- Medical Devices

- Global Balloon Introducer System Market

Global Balloon Introducer System Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Global Balloon Introducer System Market by Product (Normal Balloon Introducer, Cutting and Scoring Balloon Introducer, Drug-Coated Balloon Introducer, and Stent Graft Balloon Introducer), by Technology (Rapid Exchange (Rx), Over the Wire (OTW), and Fixed Wire Balloon Catheter), by Application (Coronary Artery Diseases, Peripheral Artery Diseases, and Neurovascular Diseases) by End User (Hospital, Catheterization Laboratories, and Ambulatory Surgical centers), and Regional Analysis from 2026 to 2033.

Balloon Introducer System Market Share and Trends Analysis

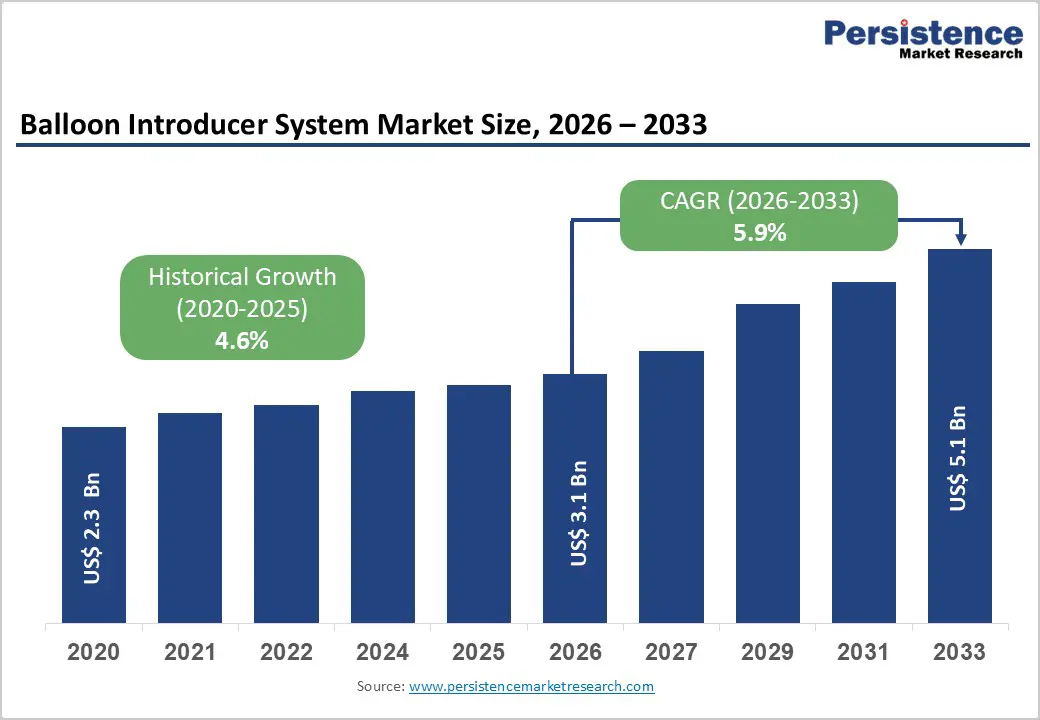

The global Balloon Introducer System Market size is estimated to grow from US$ 3.1 Bn in 2026 to US$ 5.1 Bn by 2033. The market is projected to record a CAGR of 5.9% during the forecast period from 2026 to 2033.

Global demand for balloon introducer systems is rising steadily, driven by the growing burden of cardiovascular and peripheral vascular diseases worldwide. Increasing prevalence of coronary artery disease, peripheral artery disease, and neurovascular disorders largely linked to aging populations, diabetes, obesity, and sedentary lifestyles is expanding the pool of patients requiring catheter-based interventions. Rising procedure volumes for angioplasty, stent deployment, and endovascular therapies are directly supporting demand for reliable and high-performance balloon introducer systems. Advancements in catheter design, including improved trackability, pushability, and coating technologies, are enhancing procedural success rates while reducing complications. The shift toward minimally invasive, image-guided, and outpatient interventions is further accelerating adoption. Additionally, expanding healthcare investments in catheterization laboratories, growing interventional cardiology expertise, and continuous clinical innovation in balloon technologies are reinforcing sustained market growth across both developed and emerging regions.

