- Automotive Components & Materials

- Automotive Radiator Market

Automotive Radiator Market Size, Share, and Growth Forecast for 2026 - 2033

Automotive Radiator Market Segment Forecasted by Product Type (Down-flow, Crossflow), by Vehicle (Compact, Sub-compact, Mid-size, Sedans, Luxury, Vans), by Material (Aluminium, Copper/Brass, Aluminium/Plastic), by Sales Channel, and Regional Analysis for 2026 - 2033

Automotive Radiator Market Share and Trends Analysis

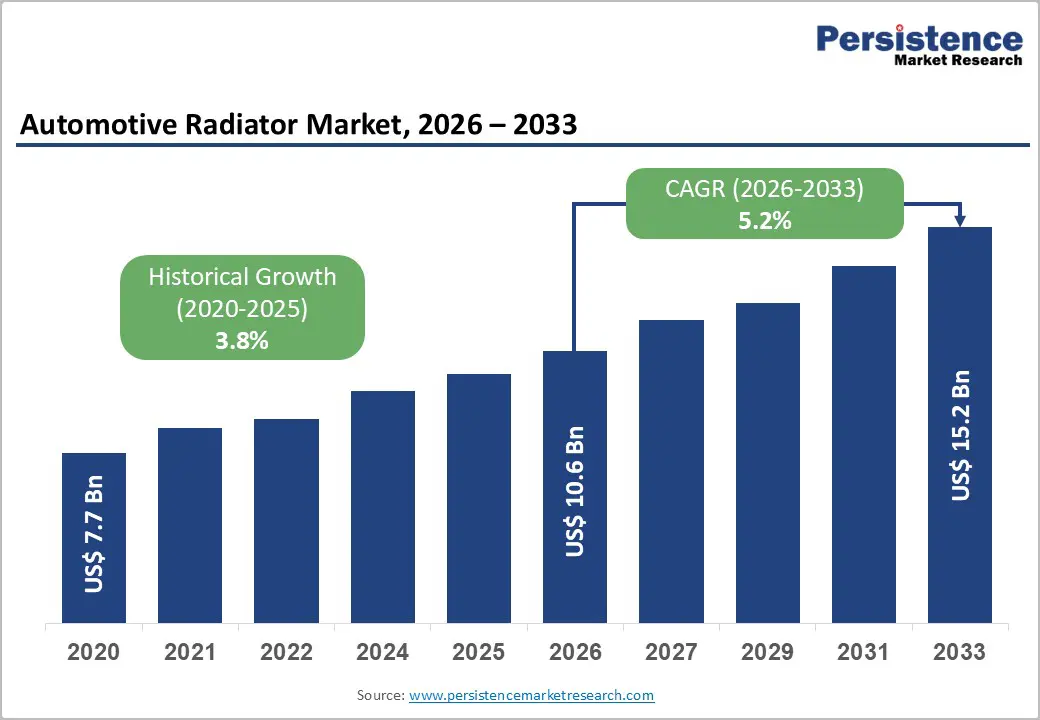

The global automotive radiator market size is likely to be valued at US$ 10.6 billion in 2026 and is projected to reach US$ 15.2 billion by 2033, growing at a CAGR of 5.2% between 2026 and 2033. This expansion is underpinned by sustained vehicle production growth across developed and emerging economies, accelerated electrification driving demand for advanced thermal management systems, and stringent emission regulations necessitating efficient engine cooling solutions.

Key Industry Highlights:

- Dominant Material: Aluminum-plastic composite radiators dominate with approximately 64% share, driven by lightweight construction reducing vehicle weight by 30% to 40% compared to copper-brass alternatives, supporting fuel efficiency while offering superior corrosion resistance and cost-effectiveness.

- Fastest Growing Material: Original equipment manufacturer channels command approximately 72% share through direct integration into vehicle assembly lines, while aftermarket segments grow steadily at approximately 28% share, driven by expanding global vehicle fleets requiring replacement components and performance upgrades.

