- Automotive Components & Materials

- Automotive Kingpin Market

Automotive Kingpin Market Size, Share, Trends, Growth, Forecasts 2025 - 2032

Automotive Kingpin Market By Product Type (Kits, Individual Parts) Sales Channel (OEM, Aftermarket), Vehicle Type (Light Commercial Vehicles, Heavy Commercial Vehicles, Off-road Vehicles), Regional Analysis 2025 - 2032

Automotive Kingpin Market Share and Trends Analysis

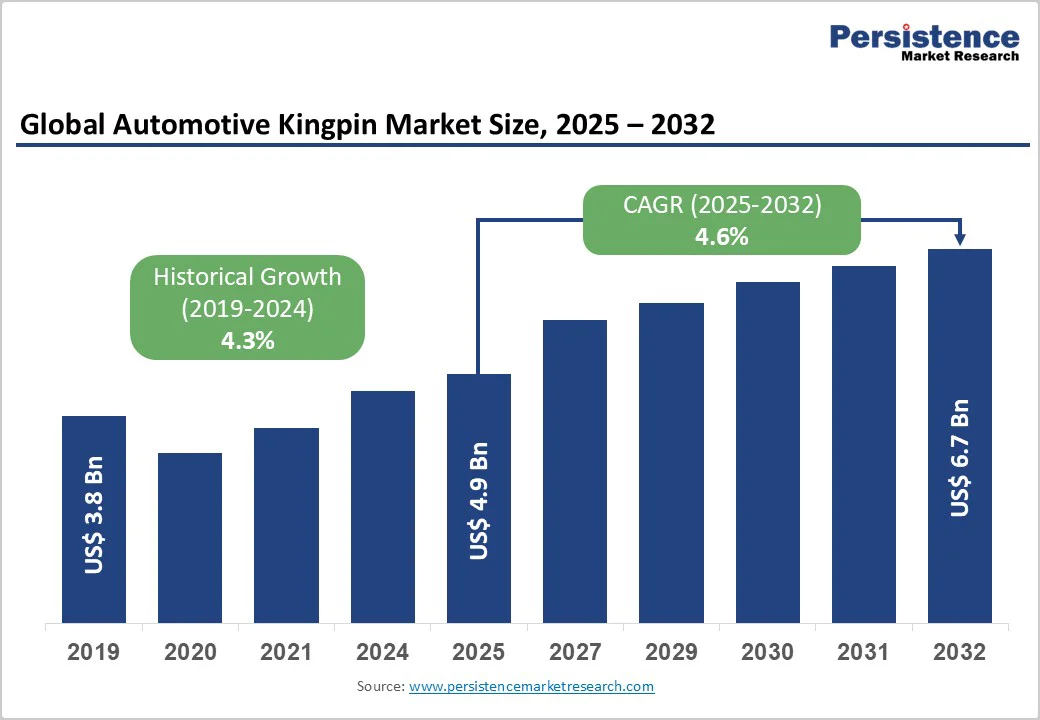

The global Automotive Kingpin Market size was valued at US$4.9 Bn in 2025 and is projected to reach US$6.7 Bn by 2032, growing at a CAGR of 4.6% between 2025 and 2032. This steady expansion reflects sustained demand from the commercial vehicle sector, driven by expanding logistics and transportation industries globally, as well as by increasing construction and mining activities that require heavy-duty vehicles equipped with reliable steering components.

The market growth is further supported by rising replacement demand in aftermarket channels as aging commercial vehicle fleets require kingpin maintenance and component upgrades, alongside continuous infrastructure development programs in emerging economies, generating substantial demand for heavy commercial vehicles.

Key Market Highlights:

- Individual Parts dominate with 72% market share while the Kits segment achieves the fastest growth at 5.5% CAGR, reflecting market preferences for both component flexibility and complete assembly solutions.

- OEM channel maintains 55% market leadership while Aftermarket grows at 5.3% CAGR, supported by expanding commercial vehicle installed base and increasing replacement demand.

