- Automotive Components & Materials

- Automotive Roof System Market

Automotive Roof System Market Size, Share, and Growth Forecast for 2026 - 2033

Automotive Roof System Market by Roof Type (Sunroof and Moonroof, Panoramic Roof, Others), Vehicle Type (Passenger Cars, and Light Commercial Vehicles), Technology Type (Semi‑Automatic, Automatic), and Regional Analysis, 2026 - 2033

Automotive Roof System Market Size and Trend Analysis

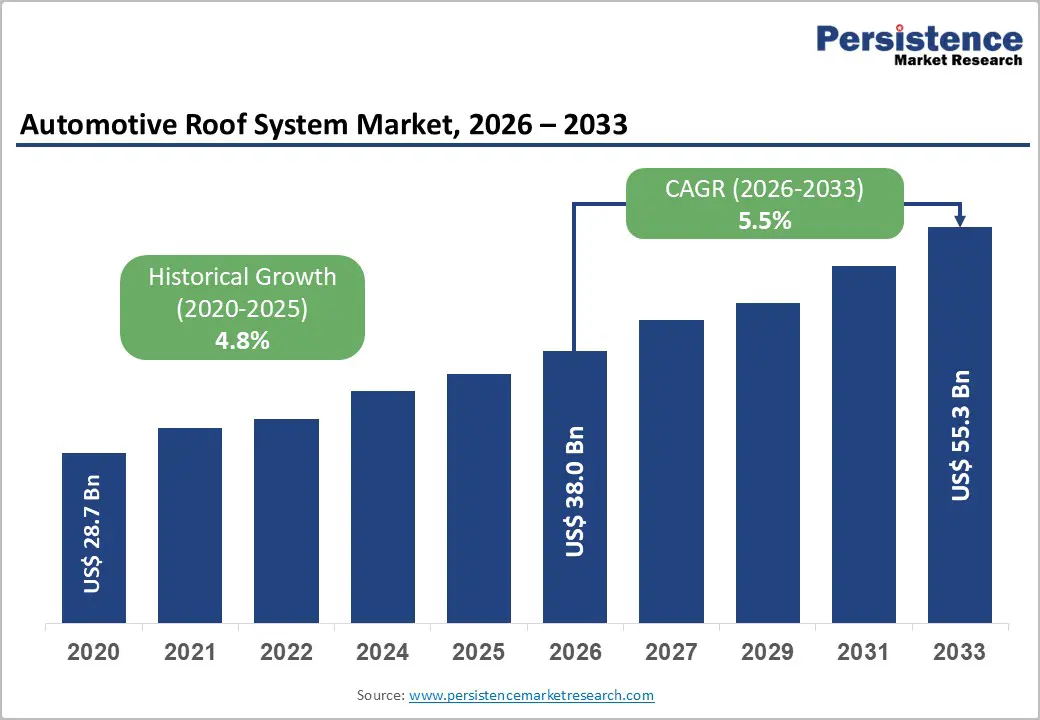

The global automotive roof system market is projected to reach US$ 38.0 billion in 2026 and US$ 55.3 billion by 2033, growing at a CAGR of 5.5% over the forecast period. This expansion is underpinned by rising consumer preference for comfort-oriented and visually distinctive vehicle interiors, alongside rapid growth in SUV/MUV and electric vehicle (EV) segments that increasingly feature advanced roof systems as standard or high-value options.