Key Industry Highlights

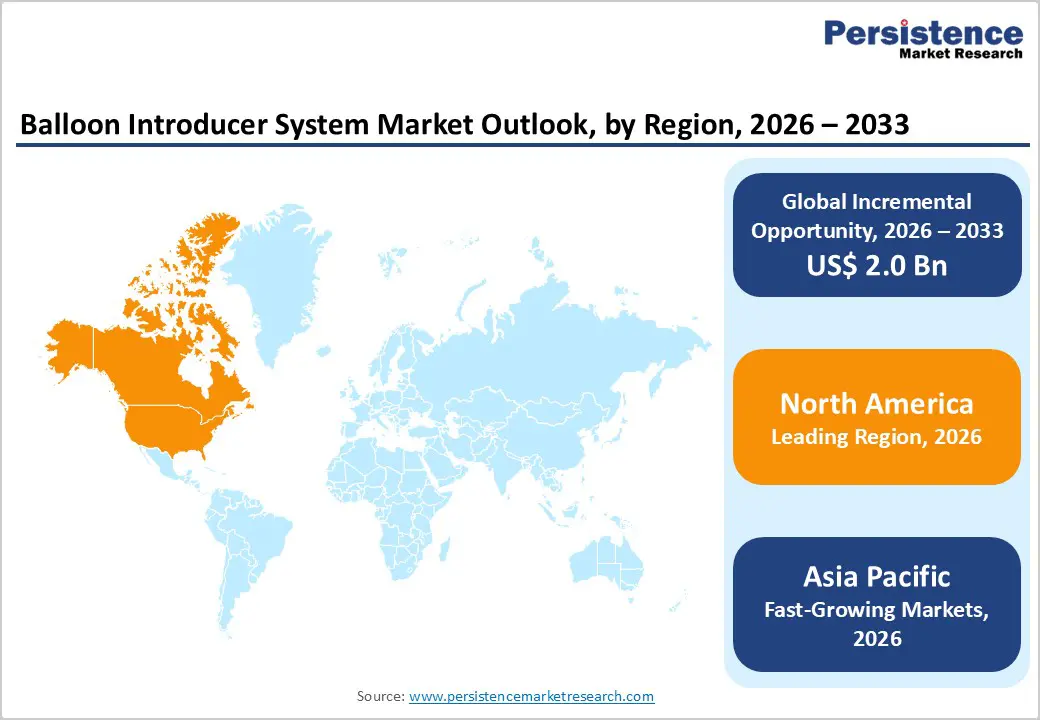

- Leading Region: North America holds the largest market share at 48.5%, supported by advanced catheterization infrastructure, high volumes of coronary and peripheral interventions, favorable reimbursement policies, and early adoption of next-generation balloon introducer technologies.

- Fastest-Growing Region: Asia Pacific is expanding at the fastest pace due to a large and underserved patient population, rising incidence of cardiovascular diseases, rapid growth of tertiary care hospitals, and increasing government investment in cardiac and vascular care.