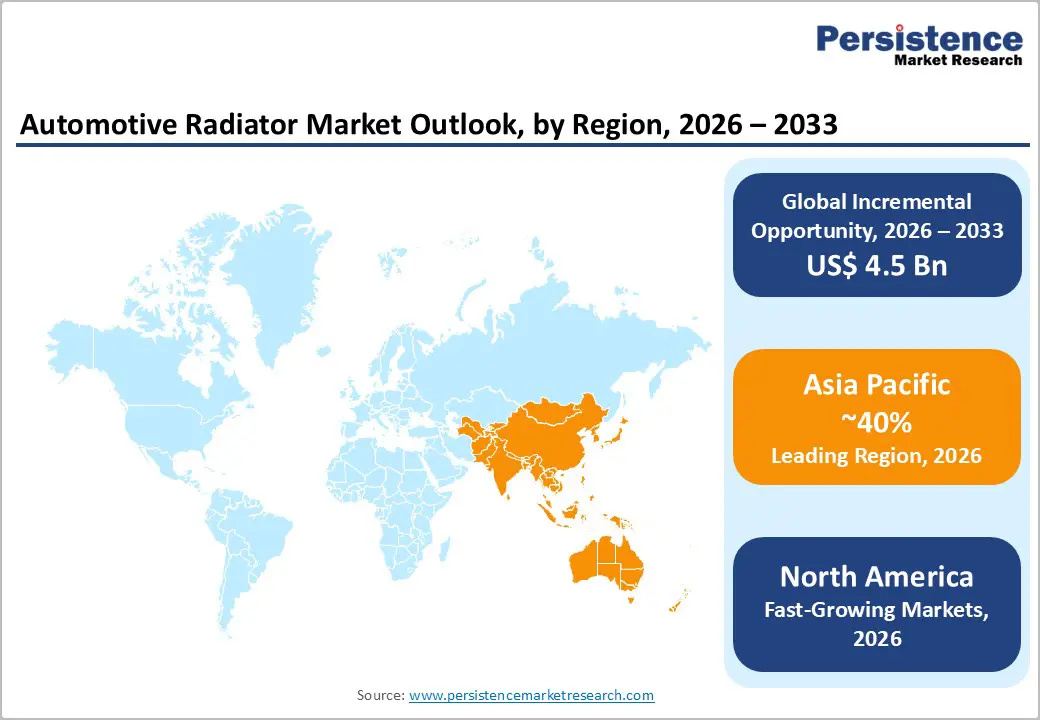

- Dominant Region: Asia Pacific leads regional distribution with approximately 40% market share, dominated by China's position as the world's largest vehicle production hub, manufacturing 23 million cars in 2024, and rapidly expanding electric vehicle adoption, creating specialized battery cooling radiator demand.

- Crossflow radiator configurations hold approximately 58% market share due to superior cooling efficiency and optimal fitment in modern low-profile vehicle architectures, while down-flow designs maintain relevance in commercial vehicles and specific SUV applications.

- Opportunities: Strategic partnerships, including the October 2024 Valeo-MAHLE Joint Development Agreement for electric vehicle thermal management and the November 2024 Valeo-Modine collaboration for high-performance aluminum radiators demonstrate industry emphasis on electrification capabilities and advanced materials innovation.

| Key Insights | Details |

|---|---|

|

Automotive Radiator Market Size (2026E) |

US$ 10.6 Bn |

|

Market Value Forecast (2033F) |

US$ 15.2 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.2% |

|

Historical Market Growth (CAGR 2020 to 2024) |

3.8% |

Market Dynamics Analysis

Drivers - Rapid Electrification and Hybrid Vehicle Adoption Driving Advanced Thermal Management Demand

The automotive industry's transition toward electrification represents a fundamental growth catalyst for the Automotive Radiator Market, as electric and hybrid vehicles require sophisticated cooling systems beyond traditional engine applications. Hybrid and battery electric vehicles necessitate additional low-temperature heat exchangers for regulated battery cooling, power electronics thermal management, and motor temperature control to ensure optimal performance and longevity. According to industry data, global electric vehicle sales are projected to surpass 150 million units annually by 2030, with battery electric vehicles and plug-in hybrid electric vehicles leading adoption across major markets. In India alone, electric vehicle sales reached 100,000 units in 2024, creating substantial demand for specialized lightweight and heat-resistant wheel cooling systems and related thermal components.

