- Baby Care & Accessories

- Baby Crib Sheet Market

Baby Crib Sheet Market Size, Share, and Growth Forecast 2026 - 2033

Baby Crib Sheet Market by Product Type (Round, Mini), Material Type (Organic, Conventional), Distribution Channel (Specialty Store, Supermarket, Online Stores), Application (Household, Commercial), and Regional Analysis 2026 - 2033

Baby Crib Sheet Market Share and Trends Analysis

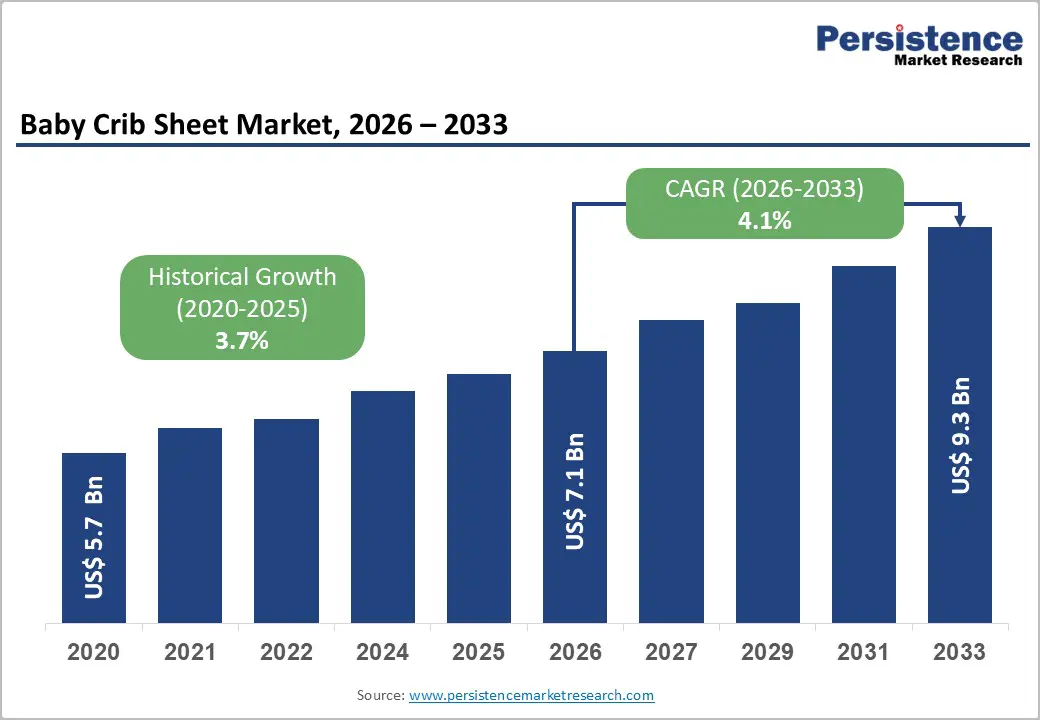

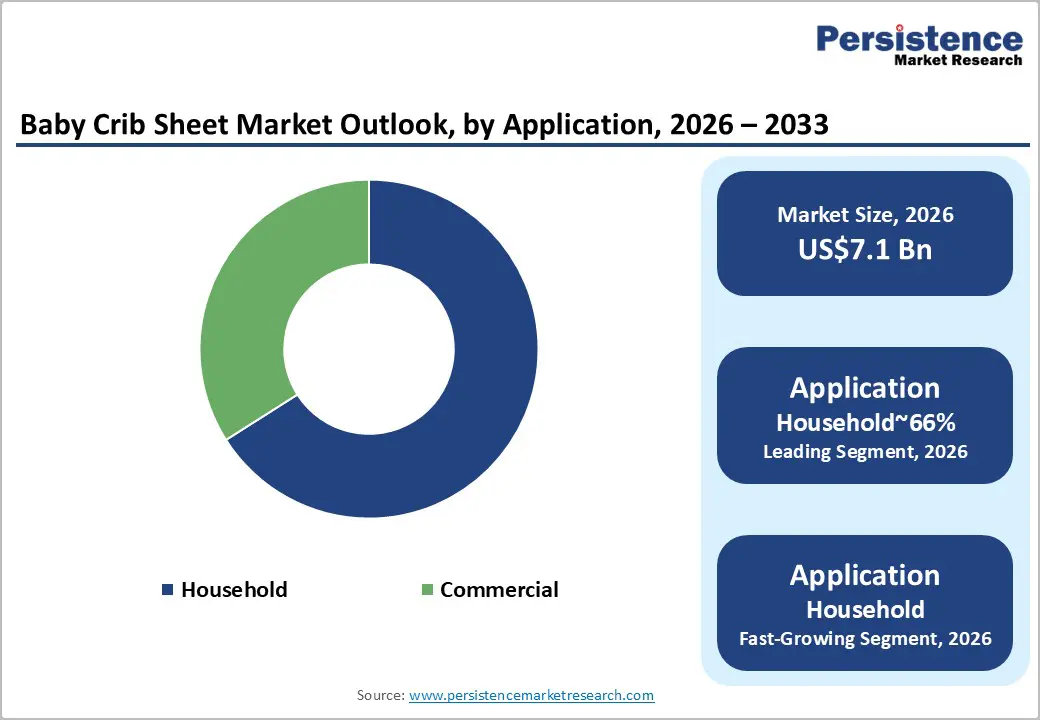

The global baby crib sheet market size is likely to be valued at US$7.1 billion in 2026 and is expected to reach US$ 9.3 billion by 2033, growing at a CAGR of 4.1% during the forecast period between 2026 and 2033, driven by the increasing urbanization in emerging economies, which has led to a rise in nuclear family structures and a corresponding demand for specialized nursery products.

The growing awareness among parents of infant safety and comfort, along with the shift toward organic and non-toxic materials, are key factors contributing to market expansion. The rapid rise of e-commerce platforms has also played a significant