- Automotive Components & Materials

- Automotive Operating System Market

Automotive Operating System Market Size, Share, and Growth Forecast 2026 – 2033

Automotive Operating System Market by OS Type (QNX, Android, Linux, Windows), Application (Infotainment System, ADAS & Safety System, Connected Services, Body Control & Comfort System, Powertrain Control, Others), Vehicle Type (Passenger Car, Light Commercial Vehicle, Heavy Commercial Vehicle), and Regional Analysis for 2026–2033

Automotive Operating System Market Size and Trend Analysis

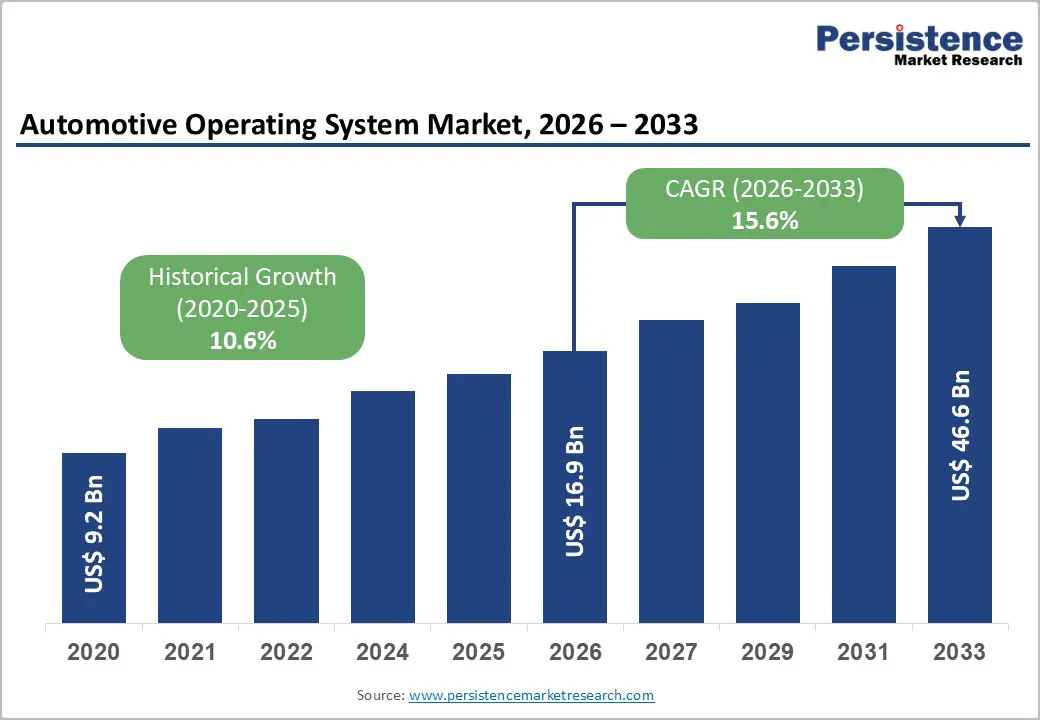

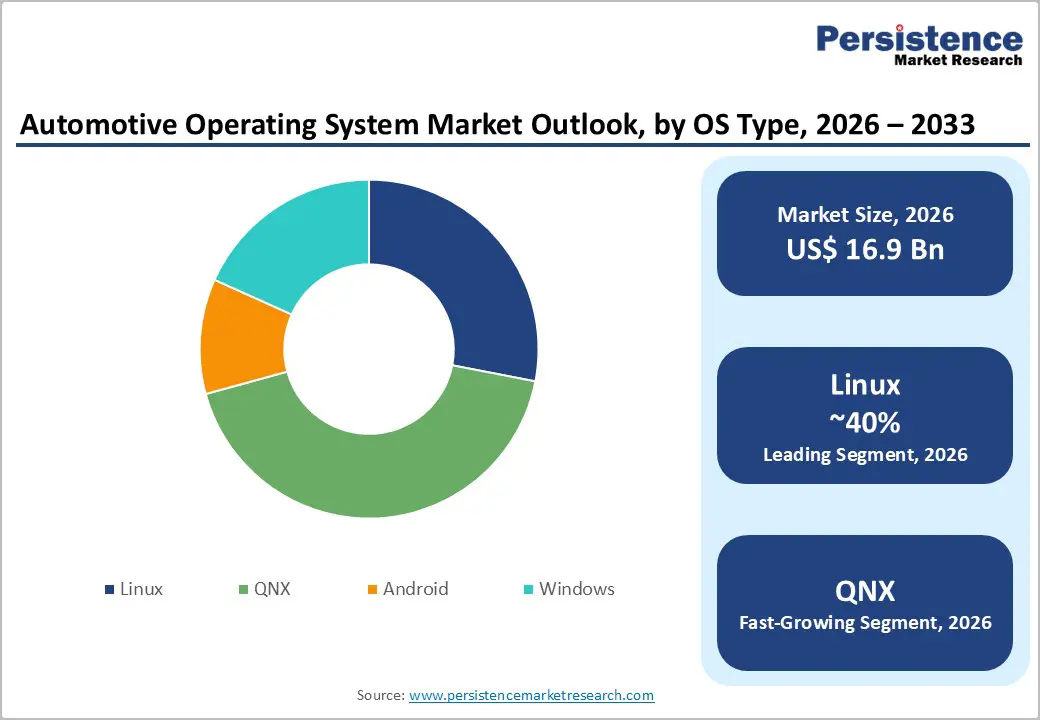

The global Automotive Operating System market is valued at US$ 16.9 Bn in 2026 and is projected to reach US$ 46.6 Bn by 2033, growing at a CAGR of 15.6% between 2026 and 2033.

The rapid proliferation of connected and software-defined vehicles is the primary catalyst driving the adoption of automotive operating systems globally. Modern vehicles increasingly rely on sophisticated OS platforms to manage infotainment, advanced driver assistance, real-time diagnostics, and over-the-air updates. According to the International Energy Agency (IEA), global electric vehicle sales surpassed 10 million units in 2022 and continued to accelerate through 2024, with EVs inherently demanding more complex software architectures.

Key Industry Highlights:

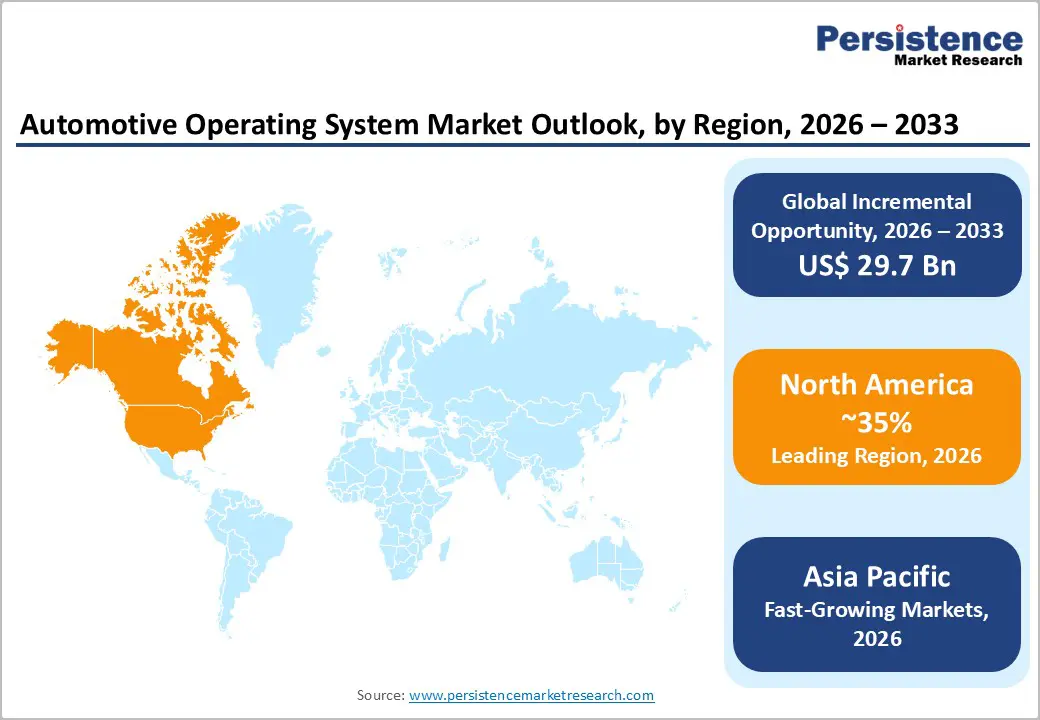

- Leading Region: North America leads the automotive OS market owing to its advanced EV ecosystem, strong regulatory framework under NHTSA, and the presence of key innovators such as BlackBerry QNX and Google LLC, supported by a high vehicle software content ratio per unit.

- Fastest Growing Region: Asia Pacific is the fast-growing region, propelled by China's dominant NEV market, Indian government-backed connected vehicle mandates (AIS-140), and Japan's OEM investments in collaborative open-source OS platforms like AGL.

- Dominant Segment: The infotainment system application segment dominates with approximately 34% revenue share, underpinned by consumer demand for seamless digital in-cabin experiences and broad adoption of Android Automotive OS and AGL platforms.

- Fastest Growing Segment: The ADAS & Safety System application segment is the fastest growing category, driven by EU GSR 2022/2019 mandates effective July 2024 and NHTSA safety requirements accelerating deployment of safety-certified OS solutions across new vehicle models.

- Key Opportunity: Over-the-air (OTA) software update platforms present a significant monetization opportunity, with connected vehicle services projected to generate US$ 750 billion annually by 2030, enabling OS vendors to support recurring post-sale revenue for automakers.

DRO Analysis

Drivers - Surge in Software-Defined Vehicle Architecture Adoption

The global automotive industry is undergoing a fundamental transformation toward software-defined vehicles (SDVs), where the vehicle's core functions are governed by software layers running on centralized OS platforms rather than distributed embedded controllers. According to McKinsey & Company, software content in a premium vehicle is expected to account for over 30% of total vehicle value by 2030.

The transition is driven by consumer demand for seamless digital experiences, continuous feature updates, and cybersecurity compliance. Original equipment manufacturers (OEMs), including Volkswagen Group, General Motors, and Toyota Motor Corporation, have unveiled dedicated software subsidiaries to accelerate OS standardization, directly stimulating demand for robust and scalable automotive OS platforms across model lineups.

Regulatory Push for Advanced Driver Assistance and Safety Compliance

Stringent government regulations mandating the integration of ADAS functionalities are creating sustained demand for real-time, safety-certified automotive operating systems. The European Union's General Safety Regulation (GSR) 2022/2019 mandates the inclusion of intelligent speed assistance, autonomous emergency braking, and lane-keeping systems across all new vehicles sold in EU markets starting July 2024.

Similarly, the U.S. National Highway Traffic Safety Administration (NHTSA) has reinforced requirements for collision avoidance technologies. These mandates necessitate OS platforms that are certified under functional safety standards such as ISO 26262 (ASIL-D) and AUTOSAR Adaptive, fuelling demand for safety-grade OS solutions like QNX Neutrino and certified Linux-based stacks.

Restraints - High Development and Certification Costs

Developing and certifying an automotive-grade OS for functional safety compliance is an extraordinarily resource-intensive process. Achieving ISO 26262 ASIL-D certification required for safety-critical domains like steering and braking can cost upward of US$ 10 million per project and take three to five years, as reported by engineering consultancies familiar with automotive software validation.

This creates a significant barrier for smaller Tier-2 suppliers and new entrants, effectively consolidating the market around a handful of large incumbents. The ongoing certification burden slows the pace at which new OS innovations can reach production vehicles and discourages investment from startups lacking legacy automotive relationships.