Stringent Emission Regulations and Fuel Efficiency Standards Mandating Enhanced Cooling Systems

Increasingly rigorous environmental regulations worldwide are compelling automotive manufacturers to optimize engine performance through advanced thermal management, directly stimulating radiator market expansion. The implementation of Corporate Average Fuel Economy standards in the United States regulates average fuel economy for new vehicles, requiring manufacturers to meet strict benchmarks to avoid penalties, which significantly impacts cooling system specifications. Similarly, the European Union's updated Euro 7 emission standards mandate lower volatile organic compound emissions and enhanced operational efficiency, forcing automakers to integrate high-performance radiators that maintain optimal engine temperatures while minimizing emissions. The trend toward engine downsizing for improved fuel efficiency further intensifies cooling requirements, as smaller displacement turbocharged engines generate concentrated heat loads demanding compact yet highly effective radiator designs with superior thermal performance.

Restraint - Fluctuating Raw Material Prices and Supply Chain Vulnerabilities

The Automotive Radiator Market confronts significant cost pressures from volatile pricing of essential raw materials, including aluminum, copper, brass, titanium dioxide, polyester resins, and specialized solvents used in manufacturing processes. Aluminum and copper experienced notable price fluctuations exceeding 11% in 2023 due to supply chain disruptions tied to global shipping uncertainties, geopolitical tensions including U.S.-China trade conflicts, and the lingering effects of the Ukraine-Russia war on European energy supplies and industrial operations. These raw material cost variations create margin pressure, particularly for mid-tier manufacturers unable to effectively hedge material exposure or pass costs to customers in highly competitive segments. The automotive value chain remains vulnerable to transportation delays, with global container shipping costs peaking at levels 4.7 times higher than pre-2020 averages, intensifying procurement risks and affecting lead times for radiator components.

Transition to Electric Vehicles Potentially Reducing Traditional Radiator Demand

While electrification creates opportunities for advanced thermal management solutions, the shift away from internal combustion engines presents structural challenges for conventional radiator applications, as fully electric vehicles eliminate traditional engine cooling requirements that have historically driven market demand. Battery electric vehicles require fundamentally different thermal architecture compared to combustion engines, potentially reducing the number of radiators per vehicle or shifting demand toward specialized low-temperature cooling loops with different design specifications and lower unit values. This transition introduces market uncertainty as manufacturers must balance investments between declining combustion engine applications and emerging electric vehicle thermal systems, while managing product portfolio transitions across different vehicle segments adopting electrification at varying rates influenced by regional infrastructure development, consumer preferences, and government incentives.

Opportunity - Emerging Markets Vehicle Production Expansion and Aftermarket Growth

Rapid motorization across emerging economies, including India, ASEAN nations, Brazil, and Africa presents substantial opportunities for both original equipment manufacturers and aftermarket radiator applications in the automotive radiator market. India produced over 31 million vehicles in FY 2025 and exported 5.3 million units, creating dual prospects for OEM finishing-line supplies and aftermarket demand through extensive domestic retail networks addressing replacement and upgrade requirements. Brazil's automotive sector demonstrated 14% year-over-year sales growth in 2024, highlighting demand for competitively priced cooling solutions driven by local consumer preferences for flexible-fuel and hybrid vehicles that require robust thermal management across varied fuel types. These markets provide cost-sensitive yet high-volume opportunities for manufacturers equipped with efficient distribution channels, localized production facilities, and product lines tailored to regional climate conditions, vehicle usage patterns, and price sensitivities.

