- Automotive Components & Materials

- Automotive Switch Market

Automotive Switch Market Size, Share, and Growth Forecast 2026 - 2033

Automotive Switch Market by Application (Steering Wheel Switches, Door Panels, Roof Modules, Function Switches, Climate & Comfort Controls, Infotainment & Multimedia Controls, Gear Shifts and Seat Controls) Sales Channel (OEM and Aftermarket) Vehicle Type (Passenger vehicles, Light Commercial Vehicles, and Heavy Commercial Vehicles) and Regional Analysis for 2026 - 2033

Automotive Switch Market Share and Trends Analysis

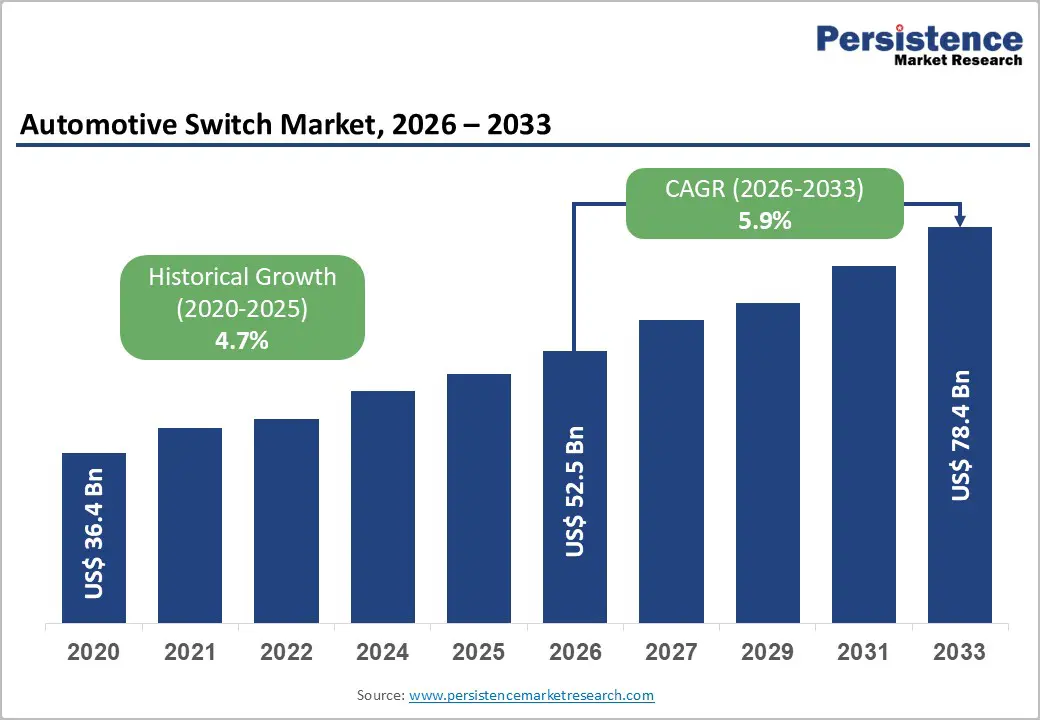

The global automotive switch market size was valued at US$ 52.5 Bn in 2026 and is projected to reach US$ 78.4 Bn by 2033, growing at a CAGR of 5.9% between 2026 and 2033.

Market growth is driven by rising demand for vehicle electrification, increasing integration of Advanced Driver Assistance Systems (ADAS), and the growing complexity of modern vehicle interiors. Vehicles are shifting from mechanical switches to sophisticated electronic control systems, with mid-class vehicles expected to feature more than 200 sensors by 2026 to support driver-assistance systems.

Key Industry Highlights:

- Leading Region: Asia Pacific dominates the automotive switch market with approximately 40% global market share, driven by exceptional vehicle production volumes in China, Japan, India, and ASEAN countries, combined with rapid EV adoption and manufacturing cost advantages supporting regional supply chain expansion.

- Fastest-Growing Region: Europe automotive switch market exhibits fastest regional growth at 8.1% CAGR through 2033, driven by accelerating passenger car sales, rising middle-class disposable income, and feature integration in mass-market vehicle segments supported by expanding EV adoption at 10.1% CAGR.

