- Automotive Components & Materials

- Automotive Transfer Case Market

Automotive Transfer Case Market Size, Share, and Growth Forecast, 2025 - 2032

Automotive Transfer Case Market by Vehicle Outlook (ICE Vehicles, Hybrid Vehicles and Off Highway Vehicles), by Drive (Gear Driven and Chain Driven), by Shift Type (Manual Shift on the Fly (MSOF) and Electronic Shift on the Fly (ESOF)), and Regional Analysis for 2025 - 2032

Automotive Transfer Case Market Size and Trends Analysis

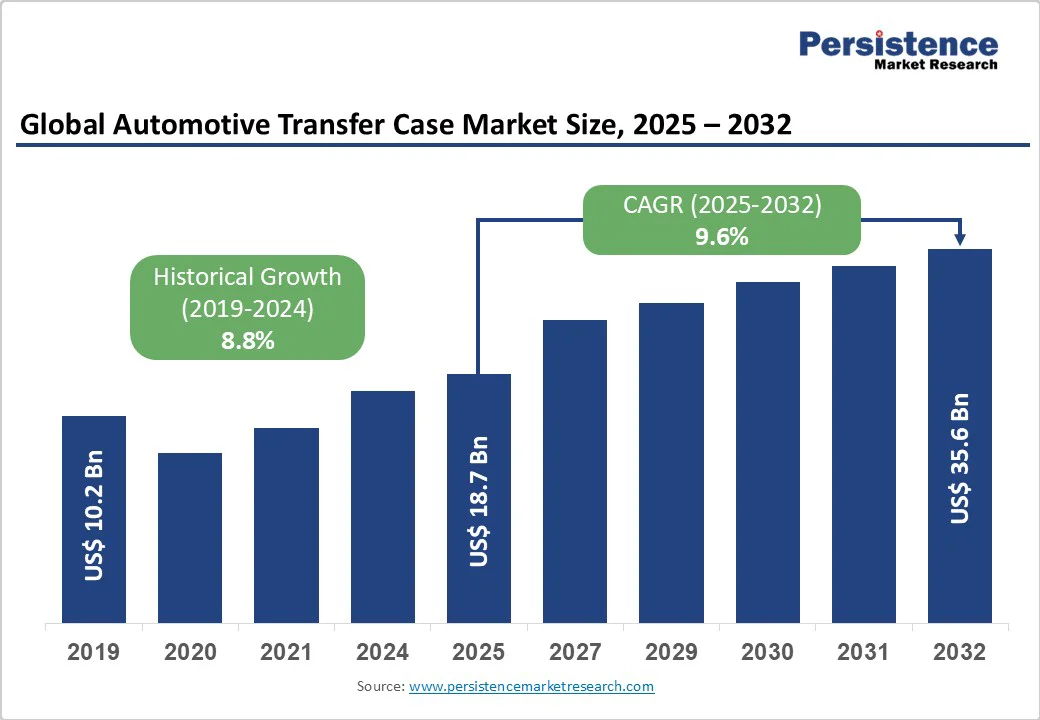

The global automotive transfer case market size is likely to value US$ 18.7 billion in 2025 and is projected to reach US$ 35.6 billion by 2032, growing at a CAGR of 9.6% between 2025 and 2032.

The market expansion is driven by automotive electrification trends, enhanced fuel efficiency requirements, and growing adoption of electronic control systems enabling seamless power distribution between vehicle axles.

Key Industry Highlights:

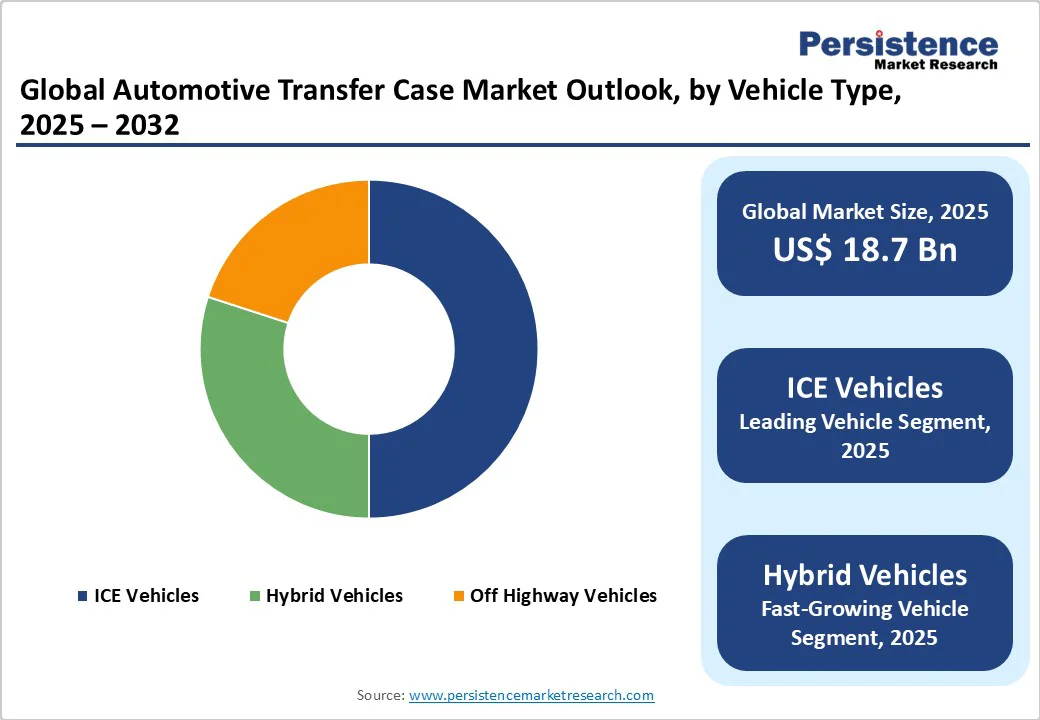

- Vehicle Segments: Internal Combustion Engine (ICE) vehicles dominate the market with a 42.4% share in 2025, driven by their established infrastructure, mature supply chains, and widespread global adoption. Hybrid vehicles represent the fastest-growing segment, supported by stringent emission regulations, fuel efficiency requirements, and the transition toward low-emission mobility solutions integrating both electric and conventional powertrains.

- Technology Segments: Chain-driven systems maintain a commanding 63.7% share, favored for their cost-effectiveness, durability, and reduced noise levels in mass-market vehicles. Gear-driven systems exhibit the fastest growth, propelled by rising demand in heavy-duty and high-performance applications where superior torque handling and reliability are essential.

- Control System Segments: Manual Shift-on-the-Fly (MSOF) systems hold a dominant 58.4% share, valued for their reliability, simplicity, and affordability across light trucks and SUVs. Meanwhile, Electronic Shift-on-the-Fly (ESOF) systems are the fastest-growing, projected to expand at a 12.3% CAGR, driven by increasing consumer preference for automation, comfort, and enhanced vehicle control.

