- Automotive Components & Materials

- Automotive Side Impact Beams Market

Automotive Side Impact Beams Market Size, Share, and Growth Forecast, 2026 - 2033

Automotive Side Impact Beams Market by Vehicle Type (Passenger Car, Commercial, Electric Vehicle), Material Type (Steel, Aluminum), Sales Channel (OEM, Aftermarket), Application (Front Door, Rear Door), and Regional Analysis 2026–2033

Automotive Side Impact Beams Market Size and Trends Analysis

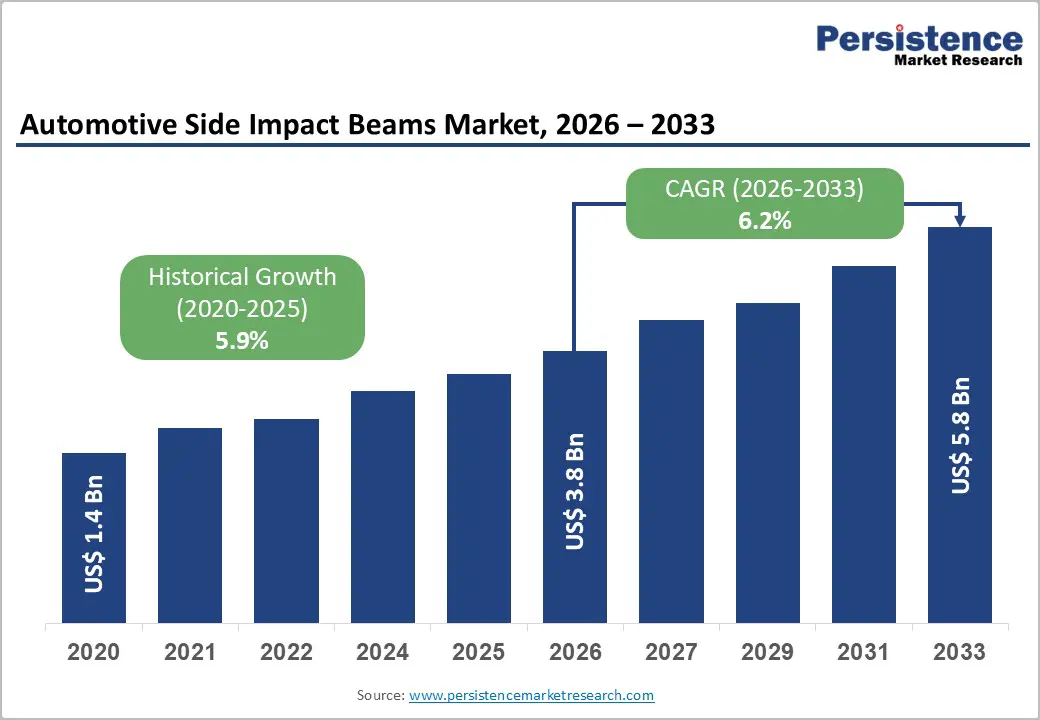

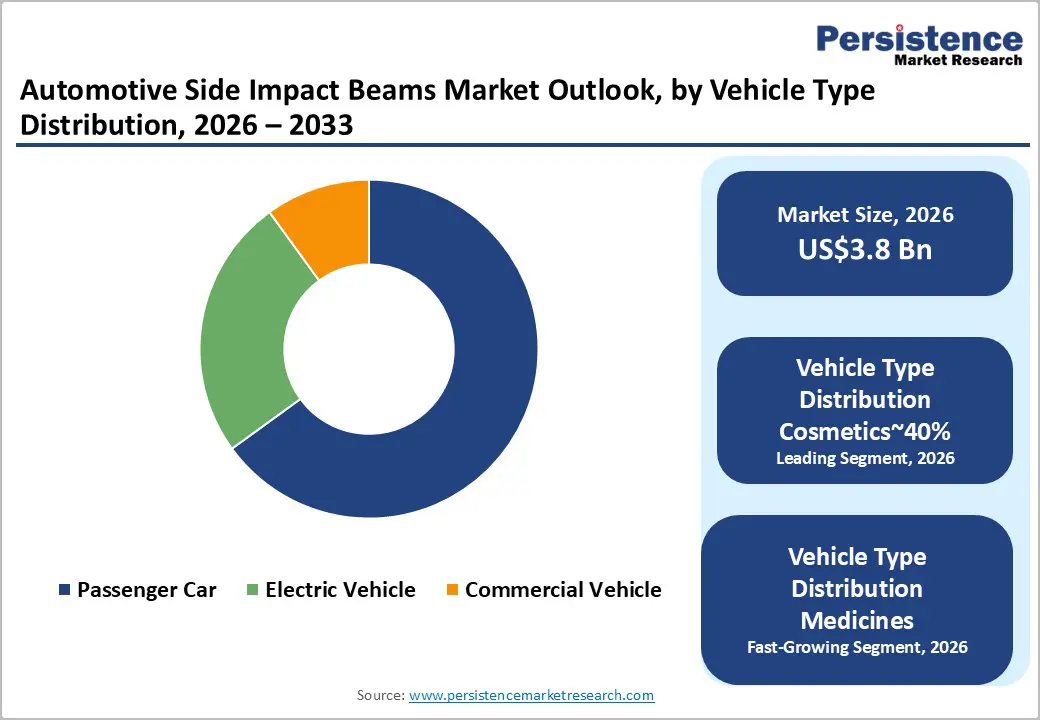

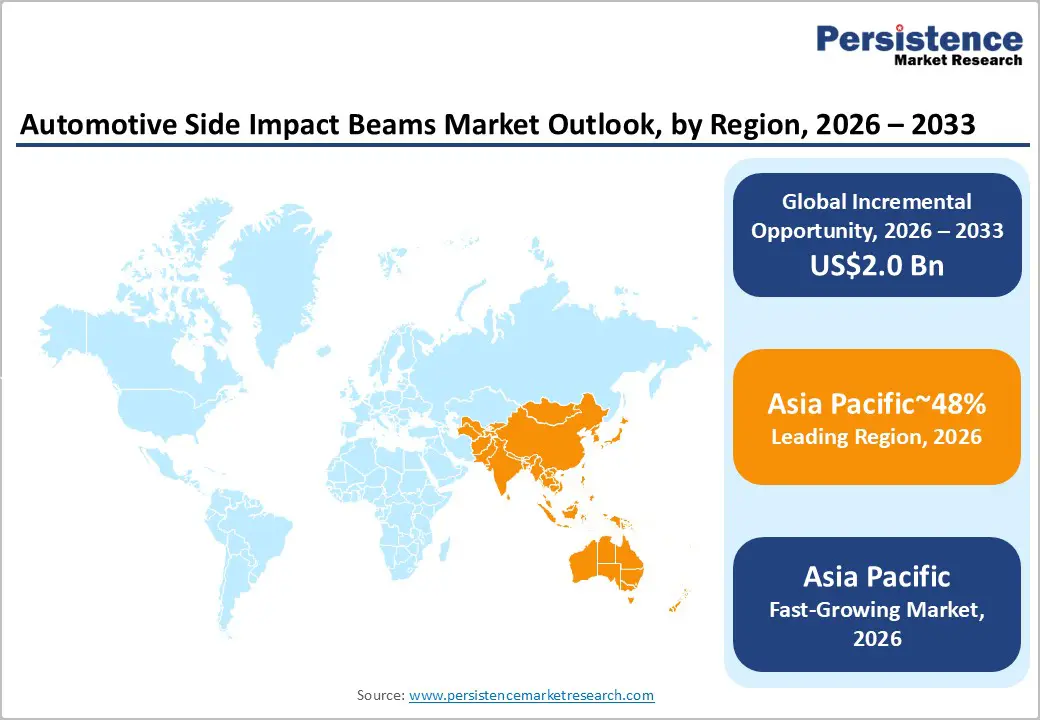

The global automotive side impact beams market size is projected to be valued at US$3.8 billion in 2026 and is projected to reach US$5.8 billion by 2033, growing at a CAGR of 6.2% between during the forecast period from 2026 to 2033, driven by the intensifying stringency of global vehicular safety mandates and the surging production of electric vehicles (EVs), which require specialized structural reinforcement to protect floor-mounted battery packs. The market’s evolution is characterized by a strategic shift toward lightweighting to meet carbon emission targets without compromising structural integrity.

Key Industry Highlights:

- Leading Region: Asia-Pacific is anticipated to lead the global automotive side-impact beam market, with approximately 48% share, driven by high vehicle production, growing SUV penetration, and emerging safety regulations in India, China, and Southeast Asia.

- Leading Material Type: Steel is expected to remain the leading material in the global automotive side impact beam market, accounting for approximately 70% of the market, owing to its superior shock absorption, structural rigidity, and cost-effectiveness in protecting vehicle occupants during side collisions.

- Leading Vehicle Type: Passenger cars are expected to remain the leading vehicle type, accounting for approximately 75% share, as they represent the largest production volume and highest integration of side impact safety components globally.