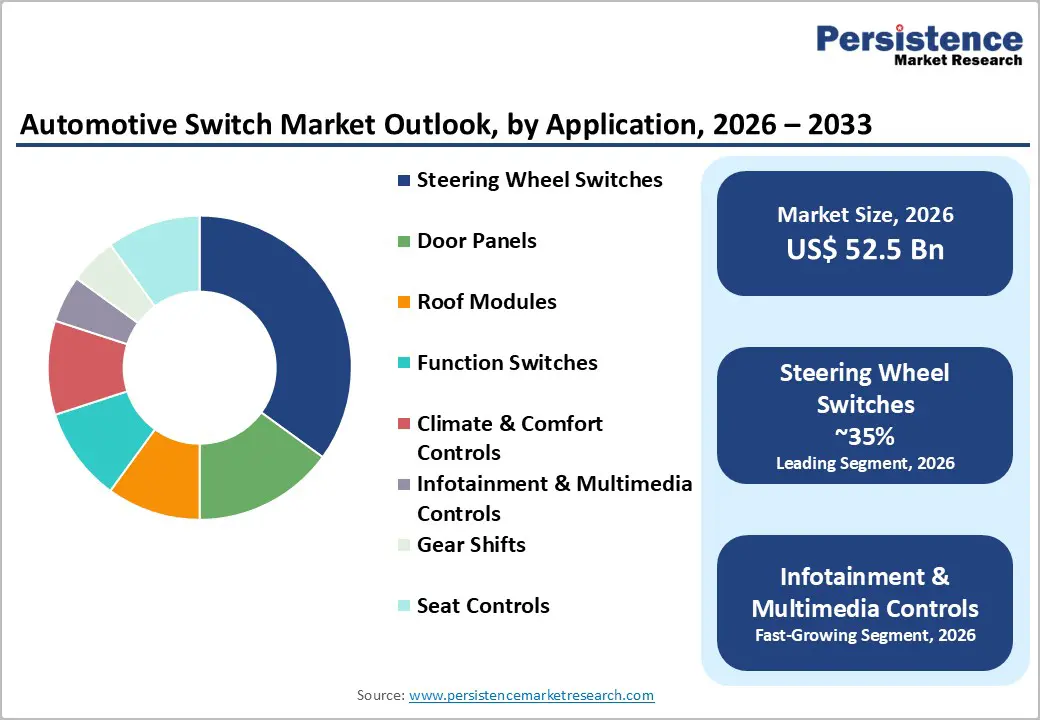

- Dominant Segment: Steering wheel switches command approximately 35% application segment share, reflecting critical role in modern vehicle design and regulatory mandates for ADAS engagement controls, with OEM adoption rates reaching 64% in premium vehicle segments.

- Fastest Growing Segment: Infotainment and multimedia control switches represent the fastest-growing application subsegment, expanding at 2.5% CAGR, driven by consumer demand for seamless connectivity, personalized driving experiences, and integration with advanced digital cockpit systems in passenger vehicles.

- Key Market Opportunity: The automotive smart surfaces and integrated controls market presents a significant opportunity, projected to reach US$ 20.82 Bn by 2036 at a 14.1% CAGR, driven by premium vehicle demand for minimalist interior designs, manufacturing efficiency gains from component consolidation, and consumer preference for digitally enhanced cabin experiences.

| Key Insights | Details |

|---|---|

| Automotive Switch Market Size (2026E) | US$ 52.5 Bn |

| Market Value Forecast (2033F) | US$ 78.4 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.9% |

| Historical Market Growth (CAGR 2020 to 2024) | 4.7% |

Market Dynamics

Drivers - Accelerating Vehicle Electrification and EV Adoption

The global shift toward electric vehicles is fundamentally transforming automotive switch demand. Unlike traditional internal-combustion engine vehicles, EVs require specialized high-voltage switching systems for battery management, power distribution, and charging. The vehicle electrification market is projected to grow from US$ 51.84 Bn in 2026 to US$ 83.87 Bn by 2033 at a 7.1% CAGR, driving significant demand for advanced automotive switch technologies. Passenger car production in India is growing at a positive CAGR, with the electric vehicle segment expanding even faster. This electrification trend extends to commercial vehicles, where the adoption of electric and hybrid powertrains necessitates sophisticated control switches for battery monitoring, thermal management, and regenerative braking systems.