role, providing wider access to premium organic and niche crib sheet options, such as round and mini variations, especially in regions experiencing growth in the middle-class population.

Key Industry Highlights:

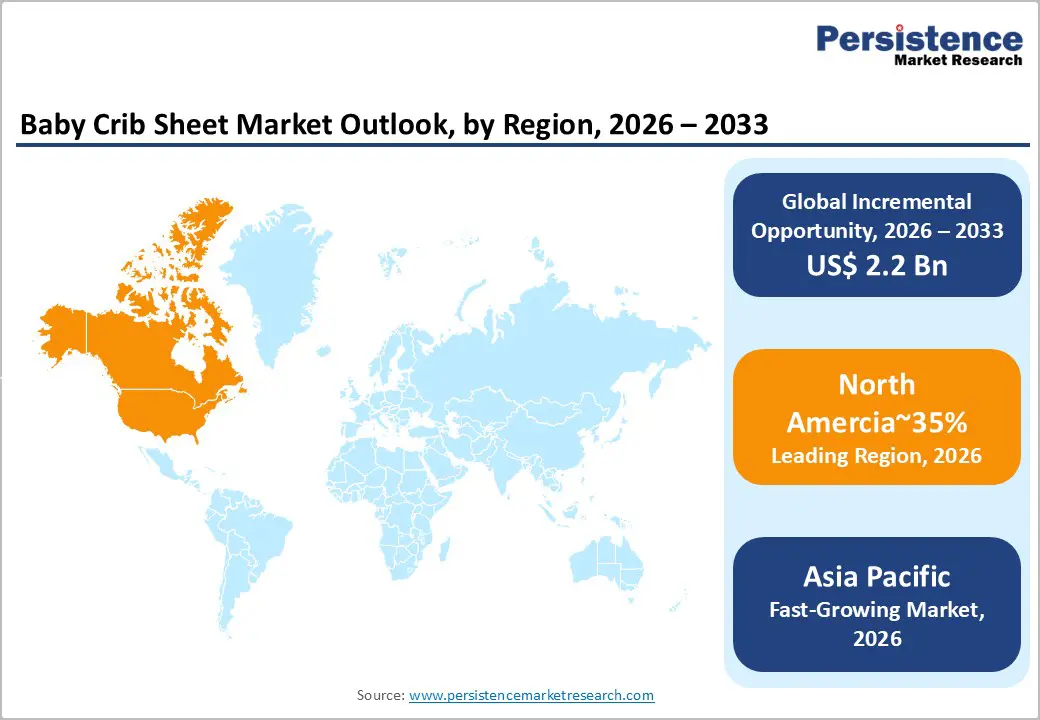

- Leading Region: North America is expected to be the leading market, accounting for 35% of the market, supported by high disposable incomes, strong preference for premium baby products, and widespread adherence to safety and quality certifications. Mature retail infrastructure and brand loyalty further reinforce regional dominance.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing region, driven by rapid urbanization, rising middle-class households, and increasing penetration of organized baby care retail, particularly across major emerging economies.

- Fastest-growing Product Type: Round crib sheets make up 52% of the market share, highlighting their dominance in the market. They are also expected to be the fastest-growing subsegment, driven by a strong alignment between functional safety needs and parents' desire to minimize risks for their infants.