Fragmentation and Interoperability Challenges

The automotive OS landscape is highly fragmented, with multiple incompatible platforms, QNX, Android Automotive OS, Linux-based AGL (Automotive Grade Linux), and proprietary stacks competing without universal standards for middleware and application interfaces. This fragmentation complicates integration with third-party applications and hardware from diverse suppliers.

According to the Linux Foundation's Automotive Grade Linux (AGL) project reports, over 140 member companies are working to harmonize standards, yet automakers still face considerable overhead in porting software across different OS environments, increasing total development cost and time-to-market for connected vehicle features.

Opportunities - Expanding Electric Vehicle Fleet Creates Demand for Next-Generation OS Platforms

The global shift toward electric mobility presents a transformative opportunity for automotive OS providers. EVs, by design, require centralized electronic architectures and sophisticated energy management software, making them ideal platforms for advanced OS deployment. The IEA's Global EV Outlook 2024 projects the global EV stock to exceed 300 million vehicles by 2030.

This electrification trajectory will require OS platforms capable of managing battery management systems (BMS), regenerative braking algorithms, thermal management, and real-time connectivity in a unified software environment. Companies that develop modular, scalable, and energy-efficient OS architectures tailored for EV platforms will capture a disproportionate share of the market growth, particularly among new EV-native OEMs in China, Europe, and North America.

Over-the-Air (OTA) Update Capabilities as a Revenue-Generating Platform

Automotive operating systems increasingly serve as the foundation for post-sale revenue generation through over-the-air (OTA) software updates, subscription-based feature unlocking, and connected services monetization. Tesla, Inc. pioneered this model and demonstrated that a software-first OS strategy can generate substantial recurring revenue. McKinsey estimated that connected vehicle services could generate US$ 750 billion in annual revenue globally by 2030.

Traditional OEMs such as BMW Group and Mercedes-Benz AG have already launched paid OTA feature subscription services. This shift from one-time hardware revenue to recurring software revenue creates a compelling long-term opportunity for OS vendors to embed deeply within vehicle lifecycle monetization strategies, especially as vehicles remain in service for 10–15 years.

Category-wise Analysis

OS Type Insights

Among all OS types, Linux-based platforms, most notably automotive grade Linux (AGL)command the largest share, accounting for approximately 38% of the overall automotive OS market. Linux's dominance is underpinned by its open-source architecture, rich developer ecosystem, and strong adoption by OEMs seeking cost-effective, customizable solutions. The Linux Foundation's AGL project counts over 140 member organizations, including Toyota, Suzuki, and Panasonic, reflecting deep industry trust.

Furthermore, Linux platforms benefit from extensive toolchain support, rapid iteration cycles, and compatibility with modern container-based software development paradigms, making them the preferred choice for infotainment and connected services across both passenger and commercial vehicle segments.

Application Insights

The infotainment system application holds the leading position in the automotive OS market, representing approximately 34% of total market revenue. Infotainment systems are the most visible and consumer-facing application of automotive OS technology, integrating navigation, media, voice assistants, and smartphone mirroring. Consumer expectations for in-vehicle digital experiences, benchmarked against smartphones, continue to elevate OEM investments in infotainment OS platforms.

According to a J.D. Power survey, infotainment system quality consistently ranks among the top three factors influencing vehicle purchase decisions in North America. The segment's dominance is further reinforced by the widespread integration of platforms like Android Automotive OS and Apple CarPlay compatibility layers, driving continuous OS upgrades and replacements.

Vehicle Type Insights

The Passenger Car segment dominates the vehicle type category, accounting for approximately 62% of the automotive OS market. This dominance is driven by the sheer volume of global passenger car production and the accelerating pace of feature integration in mid-to-premium segments. According to the International Organization of Motor Vehicle Manufacturers (OICA), global passenger car production exceeded 70 million units in 2023, with a growing proportion equipped with advanced infotainment and ADAS systems requiring sophisticated OS solutions.