Integration of Advanced Driver Assistance Systems (ADAS)

The mandatory integration of ADAS across global automotive markets is creating substantial demand for automotive switches. ADAS features, including adaptive cruise control, lane-keeping assistance, automatic emergency braking, and collision avoidance systems, all depend on sophisticated control interfaces accessible via steering-wheel switches and integrated control panels. The Advanced Driver Assistance Systems market expanded from US$ 43.03 Bn in 2024 to US$ 49.56 Bn in 2026, reflecting rapid regulatory adoption. European regulatory standards have mandated advanced safety features, requiring manufacturers to integrate hands-on detection sensors and multifunction steering-wheel switches. The steering wheel switches market, valued at US$ 3.5 Bn in 2026, is experiencing steady demand from infotainment control segments, growing at a 2.5% CAGR through 2034, underscoring the critical role of switches in modern vehicle safety systems.

Restraints - Raw Material Price Volatility and Supply Chain Complexity

Automotive switch manufacturers face significant challenges from fluctuating raw material costs, particularly for copper, aluminum, and specialized electronic components required for advanced switch assemblies. Supply chain disruptions and geopolitical tensions have intensified price volatility for critical materials used in switch manufacturing. Additionally, the complexity of sourcing compliant materials for multi-voltage and high-reliability switches compounds production costs. The transition from mechanical to electronic components increases the dependency on semiconductor materials, which have experienced substantial price fluctuations in recent years. Manufacturers must invest in inventory management and strategic sourcing to mitigate these risks, ultimately increasing operational costs.

Integration of Touch-Based Interfaces and Technology Transition Challenges

The automotive industry's shift toward touch-sensitive, gesture-recognition, and voice-activated controls poses challenges for traditional automotive switch manufacturers. While these technologies offer enhanced user experiences, they require significant research and development investment, specialized manufacturing capabilities, and integration expertise. The transition from mechanical switches to capacitive touch interfaces and haptic feedback systems demands retooling of production facilities and workforce retraining. Furthermore, the rapid pace of digital transformation creates compatibility issues with existing vehicle platforms, making it difficult for manufacturers to maintain revenue streams from legacy products while transitioning to next-generation technologies.

Opportunities - Emerging Premium Vehicle Segment and Smart Interior Integration

The robust growth in premium and luxury vehicle segments globally presents substantial opportunities for advanced automotive switch suppliers. Premium vehicles increasingly feature sophisticated multi-zone climate controls, panoramic sunroofs with automated control modules, and integrated digital cockpits requiring complex switch arrays. The vehicle roof control module market is projected to grow at 7.53% CAGR between 2026 and 2034, driven by rising demand for sunroofs, panoramic roofs, and convertible mechanisms in SUVs and premium sedans. China, with its growing middle-class population and rising disposable income, is particularly driving this segment, with 550 million middle-class consumers expected by 2030. The automotive smart surfaces and integrated controls market is anticipated to reach US$ 20.82 Bn by 2036 with a 14.1% CAGR, offering significant growth opportunities for suppliers capable of integrating multiple switching functions into centralized smart surface platforms.

Connected Vehicles and Over-the-Air Update Capabilities

The proliferation of connected vehicles and autonomous driving technologies is opening new opportunities for automotive switches with embedded software capabilities and Over-the-Air (OTA) update functionality. Vehicles equipped with connected-vehicle technology enable remote diagnostics, predictive maintenance alerts, and dynamic software updates that enhance switch performance and safety features without requiring physical service interventions.

ZF Friedrichshafen has deployed steer-by-wire systems featuring advanced control software for premium vehicles, indicating market acceptance of digitally enabled switch solutions. The integration of 5G connectivity and vehicle-to-everything (V2X) communication standards requires switches capable of managing complex data transmission protocols and real-time control signals. Fleet operators and ride-sharing platforms represent emerging customer segments with substantial demand for telematics-enabled switches that support fleet management, driver safety monitoring, and operational efficiency optimization.

Category-wise Analysis

By Application Insights

Steering wheel switches command the largest share of the application segment, capturing approximately 35% of the total market value. This dominance underscores the critical role of steering-mounted controls in modern vehicle design, with OEM adoption rates reaching 64% in premium vehicle segments. Steering wheel switches consolidate multiple control functions, audio, cruise control, infotainment navigation, and ADAS engagement into ergonomically positioned interfaces that enhance driver safety by minimizing hand displacement from the wheel.