Key Industry Highlights

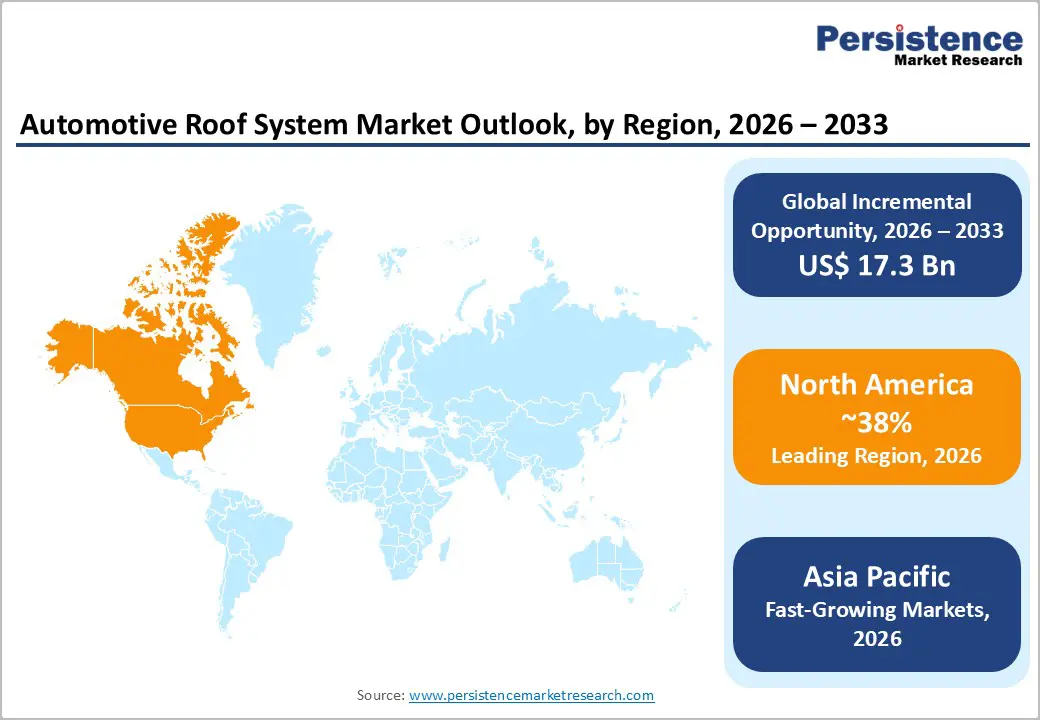

- Leading Region: North America leads the automotive roof system market with 38% share, due to high penetration of SUVs, premium vehicles, and EVs, supported by strong consumer demand for comfort-oriented and visually distinctive roof systems.

- Fastest growing region: Asia Pacific is the fastestgrowing region, holding 7.1% CAGR, driven by rising SUV/MUV and EV production in China, India, and ASEAN, along with expanding manufacturing capabilities for glass and electronics.