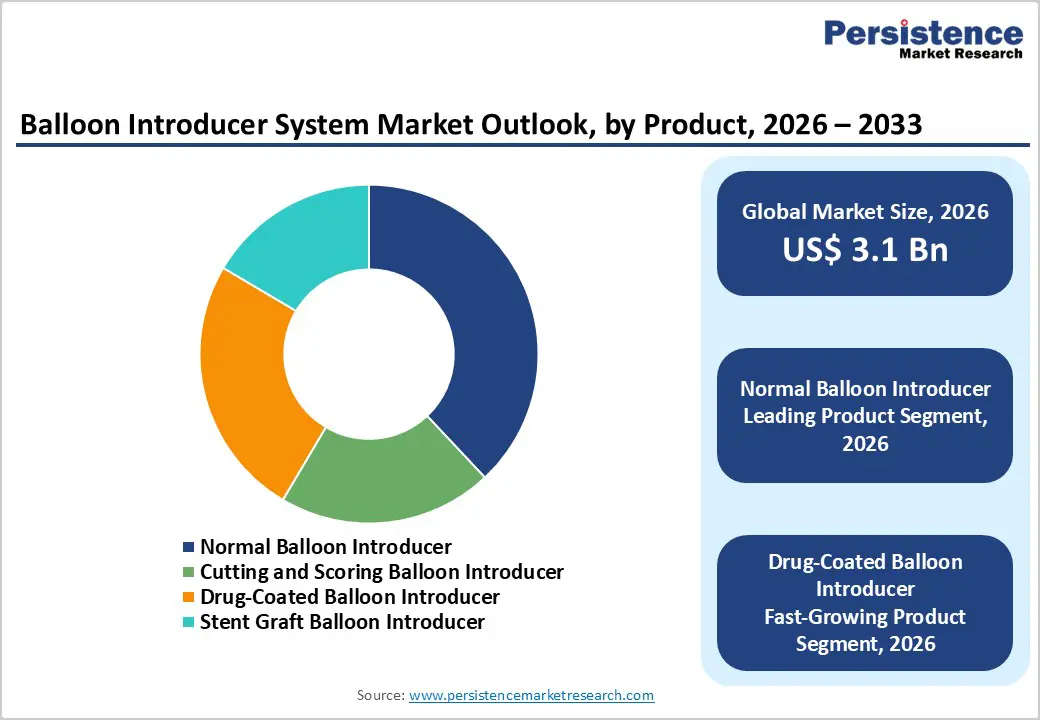

- Leading Product Segment: Normal balloon introducer dominates the market due to its cost-effectiveness, procedural reliability, and broad applicability across coronary, peripheral, and neurovascular interventions.

- Fastest-Growing Product Segment: Drug-coated balloon introducer is witnessing rapid growth as its use expands in restenosis-prone lesions and complex vascular interventions.

- Leading Application Segment: Coronary artery diseases remain the largest application segment due to high intervention volumes among aging populations and widespread adoption of percutaneous coronary procedures.

- Fastest-Growing Application Segment: Peripheral artery diseases are expanding rapidly as early endovascular intervention becomes standard practice for limb preservation and vascular restoration.

| Key Insights | Details |

|---|---|

| Balloon Introducer System Market Size (2026E) | US$ 3.1Bn |

| Market Value Forecast (2033F) | US$ 5.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.9% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.6% |

Market Dynamics

Driver – Rising Burden of Cardiovascular Diseases and Advancements in Balloon Catheter Technologies Driving Market Growth

The increasing global prevalence of cardiovascular and peripheral vascular diseases is a primary driver of sustained growth in the balloon introducer system market. Rising incidence of coronary artery disease, peripheral artery disease, and neurovascular disorders driven by aging populations, diabetes, obesity, smoking, and sedentary lifestyles is significantly expanding the number of patients requiring catheter-based interventions. Higher survival rates following acute cardiac events and chronic vascular conditions are increasing demand for repeat and complex endovascular procedures, further supporting long-term utilization of balloon introducer systems.

Technological advancements are accelerating adoption across interventional settings. Continuous innovation in balloon design, including improved trackability, pushability, lesion-crossing capability, and pressure resistance, is enhancing procedural success rates and clinical outcomes. Developments in coating technologies, shaft materials, and balloon compliance profiles are reducing vessel trauma and procedural complications. In parallel, growing adoption of minimally invasive, image-guided interventions and expansion of catheterization laboratories worldwide are increasing procedural volumes. Integration of balloon introducer systems with advanced imaging platforms and next-generation guidewires is further improving precision and efficiency. Together, rising disease burden and sustained technological innovation are driving steady expansion of the global balloon introducer system market.

Restraints – High Procedure Costs and Limited Access to Advanced Interventional Care Restricting Market Penetration

High procedural costs associated with endovascular interventions remain a key restraint for the balloon introducer system market, particularly in low- and middle-income regions. Although balloon introducer devices themselves are relatively standardized, overall treatment costs are elevated due to the need for advanced catheterization laboratories, imaging systems, contrast agents, and highly trained interventional specialists. Expenses related to consumables, repeat procedures, and post-intervention monitoring further increase the economic burden on healthcare systems and patients. In many regions, inconsistent or limited reimbursement coverage for interventional cardiology and peripheral procedures restricts patient access and delays treatment.

Additionally, uneven availability of skilled interventional cardiologists and vascular specialists limits broader market adoption. Balloon-based interventions require specialized training and experience, particularly for complex coronary, peripheral, and neurovascular procedures. In emerging markets, gaps in healthcare infrastructure, limited access to cath labs, and fragmented referral pathways contribute to underutilization. Rural and semi-urban areas often lack advanced diagnostic and interventional capabilities, leading to delayed diagnosis and reliance on medical management rather than procedural intervention. These economic, infrastructural, and workforce-related constraints continue to limit full market potential despite growing clinical demand.

Opportunity – Expansion of Catheterization Infrastructure and Shift Toward Minimally Invasive Interventions Creating Growth Potential

Expansion of advanced cardiovascular care infrastructure presents a significant growth opportunity for the global balloon introducer system market. Governments and private healthcare providers are increasingly investing in catheterization laboratories, cardiac care centers, and vascular specialty hospitals to address the rising burden of cardiovascular disease. Development of tertiary and quaternary care facilities, particularly in Asia Pacific, Latin America, and the Middle East, is improving access to interventional procedures and supporting higher device utilization. These investments are enabling wider adoption of modern balloon introducer systems across both public and private healthcare settings.