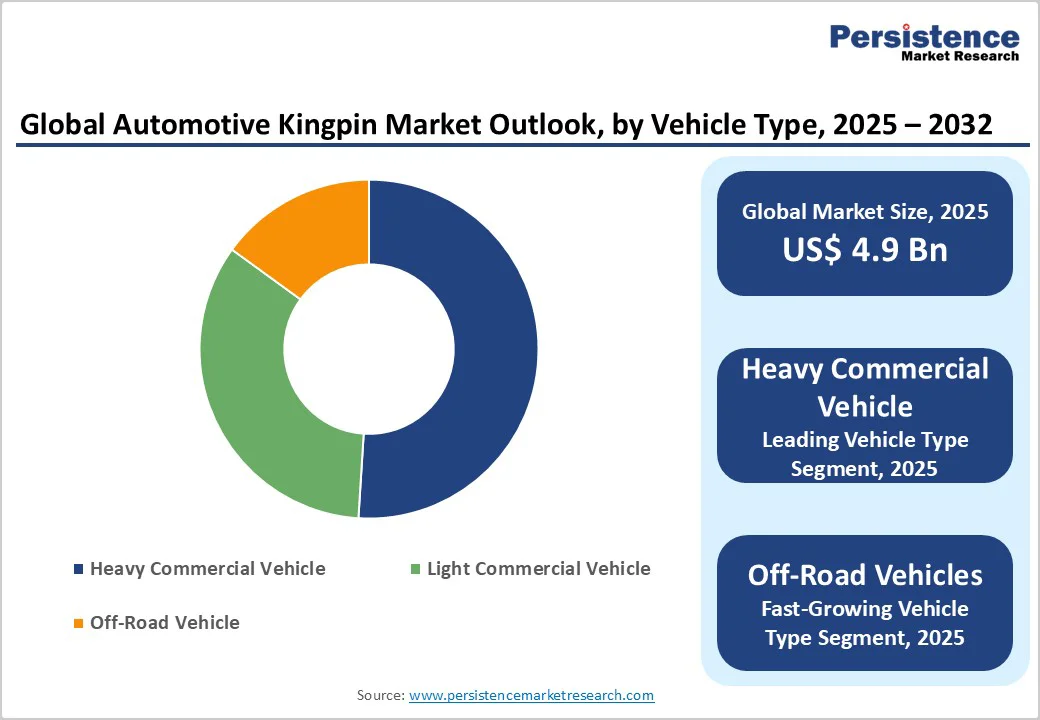

- Heavy Commercial Vehicles hold 51% share with Light Commercial Vehicles growing at 4.3% CAGR, driven by intensive HCV kingpin usage and expanding LCV deployment for last-mile logistics.