- Key Industry Developments: In April, 25 KIRCHHOFF Automotive debuted SIBORA Silicon-Boron steel for improved energy absorption at Auto Shanghai 2025. KIRCHHOFF automotive showcased components made from the new "SIBORA" silicon-boron steel grade. Developed in collaboration with Volkswagen, this material is specifically optimized for hot-formed structural components, such as side-impact beams, to achieve 15% higher energy absorption in crashes.

| Report Attribute | Details |

|---|---|

|

Automotive Side Impact Beams Market Size (2026E) |

US$3.8 Bn |

|

Market Value Forecast (2033F) |

US$5.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Material Innovation Enabling Cost-Effective Weight Reduction

Material innovation is increasingly shaping competitive dynamics by enabling structural weight reduction without destabilizing cost structures. Advanced high-strength steel grades support thinner beam geometries while reinforcing energy absorption performance, allowing OEMs to optimize crash compliance using existing cold-forming infrastructure. This preserves capital efficiency and shortens industrialization timelines, positioning AHSS as the default solution across high-volume platforms. Aluminum alloys and composite systems extend the lightweighting envelope, but their adoption remains uneven due to elevated raw material costs, longer cycle times, and tooling complexity, creating a segmented material hierarchy rather than wholesale substitution.

Electric vehicle architectures are intensifying demand for hybridized material strategies as battery mass and packaging constraints reshape load-path requirements. Localized reinforcement with carbon or aramid fibers, selectively integrated into high-strength steel, is emerging as a pragmatic compromise between performance and cost. This approach aligns gains in lightweighting with regulatory safety thresholds while compressing the incremental cost per kilogram saved. As a result, material selection is becoming a value-chain optimization exercise, favoring suppliers with multi-material engineering capability and scalable manufacturing discipline.

Technological Complexity and Integration Challenges

The shift toward thinner door architectures is intensifying structural and engineering constraints across the side-impact protection value chain. Compressing energy absorption capacity into a reduced sectional depth requires complex beam geometries, tighter tolerances, and advanced metallurgical control, often necessitating heat treatment or press-hardening. These requirements elevate R&D intensity, extend validation timelines, and increase upfront engineering costs for OEMs, particularly on high-volume platforms where design changes cascade across multiple vehicle derivatives.

Parallel integration of side-curtain airbag sensors and wiring within constrained door cavities further complicates packaging. Spatial competition between safety electronics and structural members limits beam cross-section optimization, forcing trade-offs between crash performance, manufacturability, and interior space targets. This convergence of structural and electronic requirements reinforces development risk and favors suppliers with integrated design, simulation, and systems-level packaging expertise capable of resolving multi-constraint optimization challenges at scale.

Integration of Advanced Driver Assistance Systems and Predictive Safety Architectures

The integration of advanced driver assistance systems with passive safety components is reshaping opportunity pathways within automotive structural design. Expanding NCAP requirements reinforces a systems-level safety framework in which side-impact beams must align with sensor placement, electrical routing, and real-time energy-management logic. This convergence supports the emergence of smart beam architectures that incorporate embedded sensing, impact prediction, and data-capture functions. As passive safety increasingly interacts with predictive electronics, value shifts toward modular, electronics-ready designs, enabling suppliers to capture pricing uplift through differentiated integration capability rather than material substitution alone.

In December 2025, HARMAN acquired ZF’s ADAS business to enable unified predictive safety and cross-domain computing platforms. This development directly reinforces the smart beam opportunity by accelerating the adoption of unified computing architectures in which ADAS perception informs predictive safety actions. Real-time lateral collision forecasting enables earlier activation and optimization of passive structures, thereby increasing the functional importance of sensor-integrated side-impact beams. The transaction validates cross-domain safety integration as a commercial priority, strengthening demand for beam designs engineered to interface seamlessly with predictive electronics and centralized vehicle computing platforms.

Category–wise Analysis

Vehicle Type Insights

Passenger cars are expected to be the leading segment in the automotive side impact beam market, accounting for an estimated 60% share of overall revenue. This dominance is driven by high global production volumes, NCAP-focused safety requirements, and urban collision exposure. Passenger vehicles rely on advanced side impact beams for occupant protection, including integration with airbags and door modules, while new materials and lightweighting initiatives support compliance with emission and safety standards.