The rise of Chinese new energy vehicle (NEV) brands such as BYD Co., Ltd. and NIO Inc., which prioritize software-rich in-cabin experiences, has further amplified OS adoption within the passenger car category, sustaining its dominant share.

Regional Analysis

North America Automotive Operating System Market Trends & Analysis

North America represents one of the most mature and technologically advanced automotive OS markets, accounting for approximately 28% of global revenues. The region benefits from a strong ecosystem of technology suppliers, a well-developed regulatory framework, and the presence of pioneering EV manufacturers. The U.S. Inflation Reduction Act (IRA) of 2022 has accelerated domestic EV adoption by providing consumer tax credits of up to US$ 7,500 per vehicle, indirectly stimulating demand for advanced automotive OS platforms. Major players such as BlackBerry QNX, headquartered in Waterloo, Ontario, and Silicon Valley technology giants, including Google LLC and Apple Inc., have established the region as a critical hub for automotive software innovation.

U.S. Automotive Operating System Market Size

The U.S. accounts for the largest market within North America, estimated at approximately US$ 3.8 Bn in 2026. Strong OEM investment in vehicle software platforms, combined with federal safety mandates from NHTSA for collision avoidance and automated driving systems, underpins robust demand. The U.S. also leads in connected vehicle infrastructure deployment, with V2X (Vehicle-to-Everything) pilot programs expanding across multiple states.

Europe Automotive Operating System Market Trends, Drivers & Insights

Europe holds a substantial share of the global automotive OS market, driven by the region's stringent safety and emissions regulations and the presence of world-class automotive OEMs. The European Union's General Safety Regulation (EU GSR 2022/2019), effective July 2024, mandates a comprehensive suite of ADAS features for all new vehicles, creating a structural and sustained demand for safety-certified OS platforms. Germany's Verband der Automobilindustrie (VDA) reported that German Automotive R&D expenditure exceeded € 22 billion in 2022, a significant portion directed toward software and connectivity.

Germany Automotive Operating System Market Size

Germany is Europe's largest automotive OS market, estimated at approximately US$ 1.7 Bn in 2026. As home to Volkswagen AG, BMW Group, and Mercedes-Benz AG, Germany generates substantial OS procurement and in-house development activity, particularly for premium ADAS and infotainment applications.

U.K. Automotive Operating System Market Size

The U.K. automotive OS market is estimated at approximately US$ 680 Mn in 2026. The market is supported by the U.K. government's Zero Emission Vehicle (ZEV) mandate requiring 22% of new car sales to be zero-emission by 2024, progressively scaling to 100% by 2035, stimulating automotive software investment.

France Automotive Operating System Market Size

The French automotive OS market is valued at approximately US$ 520 Mn in 2026. Stellantis N.V. and Renault Group, both headquartered in France, have announced significant investments in software-defined vehicle platforms, including dedicated OS development centers, stimulating the domestic market.

Asia Pacific Automotive Operating System Market Drivers & Analysis

Asia Pacific is the fast-growing market for automotive operating systems and is forecast to register the highest CAGR over the 2026–2033 period. China alone accounted for over 35% of global new energy vehicle sales in 2023, according to the China Association of Automobile Manufacturers (CAAM). The region's dynamic NEV ecosystem, featuring vertically integrated software-hardware stacks from companies such as BYD, NIO, and Li Auto, is establishing new benchmarks for OS sophistication

China Automotive Operating System Market Size

China is the world's largest automotive OS market by volume, with a national market size estimated at approximately US$ 3.2 Bn in 2026. Government support for indigenized automotive operating systems, including homegrown platforms from Huawei Technologies Co., Ltd. and Baidu Apollo alongside China's NEV leadership, makes it the most dynamic growth arena globally.

India Automotive Operating System Market Size

India's automotive OS market is estimated at approximately US$ 480 Mn in 2026. India's ambitious AIS-140 connected vehicle standard, mandating GPS tracking and emergency response for commercial vehicles, is a key regulatory driver. Rapidly growing domestic EV adoption and OEM investments by Tata Motors and Mahindra & Mahindra are accelerating OS deployment.