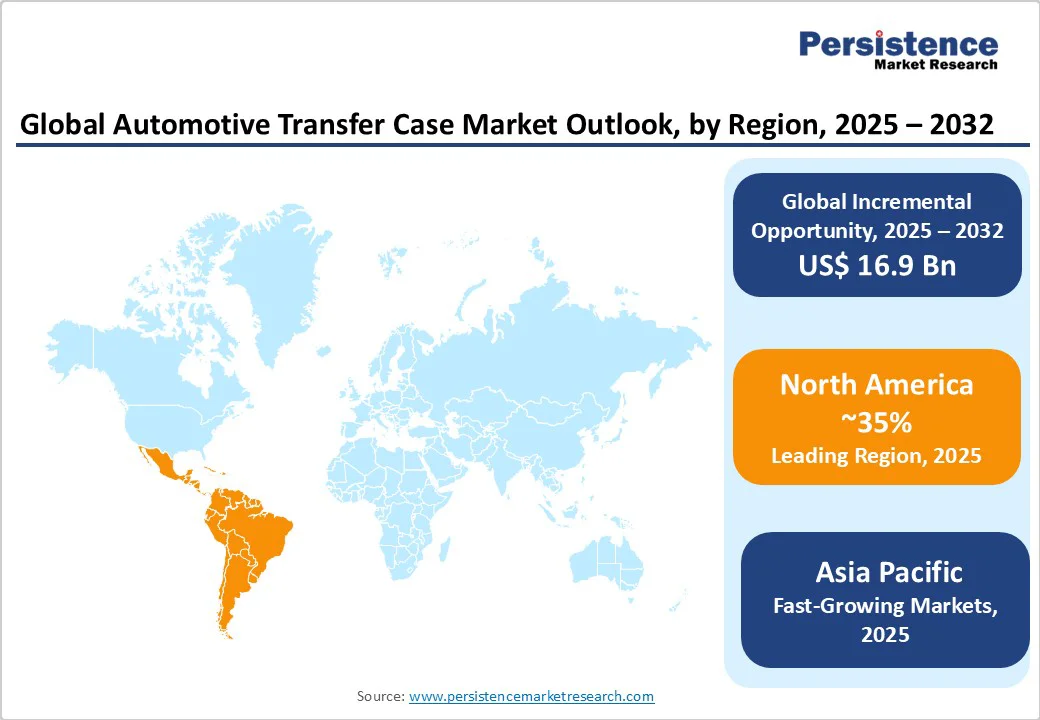

- Regional Leaders: North America leads the global market with a 35% share (valued at US$ 6.5 billion in 2025), supported by strong SUV and pickup truck demand, advanced manufacturing infrastructure, and off-road vehicle popularity. Asia Pacific is the fastest-growing region, projected to grow at an 11.2% CAGR, fueled by rapid automotive production expansion, rising vehicle ownership, and growing demand for all-wheel-drive systems in emerging markets.

- Technology Developments: The market is witnessing transformation through AI-powered torque distribution, predictive engagement systems, and electrification-compatible drivetrain architectures. These advancements enhance performance, safety, and energy efficiency, enabling the evolution of intelligent, adaptive transfer cases aligned with next-generation mobility trends.

- Strategic Market Developments: Leading players are focusing on innovation and global expansion, highlighted by BorgWarner’s US$ 200 million EV partnership in China, Magna’s launch of the intelligent iAWD system, and ZF’s US$ 450 million acquisition aimed at strengthening its electrified powertrain portfolio. These develop ents underscore the industry’s commitment to electrification, automation, and strategic consolidation.

| Key Insights | Details |

|---|---|

| Automotive Transfer Case Market Size (2025E) | US$ 18.7 Bn |

| Market Value Forecast (2032F) | US$ 35.6 Bn |

| Projected Growth (CAGR 2025 to 2032) | 9.6% |

| Historical Market Growth (CAGR 2019 to 2024) | 8.8% |

Market Dynamics

Drivers - Surging Global Demand for SUVs and AWD/4WD Vehicles

The worldwide shift toward SUV adoption represents the primary growth catalyst for the transfer case market, with SUV sales accounting for over 50% of total vehicle sales in key markets including the United States.

According to the International Organization of Motor Vehicle Manufacturers (OICA), global SUV production reached 35.2 million units in 2023, representing a 12% increase from the previous year. The Asia-Pacific region demonstrates particularly strong SUV demand, with China's SUV market expanding at 15% annually through 2024, directly correlating with transfer case requirements.

Consumer preference for vehicles capable of handling diverse terrains and weather conditions drives sustained demand for AWD systems, with over 48.6% of new vehicles sold in North America featuring AWD capabilities as of 2023. The premium vehicle segment's increasing adoption of AWD as standard equipment further amplifies market growth, as luxury automakers position all-wheel drive as essential safety and performance technology.

Technological Advancement and Electronic System Integration

The automotive industry's transition toward sophisticated electronic control systems transforms traditional mechanical transfer cases into intelligent, software-controlled components capable of real-time torque distribution optimization.

Electronic Shift-on-the-Fly (ESOF) technology adoption accelerates at 12.3% CAGR through 2032, driven by consumer demand for seamless drivetrain operation and improved fuel efficiency. Advanced transfer cases incorporating predictive algorithms, sensor integration, and automated engagement capabilities enhance vehicle performance while reducing driver workload.

According to industry surveys, electronically controlled transfer cases improve fuel economy by 8-12% compared to traditional mechanical systems through precise power management and reduced parasitic losses. The integration of transfer cases with vehicle stability control, traction management, and autonomous driving systems creates additional value propositions supporting premium pricing and market expansion.

Restraints - High Development and Manufacturing Costs

The complexity of modern transfer case systems, particularly those incorporating electronic controls and smart technologies, results in substantial development and manufacturing expenses that constrain market accessibility.

Advanced ESOF systems require significant investment in research and development, specialized manufacturing equipment, and quality assurance processes, with development costs often exceeding $50 million for next-generation platforms. Raw material price volatility affects production costs, with steel and aluminum price fluctuations impacting manufacturing expenses by 15-20% annually.

The integration of electronic components, sensors, and control modules increases system complexity and unit costs, making advanced transfer cases less viable for budget vehicle segments where price sensitivity remains paramount. Supply chain disruptions and semiconductor shortages further compound cost pressures, affecting production schedules and inventory management.

Supply Chain Vulnerabilities and Integration Complexity

The automotive transfer case industry faces persistent supply chain challenges, including component shortages, logistics disruptions, and geopolitical tensions affecting global manufacturing networks. Semiconductor availability constraints impact electronic transfer case production, with delivery delays extending 12-16 weeks beyond normal lead times as of 2024.