Advanced Materials and Intelligent Thermal Management Technologies

Technological convergence presents transformative opportunities through the development of lightweight materials, intelligent coatings, and integrated sensor technologies that enhance radiator performance while addressing sustainability imperatives. The automotive wheel coating sector, valued at US$ 3.3 billion in 2025 and projected to reach US$ 4.7 billion by 2032, demonstrates parallel innovation trajectories with powder and ceramic coating technologies that improve corrosion resistance and durability, concepts equally applicable to radiator manufacturing optimization. Aluminum radiator adoption continues expanding due to the weight advantages of 30% to 40% lighter construction compared to copper-brass alternatives, directly improving vehicle fuel efficiency while offering superior corrosion resistance and seamless brazed construction, reducing leak risks.

Category-wise Analysis

By Product Type Insights

Crossflow radiator designs hold approximately 58% market share in 2026, driven by their superior cooling efficiency and optimal fitment in modern low-profile vehicle architectures. Crossflow configurations position inlet and outlet tanks on opposite sides, enabling longer tube lengths and increased surface area for heat dissipation within compact horizontal spaces that characterize contemporary vehicle design. This architecture proves particularly advantageous for passenger cars and sedans where engine bay height constraints favor wider, flatter cooling system layouts. Crossflow radiators deliver enhanced thermal performance for downsized turbocharged engines generating concentrated heat loads, while accommodating integration with air conditioning condensers and additional cooling modules in increasingly complex thermal management systems.

By Sales Channel Insights

Original equipment manufacturer channels dominate with approximately 72% market share in 2026, reflecting direct integration of radiators into vehicle assembly lines where performance consistency, regulatory compliance, and lifecycle reliability requirements drive stable procurement volumes. OEM applications benefit from coordinated engineering specifications, quality control protocols, and long-term supply agreements that ensure radiators precisely match vehicle thermal requirements across diverse operating conditions. Manufacturers supplying OEM channels maintain close collaborative relationships with automotive producers throughout product development cycles, enabling customization of radiator designs for specific vehicle platforms, engine configurations, and market requirements. The aftermarket segment, representing approximately 28% share, experiences steady growth driven by an expanding global vehicle fleet requiring replacement components due to wear, damage, or performance upgrades.