Japan Automotive Operating System Market Size

Japan's automotive OS market is valued at approximately US$ 1.1 Bn in 2026. Toyota Motor Corporation's Arene OS initiative and collaborative efforts within the Automotive Grade Linux (AGL) consortium reflect Japan's commitment to building globally competitive OS platforms for next-generation vehicles.

Competitive Landscape

The global automotive operating system market exhibits a moderately consolidated structure, with a small number of established technology and software companies commanding significant market influence alongside a fragmented tail of niche and regional players.

BlackBerry Limited (QNX), Google LLC (Android Automotive OS), and Linux Foundation (AGL) collectively anchor the market. Key competitive strategies include deep OEM integration agreements, investment in functional safety certifications, and strategic acquisitions.

Key Developments

- In June 2025, NXP Semiconductors N.V. announced the acquisition of TTTech Auto GmbH to strengthen its position in the automotive operating system market. The deal aims to accelerate software-defined vehicle development by combining NXP Semiconductors N.V.’s high-performance processors with TTTech Auto GmbH’s expertise in safety-critical automotive middleware and real-time networking solutions.

- In May 2025, Volvo Cars and Google LLC expanded their strategic partnership to integrate Google’s Gemini AI into Volvo vehicles equipped with Android Automotive OS. This collaboration enhances in-car intelligence, enabling natural voice interaction, predictive navigation, and personalized driver assistance, reinforcing Volvo’s focus on connected, AI-driven mobility experiences.

Global Automotive Operating System Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 9.2 Bn |

|

Current Market Value (2026) |

US$ 16.9 Bn |

|

Projected Market Value (2033) |

US$ 46.6 Bn |

|

CAGR (2026-2033) |

15.6% |

|

Leading Region |

North America, 35% share |

|

Dominant Application |

Infotainment System, 35% share |

|

Top-ranking Product |

Linux-based platforms, 40% |

|

Incremental Opportunity |

US$ 29.7 Bn |

Companies Covered in Automotive Operating System Market

- BlackBerry Limited (QNX)

- Google LLC (Android Automotive OS)

- Linux Foundation (AGL)

- Microsoft Corporation

- Wind River Systems, Inc.

- Green Hills Software LLC

- ENEA AB

- OpenSynergy GmbH

- Elektrobit (EB)

- Continental AG

- Robert Bosch GmbH

- Aptiv PLC Huawei Technologies Co., Ltd.

- Baidu, Inc.

- Toyota Motor Corporation

Frequently Asked Questions

The global Automotive Operating System market is valued at approximately US$ 16.3 Bn in 2026 and is projected to reach US$ 46.6 Bn by 2033, expanding at a robust CAGR of 15.6% over the forecast period. This growth is driven by the rapid proliferation of software-defined vehicles, EV adoption, and regulatory mandates for ADAS integration.

The primary growth drivers include the global industry transition toward software-defined vehicle (SDV) architectures and stringent government safety regulations mandating ADAS features.

The Infotainment System segment holds the leading position, capturing approximately 34% of total market revenue. The segment's dominance reflects consumer demand for connected digital in-cabin experiences, broad adoption of Android Automotive OS and AGL-based platforms, and the fact that infotainment remains one of the top three purchase decision factors for vehicle buyers.

North America currently leads the global automotive OS market, accounting for approximately 28% of global revenues. The region's leadership is anchored due to BlackBerry QNX, Google LLC, and a mature EV ecosystem supported by the U.S. Inflation Reduction Act (IRA), combined with the highest per-vehicle software content ratios globally.

The key market players include BlackBerry Limited (QNX), Google LLC (Android Automotive OS), The Linux Foundation (Automotive Grade Linux), Microsoft Corporation, Wind River Systems, Inc., Green Hills Software LLC, Continental AG, Robert Bosch GmbH, Huawei Technologies Co., Ltd., and Toyota Motor Corporation (Arene OS), among others.