The complexity of integrating modern transfer cases with existing vehicle architectures creates engineering challenges, particularly for retrofitting applications and legacy platform upgrades. Manufacturing capacity constraints limit production scaling capabilities, while quality control requirements for safety-critical drivetrain components necessitate extensive testing and validation processes.

Geographic concentration of specialized component suppliers creates vulnerability to localized disruptions, affecting global supply chain stability and market growth potential.

Opportunity - Emerging Market Expansion and Infrastructure Development

Developing economies in Asia-Pacific, Latin America, and Africa present substantial growth opportunities, with automotive production in these regions projected to increase 8.3% annually through 2032. Countries including India, Brazil, and Indonesia are experiencing rising disposable incomes and infrastructure development supporting increased vehicle ownership and SUV adoption.

Government initiatives promoting automotive manufacturing and foreign direct investment create favorable conditions for transfer case demand expansion. Rural and semi-urban areas in emerging markets demonstrate growing preference for AWD vehicles due to challenging road conditions and infrastructure limitations, creating new market segments for transfer case applications. The addressable market in emerging economies represents approximately $8.7 billion in additional opportunity through 2032.

Aftermarket Growth and Service Innovation

The expanding global vehicle fleet creates substantial aftermarket opportunities for transfer case replacement, upgrade, and maintenance services, with the global automotive aftermarket valued at $485 billion in 2024. Average transfer case service life ranges from 100,000 to 150,000 miles, ensuring consistent replacement demand across aging vehicle populations.

The trend toward vehicle customization and performance enhancement drives aftermarket demand for upgraded transfer cases offering improved capabilities and electronic controls. Service digitization and predictive maintenance technologies enable proactive transfer case monitoring and replacement scheduling, creating new revenue streams for manufacturers and service providers. The aftermarket segment represents approximately 35% of total transfer case market value by 2032.

Segmentation Analysis

Vehicle Outlook Analysis - ICE Vehicles Market Leadership

Internal Combustion Engine (ICE) vehicles dominate the transfer case market with a 42.4% share, supported by established manufacturing infrastructure and widespread adoption across SUVs, trucks, and commercial vehicles. These systems deliver high torque capacity, durability, and reliability essential for off-road and heavy-duty applications. The segment benefits from mature supply chains, standardized production, and strong aftermarket networks ensuring long-term market stability.

Hybrid vehicles represent the fastest-growing segment, propelled by stringent emission regulations and increasing demand for fuel-efficient powertrains. Hybrid transfer cases enable seamless coordination between electric motors and internal combustion engines, optimizing torque distribution and regenerative braking. Supported by government incentives and OEM investments in electrified platforms, this segment continues to expand rapidly through innovations in power management and lightweight drivetrain design.

Drive Type Analysis - Chain Driven Systems Dominance

Chain-driven transfer cases dominate the market with a commanding 63.7% share, attributed to their superior power transmission efficiency, compact design, and cost-effective manufacturing. These systems deliver smooth torque transfer with reduced noise and vibration, ensuring reliability across diverse driving conditions. The segment’s growth is supported by mature manufacturing processes, extensive OEM integration, and long service life, making chain systems the preferred choice for mass-market SUVs and light-duty vehicles.

Gear-driven transfer cases represent the fastest-growing segment, driven by rising demand for heavy-duty and high-performance vehicles requiring exceptional torque capacity and durability. Advances in precision engineering, materials technology, and gear design have enhanced system strength, reduced weight, and improved operational efficiency. Their superior control response and robustness make gear-driven systems increasingly attractive for commercial and off-road applications.

Shift Type Analysis - Manual Shift on the Fly (MSOF) Market Leadership

Manual Shift on the Fly (MSOF) systems dominate the market with a 58.4% share, driven by their cost-effectiveness, mechanical simplicity, and reliability in demanding environments. These systems provide drivers with direct control over transfer case engagement, ensuring predictable performance and ease of maintenance. MSOF technology remains favored in off-road, heavy-duty, and commercial applications where operator control and durability outweigh automation needs. Established service infrastructure and lower manufacturing costs further strengthen segment leadership.

Electronic Shift on the Fly (ESOF) systems represent the fastest-growing segment, expanding at a 12.3% CAGR through 2032. Growth is fueled by rising consumer preference for convenience, automation, and vehicle system integration. ESOF systems enable seamless engagement, optimize torque distribution, and integrate with stability and terrain response systems, supporting advanced driver-assistance and smart vehicle functionalities.