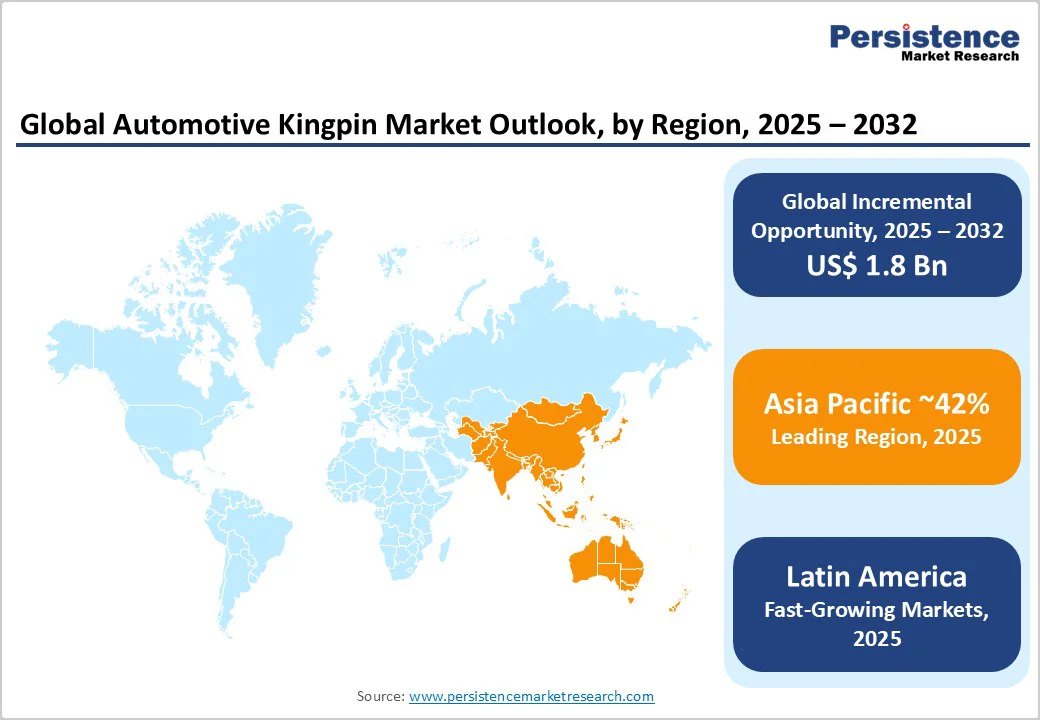

- Asia Pacific dominates with 42% global market share, Europe holds 21%, North America is poised to achieve 4.3% CAGR, reflecting regional commercial vehicle production patterns and infrastructure development.

- Top four manufacturers control approximately 30% market share in moderately fragmented competitive landscape, enabling competition through product quality, innovation, and service differentiation.

- Strategic developments focus on advanced materials, simplified installation systems, and expanded aftermarket coverage, with manufacturers investing in technology innovation and geographic expansion.

| Key Insights | Details |

|---|---|

|

Automotive Kingpin Market Size (2025E) |

US$ 4.9 Billion |

|

Market Value Forecast (2032F) |

US$ 6.7 Billion |

|

Projected Growth CAGR (2025-2032) |

4.6% |

|

Historical Market Growth (2019-2024) |

4.3% |

Market Dynamics

Driver - Expanding Global Logistics and Transportation Industry Driving Commercial Vehicle Demand

The automotive kingpin market experiences substantial growth momentum from the rapidly expanding global logistics and transportation sector, which serves as the backbone for commercial vehicle demand and subsequent kingpin requirements. The accelerating growth of the global logistics and transportation sector is fueling a surge in commercial vehicle demand, with medium and heavy commercial vehicles poised to expand at an impressive 4.4% year-over-year pace in 2025, reflecting the sector’s vital role in powering global trade and mobility.

The surge in e-commerce logistics, expected to exceed 535 billion USD in 2025, creates intense demand for last-mile delivery vehicles and long-haul freight trucks that require durable kingpin assemblies for reliable steering performance. Furthermore, the construction and mining application segment within heavy trucks is expected to expand at an accelerated pace during the forecast period, driven by massive public infrastructure spending initiatives. In India alone, the Ministry of Road Transport and Highways awarded over INR 1.2 trillion worth of road contracts in fiscal year 2023-2024, directly stimulating demand for heavy construction trucks requiring robust kingpin systems.

Infrastructure Development and Government Capital Expenditure Programs

Government-led infrastructure development initiatives across major economies serve as powerful catalysts for automotive kingpin demand through their direct impact on commercial vehicle fleet expansion and utilization rates. India's Union Budget 2023-24 allocated a capital outlay of USD 122.3 billion (INR 10 trillion) for infrastructure development, driving growth in sectors such as steel, cement, mining, and construction that are key consumers of heavy commercial vehicles equipped with kingpin steering systems. The Indian government's focus on road infrastructure, with targets to build 20 kilometers of new highway per day requiring approximately USD 41 billion in private-sector investment over three to four years, creates sustained demand for construction and logistics vehicles. China's infrastructure investments in roads have grown by over 40 times since 1990 to approximately USD 60 billion annually in 2005, with a third allocated to the National Expressway Network. The Belt and Road Initiative (BRI) has strengthened trade connections with Central Asia and Europe, leading to a need for upgraded heavy-duty trucks for transcontinental cargo, with over 60% of BRI freight moved by road. This ongoing infrastructure development increases demand as heavy commercial vehicles face accelerated kingpin wear from harsh conditions, requiring more frequent maintenance.