- Fastest-growing Application: Household applications are expected to account for 66% of total demand and represent the fastest-growing segment, underscoring their strong presence in residential infant care.

- Key Industry Developments: The industry is undergoing active consolidation through strategic acquisitions, alongside intensified competition in safety certifications, material transparency, and sustainability credentials, rather than on price. In July 2024, Crown Crafts, Inc. acquired Baby Boom Consumer Products. The merger unites a leader in toddler bedding with Crown Crafts’ expansive nursery portfolio, creating a dominant force in the crib sheet and accessory market through consolidated distribution and design expertise.

| Key Insights | Details |

|---|---|

|

Baby Crib Sheet Market Size (2026E) |

US$7.1 Bn |

|

Market Value Forecast (2033F) |

US$9.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.7% |

Market Dynamics - Drivers, Barriers, and Opportunities

Rising Parental Emphasis on Infant Health and Sleep Safety Standards

Contemporary parental behavior is undergoing a structural shift toward evidence-based infant care, reinforced by heightened awareness of sleep-related safety risks and institutional guidance. Regulatory bodies and pediatric associations have intensified scrutiny around safe sleep environments, repositioning infant bedding from a discretionary purchase to a compliance-driven necessity. This regulatory reinforcement has materially elevated consumer sensitivity to certification, material safety, and fit integrity, particularly as safe sleep protocols gain wider penetration through clinical guidance and public education channels. As a result, certified crib sheets increasingly function as risk-mitigation tools rather than lifestyle accessories, supporting sustained baseline demand even in cost-conscious households.

Concurrently, behavioral normalization of sleep-focused parenting is reinforcing repeat-purchase dynamics within the category. High-frequency laundering driven by hygiene standards and infant care routines structurally increases per-household consumption volumes, supporting premiumization without proportional volume elasticity. Digital parenting ecosystems and pediatric-led messaging continue to amplify expectations around comfort, breathability, and material performance during prolonged infant sleep cycles. Together, these forces are compressing tolerance for non-certified alternatives while favoring manufacturers with regulatory alignment, material traceability, and scalable compliance capabilities.

Declining Birth Rates in Developed Economies

Declining fertility rates across developed economies represent a structural restraint on the baby crib sheet market, compressing long-term volume expansion despite rising per-child expenditure. Demographic contraction in North America, Europe, and parts of East Asia is steadily reducing the absolute pool of new infant households, limiting replenishment-driven growth for standardized crib bedding. This demographic headwind weakens scale economics for mass-market manufacturers, intensifies competition for a shrinking consumer base, and shifts value creation toward differentiation, deeper certification, and premium positioning rather than unit-volume growth.

In countries such as Japan and South Korea, birth rates reached record lows in 2024-2025. This demographic inflection is accelerating strategic realignment across the value chain, with manufacturers reallocating capital toward higher-margin organic materials, design-led premium assortments, and adjacent age-category extensions. While premiumization partially offsets declining birth volumes, it does not fully offset structural demand erosion, reinforcing uneven market outcomes in which scale, brand trust, and compliance capabilities increasingly determine resilience.

Expansion into the "Smart Nursery" Ecosystem

The convergence of infant care products with connected-home and digital health technologies is opening a structurally attractive avenue for value expansion. As parental expectations evolve toward continuous, data-supported reassurance, passive monitoring solutions that operate without direct skin contact are gaining conceptual and commercial relevance. Textile-based platforms that capture physiological and environmental indicators integrate seamlessly into daily infant care routines, reducing friction associated with wearable devices while reinforcing safety and comfort priorities. This alignment positions connected bedding solutions as a natural extension of evidence-led parenting rather than a discretionary technology add-on.

From a market-structure perspective, this evolution favors participants capable of bridging traditional manufacturing with software-enabled service delivery. Collaboration between material specialists and health-technology providers enables premium positioning, recurring engagement models, and deeper consumer stickiness through analytics-driven insights. The embedded data layer strengthens brand trust, supports iterative product refinement, and elevates switching costs over time. Commercialization is contingent on disciplined execution across sensor reliability, data governance, and regulatory alignment, creating meaningful entry barriers. As smart nursery adoption scales, entities with integration capabilities, deep compliance, and ecosystem partnerships are positioned to capture outsized economic value in this emerging demand vector.

