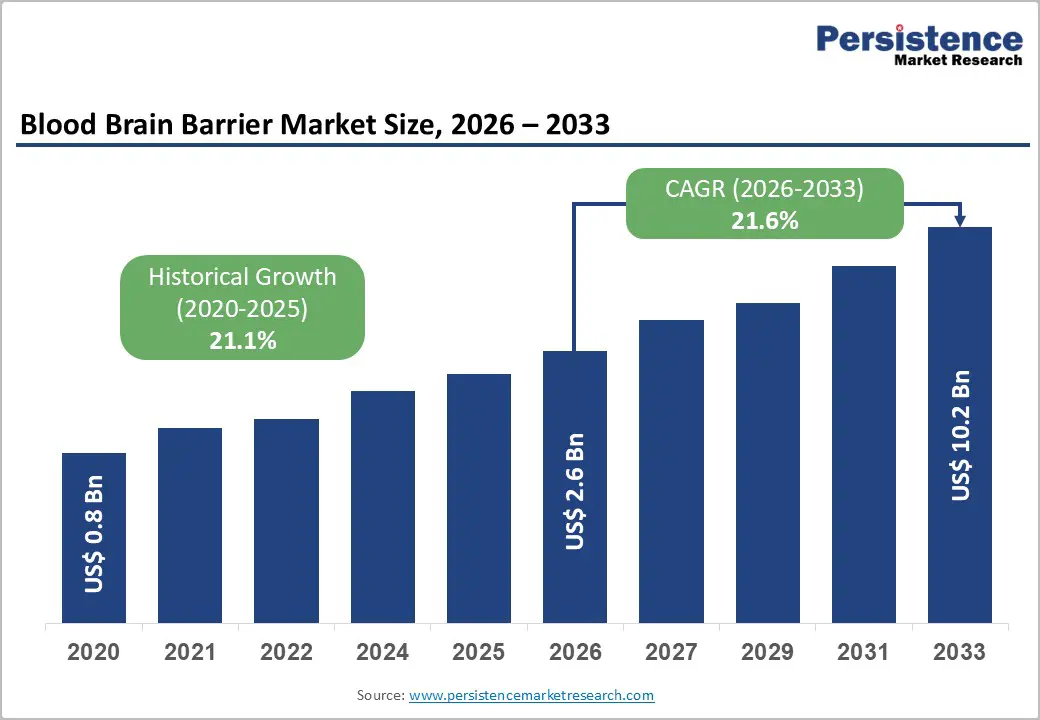

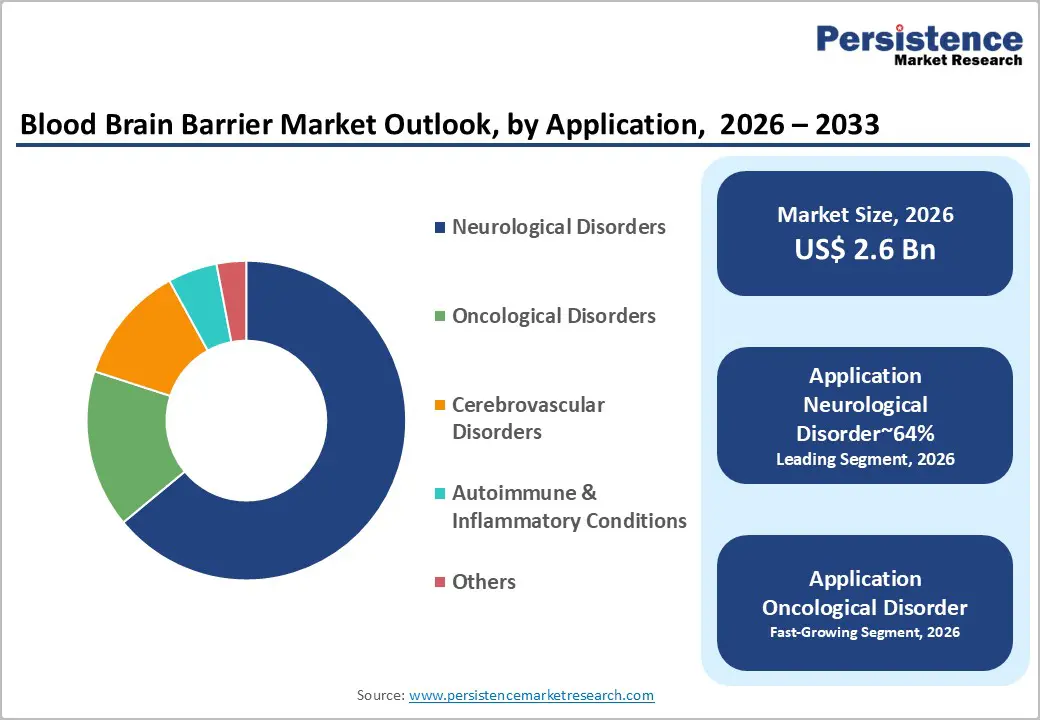

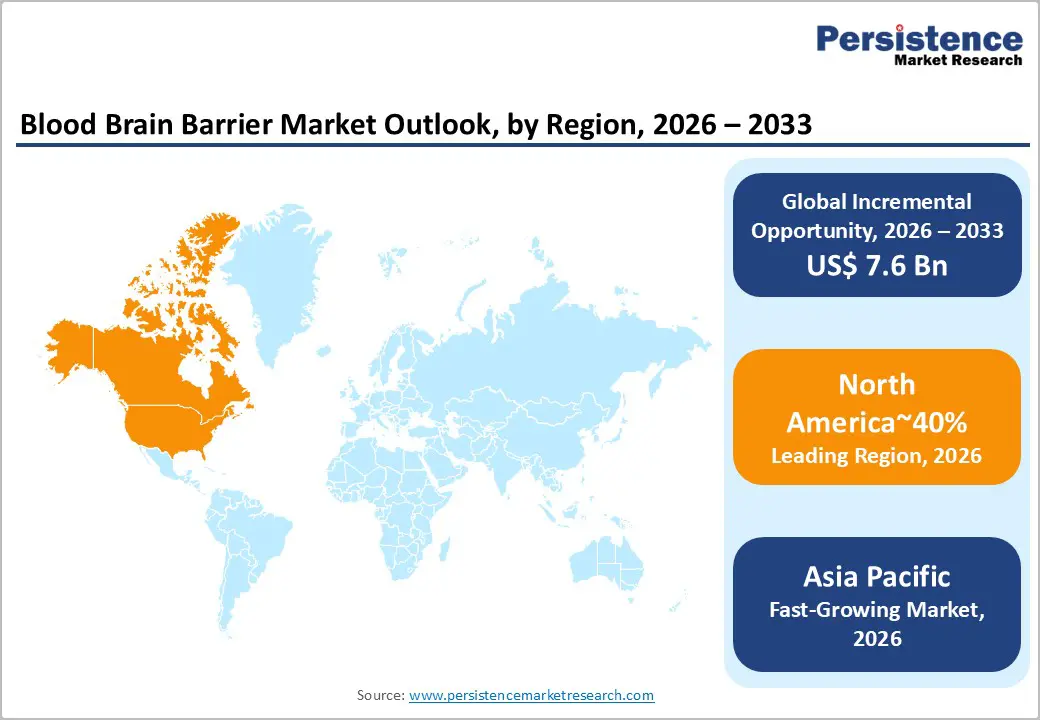

The global blood brain barrier technology market size is likely to be valued at US$2.6 billion in 2026 and is expected to reach US$10.2 billion by 2033, growing at a CAGR of 21.6% during the forecast period from 2026 to 2033, driven by the rising prevalence of complex neurological disorders that necessitate sophisticated delivery systems for large-molecule therapeutics. Structural shifts toward nanocarrier-based systems reinforce uptake across neuro and onco applications.

Advancements in non-invasive delivery mechanisms are currently reshaping clinical treatment paradigms for brain-related pathologies. Targeted drug delivery remains a critical priority for oncological and neurodegenerative pharmaceutical pipelines. Market momentum continues to accelerate as genomic research identifies novel vascular transport receptors. This trajectory positions the market for sustained momentum amid evolving therapeutic needs.

Key Industry Highlights:

- Leading Region: North America is projected to lead, accounting for approximately 40% share in 2026, supported by robust clinical research infrastructure and high healthcare expenditure.

- Fastest-growing Region: Asia Pacific is anticipated to grow the fastest, driven by rapid healthcare modernization and increasing investments in biotechnology.

- Leading Technology: Non-invasive is expected to lead, accounting for approximately 69% share in 2026, anchored by patient safety and reduced procedural complexity.