Recent industrial updates include the shift to large-scale underbody castings, integrated side impact modules, and the introduction of green steel alloys. Technological trends focus on hollow-section high-strength steel, multi-material joining, and early-stage smart sensors for impact prediction. Regulatory mandates, such as UN R95, FMVSS 214, and Euro NCAP far-side and pole tests, have increased the adoption of UHSS and reinforced-beam designs. Leading players include Kirchhoff Automotive, Gestamp, Aisin Corporation, Benteler International, and Arconic, with Asia Pacific dominating production and Europe leading in technological innovation.

Electric Vehicles (EVs) are anticipated to be the fastest-growing sub-segment in the side impact beam market, driven by battery protection requirements, increased vehicle weight, and government electrification policies. EV beams must manage higher kinetic energy while safeguarding underfloor battery packs, spurring adoption of UHSS, bionic thin-walled structures, aluminum extrusions, and multi-material hybrid systems. Key industrial trends include thermal runaway mitigation, AI-assisted crash simulations, and multi-material optimization for lightweighting without compromising safety.

Regulatory standards, including Euro NCAP side pole tests, UN Regulation 135, and FMVSS 214, ensure global compliance and accelerate technology adoption. Leading suppliers in this space are Kirchhoff Automotive, Gestamp, Benteler International, Aisin Takaoka, and H-One Co. Europe holds the largest market share due to early EV adoption, while Asia Pacific is the fastest-growing region, driven by domestic EV expansion in China and India.

Application Insights

The front door side-impact beam is expected to lead the automotive side-impact beam market, accounting for approximately 55% of the market in 2026, driven by a critical focus on front-seat occupant safety. This segment benefits from the "Front-First" design philosophy, where drivers and front passengers are closest to the impact zone, necessitating high-strength engineering and thicker, tailor-welded beams.

Technological advancements such as hot-stamped Boron steel, smart-sensing pre-crash beams, and acoustic-damping integration enhance both occupant protection and cabin comfort. Modular door assemblies and ring-structure BiW designs further streamline manufacturing while maintaining safety integrity. Leading suppliers such as Gestamp, ArcelorMittal, and H-One leverage global OEM relationships and patented high-tensile steels to reinforce the segment’s dominance, while continuous upgrades in front-beam geometry ensure compatibility with SUVs and modern vehicle ergonomics, solidifying its market leadership.

The Rear Door Side-Impact Beam segment is projected to be the fastest-growing segment in the automotive side-impact beam market, driven by increased emphasis on rear-seat occupant safety and family-oriented vehicle design. Growth is driven by dual-beam rear door architectures, laser-welded reinforcement at B- and C-pillar junctions, and integration with window and child-lock modules.

EV adoption has prompted enhanced intrusion resistance to protect rear battery packs, while lightweight aluminum and sustainable materials reduce mass without compromising energy absorption. Manufacturers such as Benteler International, Kirchhoff Automotive, Shiloh Industries, and AISIN are innovating with modular, high-strength rear beams to meet stricter IIHS and Euro NCAP standards. The convergence of ride-sharing, SUV ride-height considerations, and child-safety prioritization is accelerating adoption, making rear beams a critical growth engine.

Regional Insights

Asia Pacific Automotive Side Impact Beams Market Trends

Asia-Pacific is projected to remain the leading and fastest-growing regional market, accounting for approximately 48% of global side-impact beam demand, supported by rapid industrialization, regulatory harmonization, and extensive automotive production capacity. China and India serve as dual growth engines, with Chinese manufacturers supplying high-volume platforms and Indian suppliers capturing emerging market adoption. The region benefits from a developing local manufacturing ecosystem, enabling cost-competitive production and accelerating compliance with advanced safety standards, such as BNVSAP, in India. Regulatory enforcement and large-scale platform deployment collectively reinforce Asia Pacific’s structural dominance and long-term revenue potential.

Market expansion is particularly pronounced in EV-related components and emerging vehicle platforms, reflecting structural shifts toward electrification and lightweighting. India shows strong adoption momentum, while China continues to scale both conventional and electric vehicle production. Strategic imperatives for suppliers include investing in high-volume, cost-efficient manufacturing, integrating advanced safety technologies, and supporting platform innovation, positioning the region as both a production hub and a growth-focused market with accelerated adoption compared with mature North American and European markets.

Europe Automotive Side Impact Beams Market Trends

Europe is expected to remain a key regional market, characterized by mature production networks, regulatory harmonization, and high technological integration. The region’s market structure is reinforced by stringent EU-wide safety standards and circular economy mandates, which sustain the adoption of advanced materials and premium platform solutions. Strong supplier positioning, exemplified by integrated manufacturing capabilities, supports consistent revenue capture, while continued premium-vehicle demand and the EV transition underpin stable growth relative to North American markets.