The segment's growth is reinforced by regulatory mandates requiring hands-on detection capabilities for Level 2 and Level 3 autonomous driving systems. China leads this segment with vehicles integrating advanced multifunction steering wheels, supported by local manufacturers Geely, BYD, and SAIC, implementing premium interior components in mass-market models. Infotainment and multimedia controls represent the fastest-growing application sub-segment, driven by increasing consumer demand for seamless connectivity and personalized in-vehicle experiences.

By Vehicle Type Insights

Passenger vehicles represent the dominant vehicle type segment, accounting for approximately 56% of total automotive switch market value. This leadership position stems from exceptionally high global production volumes, with passenger-car manufacturing exceeding 80 million units annually. Every passenger vehicle typically includes 15-25 switches across various applications, including HVAC control, power windows, seat adjustment, door locks, and advanced safety systems. The segment benefits from consistent replacement demand in mature markets and rapidly growing new-vehicle sales in the Asia-Pacific, where passenger-car sales account for over 50% of the region's automotive market value.

Light commercial vehicles (LCVs) are experiencing accelerated switch adoption due to integration of advanced telematics, fleet management systems, and safety features required by regulatory standards in developed markets. Heavy commercial vehicles require specialized high-reliability switches for demanding operational environments, positioning this segment for significant growth as fleets electrify and adopt autonomous driving features.

By Sales Channel Insights

The Original Equipment Manufacturer (OEM) channel maintains dominance with approximately 64% market share, reflecting the tight integration between switch suppliers and vehicle manufacturers during the design and production phases. OEM relationships are characterized by long-term supply agreements, stringent quality certifications, and collaborative product development for next-generation vehicle platforms. OEM suppliers benefit from predictable demand patterns tied to vehicle production schedules and opportunities to influence specifications for emerging technologies such as OTA update-enabled switches and integrated smart surface controls.

The aftermarket segment is expanding rapidly, with a 8% CAGR, driven by an aging vehicle fleet, rising consumer demand for interior upgrades, and the availability of advanced replacement switches with enhanced functionality. The aftermarket is particularly robust in North America, where more than 280 million vehicles are in active use, creating substantial demand for replacement and customization. India's automotive aftermarket is growing at exceptional rates, with vehicle customization becoming increasingly popular among middle-income consumers seeking to upgrade vehicle features.

Regional Insights

North America Automotive Switch Trends

North America maintains a significant position in the global automotive switch market, driven by robust SUV and pickup truck production, which together account for over 75% of new-vehicle sales in the region. The United States leads regional demand through strong adoption of luxury vehicles featuring premium switch technologies with haptic feedback, touch-sensitive interfaces, and integrated climate controls. Regulatory frameworks established by the National Highway Traffic Safety Administration (NHTSA) mandate advanced safety features, including electronic stability control, automatic emergency braking, and lane-keeping assistance, necessitating sophisticated switch solutions across vehicle portfolios. Electric vehicle adoption in North America has accelerated significantly, with EV sales growing at 15-20% annually and reaching approximately 1.5 million units in 2024.

Tesla, Ford, General Motors, and Lucid Motors are integrating steering-wheel switches with advanced connectivity for navigation, media control, and driver-assistance-system engagement, thereby driving innovation in switch design and functionality. The aftermarket segment is particularly robust, with enthusiasts and fleet operators actively upgrading interior components with advanced replacement switches. North America is projected to grow at 1.5-2.5% CAGR through 2033, reflecting market maturity combined with steady EV transition momentum and replacement demand from aging vehicle fleets.

Europe Automotive Switch Trends

Europe is a highly regulated market, with regulatory harmonization through the Whole Vehicle Type-Approval System (WVTA) standardizing safety requirements across EU member states. Germany leads the region as the world's first country to establish comprehensive regulatory frameworks for autonomous driving (Level 3-4), creating demand for advanced switch technologies supporting automated vehicle control. Germany's automotive manufacturing ecosystem, centered around Volkswagen, BMW, Mercedes-Benz, and Audi, drives innovation in premium switch solutions featuring capacitive touch interfaces and multi-zone control capabilities. France, Spain, and the United Kingdom are experiencing growth in the premium vehicle segment, with increased demand for sophisticated infotainment controls and climate-management switches.

European manufacturers emphasize sustainable manufacturing practices and materials, with the growing adoption of recyclable switch components aligned with EU circular-economy directives. EV production is particularly strong across the Nordic countries, where Norway, Sweden, and Iceland have achieved EV adoption rates of 80% or higher, thereby driving specialized demand for high-voltage switching systems. ZF Friedrichshafen, Continental, and Bosch maintain a strong market presence through continuous innovation in switch design and integration with vehicle electronic architectures. Europe is expected to register 4-5% CAGR growth, supported by regulatory mandates and premium vehicle segment expansion.