- Leading Application: The neurological segment is anticipated to dominate, accounting for approximately 64% share in 2026, anchored by the high incidence of Alzheimer’s and Parkinson’s.

| Key Insights | Details |

|---|---|

|

Blood Brain Barrier Technology Market Size (2026E) |

US$2.6 Bn |

|

Market Value Forecast (2033F) |

US$10.2 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

21.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

21.1% |

DRO Analysis

Driver Analysis – Rising Neurological Disease Prevalence and Targeted Delivery Innovation

The increasing prevalence of neurodegenerative disorders is intensifying demand for advanced brain-targeted delivery systems globally. Conditions such as Alzheimer’s and Parkinson’s require sustained therapeutic concentrations within protected cerebral environments. Conventional administration pathways face constraints due to restrictive vascular barriers limiting effective drug penetration. This clinical limitation drives the adoption of specialized transport mechanisms, enhancing targeting precision and reducing systemic exposure. Healthcare systems prioritize solutions balancing efficacy with safety across vulnerable populations requiring long-term neurological treatments. Regulatory emphasis on safety and efficacy further accelerates the adoption of precision-oriented transport mechanisms across pharmaceutical pipelines.

Roche utilizes Brain Shuttle technology to enhance antibody penetration within central nervous system therapeutic applications. These platforms leverage receptor-mediated pathways, improving delivery efficiency and therapeutic precision across neurological treatment frameworks. Clinical pipelines increasingly prioritize transport-enabled biologics addressing complex central nervous system disorders with higher specificity. The integration of delivery technologies reshapes drug development by aligning pharmacokinetics with targeted tissue engagement. Cost structures shift toward advanced biologics and delivery integration, reflecting higher development and validation requirements. This convergence between disease burden and delivery innovation strengthens sustained demand for advanced therapeutic transport systems globally.

Breakthroughs in Nanotechnology-Enabled Drug Delivery Systems

Nanotechnology advancements enable encapsulation of therapeutic agents within carriers, overcoming complex biological delivery barriers. These systems protect active compounds from enzymatic degradation, preserving efficacy during systemic circulation phases. Surface functionalization facilitates targeted interaction with endothelial structures, improving localization within sensitive brain tissues. Reduced reliance on invasive procedures enhances treatment accessibility while minimizing associated clinical risks significantly. Improved particle stability ensures consistent performance, strengthening adoption across regulated pharmaceutical manufacturing environments globally.

Abiogen Pharma utilizes nanocarrier systems engineered for the efficient transport of hydrophilic therapeutic compounds. These technologies integrate with established production workflows, enabling scalable manufacturing of complex therapeutic formulations efficiently. Enhanced delivery efficiency reduces dosing frequency, improving adherence and optimizing overall treatment outcomes across patient groups. Material science innovation continuously refines carrier composition, supporting improved biocompatibility and controlled release mechanisms. Cost structures shift toward advanced materials and precision engineering, increasing development complexity and validation requirements. This technological progression expands application scope across neurological and oncological domains, requiring targeted therapeutic interventions.

Restraint Analysis – High Manufacturing Complexity in Nanocarrier Production

Scalable production of stable nanocarriers requires stringent control over particle uniformity and physicochemical consistency. Variability in yield inflates cost structures, particularly within lipid-based carrier systems requiring specialized inputs. Supply disruptions in critical raw materials further compound margin pressures across integrated pharmaceutical manufacturing operations. Manufacturers encounter persistent batch-to-batch inconsistencies, complicating regulatory validation and quality assurance processes. These technical constraints limit affordability and restrict adoption among mid-tier pharmaceutical companies with constrained capital structures. Process standardization remains challenging due to sensitivity of nanoscale formulations to environmental and operational fluctuations.

Modulus Discovery demonstrates peptide transporter platforms that highlight reproducibility challenges during scale-up and commercialization phases. Facility expansions encounter validation hurdles as regulatory frameworks demand stringent consistency across production cycles. Downstream healthcare providers prioritize cost-effective therapeutic alternatives amid constrained procurement budgets and reimbursement limitations. This dynamic results in stagnating procurement volumes, particularly within price-sensitive regional healthcare systems globally. Elevated production complexity increases dependency on specialized infrastructure and skilled technical labor across manufacturing environments. These cumulative barriers persist despite technological refinements, constraining widespread commercialization of advanced nanocarrier-based therapeutics.

Physiological Complexity of Cerebral Vasculature

The restrictive architecture of cerebral vasculature presents a persistent biological constraint for therapeutic delivery systems. Tight junctions between endothelial cells prevent the passage of most large-molecule drugs across protective barriers. Active efflux transporters continuously remove foreign substances, limiting retention within the central nervous system environments. These defense mechanisms significantly reduce the effectiveness of many advanced therapeutic delivery candidates under development. Overcoming such barriers without inducing tissue damage remains a primary engineering and clinical challenge. The interplay between vascular protection and drug permeability creates stringent constraints on delivery system design.