By Vehicle Type Insights

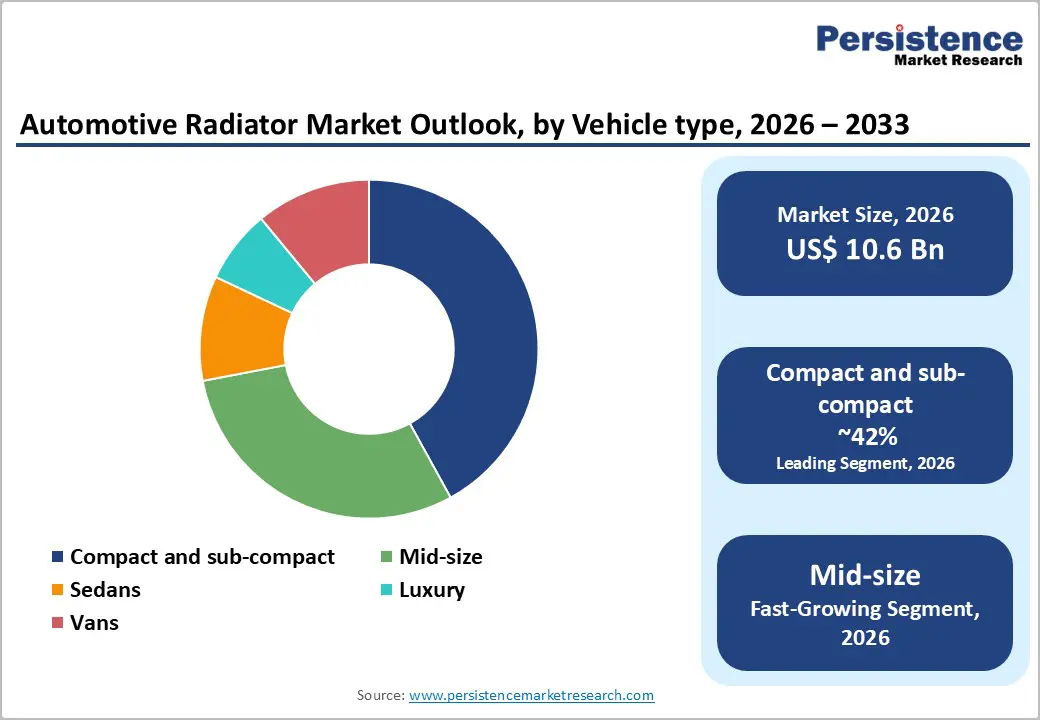

Compact and sub-compact vehicles collectively represent approximately 42% market share in 2026, reflecting their dominance in global passenger car sales particularly across price-sensitive emerging markets and urban mobility applications. These vehicle segments prioritize cost-effective cooling solutions featuring aluminum-plastic radiator constructions that balance thermal performance with manufacturing economies and weight reduction objectives. Sedan and mid-size vehicle categories account for approximately 35% share, typically specifying more robust radiator designs with enhanced capacity to support larger displacement engines, extended highway operation requirements, and premium market expectations for durability and reliability. Luxury vehicle segments, though representing a smaller volume share of approximately 12%, command premium radiator specifications incorporating advanced materials, integrated sensors for thermal monitoring, and sophisticated designs supporting high-performance engines generating substantial heat output.

By Material Insights

Aluminum-plastic composite radiators command approximately 64% market share in 2026, establishing clear leadership through an advantageous combination of lightweight construction, cost-effectiveness, corrosion resistance, and manufacturing efficiency. These radiators feature aluminum core construction with plastic end tanks, delivering weight reductions supporting fuel efficiency objectives while offering excellent thermal conductivity and recyclability aligning with automotive industry sustainability initiatives. Aluminum radiators accelerate cooling of heated coolant through superior heat absorption and conduction properties compared to alternative materials, while brazed all-aluminum construction eliminates soldered joints that create thermal resistance and potential leak points. The projected absolute dollar opportunity for aluminum materials exceeds US$ 12.6 billion between 2024 and 2032, reflecting sustained adoption across passenger vehicles, light commercial vehicles, and electric vehicle applications.

Regional Insights and Trends

North America Automotive Radiator Market Trends

North America accounts for approximately 24% of the global automotive radiator market, with the United States representing the dominant country market driven by a substantial vehicle fleet size, robust automotive manufacturing presence, and stringent regulatory frameworks governing fuel efficiency and emissions. The U.S. market demonstrates steady growth supported by Corporate Average Fuel Economy standards compelling manufacturers to optimize engine thermal management, while Environmental Protection Agency oversight of automotive refinishing processes and component manufacturing ensures environmental compliance throughout supply chains.

North American market dynamics reflect a balanced emphasis on supporting traditional internal combustion engine vehicles that continue dominating the fleet while preparing for electrification transition, with manufacturers investing in dual-capability production facilities accommodating both conventional and electric vehicle thermal management requirements. The region witnesses significant activity in pickup truck and SUV segments where radiator specifications address towing capacity requirements, off-road operating conditions, and performance applications demanding enhanced cooling capacity.

Europe Automotive Radiator Market Trends

Europe represents approximately 28% of global market share, with Germany establishing leadership as the continent's largest automotive production base, manufacturing 4.1 million cars in 2024 and maintaining strength in premium vehicle segments where approximately 60% of global premium cars originate. The European market operates under exceptionally stringent regulatory frameworks, including REACH regulations governing chemical substances, updated Euro 7 emission standards, and EU Green Deal commitments mandating substantial carbon footprint reductions across automotive manufacturing and operations.