Restraint - Competition from Alternative Steering Technologies, Including Ball Joint Systems

The automotive kingpin market faces significant competitive pressure from ball joint steering systems, which have gained widespread adoption in modern vehicle designs due to cost efficiency advantages and simplified manufacturing processes. The automotive industry's historical transition from kingpin to ball joint assemblies was driven primarily by cost efficiency considerations, as ball joints can be manufactured with similar tolerances to tie rod ends but at lower production costs. Ball joints offer comparable steering functionality while requiring less complex installation procedures and eliminating the need for specialized reaming equipment required for traditional kingpin installations.

The average ball joint price ranges from USD 20 to USD 80 per unit, potentially offering cost advantages over complete kingpin kits in certain applications. Ball joint systems provide adequate performance for lighter commercial vehicles and passenger vehicles, leading original equipment manufacturers to specify ball joints for vehicle categories that previously utilized kingpin assemblies, thereby constraining kingpin market expansion into these segments. Industry experience shows kingpins still outperform in heavy-duty use, as ball joints often fail in Dana 60 axles with weaker knuckles under extreme loads. Yet, the rise of ball joint delete systems and retrofit kits is reshaping the market, driving fragmentation and competitive pressure on traditional kingpin pricing and share.

Raw Material Price Volatility and Supply Chain Constraints

The automotive kingpin market experiences significant cost pressures from fluctuations in raw material prices, particularly steel and specialty alloys that constitute the primary materials for kingpin manufacturing, creating profitability challenges for manufacturers and pricing uncertainty for purchasers. Kingpins are manufactured predominantly from high-strength steel and forged steel materials that require precise metallurgical properties to withstand extreme steering loads and wear conditions. Global steel price volatility, driven by changing commodity markets, energy costs, and international trade dynamics, directly impacts kingpin manufacturing costs and profit margins throughout the supply chain. The automotive industry's susceptibility to global economic downturns presents additional restraint on market expansion, as commercial vehicle sales decline during economic contractions, reducing new kingpin demand from original equipment manufacturers.

Supply chain disruptions, including those experienced during recent global events, have caused delivery delays and increased logistics costs for kingpin components, affecting both manufacturers and end users. The specialized nature of kingpin manufacturing requires significant capital investment in forging equipment, heat-treatment facilities, and precision-machining capabilities, creating barriers to rapid capacity expansion when demand surges. Raw material procurement challenges are particularly acute for manufacturers serving multiple geographic markets, as transportation costs and import duties can significantly impact delivered component costs, especially for aftermarket distributors maintaining inventory across diverse regions.

Opportunity - Technology Innovation in Materials and Integrated Steering Systems

Advancing material science and steering system integration technologies present significant opportunities for kingpin manufacturers to develop differentiated products offering superior performance, extended service life, and compatibility with emerging vehicle technologies, including electric commercial vehicles. The development of advanced kingpin materials, including high-strength alloys and composite materials, is improving durability and longevity while reducing maintenance costs and improving vehicle efficiency.

Modern kingpins designed to withstand higher stress levels enable commercial vehicles to operate with heavier payloads and more demanding duty cycles, creating value propositions for fleet operators seeking to maximize asset utilization. The global electric commercial truck market is experiencing rapid growth, particularly in China, where adoption levels are projected to reach 46% of sales by 2030, supported by government subsidies, declining battery costs, and heightened manufacturing competition. Electric trucks demand advanced kingpin designs to handle unique weight distribution, regenerative braking, and steering-assist systems, opening the door to next-gen, EV-focused solutions. Integrating sensors and condition monitoring enables predictive maintenance, optimizing replacements based on real wear data. Meanwhile, R&D in lightweight kingpins supports vehicle efficiency and payload gains, allowing innovators to capture premium market positioning.