The ongoing shift toward minimally invasive, catheter-based interventions is further creating strong growth avenues. Physicians are increasingly favoring angioplasty and endovascular therapies over open surgical procedures due to shorter recovery times, reduced complication risks, and lower overall healthcare costs. Growing adoption of outpatient and same-day discharge models is reinforcing demand for efficient, easy-to-handle balloon introducer systems. Advancements in drug-coated balloons, specialty balloons, and compatibility with complex lesion management are expanding clinical applications. In parallel, continued research into novel materials, coatings, and device integration is expected to unlock new opportunities and sustain long-term market growth.

Category-wise Analysis

By Product, Normal Balloon Introducer Leads Owing to Broad Clinical Utility and Cost Efficiency

The normal balloon introducer segment is projected to dominate the global balloon introducer system market in 2026, accounting for a revenue share of 38.0%. Segment leadership is primarily driven by its broad applicability across coronary, peripheral, and neurovascular interventions, making it a first-line choice in routine angioplasty procedures. Normal balloon introducers offer reliable performance, predictable inflation characteristics, and compatibility with a wide range of guidewires and access systems. Their relatively lower cost compared to specialized or drug-coated variants supports widespread adoption, particularly in high-volume catheterization laboratories and cost-sensitive healthcare settings. Strong physician familiarity, standardized procedural workflows, and consistent clinical outcomes further reinforce their dominance. Additionally, continuous refinements in balloon materials, shaft flexibility, and trackability have enhanced procedural reliability, supporting sustained use across both elective and emergency interventions.

By Application, Rapid Exchange (Rx) Systems Dominate Due to Procedural Efficiency and Ease of Use

The rapid exchange (Rx) segment is projected to dominate the global balloon introducer system market in 2026, accounting for a revenue share of 52.0%. This dominance is attributed to the growing preference for streamlined interventional workflows that reduce procedure time and improve catheter handling. Rapid exchange systems enable single-operator control, faster device exchanges, and improved procedural efficiency, which are critical in high-throughput cardiac catheterization environments. Increasing volumes of coronary and peripheral interventions, particularly among aging populations with complex vascular disease, continue to support strong adoption. Rx systems are especially favored in minimally invasive procedures due to their ease of navigation and reduced learning curve. Technological advancements improving pushability, torque response, and lesion-crossing performance further strengthen their clinical appeal, reinforcing rapid exchange platforms as the preferred technology across most interventional settings.

By End User, Hospitals Maintain Leadership Due to High Procedure Volumes and Advanced Capabilities

The hospitals segment is projected to dominate the global balloon introducer system market in 2026, accounting for a revenue share of 64.5%. Hospitals remain the primary centers for complex cardiovascular and endovascular interventions due to their access to advanced imaging infrastructure, hybrid operating rooms, and multidisciplinary interventional teams. High patient inflow for coronary artery disease, peripheral artery disease, and neurovascular conditions sustains consistent demand for balloon introducer systems. Hospitals are also early adopters of next-generation catheter technologies, supported by structured procurement processes and clinical evaluation committees. The availability of intensive care support, emergency services, and specialized interventional cardiology units further reinforces hospital dominance. While ambulatory surgical centers are gradually expanding their role in selected procedures, hospitals continue to lead due to their capacity to manage high-risk and complex cases.

Region-wise Insights

North America Balloon Introducer System Market Trends

The North America balloon introducer system market is expected to dominate globally with a value share of 48.5% in 2026, led primarily by the U.S. The region benefits from a highly developed healthcare infrastructure, widespread access to catheterization laboratories, and high procedural volumes for coronary and peripheral interventions. A strong prevalence of cardiovascular diseases, driven by aging demographics, obesity, diabetes, and sedentary lifestyles, sustains long-term demand. Favorable reimbursement frameworks for interventional cardiology procedures support early diagnosis and timely treatment, enabling rapid adoption of advanced balloon introducer technologies.

The presence of leading medical device manufacturers, robust physician training programs, and continuous clinical research activity further accelerates innovation uptake. Additionally, strong emphasis on minimally invasive procedures, outpatient catheter-based treatments, and quality outcome metrics reinforces consistent utilization across both academic and community hospital settings.