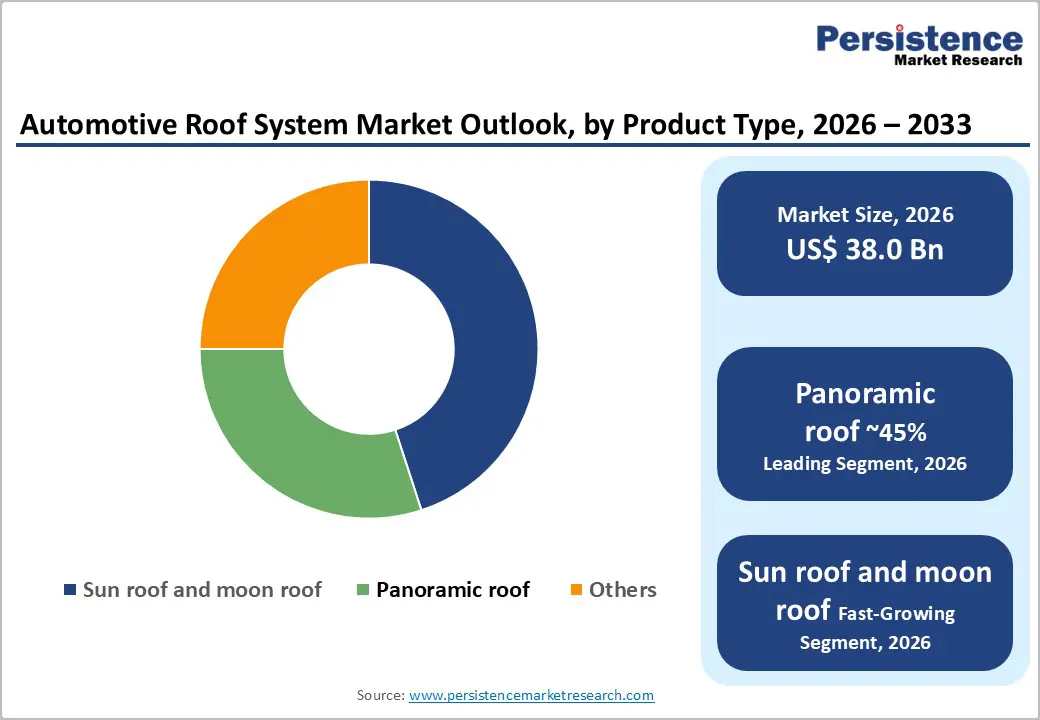

- Dominant Roof Type: The panoramic roof segment dominates the Type-based category, capturing around 45% of the market share due to its ability to enhance cabin openness, natural light, and premium perception across SUVs and EVs.

- Fastest-growing Roof Type: The automatic roof systems segment within Technology Type is growing fastest, as electrically actuated, smart, and app-integrated systems gain traction in premium, SUV, and EV segments.

- Key Opportunity: The integration of panoramic, multi-optional, and solar-integrated roof systems into SUVs and EVs, supported by lightweight materials and digital connectivity, represents the most significant long-term opportunity in the Automotive Roof System Market.

| Key Insights | Details |

|---|---|

|

Automotive Roof System Market Size (2026E) |

US$ 9.8 Bn |

|

Market Value Forecast (2033F) |

US$ 13.3 Bn |

|

Projected Growth CAGR (2026-2033) |

4.5% |

|

Historical Market Growth (2020-2025) |

3.8% |

Market Dynamics

Driver - SUV and EV Popularity Accelerates Demand for Panoramic and Sunroof Systems as Premium Comfort Features

The automotive roof system market is experiencing strong growth due to the rising popularity of SUVs, MUVs, and premium vehicles that increasingly feature panoramic roofs and sunroof systems as standard or optional offerings. Industry-aligned data indicates that the SUV and MUV segment already contributes nearly 36% of total roof-system demand, driven by higher vehicle pricing and strong consumer willingness to invest in comfort and style features.

Panoramic glass roofs enhance cabin brightness, create a feeling of spaciousness, and deliver a luxury driving experience, which resonates strongly with buyers in China, Europe, and North America, where SUV sales continue to outpace sedans. Additionally, the rapid expansion of electric vehicles is driving roof system adoption, as EV designs often feature large fixed or operable glass roofs to highlight modern styling and enhance the passenger experience. With global EV production rising steadily, the installed base of advanced roof systems is expected to grow significantly.

Smart, Lightweight, and Automatic Roof Technologies Transform User Experience and Drive Long-Term Market Growth

Technological progress is driving growth in the automotive roof system market, particularly through the shift from semi-automatic to fully automatic and smart roof systems. Modern designs now include sensor-based operation, smartphone control, automatic shading, and weather-responsive closing features that improve comfort, safety, and ease of use. Industry assessments indicate that automatic roof systems are outpacing manual alternatives, driven by broader trends in vehicle digitalization and connected technologies.

Innovation in lightweight glass, polycarbonate, and composite materials is helping manufacturers reduce overall vehicle weight while improving insulation, UV protection, and noise control. Advanced laminated glass and electrochromic panels are increasingly used in premium and EV models to manage sunlight without mechanical shades. These improvements also support solar-integrated roof concepts that power auxiliary systems. Growing R&D investment by OEMs and suppliers is accelerating the commercialization of next-generation roof solutions, driving long-term market expansion.