Expansion of Aftermarket Distribution Channels and Service Networks

The growing complexity of commercial vehicle maintenance and the increasing specialization required for kingpin service create opportunities for manufacturers and distributors to expand aftermarket presence through enhanced service networks, technical training programs, and comprehensive product portfolios. The aftermarket segment is witnessing significant growth due to the increasing need for kingpin replacements in aging commercial vehicle fleets, with many fleet operators opting for high-quality replacement parts to ensure reliability and minimize downtime. Manufacturers can develop comprehensive kingpin kits incorporating all necessary components, including pins, bearings, bushings, seals, and installation hardware to simplify replacement procedures and reduce technician labor time. Stemco's Kaiser QwikKit kingpin kit provides 2-3 times the life cycle of standard kingpin kits and does not require reaming, demonstrating how product innovation can create competitive advantages in aftermarket channels.

The development of universal kingpin solutions compatible with multiple vehicle platforms enables distributors to reduce inventory complexity while maintaining broad application coverage, improving supply chain efficiency, and customer service levels. Strategic partnerships with commercial vehicle dealers, independent repair facilities, and fleet maintenance operations can expand market reach and create recurring revenue streams through authorized service networks. Manufacturers offering technical training programs, installation tools, and comprehensive documentation support can differentiate their products and build customer loyalty in competitive aftermarket environments where quality, availability, and technical support influence purchasing decisions.

Category-wise Analysis

Product Type Insights

Individual parts maintain market leadership with a commanding 72% market share, reflecting the segment's dominance in both original equipment manufacturing and aftermarket applications, where components including pins, bearings, bushings, seals, and related hardware, are sold separately rather than in complete assemblies. This substantial market share stems from the flexibility individual parts provide to maintenance technicians and fleet operators who can replace specific worn components rather than complete kingpin assemblies, enabling cost optimization and targeted repairs based on actual component condition. The individual parts segment gains strength from wide distribution networks, versatile fitment across commercial vehicle platforms, and seamless integration with existing inventory systems. High-volume production further enhances cost efficiency, enabling competitive pricing without compromising the stringent quality standards essential for steering system reliability.

Kits represent the fastest-growing segment driven by increasing demand for complete kingpin assemblies that simplify installation procedures, reduce labor time, and ensure component compatibility throughout the steering system. The kits segment is gaining traction as fleet operators favor all-in-one replacement solutions that cut downtime and guarantee consistent quality. By bundling components, kingpin kits simplify sourcing, lower procurement costs, and ensure parts meet OEM standards. Growth is further boosted by advanced designs using superior materials, precision-matched parts, and innovations like STEMCO’s Kaiser QwikKit, which eliminates reaming and extends service life.

Sales Channel Insights

Original Equipment Manufacturers (OEM) channel maintains market dominance with 55% market share, reflecting the channel's control over new commercial vehicle production and its role in specifying kingpin systems that meet vehicle design requirements and performance standards. OEM dominance stems from long-term supply relationships with commercial vehicle manufacturers, integrated product development processes, and quality assurance requirements that favor established kingpin suppliers with proven track records. The OEM channel benefits from early involvement in vehicle development programs, enabling kingpin suppliers to optimize designs for specific applications, integrate with complementary steering components, and achieve cost efficiencies through production volumes aligned with vehicle manufacturing schedules.

Aftermarket channels demonstrate robust growth, driven by expanding commercial vehicle installed base requiring replacement components, increasing vehicle operating lifespans, and growing sophistication of independent service providers capable of performing kingpin installations. The development of new technologies in the automotive industry, resulting in longer vehicle lifespans, is driving demand for repair and maintenance services, which in turn is increasing sales of automotive kingpins in the aftermarket. The aftermarket segment benefits from increasing availability of high-quality replacement kingpins that meet or exceed OEM specifications at competitive price points, supported by growing distribution networks and technical support resources that enable independent service providers to perform professional installations.

Vehicle Type Insights

Heavy Commercial Vehicles (HCV) dominate the market with approximately 51% market share, reflecting this segment's intensive kingpin usage requirements and the critical role kingpins play in heavy-duty steering systems supporting substantial vehicle weights and demanding operating conditions. Heavy commercial vehicles experience higher kingpin replacement rates due to extreme loads, harsh operating environments, and intensive duty cycles that accelerate component wear. The segment encompasses various applications, including long-haul freight trucks, construction vehicles, mining equipment, and specialized heavy haulers, each requiring robust kingpin assemblies engineered to withstand specific operating demands. The HCV segment's market dominance is reinforced by regulatory requirements for commercial vehicle safety inspections that identify worn kingpins requiring replacement, creating sustained aftermarket demand.