Europe Balloon Introducer System Market Trends

The Europe balloon introducer system market is expected to grow steadily, supported by an aging population and rising incidence of cardiovascular and peripheral vascular diseases. Key countries including Germany, the U.K., France, Italy, and the Nordic region contribute significantly due to well-established public healthcare systems and strong access to interventional cardiology services. Increasing adoption of standardized clinical guidelines and evidence-based treatment pathways ensures stable procedure volumes across the region.

Healthcare systems are increasingly emphasizing minimally invasive approaches to reduce hospital stays and overall treatment costs, supporting demand for balloon-based interventions. Cost-containment pressures are encouraging hospitals to adopt reliable, durable balloon introducer systems with proven clinical performance. Cross-border clinical collaborations, pan-European training initiatives, and gradual regulatory harmonization are improving technology diffusion. Together, these factors are supporting consistent, incremental growth across the European market.

Asia Pacific Balloon Introducer System Market Trends

The Asia Pacific balloon introducer system market is expected to register a relatively higher CAGR of around 7.9% between 2026 and 2033, driven by rapid healthcare infrastructure expansion and rising interventional procedure volumes. Countries such as China, India, Japan, South Korea, and Southeast Asian nations are experiencing increased diagnosis and treatment of coronary and peripheral artery diseases due to urbanization, lifestyle changes, and aging populations. Expanding access to tertiary care hospitals, growing numbers of trained interventional cardiologists, and rising healthcare expenditure are improving procedural penetration.

Government initiatives aimed at strengthening cardiac care networks and improving emergency vascular services are accelerating adoption. Additionally, medical tourism, private hospital expansion, and partnerships with global device manufacturers are enhancing technology availability. Increasing awareness of early intervention benefits and improving procedural outcomes are expected to sustain strong regional momentum.

Market Competitive Landscape

The global balloon introducer system market is highly competitive, with strong participation from companies such as Koninklijke Philips N.V., Medtronic, MicroPort Scientific Corporation, OrbusNeich Medical, and Terumo Corporation. These players benefit from broad cardiovascular and endovascular device portfolios, long-standing relationships with interventional cardiologists and vascular surgeons, advanced catheter and balloon design capabilities, and well-established global distribution networks. Competitive strategies focus on expanding balloon introducer offerings, improving trackability, pushability, and lesion-crossing performance, supporting minimally invasive interventions, and enhancing overall procedural efficiency.

Companies are also investing in clinical studies, product portfolio expansions, physician training initiatives, and geographic penetration across emerging markets. Ongoing innovation in balloon materials, coating technologies, shaft design, and compatibility with complex interventional procedures is intensifying competition and supporting continuous market evolution.

Key Industry Developments:

- In March 2025, Abbott announced that it had secured CE Mark approval in Europe for its Volt™ PFA System for the treatment of patients with atrial fibrillation (AFib). Following the earlier-than-anticipated regulatory clearance, Abbott initiated commercial pulsed field ablation procedures across select EU centers with physicians who had previously gained hands-on experience with the Volt PFA System through the company’s clinical studies. Abbott plans to progressively broaden the system’s commercial rollout across additional European markets during the second half of the year.

- In October 2022, Cordis announced the acquisition of Switzerland-based MedAlliance, a leader in drug-eluting balloon technologies, subject to customary regulatory approvals. The deal enables Cordis to expand global access to MedAlliance’s SELUTION SLR™ drug-eluting balloon, with the potential to treat up to two million patients by 2027. The transaction includes an initial $35 million investment, a $200 million payment at closing in 2023, and additional regulatory and commercial milestone payments through 2029.

Companies Covered in Global Balloon Introducer System Market

- Koninklijke Philips N.V.

- Medtronic

- MicroPort Scientific Corporation

- OrbusNeich Medical

- Terumo Corporation.

- Abbott Laboratories

- B. Braun Melsungen AG

- Becton Dickinson and Company

- Biotronik AG

- Boston Scientific Corporation

- Cardinal Health Inc.

- Cardionovum GmbH

- Concept Medical Inc.

- Cook

- Others

Frequently Asked Questions

The global balloon introducer system market is projected to be valued at US$ 3.1 Bn in 2026.

Rising prevalence of cardiovascular diseases, increasing preference for minimally invasive procedures, and expanding healthcare infrastructure globally drive the balloon introducer system market growth.

The global balloon introducer system market is poised to witness a CAGR of 5.9% between 2026 and 2033.

Technological advancements in device design, expanding applications beyond cardiology, and growing adoption in emerging markets present key opportunities for market expansion.

Koninklijke Philips N.V., Medtronic, MicroPort Scientific Corporation, OrbusNeich Medical, Terumo Corporation are some of the key players in the balloon introducer system market.