Restraints - Strict Safety Regulations and Weight Compliance Standards Increase Engineering Complexity and Limit Mass-Market Adoption

Strict safety and regulatory standards pose a major challenge for the Automotive Roof System Market, particularly regarding roof strength, rollover protection, and impact resistance. Organizations such as the NHTSA in the United States and Euro NCAP in Europe enforce demanding structural and performance requirements that limit excessive glass coverage and require reinforced designs. To meet compliance standards, manufacturers must integrate additional safety components and conduct extensive testing, which increases product development costs and production timelines.

At the same time, growing pressure to meet fuel-efficiency and emissions-reduction targets forces OEMs to carefully balance comfort features with vehicle weight-reduction strategies. Large glass roofs often require structural compensation elsewhere in the vehicle body, raising engineering complexity. Any failure to meet regulatory expectations can lead to recalls and reputational damage, making manufacturers cautious in mass-market adoption. As a result, these regulatory pressures slow penetration of roof systems in economy vehicles and constrain overall market expansion.

Rising Raw Material Prices and Supply Chain Disruptions Pressure Costs and Slow Roof System Expansion

Fluctuating prices of key raw materials continue to limit profitability and expansion in the automotive roof system market. Glass, aluminum, polymers, and electronic components form the core of panoramic and automatic roof systems, and their costs are highly sensitive to energy prices, supply-chain disruptions, and global demand cycles. Sharp increases in material prices directly impact margins for Tier-1 suppliers such as Webasto, Inalfa, and Magna, forcing OEMs to either absorb cost increases or restrict roof systems to higher-priced vehicle segments.

In addition, the growing use of motors, sensors, and control modules exposes roof systems to semiconductor shortages, which have previously caused production delays across the automotive industry. These disruptions can slow vehicle launches and reduce manufacturing volumes. In highly price-sensitive regions such as India and Latin America, cost pressures make advanced roof systems less feasible for entry-level models, limiting market penetration and slowing overall demand growth.

Opportunities - Growing SUV and EV Production Creates Strong Opportunities for Modular and Multi-Functional Roof Solutions

Significant growth opportunities exist as panoramic and multifunctional roof systems gain adoption in SUVs and electric vehicles. Panoramic sunroofs already dominate the sunroof category and are rapidly expanding beyond luxury cars into mid-range SUVs and crossovers, which represent a growing share of global vehicle production. EV manufacturers are also using large glass roofs to create futuristic designs and enhance cabin ambiance, further driving demand for roof systems. Multi-optional roof systems that combine sliding, tilting, shading, and ventilation functions within a single modular design are gaining popularity because they reduce platform complexity and tooling costs for OEMs.

These systems offer flexibility across different vehicle models and regional climate conditions. Suppliers are increasingly focusing on scalable, modular roof solutions that can be localized for the Asia Pacific, Europe, and North America. As SUV and EV sales continue to rise globally, these advanced roof configurations will remain a major driver of long-term market growth.

Connected Smart Roof Ecosystems Open New Revenue Streams Across Premium Vehicles and Commercial Fleet Segments

Another promising opportunity is developing smart, connected roof systems that integrate seamlessly with modern vehicle digital platforms. Today’s roof systems go beyond basic mechanical operation, offering app-based control, voice commands, automatic weather detection, and real-time diagnostics. These features enhance the customer experience and align with the growing trend toward connected vehicles, particularly in premium and luxury segments, where consumers expect high-tech convenience. OEMs are increasingly positioning smart roofs within the digital cockpit ecosystem, enabling them to enhance vehicle differentiation and boost profit margins.

At the same time, fleet operators and ride-hailing companies are exploring roof-integrated lighting, sensors, and monitoring systems to improve passenger comfort, branding, and safety. Features such as UV-blocking glass are especially valuable in hot regions like India and the Middle East. As 5G connectivity and vehicle automation expand, roof-mounted technology will play a larger role in vehicle intelligence and service innovation.

Category-wise Analysis

By Product Type Insights

The Panoramic Roof segment has emerged as the dominant configuration in the Automotive Roof System Market, accounting for approximately 45% of total demand in recent years. Its popularity is driven by the large glass roof that extends across the vehicle, offering enhanced natural light and an open, premium cabin experience for both front and rear passengers. Automakers in the United States, Germany, and China increasingly include panoramic roofs in SUVs, crossovers, and EVs as a key design feature to strengthen vehicle appeal.