Regional Market Insights

North America Market Analysis

North America holds a dominant 35% share of the global automotive transfer case market, valued at USD 6.5 billion in 2025 and projected to reach USD 12.5 billion by 2032. The U.S. drives regional demand, supported by robust SUV and pickup truck sales, which account for over 70% of new vehicle purchases. The region benefits from mature manufacturing infrastructure, high consumer purchasing power, and a strong preference for AWD vehicles. Major automakers such as Ford, General Motors, and Stellantis are key demand contributors.

Regulatory frameworks like CAFE standards encourage fuel-efficient and low-emission technologies, fostering innovation in intelligent, lightweight, and electrification-compatible transfer cases. Continued R&D investment in smart control systems and advanced materials positions North America as a global hub for transfer case design and production excellence.

Europe Market Analysis

Europe accounts for 25% of the global automotive transfer case market, valued at USD 4.7 billion in 2025 and projected to reach USD 8.9 billion by 2032. Growth is fueled by premium vehicle production, stringent emission regulations, and strong demand for AWD-equipped models. Germany leads the region, supported by luxury OEMs such as BMW, Mercedes-Benz, and Audi, which integrate advanced drivetrain systems across their lineups.

The region’s engineering excellence, manufacturing sophistication, and EU carbon-neutrality goals promote investment in lightweight, efficient, and electrification-ready transfer cases. Key markets Germany, U.K., and France benefit from strong export activity and domestic SUV demand. Leading players like ZF Friedrichshafen and Continental drive innovation through hybrid-compatible systems, intelligent control technologies, and sustainable material advancements aligned with Europe’s green mobility transition.

Asia Pacific Market Analysis

Asia Pacific stands as the fastest-growing automotive transfer case market, expanding at a CAGR of 11.2% through 2032, driven by surging automotive production and rising SUV demand across China, India, and ASEAN countries. The region’s cost-efficient manufacturing base, large domestic markets, and government-backed industrial programs strengthen its competitive position. China leads regional output with over 12 million SUVs produced in 2024, while India’s growing middle class and infrastructure investments further stimulate demand.

Japan and South Korea contribute through advanced hybrid transfer case and electronic control technologies, fostering innovation. The market features international OEMs and regional players expanding through technology partnerships, local manufacturing, and electrification-ready designs. Rising investment in smart mobility and EV integration supports Asia Pacific’s continued market leadership and technological advancement.

Competitive Landscape

The global automotive transfer case market exhibits moderate concentration with leading players maintaining significant positions through comprehensive product portfolios, established OEM relationships, and technological capabilities.

BorgWarner Inc. commands approximately 22% market share through innovation leadership and strategic partnerships with major automakers, while Magna International Inc. holds 18% share leveraging integrated manufacturing capabilities and global presence. ZF Friedrichshafen AG, American Axle & Manufacturing, and JTEKT Corporation maintain strong positions through specialized engineering expertise and comprehensive drivetrain solutions.

The market structure includes multinational corporations, specialized component manufacturers, and regional players competing across different technology segments and geographic markets.

Key Industry Developments:

- In Jan 2024, BorgWarner revealed a comprehensive electric propulsion system, integrating motor, power electronics, and battery components to optimize efficiency in electric vehicles. This development reflects BorgWarner's collaborative approach, leveraging extensive research and strategic partnerships to deliver cutting-edge solutions tailored to the evolving demands of electric mobility.

- In February 2024, With Mahindra & Mahindra having been granted permission to use the trademark "Scorpio X," it is quite probable that the company will soon introduce its pickup truck to the Indian market. It seems that a production model that is based on the Scorpio N model will soon be released, as indicated by this action.

Companies Covered in Automotive Transfer Case Market

- BorgWarner Inc.

- Magna International Inc.

- American Axle & Manufacturing, Inc.

- JTEKT Corporation

- Schaeffler AG

- ZF Friedrichshafen AG

- Melrose Industries PLC (GKN Ltd)

- Aisin Corporation

- Dana Incorporated

- Divgi TorqTransfer Systems Limited

- Others Key Players

Frequently Asked Questions

The Automotive Transfer Case market is estimated to be valued at US$ 18.7 Bn in 2025.

The key demand driver for the Automotive Transfer Case market is the rising global demand for SUVs, pickup trucks, and off-road vehicles, which require advanced drivetrain systems to enhance traction, stability, and performance across diverse terrains.

In 2025, the North America region will dominate the market with an exceeding 35% revenue share in the global Automotive Transfer Case market.

Among the Vehicle Type, ICE Vehicles holds the highest preference, capturing beyond 42.4% of the market revenue share in 2025, surpassing other vehicle type.

The key players in the Automotive Transfer Case are BorgWarner Inc., Magna International Inc., JTEKT Corporation and Schaeffler AG.