Biological variability among patients introduces unpredictability in drug distribution, absorption kinetics, and therapeutic response outcomes. I-Mab develops claudin-targeting technologies that must address fluctuating expression levels of barrier protein structures. These physiological differences affect delivery consistency and complicate reproducibility across heterogeneous patient populations globally. Aliada Therapeutics advances MODEL platform capabilities to refine ligand-receptor interactions, improving transport reliability across varying conditions. Regulatory validation becomes complex due to inconsistent pharmacokinetic profiles observed across diverse clinical cohorts. This inherent biological complexity continues to constrain scalable deployment of brain-targeted therapeutic delivery systems.

Opportunity Analysis – Expansion of Non-Invasive Focused Ultrasound in Neurotherapeutics

Focused ultrasound provides a temporary and reversible mechanism to modulate vascular barrier permeability within cerebral tissues. This technology enables localized drug delivery without requiring invasive surgical penetration of cranial structures. Increasing clinical validation of ultrasound-mediated transport is attracting capital from regulated medical device manufacturers globally. Precision targeting of specific brain regions enhances therapeutic outcomes for focal tumor and neurological disorder treatments. Patient preference for non-invasive modalities reduces hospitalization duration and lowers risk exposure associated with surgical interventions. These attributes position focused ultrasound as a viable pathway for advancing targeted neurotherapeutic delivery frameworks.

Integration of imaging modalities with ultrasound platforms is establishing new clinical workflows within neuro-oncology treatment environments. Insightec deploys Exablate Neuro systems, enabling controlled barrier modulation under real-time imaging guidance. This convergence facilitates direct delivery of therapeutic agents into localized brain tumor regions with improved precision. Complementary innovation continues to refine system interoperability and enhance procedural reproducibility across clinical settings. Regulatory acceptance strengthens as safety and efficacy data accumulate across diverse patient cohorts globally. Expanding adoption of these integrated systems is reinforcing demand for specialized hardware and software within neurotherapeutic infrastructure.

AI-Optimized Design Platforms in Brain Drug Delivery

Artificial intelligence algorithms enable the prediction of optimal carrier properties for effective biological barrier traversal mechanisms. These computational approaches reduce reliance on empirical screening, accelerating lead identification within complex therapeutic pipelines. Pharmaceutical companies leverage such platforms to compress research timelines and optimize resource allocation across development stages. Emerging demand for personalized neurotherapies expands application scope for data-driven design methodologies in targeted delivery. Regulatory support for digital health technologies strengthens investment flows into integrated computational drug discovery ecosystems.

Insilico Medicine advances artificial intelligence-generated blood-brain barrier penetrants through virtual screening and predictive modeling frameworks. Platform integration of machine learning into discovery pipelines enhances candidate optimization and improves molecular targeting precision. Strategic collaborations with nanotechnology firms refine carrier profiles and improve translational feasibility across therapeutic applications. This convergence of artificial intelligence and material science strengthens positioning within niche and orphan neurological indications. Cost efficiencies emerge through reduced experimental burden and improved success rates across early-stage development phases.

Category–wise Analysis

Technology Insights

Non-invasive technology is expected to lead, accounting for approximately 69% share in 2026, underpinned by the rising demand for outpatient procedures. This segment prioritizes patient comfort and minimizes the risks associated with traditional neurosurgical interventions. Advanced chemical and biological transport mechanisms allow for the systemic administration of brain-targeted therapeutic agents. Adoption remains anchored in safety and efficacy, as manufacturers focus on reducing procedural complexity and cost. Insightec with Exablate Neuro provides a clinical benchmark for non-surgical barrier modulation through focused ultrasound energy. Roche with Brain Shuttle further demonstrates the potential of intravenous protein-based transport platforms. This structural shift toward non-invasive solutions sustains the segment’s dominance within neurological care frameworks.

Non-invasive technology is anticipated to be the fastest-growing segment, driven by the rapid evolution of ligand-mediated transport and nanocarrier systems. Pharmaceutical companies are prioritizing delivery methods that do not require specialized surgical suites or prolonged hospitalization. This trend aligns with global healthcare initiatives aimed at reducing the economic burden of chronic disease management. Denali Therapeutics with Transport Vehicle (TV) platform exemplifies the transition toward sophisticated molecular shuttling technologies. Ongoing research into intranasal delivery routes further expands the scope of non-invasive therapeutic applications. As regulatory pathways for these technologies become clearer, clinical uptake is projected to accelerate significantly. This momentum is reinforced by increasing patient preference for treatments that offer minimal lifestyle disruption.