Technological improvements in laminated glass, UV-blocking coatings, and thermal insulation have significantly reduced heat buildup and glare, making panoramic roofs practical even in warmer climates such as India and Southeast Asia. These enhancements improve passenger comfort while maintaining visibility and aesthetics. As production volumes increase and manufacturing costs decline with economies of scale, panoramic roofs are expected to maintain their leadership position and continue to drive market growth.

By Vehicle Type Insights

The SUV and MUV segment represents the largest category in the Automotive Roof System Market, accounting for approximately 36% of global demand. This dominance reflects a strong global shift toward larger, more versatile vehicles with higher seating positions, spacious interiors, and premium comfort features. In regions such as North America, China, and India, SUVs have consistently outperformed sedans in sales, encouraging manufacturers to bundle sunroof and panoramic roof options with higher-trim models.

These roof systems enhance visual appeal while helping OEMs justify higher pricing. Structurally, SUV platforms are better suited to large glass panels, as their stronger body structures can better meet safety and reinforcement requirements. The rapid growth of electric SUVs further strengthens this trend, with manufacturers using panoramic roofs to emphasize modern design and innovation. As consumers in emerging markets continue upgrading to larger vehicles, the SUV/MUV segment will remain the primary growth driver for roof systems worldwide.

By Technology Type Insights

Automatic roof systems are rapidly becoming the preferred technology in the Automotive Roof System Market, especially within mid-range and premium vehicles. These systems use electric motors, sensors, and electronic control units to deliver smooth, hands-free operation, automatic rain detection, and intelligent shading features. Compared to semi-automatic designs, automatic systems offer greater convenience, enhanced safety, and seamless integration with vehicle infotainment and climate-control platforms.

Industry trends show that OEMs are increasingly standardizing automatic roof systems in higher trims, reflecting strong consumer demand for smart vehicle features. Technological advancements in motor efficiency, noise reduction, and electronic reliability have made these systems more durable and cost-effective. In addition, automatic roofs can be linked with speed sensors and weather systems to adjust operation automatically, improving passenger comfort. As connected vehicles become mainstream and digital integration deepens, automatic roof systems are expected to capture a growing share of the overall market.

Regional Insights

North America Automotive Roof System Market Trends

North America remains a leading market for automotive roof systems, supported by strong demand for SUVs, premium vehicles, and advanced comfort features. U.S. consumers show a strong preference for panoramic and sunroof-equipped vehicles, particularly within higher trim packages of crossovers and pickup trucks. At the same time, regulatory pressure from agencies such as the NHTSA and EPA encourages lightweight and structurally efficient roof designs to support fuel economy goals. The region is also a major innovation hub, with suppliers like Magna, Inteva, and Webasto working closely with domestic automakers to develop smart and solar-integrated roof systems.

Recent launches by Tesla, Ford, and General Motors have highlighted large glass roofs and automated shading technologies, reinforcing the trend toward premiumization. As EV adoption increases through federal incentives and sustainability policies, demand for advanced roof systems is expected to grow steadily, keeping North America at the forefront of technological development and market value.

Europe Automotive Roof System Market Trends

Europe is a mature yet innovation-driven market for automotive roof systems, led by Germany, the United Kingdom, France, and Spain. European consumers place strong value on comfort, aesthetics, and technological sophistication, which has encouraged widespread adoption of sunroof and panoramic roof configurations across premium and mid-range vehicles. Automakers such as BMW, Audi, Mercedes-Benz, and Volkswagen integrate roof systems as standard features in many SUVs and luxury models.

Strict EU safety regulations and emission targets also promote the use of lightweight materials and efficient mechanical designs to maintain vehicle performance. At the same time, smart roof technologies, including automatic operation and sensor-based systems, are gaining popularity, particularly in premium models that emphasize digital features. These systems enhance convenience and align with Europe’s strong trend toward connected-vehicle adoption. As electric vehicle production continues expanding under climate policies, Europe will remain a key innovation center and steady growth market for advanced roof systems.