Light Commercial Vehicles (LCV) represent the fastest-growing vehicle segment with a positive CAGR driven by expanding last-mile delivery operations, increasing e-commerce logistics requirements, and growing adoption of commercial vans and light trucks for urban freight distribution. This accelerated growth reflects the LCV segment's expanding role in modern logistics ecosystems where efficient urban delivery networks require large fleets of smaller commercial vehicles equipped with reliable steering components. The segment benefits from increasing vehicle production to support growing delivery services, with e-commerce expansion creating sustained demand for light commercial vehicles capable of navigating urban environments while maintaining load capacity.

Regional Market Insights

North America Automotive Kingpin Market Trends

North America demonstrates a prominent CAGR of 4.3%, reflecting sustained market expansion supported by stable commercial vehicle demand, established logistics infrastructure, and ongoing fleet renewal cycles that generate consistent kingpin requirements across both OEM and aftermarket channels. The region's growth trajectory stems from resilient transportation and logistics sectors, with the United States maintaining leadership in commercial vehicle operations supported by extensive highway networks, established freight corridors, and sophisticated supply chain ecosystems.

North America contributes a substantial volume of around 15 million vehicles through its mature commercial vehicle market, according to OICA. The United States market benefits from stringent vehicle safety regulations requiring regular commercial vehicle inspections that identify worn steering components, including kingpins, creating recurring aftermarket demand. The region's commercial vehicle fleet operates in diverse applications ranging from long-haul freight to construction and municipal services, each generating specific kingpin requirements and replacement patterns.

North America's kingpin market strength reflects its advanced manufacturing capabilities, established distribution networks, and sophisticated aftermarket service infrastructure that supports both independent repair facilities and fleet maintenance operations. The region benefits from proximity to commercial vehicle manufacturing operations in the United States and Canada, enabling collaborative product development and just-in-time delivery that optimizes inventory management and reduces supply chain costs. Investment trends favor technology innovation in kingpin materials and designs, with manufacturers developing advanced products that offer extended service life, reduced maintenance requirements, and compatibility with emerging commercial vehicle technologies, including electric powertrains and advanced driver assistance systems.

Europe Automotive Kingpin Market

Europe maintains 21% of global automotive kingpin market share, positioning the region as a significant market supported by substantial commercial vehicle manufacturing, established logistics networks, and stringent vehicle safety standards that drive quality requirements for steering components. The region's market position reflects its role as a major commercial vehicle production hub, with countries including Germany, the United Kingdom, France, and Spain contributing substantial manufacturing output that generates OEM kingpin demand.

Germany leads European commercial vehicle production and kingpin adoption, benefiting from the presence of major commercial vehicle manufacturers and a sophisticated automotive supply chain that supports both domestic and export markets. The European Union's regulatory harmonization creates consistent kingpin specifications and safety requirements across member states, facilitating market efficiency and enabling manufacturers to optimize product portfolios for regional applications.

Europe's kingpin market demonstrates steady growth supported by ongoing commercial vehicle fleet renewal, increasing logistics activity driven by e-commerce expansion, and infrastructure development programs that stimulate construction vehicle demand. European fleet operators prioritize total cost of ownership efficiency, fueling demand for durable kingpin components that extend service life and reduce maintenance needs. Strong commercial vehicle bases in the U.K., France, and Spain, spanning urban logistics to long-haul freight, sustain steady OEM and aftermarket demand.

The region’s well-developed distribution networks, skilled service providers, and robust technical support further strengthen its position in the global kingpin market. The region's focus on vehicle electrification and emission reduction creates opportunities for kingpin suppliers to develop components optimized for electric commercial vehicles, which are gaining market share in urban delivery and municipal applications where zero-emission requirements influence vehicle procurement decisions.