Asia Pacific Automotive Switch Trends

Asia Pacific commands the largest global market share, representing approximately 40% of the total automotive switch market value, with exceptional growth driven by China, Japan, India, and emerging ASEAN nations. China alone produced over 30 million vehicles in 2024, establishing itself as the world's largest automotive manufacturing hub. Chinese EV manufacturers, including BYD, NIO, Li Auto, and XPeng, are rapidly expanding production, with EV sales exceeding 10 million units annually and projected to represent 40-50% of total Chinese vehicle sales by 2030. This electrification wave is driving massive demand for specialized automotive switches supporting high-voltage battery management, regenerative braking systems, and advanced infotainment platforms. Japan maintains technological leadership through Denso, Panasonic, and Alps Alpine, which supply sophisticated switch solutions to Toyota, Honda, Nissan, and Subaru.

India's automotive switch market is experiencing exceptional growth, valued at US$ 528.78 Mn in 2024 and projected to reach US$ 910 Mn by 2033 at 8.06% CAGR, driven by rising passenger car sales and increasing feature integration in mass-market vehicles. India's passenger car segment generated US$ 296.40 Mn in switch demand in 2024, while the EV segment is growing at 10.04% CAGR, reflecting the accelerating adoption of electric vehicles among Indian consumers.

Competitive Landscape

The global automotive switch market exhibits a moderately consolidated structure characterized by dominance of established multinational suppliers alongside emerging regional manufacturers. The top five players Robert Bosch, Continental, ZF Friedrichshafen, Valeo, and Denso collectively control approximately 35% of global market share through strong OEM relationships, extensive product portfolios, and vertical integration capabilities.

Bosch and Continental leverage their automotive electronics expertise to expand into advanced switching solutions with integrated software capabilities and OTA update functionality. Strategic differentiators include technological innovation in haptic feedback systems, integration of artificial intelligence for predictive maintenance, development of multi-functional smart surface controls, and vertical integration into semiconductor components for high-reliability automotive applications.

Key Developments:

- Q3 2024: Continental AG unveiled a new modular switch platform enabling flexible integration of multiple control functions into centralized vehicle control modules, significantly reducing manufacturing complexity and component costs while supporting OTA software updates for enhanced vehicle functionality.

- December 2024: Denso announced strengthened partnership with Onsemi for procurement of advanced automotive sensors supporting ADAS and autonomous driving technologies, reinforcing commitment to integrated sensing and control solutions for next-generation vehicle platforms.

- January 2026: ZF Friedrichshafen confirmed deployment of steer-by-wire switching systems featuring advanced control software for premium Chinese EV manufacturer NIO, demonstrating technological acceptance of digitally-enabled steering control solutions in luxury automotive segments.

Companies Covered in Automotive Switch Market

- Robert Bosch

- Continental

- Delphi Technologies (BorgWarner)

- ZF Friedrichshafen

- Valeo

- Denso

- Magna

- Aptiv

- Johnson Electric

- Others Key Players

Frequently Asked Questions

The global automotive switch market was valued at US$ 52.5 Bn in 2026 and is projected to reach US$ 78.4 Bn by 2033, expanding at a 5.9% CAGR during the forecast period.

Key demand drivers include accelerating vehicle electrification with global EV production exceeding 15 million units annually, mandatory integration of Advanced Driver Assistance Systems (ADAS) across global markets, rising adoption of digital cockpits and infotainment systems, increasing consumer demand for vehicle comfort and convenience features, and regulatory mandates requiring sophisticated vehicle control interfaces for autonomous driving functions.

Steering wheel switches represent the dominant application segment, commanding approximately 35% of market value, driven by their critical role in ADAS engagement, infotainment control, and their adoption across 64% of OEM platforms in premium vehicle segments where safety and driver convenience are prioritized.

Asia Pacific leads the global market with approximately 40% market share, driven by exceptional vehicle production volumes in China (exceeding 30 million units annually), rapid EV adoption, strong automotive manufacturing ecosystems in Japan and India.

Leading market players include Robert Bosch GmbH, Continental AG, ZF Friedrichshafen AG, Valeo S.A., Denso Corporation, and Magna International.