Application Insights

Neurological disorders are anticipated to lead the market, accounting for approximately 64% share in 2026, anchored by the high prevalence of age-related cognitive disorders. The global increase in Alzheimer’s and Parkinson’s cases necessitates reliable methods for delivering large molecules to the brain. Therapeutic success in these areas depends entirely on achieving consistent penetration through the protective vascular layer. Healthcare systems are allocating significant budgets toward long-term management strategies for neurodegenerative conditions. Biogen with Aduhelm represents the intense focus on amyloid-clearing treatments requiring specialized delivery considerations. AbbVie, with specialized neuro-pipelines, continues to invest in mechanisms that enhance drug bioavailability in cerebral tissues. This clinical demand profile ensures the continued leadership of the neurological segment.

Oncological disorders are forecast to be the fastest-growing segment, driven by the urgent need for more effective treatments for primary and metastatic brain tumors. Conventional chemotherapy often fails to reach effective concentrations due to the restrictive nature of the blood-brain barrier. Emerging delivery technologies enable the targeted release of cytotoxic agents directly into malignant tissues while sparing healthy cells. Angiochem with ANG1005 demonstrates the potential for peptide-drug conjugates to improve survival rates in brain cancer. Integration of diagnostic tools with therapeutic delivery is gaining traction within oncology research centers. As clinicians seek to overcome the limitations of systemic radiation and surgery, targeted delivery becomes essential. This strategic shift is set to expand the utilization of barrier-crossing technologies.

Regional Insights

North America Blood Brain Barrier Technology Market Trends

North America is expected to remain the leading regional market, accounting for approximately 40% share in 2026, supported by high concentrations of biotechnology innovation hubs and advanced clinical research facilities. The region’s dominance is anchored in a robust pharmaceutical industry that prioritizes high-value neurodegenerative and oncological therapeutic pipelines. Substantial healthcare expenditure facilitates the early adoption of expensive and sophisticated drug delivery technologies across hospital networks. Well-established regulatory frameworks provide a clear path for the commercialization of novel transport mechanisms and medical devices. Federal funding for brain research continues to sustain the development of groundbreaking vascular modulation strategies within academic and private sectors.

The US is expected to anchor regional momentum through sustained investments in genomic medicine and advanced neuro-oncology treatment protocols. Government-led initiatives such as the BRAIN Initiative are anticipated to accelerate the discovery of novel transport targets within the cerebral vasculature. Biogen with Aduhelm illustrates the country’s leading role in bringing complex neurological therapies to the domestic clinical market. Strategic collaborations between technology providers and major academic medical centers are projected to increase procurement volumes for specialized delivery systems. Regulatory alignment between the FDA and industry leaders further streamlines the introduction of innovative nanocarrier and transporter technologies.

Europe Blood Brain Barrier Technology Market Trends

Europe is expected to remain a mature and structurally stable regional market, with demand primarily anchored in high standards of neurological care and public health initiatives. The region's market structure is reinforced by integrated healthcare systems that emphasize long-term management of chronic brain diseases. Stringent safety regulations ensure that only the most validated and reliable delivery technologies reach the commercial stage. Collaborative research networks across the continent foster the development of standardized protocols for blood-brain barrier modulation. Procurement is likely to remain focused on cost-effective yet highly precise non-invasive delivery solutions.

Germany is anticipated to lead European market activity through its dense network of specialized neurological clinics and medical device manufacturing clusters. Significant investments in biotechnology research are expected to drive the local development of advanced transporter-mediated delivery platforms. Roche, with Brain Shuttle technology, benefits from the country’s strong focus on integrating diagnostics with targeted therapeutic interventions. Public-private partnerships are poised to enhance the accessibility of innovative treatments for Alzheimer’s across the national healthcare system. Regulatory stability within the European Medicines Agency framework provides a consistent environment for long-term product planning and market entry.

Asia Pacific Blood Brain Barrier Technology Market Trends

Asia Pacific is expected to register the fastest growth trajectory, as rapid modernization of healthcare infrastructure and expanding manufacturing capabilities accelerate market expansion. The region's momentum is anchored in rising investments from both domestic and international biotechnology firms seeking to capitalize on growing patient populations. Increasing government focus on addressing the healthcare needs of aging demographics drives demand for advanced neurological treatments. Local manufacturers are rapidly adopting global standards for the production of nanocarriers and specialized transport ligands. This geographic shift is creating new opportunities for the localized assembly and distribution of delivery systems.