Category-wise Analysis

Product Type Insights

Round crib sheets are expected to be the leading and fastest-growing product subsegment in the baby crib sheet market, accounting for approximately 52% of specialized and non-standard demand. This leadership is expected to be reinforced by the continued premiumization of nursery furniture and the rising adoption of round and oval crib formats such as the Stokke Sleepi, Babyletto Gelato, and DaVinci Kalani conversions. Demand is likely to remain concentrated among urban, design-conscious households that prioritize safety-enhancing geometries, seamless 360-degree access, and boutique nursery aesthetics. Sheet manufacturers such as SheetWorld, Newton Baby, and Aden + Anais are increasingly aligning product development toward high-tension elastic engineering, organic-certified fabrics, and temperature-regulating textiles tailored specifically for circular mattresses. Regulatory tightening around snug-fit compliance for non-full-size cribs is expected to further consolidate demand toward branded, certified round sheets, reinforcing this segment’s premium and growth-oriented positioning.

Mini crib sheets are expected to hold the remaining 48% share and sustain strong volume relevance as the primary alternative format, supported by urban micro-living and portable sleep adoption. This segment is likely to benefit from the growing use of mini cribs as secondary or transitional sleep solutions, particularly in apartments, travel settings, and shared caregiving environments. Brands such as Graco, Halo, American Baby Company, and Burt’s Bees Baby are anticipated to maintain momentum through multi-pack offerings, universal-fit stretch designs, and easy-care fabric blends optimized for frequent laundering. Product innovation is increasingly focused on super-stretch elastics, breathable constructions, and antimicrobial finishes suited for mobile use cases. While growth is expected to be steadier than round formats, mini crib sheets are likely to remain structurally important due to affordability, portability, and compatibility with convertible nursery systems.

Application Insights

Household applications are expected to be the leading and fastest-growing segment in the baby crib sheet market, accounting for approximately 66% of total demand in 2026. The household segment dominates, as crib sheets are essential, high-frequency-use products for parents managing daily infant care routines. Most households maintain multiple sheets to accommodate frequent washing cycles driven by spills, hygiene needs, and comfort preferences. Rising nuclear family structures and urban living patterns are increasing per-child spending on dedicated nursery products. Parents are prioritizing premium materials such as organic cotton and hypoallergenic fabrics to reduce health risks. Visual appeal and nursery personalization are also shaping purchasing behavior across income segments. As a result, household demand combines volume stability with strong value growth dynamics.

The commercial segment, including hospitals, clinics, daycare centers, and select hospitality providers, is expected to hold nearly 34% share in 2026. Demand is driven by institutional hygiene standards and the need for durable, easy-to-launder bedding products. Hospitals and clinics focus on medical-grade quality and bulk procurement efficiency. Daycare centers contribute incremental demand due to higher enrollment among working parents. Hospitality adoption remains niche but supports premium positioning. Overall growth in this segment is steady and operationally driven rather than preference-led.

Regional Insights

North America Baby Crib Sheet Market Trends

North America is projected to be the leading region in the baby crib sheet market, accounting for around 35% of total revenue. This dominance is driven by a mature demand base and stringent regulatory standards, particularly those set by the U.S. Consumer Product Safety Commission regarding fit, flammability, and material certification. These regulations influence both product specifications and consumer purchasing decisions. The region’s well-developed retail infrastructure, which includes both established specialty chains and direct-to-consumer (D2C) platforms, supports widespread availability of premium and certified products.

Key demand drivers in North America include a preference for sustainable materials, personalized shopping experiences, and the integration of connected nursery technologies, all of which contribute to ongoing market growth and stable pricing. Regulatory oversight, combined with high disposable income, promotes the adoption of organic and certified products, making the region a benchmark for global market standards. Advanced infrastructure and digital retail channels also enable the rapid introduction of innovative products, such as sensor-integrated and design-optimized crib sheets. Although overall volume growth is moderate due to market saturation, North America remains strategically important for premium product offerings, brand positioning, and showcasing compliance-driven product differentiation compared to other regions.

Europe Baby Crib Sheet Market Trends

Europe is likely to be a mature market for baby crib sheets, with Western European countries, especially Germany, the U.K., France, and Spain, dominating regional revenue. This is due to a well-established retail infrastructure, high disposable incomes, and environmentally conscious consumer behavior. Germany alone accounts for about 25% of the region’s demand, driven by a strong manufacturing base and high adoption of premium, eco-certified products. The market is fragmented, with both heritage brands and international players competing on compliance, design, and sustainability credentials. Regulatory alignment through the European Committee for Standardization, along with REACH chemical regulations, reinforces a preference for non-toxic, durable, and certified bedding, ensuring premium market positioning and steady revenue streams.