Growth in Europe is primarily driven by the adoption of advanced materials, including AHSS and composite beams, to meet structural lightweighting requirements and carbon footprint reduction initiatives. Regulatory enforcement across multiple EU member states incentivizes the adoption of low-emission, high-performance components, creating premium value potential for compliant suppliers. Strategic priorities focus on material efficiency, sustainability compliance, and alignment with evolving premium and electrified vehicle architectures, positioning Europe as a technologically advanced yet comparatively mature regional market with moderate growth acceleration.

North America Automotive Side Impact Beams Market Trends

North America is expected to remain a significant regional market, supported by stable regulatory frameworks and well-established OEM-supplier networks. The region’s mature production base underpins consistent demand, while compliance with NHTSA’s updated side-impact protocols ensures ongoing specification upgrades. Leading suppliers leverage modular platform strategies and localized manufacturing to maintain market share and support supply chain resilience, reinforcing predictable revenue streams within a relatively steady growth environment.

Growth dynamics in North America are primarily driven by the gradual adoption of electric vehicles, which, despite lower penetration than in Europe and the Asia-Pacific, require enhanced structural designs for battery protection and weight management. Strategic priorities include alignment with evolving regulatory standards, nearshoring initiatives under USMCA to mitigate supply chain risks, and targeted adoption of advanced materials. These factors collectively sustain North America as a mature, compliance-driven market with measured expansion potential.

Competitive Landscape

The global automotive side impact beams market is moderately consolidated, with the top five players controlling approximately 45–50% of total revenue, supported by advanced R&D capabilities and proprietary hot-stamping technologies. Competitive advantage is primarily derived from the ability to deliver multi-material solutions, combining steel, aluminum, and high-performance polymers, while ensuring alignment with OEM design specifications. Long-term supply contracts and integration with assembly line logistics reinforce high entry barriers and secure sustained revenue streams for established suppliers. Market strategies focus on product innovation, material optimization, and supply chain integration, while smaller and emerging suppliers face structural challenges in scaling production and meeting stringent safety standards. Forward growth is likely to be driven by lightweighting trends, regulatory safety mandates, and evolving OEM material preferences, sustaining moderate consolidation and strategic differentiation.

Key Industry Developments:

- In November 2025, ArcelorMittal’s Yujian™ integration solution won the Global Innovation Award. Its joint ventures, VAMA and GONVVAMA, also received the Gasgoo Award for the Yujian™ Multi-Part Integration Solution. This technology integrated the side-impact beam and door frame into a laser-welded blank, enhancing the safety-to-weight ratio for next-generation electric vehicles.

- In January 2025, Gestamp unveiled its GES-GIGASTAMPING® Door Ring at the Bharat Mobility Global Expo, enhancing side-impact integrity. The one-piece, large-format “Door Ring” replaced multiple side impact parts, improving the safety cell’s structural response in lateral collisions and reducing overall vehicle weight for the EV market.

- In October 2023, ArcelorMittal (specifically through its ArcelorMittal Tailored Blanks division) launched a new generation of multi-part door rings.

Companies Covered in Automotive Side Impact Beams Market

- BENTELER Automotive

- Kirchhoff Automotive

- Gestamp Automocion

- Magna International

- Tower International

- Aisin Takaoka

- Sango Co.

- Tata Autocomp Systems

- Motherson Sumi Systems

- Endurance Technologies

- Minth Group

- Yanfeng Automotive Interiors

- GNS America

- H-One Co. Ltd

- Flex-N-Gate (U.S.)

- Hwashin

- MARELLI

Frequently Asked Questions

The global automotive side impact beams market is projected to be valued at US$3.8 billion in 2026 and is expected to reach US$5.8 billion by 2033.

Demand is strengthening due to tightening global vehicle safety regulations, wider adoption of side-impact testing protocols, and increasing electric vehicle production requiring enhanced battery-side protection structures.

The automotive side impact beams market is expected to grow at a CAGR of 6.2% between 2026 and 2033, supported by regulatory compliance and lightweight material innovation.

The most attractive opportunities are emerging in electric vehicle platforms and lightweight multi-material beam designs, particularly in Asia Pacific, where production scale and regulatory harmonization are accelerating adoption.

Key players include Kirchhoff Automotive, Gestamp Automoción, Magna International, Benteler Automotive, Tower International, Aisin Takaoka, Tata Autocomp Systems, Motherson Sumi Systems, Minth Group, and Yanfeng Automotive Interiors.