China is expected to remain the primary engine of growth in the region through aggressive state-supported biotechnology development goals. Sustained investments in pharmaceutical R&D are anticipated to broaden the availability of targeted therapies for chronic brain disorders. I-Mab with Claudin-targeting technologies demonstrates the increasing capability of domestic firms to innovate within the complex delivery space. Growing middle-class demand for premium healthcare services is projected to increase the utilization of non-invasive focused ultrasound systems. Strategic acquisitions of Western technology firms by Chinese enterprises are likely to further accelerate local technological advancement and market penetration.

Competitive Landscape

The blood brain barrier technology market is consolidated, with leadership concentrated among specialized biotechnology and pharmaceutical firms such as Denali Therapeutics and Roche. These leaders exert influence through advanced delivery platforms, extensive patent portfolios, and integration within global pharmaceutical pipelines. Their technologies establish benchmarks for transport efficiency, safety validation, and regulatory compliance across neurological therapeutics. Long-term licensing agreements and co-development partnerships anchor their role in shaping procurement and innovation pathways. High technical complexity and capital intensity reinforce barriers, limiting participation to technologically advanced organizations. This concentration supports standardized development frameworks across emerging brain-targeted therapeutic applications.

Competitive positioning reflects vertical differentiation through platform versatility and integration across biologics, devices, and delivery systems. Premium participants emphasize high-specificity transporter technologies, while others explore scalable nanocarrier-based approaches for broader applications. Companies such as AbbVie are advancing integrated platforms combining therapeutic development with targeted delivery mechanisms. Industry dynamics include strategic acquisitions, consolidating proprietary transport technologies, and expanding clinical-stage portfolios. Platform evolution increasingly incorporates artificial intelligence and imaging tools to enhance delivery precision and monitoring. Forward-looking strategies prioritize regulatory navigation capabilities and scalable manufacturing aligned with advancing clinical commercialization pipelines.

Key Industry Developments:

- In March 2026, Lunai Bioworks executed a binding $20 million strategic transaction to acquire a BBB delivery platform and CNS Alzheimer's assets from Clemann Group. This acquisition addresses the critical "delivery bottleneck" by integrating an AI-driven platform capable of transporting inactive compounds that activate specifically once inside the brain.

- In March 2026, Denali Therapeutics received FDA accelerated approval for AVLAYAH™ (tividenofusp alfa), its first commercial Enzyme Transport Vehicle (ETV) for Hunter Syndrome. This marks the first commercial validation of a receptor-mediated "Trojan Horse" platform, proving that large-molecule enzymes can be successfully shuttled across the BBB at scale.

- In February 2026, Denali Therapeutics presented positive initial clinical data for DNL126, an ETV-enabled therapy for Sanfilippo syndrome Type A, at the 2026 WORLD Symposium. The data support an accelerated approval path for a second major ETV candidate, reinforcing Denali's lead in the rare-disease CNS market.

Companies Covered in Blood Brain Barrier Technology Market

- Denali Therapeutics

- Roche

- AbbVie

- Biogen

- Insightec

- Angiochem

- ArmaGen

- Bioasis Technologies

- I-Mab

- Eisai

- Medtronic

- CarThera

- Precision NanoSystems

- WuXi AppTec

- Insilico Medicine

- Alzheon

Frequently Asked Questions

The global blood brain barrier technology market is projected to be valued at US$2.6 billion in 2026. It is expected to reach US$10.2 billion by 2033, driven by increasing demand for targeted drug delivery in neurological and oncological disorders.

The inability of conventional therapeutics to cross the blood-brain barrier effectively is a major constraint, driving the adoption of advanced transport mechanisms such as nanocarriers and receptor-mediated systems that enhance drug bioavailability, precision, and safety in central nervous system treatments.

The blood brain barrier technology market is forecast to grow at a CAGR of 21.6% from 2026 to 2033, reflecting rapid innovation in nanotechnology, biologics, and non-invasive delivery platforms.

North America is the leading regional market, accounting for approximately 40% share, supported by strong clinical research infrastructure, high healthcare expenditure, and advanced biotechnology ecosystems driving early adoption of innovative delivery technologies.

The market is consolidated, with key players including Roche, Denali Therapeutics, AbbVie, Biogen, and Insightec, competing through advanced delivery platforms and strong R&D pipelines.