Germany, the United Kingdom, and France lead regional innovation through substantial research and development investments in electric vehicle-linked thermal management solutions, composite-compatible cooling system designs, and intelligent sensor integration enabling predictive maintenance and performance optimization. European manufacturers demonstrate expertise in premium radiator applications incorporating sophisticated materials, multi-circuit designs supporting complex thermal architectures, and aesthetic considerations reflecting luxury vehicle brand expectations.

Asia Pacific Automotive Radiator Market Analysis

Asia Pacific dominates global market geography with approximately 40% share, led by East Asia's 32% contribution, driven by China's position as the world's largest vehicle production hub and rapidly expanding electric vehicle adoption. China manufactured approximately 23 million cars in 2024, benefiting from raw material availability, a cost-effective workforce, and comprehensive automotive supply chain infrastructure supporting radiator production at competitive price points serving both domestic consumption and export markets.

Japan maintains innovation leadership through companies, including Denso Corporation and Marelli, developing radiators with integrated thermal sensors, improved heat transfer performance, and reduced carbon footprints aligned with stringent domestic efficiency standards and global export market requirements. India emerges as a significant growth market producing over 31 million vehicles in FY 2025 with exports of 5.3 million units, supported by government-led automotive production-linked incentive schemes, rising disposable incomes, and growing consumer vehicle ownership aspirations.

Competitive Landscape

The global automotive radiator market exhibits moderately consolidated competitive dynamics, with leading multinational corporations commanding significant market shares estimated collectively at 50% to 55% of total market value, while numerous regional and specialized manufacturers contribute diversity across geographic markets and vehicle segments.

Major participants pursue vertical integration strategies incorporating design engineering, component manufacturing, assembly operations, and aftermarket distribution to capture value across the supply chain while ensuring quality control and responsiveness to customer requirements. The market structure supports differentiation through advanced materials expertise, particularly in aluminum processing and composite integration, intelligent system development incorporating sensors and connectivity features.

Key Developments:

- In October 2024, Valeo S.A. and MAHLE GmbH Joint Development Agreement for Electric Vehicle Thermal Management. Valeo S.A. and MAHLE GmbH expanded their strategic partnership through a Joint Development Agreement combining Valeo's expertise in electric motors and highly efficient inverters with MAHLE's magnet-free rotor and contactless transmitter technology to develop innovative thermal management solutions for upper segment electric vehicles.

- In November 2024, Valeo S.A. and Modine Manufacturing Company Strategic Partnership for High-Performance Aluminum Radiators. Valeo S.A. announced a strategic partnership with Modine Manufacturing Company to co-develop high-performance aluminum radiators specifically optimized for electric and hybrid vehicle applications requiring advanced thermal management capabilities.

Companies Covered in Automotive Radiator Market

- Valeo S.A.

- PWR Advanced Cooling Technology

- Calsonic Kansei Corporation

- Denso Corporation

- MAHLE GmbH

- Zhejiang Yinlun Machinery Co.

- Ltd, Sanden Holdings Corporation

- T.RAD Co., Ltd

- TYC Brothers Industrial Co. Ltd.

- Nissens A/S

- Modine Manufacturing Company

- Keihin Corporation and Banco Products (I) Ltd.

- Other Key Players

Frequently Asked Questions

The global Automotive Radiator Market is valued at US$ 10.6 Bn in 2026 and is projected to reach US$ 15.2 Bn by 2033, expanding at a compound annual growth rate of 5.2% during the forecast period.

Rapid electrification and hybrid vehicle adoption represent the primary growth driver, as battery electric vehicles and plug-in hybrids require sophisticated low-temperature heat exchangers for battery cooling, power electronics thermal management, and motor temperature control.

Significant opportunities emerge from emerging markets vehicle production expansion, with India producing over 31 million vehicles in FY 2025 and Brazil demonstrating 14% year-over-year sales growth, creating substantial original equipment manufacturer and aftermarket demand.

Asia Pacific dominates the global market with approximately 40% share, led by East Asia, contributing 32%, driven by China's position manufacturing 23 million cars in 2024, with a comprehensive automotive supply chain infrastructure and rapidly expanding electric vehicle adoption.