Sustainability remains a key driver for the adoption of organic and certified materials, with Western European products capturing a significant portion of the market. Consumers' focus on eco-certifications, hypoallergenic features, and material traceability creates high barriers to entry for smaller players, benefiting established manufacturers with strong compliance capabilities. Central and Eastern Europe constitute emerging growth markets, supported by rising disposable incomes, expanding retail networks, and increasing demand for premium products. The region's growth trajectory is shaped by a mix of regulatory enforcement, eco-driven demand, and the need for advanced production infrastructure.

Asia Pacific Baby Crib Sheet Market Trends

Asia Pacific is the fastest-growing region in the baby crib sheet market, with a current market share of approximately 25%, reflecting structural expansion driven by rapid urbanization, a growing middle class, and increasing parental investment in infant care products. Market growth is reinforced by rising premiumization, adoption of organic and designer crib sheets, and accelerating digital retail penetration that facilitates broad consumer access. Structural manufacturing advantages, including raw material availability and labor efficiency, enable competitive pricing for both domestic consumption and export. Technology integration in nursery products, such as sensor-enabled bedding, further supports differentiated demand and strengthens adoption among digitally native parents, positioning the region for sustained value growth.

Emerging markets in the Asia-Pacific region, including India and Southeast Asian countries, continue to expand rapidly due to low penetration of organized retail, rising urbanization, and greater e-commerce accessibility. Growth is driven by both affordable, accessible product offerings for value-conscious consumers and premiumization targeting affluent urban households. Supply chain efficiency, localized product customization, and the expansion of retail infrastructure reinforce the region’s ability to capture both volume and value simultaneously. Policy support, infrastructural development, and growing awareness of certified and sustainable materials collectively sustain Asia Pacific’s trajectory as a structurally high-growth and opportunity-rich market.

Competitive Landscape

The global baby crib sheet market is moderately fragmented, with the top 10 players including Carter’s, Artsana Group, and Newell Brands holding approximately 30–35% of the total market share. Market concentration is higher among certified organic and premium material segments, while a diverse set of local manufacturers and niche DTC brands occupy the remainder, creating a competitive landscape driven by product differentiation rather than pricing.

Competitive positioning emphasizes material certifications such as GOTS and OEKO-TEX, design exclusivity, and enhanced breathability technologies. Smaller entrants compete through agility, specialized organic offerings, and direct-to-consumer channels, while leading players leverage brand recognition, distribution scale, and innovation in fabric technologies. Future market dynamics are expected to prioritize sustainable materials, advanced textile performance features, and digitally enabled customization, reinforcing barriers for new entrants and sustaining premium positioning for established global brands.

Key Industry Developments:

- In May 2025, Beyond Inc. relaunched buybuy BABY online with a grand reopening, tapping into its vast existing customer base and hosting a "Baby Days" digital event to aggressively capture market share in the nursery furniture and crib sheet sectors through rapid e-commerce growth.

- In October 2024, Millennium Babycares secured US$14.5 million in funding from Bharat Value Fund, which it will use to expand its manufacturing capabilities and increase the availability of high-quality domestic crib sheets in emerging markets.

- In July 2024, SIJO launched its GOTS-certified LuxeSoft Sateen Cotton Bedding Collection, addressing the growing demand for ultra-breathable, non-toxic materials and building consumer trust with its high-thread-count sateen finish for infant sleep surfaces.

Companies Covered in Baby Crib Sheet Market

- Carter’s Inc.

- Artsana S.p.A.

- Newell Brands

- Delta Children

- Burt's Bees Baby

- MeeMee

- The Pipal India

- Naturalmat USA

- Aden + Anais

- Stokke AS

- The Honest Company

- Pottery Barn Kids (Williams-Sonoma)

- Liz and Roo

- BabyBjörn AB

- Little Unicorn

Frequently Asked Questions

The global baby crib sheet market is projected to be valued at US$7.1 billion in 2026 and is expected to reach US$9.3 billion by 2033, supported by a steady demand for infant bedding essentials and premium baby products.

Demand is rising due to heightened parental focus on infant safety and comfort, increasing preference for certified and eco-friendly materials, and growing awareness of sleep quality and hygiene for newborns and toddlers.

The baby crib sheet market is expected to grow at a CAGR of 4.1% between 2026 and 2033, reflecting stable expansion driven by product premiumization and organized retail growth.

The fastest growth opportunities are emerging in Asia Pacific, supported by rapid urbanization, rising middle-class households, and increasing penetration of organized and online baby care retail channels.

Key players include Carter’s Inc., Artsana S.p.A., Newell Brands, Delta Children, Burt’s Bees Baby, MeeMee, The Pipal India, Aden + Anais, Stokke AS, The Honest Company, Pottery Barn Kids, BabyBjörn AB, and Little Unicorn.