Asia Pacific Automotive Kingpin Market Trends

Asia Pacific dominates the global automotive kingpin market with a significant market share of around 42%, establishing the region as the world's largest kingpin market, driven by massive commercial vehicle production, rapidly expanding logistics infrastructure, and substantial construction and mining activities that generate intensive kingpin requirements.

The region's market dominance stems from China's position as the world's largest commercial vehicle manufacturer and consumer, with annual production exceeding 31 million vehicles in 2024, including approximately 3.8 million commercial vehicles according to OICA statistics. China's heavy truck sales exceeded 1 million units in 2023, with Class 8 trucks reflecting intense demand for long-haul transport supported by the world's largest e-commerce ecosystem and expanding industrial production. India contributes substantially to the regional market value through commercial vehicle production of approximately 1.02 million units in 2024, supported by government infrastructure initiatives and growing logistics requirements. Japan and South Korea provide additional market scale through advanced commercial vehicle manufacturing and sophisticated steering component technologies.

Competitive Landscape

The global automotive kingpin market demonstrates moderate concentration with the leading manufacturers accounting for approximately 25 to 30% market share, creating a competitive landscape characterized by established global suppliers, regional manufacturers, and specialized component producers.

The market exhibits fragmented characteristics with numerous participants serving diverse geographic markets and vehicle applications, enabling competition based on product quality, pricing, technical support, and distribution capabilities rather than pure market dominance by a limited number of suppliers. Leading players such as Dana, Federal-Mogul, ACDelco, and Meritor dominate through diverse portfolios, strong OEM ties, and robust aftermarket networks, leveraging innovation, quality, and service excellence to sustain multi-tier competitiveness across OEM and replacement segments.

Strategic Developments

- Dana Incorporated expanded its Spicer commercial vehicle product line in 2024, introducing advanced kingpin sets featuring enhanced materials and precision manufacturing that deliver extended service life and improved performance for heavy-duty applications.

- Stemco Products Inc. launched its Kaiser QwikKit kingpin installation system in 2024, featuring innovative design that eliminates reaming requirements, reduces installation time, and provides 2-3 times the service life compared to standard kingpin kits.

- Federal-Mogul (Tenneco) completed strategic restructuring in 2024 following its 2018 acquisition, optimizing its automotive components portfolio to strengthen market position in steering and suspension parts including kingpin assemblies across both OEM and aftermarket channels.

Market leaders are redefining the kingpin landscape through innovation, precision manufacturing, and integrated kits that boost performance and reduce ownership costs. Their strategies blend advanced materials, localized production, and smart partnerships to capture emerging market growth. With predictive maintenance technologies, subscription-based service models, and strong technical support, top players are shifting from product suppliers to long-term mobility partners, delivering reliability, efficiency, and value across global commercial vehicle fleets.

Companies Covered in Automotive Kingpin Market

- Dana Incorporated

- Federal-Mogul (Tenneco)

- ACDelco (General Motors)

- Meritor Inc.

- Stemco Products Inc.

- PE Automotive GmbH

- Ferdinand Bilstein GmbH + Co. KG

- JG Automotive

- Beyonz

- Kasuya Seiko

- Diesel Technic SE

- Belton Group

- LE.MA S.r.l.

- Mulberry Fabrications Limited

- Texspin

Frequently Asked Questions

The global automotive kingpin market is valued at US$ 4.9 billion in 2025, driven by expanding commercial vehicle production, infrastructure development, and increasing aftermarket replacement demand.

The market is primarily driven by expanding global logistics and transportation industries, massive infrastructure development programs, and rising aftermarket replacement demand from aging commercial vehicle fleets requiring regular kingpin maintenance.

The automotive kingpin market demonstrates a projected CAGR of 4.6%.

Key opportunities include emerging market penetration in Asia-Pacific where heavy truck markets grow, technology innovation in advanced materials, and aftermarket expansion through comprehensive kingpin kits delivering 2-3 times standard service life.

Market leaders include Dana Incorporated, Federal-Mogul (Tenneco), ACDelco (General Motors), Meritor Inc., Stemco Products Inc., and other global players.