Asia Pacific Automotive Roof System Market Trends

Asia-Pacific is emerging as the fastest-growing region in the Automotive Roof System Market, driven by rapid urbanization, rising incomes, and the expanding production of SUVs and electric vehicles. China leads regional demand, with domestic manufacturers and joint ventures increasingly offering panoramic roofs in EVs and premium SUVs to attract younger, tech-focused consumers. India and Southeast Asian markets are also witnessing strong growth in sunroof-equipped vehicles as buyers shift toward higher-trim models and lifestyle vehicles.

The region benefits from a strong manufacturing base in glass, aluminum, and electronic components, enabling local suppliers to produce cost-effective roof systems. Global players such as Webasto, Inalfa, and AISIN are expanding production facilities across China, Thailand, and India to meet rising demand. As government EV incentives and infrastructure investments accelerate vehicle modernization, the Asia Pacific is expected to deliver the highest growth rate and become a major revenue contributor to the global roof system market.

Competitive Landscape

The automotive roof system market features a moderately consolidated structure dominated by global Tier-1 suppliers, including Webasto Group, Inalfa Roof Systems, Magna International, AISIN Corporation, Inteva Products, and Valmet Automotive. These companies benefit from strong OEM relationships, advanced engineering capabilities, and global manufacturing networks that support large-scale production. Their leadership is reinforced by continuous investment in smart roof technologies, lightweight materials, and modular roof platforms.

At the same time, regional suppliers in China, India, and Eastern Europe are gaining market share by offering cost-competitive solutions for mass-market vehicles. This creates a two-tier structure with premium innovation at the top and price-driven competition at the lower end. Key competitive strategies include partnerships, acquisitions, and joint ventures to strengthen capabilities in electronics, glass processing, and software. Suppliers are also exploring service-based models such as predictive maintenance and software upgrades, which could reshape long-term revenue streams and competitive differentiation.

Key Developments:

- In January 2025: Webasto Group introduced an advanced panoramic roof with integrated solar cells and automatic shading aimed at SUVs and EVs, enhancing energy efficiency and helping reduce auxiliary power consumption while aligning with evolving CO and fuel-efficiency regulations for premium vehicle segments.

- In March 2024, Inalfa Roof Systems expanded its manufacturing and R&D operations in India, focusing on localized production of sunroof and panoramic roof systems to meet rising OEM demand, reduce lead times, and lower costs, particularly for SUV/MUV and EV platforms.

Companies Covered in Automotive Roof System Market

- Webasto Group

- Inalfa Roof Systems Group B.V.

- AISIN CORPORATION

- HCMF

- Mahindra

- Inteva Products

- Magna International Inc.

- Valmet Automotive

- Yachiyo Industry Co. Ltd

Frequently Asked Questions

The Automotive Roof System Market is projected to reach US$ 38.0 Billion in 2026 and US$ 55.3 Billion by 2033, growing at a CAGR of 5.5% between 2026 and 2033, with a historical CAGR of 4.8% from 2020 to 2025.

Key demand drivers include rising global sales of SUVs/MUVs and electric vehicles, increasing consumer preference for panoramic and sunroof systems, and the adoption of automatic and smart roof technologies that enhance comfort, convenience, and perceived vehicle premiumness.

The Panoramic Roof segment is the leading configuration, capturing around 45% of the market share due to its ability to provide large‑area glass coverage, enhanced natural light, and premium cabin ambiance across SUVs and EVs.

North America is the leading region, supported by high penetration of SUVs, premium vehicles, and EVs, along with strong consumer demand for comfort‑oriented and visually distinctive roof systems in the United States and neighboring markets.

A key opportunity lies in the integration of panoramic, multi‑optional, and solar‑integrated roof systems into SUVs and EVs, supported by lightweight materials, digital connectivity, and smart features that enhance comfort, efficiency, and brand differentiation.